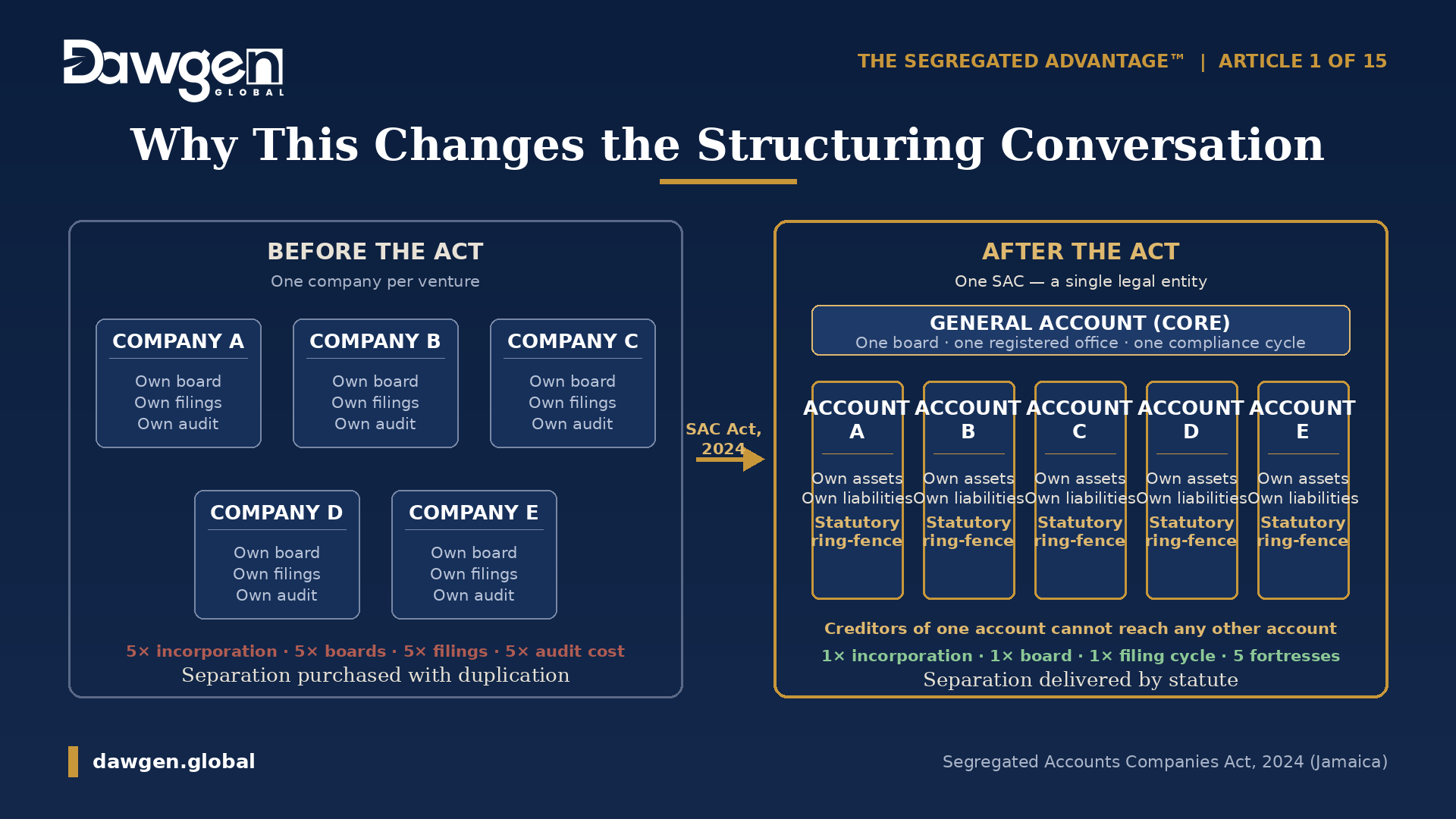

For as long as most Jamaican business owners can remember, there has been exactly one reliable way to stop trouble in one venture from sinking another: incorporate a separate company for each. A developer with four projects formed four companies. A fund manager with six portfolios wrestled with structures that the law never quite supported. A family with an operating business and an investment portfolio kept them apart with paperwork, prayer, and professional fees. Separation was possible — but it was always purchased with duplication: more incorporations, more boards, more filings, more audits, more cost.

The Segregated Accounts Companies Act, 2024 retires that trade-off. For the first time in Jamaican law, a single company can now establish any number of statutorily segregated accounts — each holding its own pool of assets and liabilities, each legally walled off from the creditors of every other account and of the company at large. One legal entity. Many fortresses. This article, the first in The Segregated Advantage™ series, explains what has changed, why it matters, and who should be paying attention.

The Gap Jamaica Just Closed

To appreciate the significance of the Act, start with what came before it. Jamaican law has always allowed parties to segregate assets contractually. A company could promise Lender A that its recourse was limited to Project A, and a Jamaican court would enforce that promise between the parties who made it. But contractual segregation has a fatal weakness: it binds only the people who signed it. A tort claimant, a tax authority, an unpaid supplier who never agreed to the limitation — none of them were bound. And in the moment that matters most, a winding up, the Companies Act treated the company’s assets as one undifferentiated pool available to its creditors as a whole.

The mismatch was felt most sharply in the funds industry. The Financial Services Commission requires that a collective investment scheme’s assets be held so that it is clear they belong to that fund and its investors — not to the manager, the custodian, or investors in other portfolios under the same umbrella. Yet no Jamaican corporate vehicle could actually deliver that separation as a matter of statute. Managers papered over the gap; the gap remained. Insurance programmes, multi-project developers and structured finance transactions faced the same structural ceiling: real segregation meant multiplying companies, and multiplying companies meant multiplying cost.

The Segregated Accounts Companies Act closes that gap at the level of statute rather than contract. The ring-fence no longer depends on who signed what. It is the law.

What Exactly Is a Segregated Accounts Company?

A segregated accounts company (SAC) is an ordinary company that registers under the Act and thereby acquires the power to create segregated accounts. Three building blocks define the structure.

The company itself. A SAC remains a single legal person. Creating a segregated account does not create a new company or a separate legal personality; it creates a statutorily protected compartment inside the existing one. The company continues to be governed by the Companies Act except where the SAC legislation deliberately overrides it.

The general account. Everything the company owns and owes that is not assigned to a segregated account sits in the general account — the “core,” in the language of cell-company jurisdictions. General creditors of the company can look only to the general account for payment.

The segregated accounts. Each segregated account is a distinct, identified pool of assets and liabilities, created by “linking” assets, rights, liabilities and obligations to it through written instruments or entries in the company’s records. A liability linked to Account A is a liability of Account A alone. A creditor of Account A has recourse to the assets of Account A — and to nothing else. The assets of Account B, Account C and the general account are, in the words of the regional model on which this legislation is built, absolutely and for all purposes protected from that creditor.

That is the entire premise, and it is worth pausing on how radical it is. Risk compartmentalisation that once required a holding company and a stable of subsidiaries can now be achieved inside one entity, with one board, one registered office, one annual compliance cycle — and a statutory wall between every compartment.

A Proven Caribbean Idea, Now in Jamaican Law

Jamaica did not invent this vehicle, and that is precisely its strength. The segregated accounts model was pioneered by Bermuda in 2000 and adopted by The Bahamas in 2004, and variants of it — protected cell companies, segregated portfolio companies — now underpin captive insurance, umbrella funds and structured finance platforms across the leading international financial centres. Two decades of regional practice have stress-tested the architecture: the registration gateways, the disclosure disciplines, the account-level solvency rules, the receivership remedies that allow one failed account to be wound down while every other account trades on undisturbed.

The Bahamas has already moved to its second generation, replacing its 2004 statute with the Segregated Accounts Companies Act, 2025, which adds incorporated segregated accounts, demergers and cross-border continuations. The direction of travel across the region is unmistakable — and Jamaica has now joined the family with a modern statute of its own.

The Act did not arrive in isolation. It is a core pillar of the legislative suite championed by the Jamaica International Financial Services Authority (JIFSA) to establish Jamaica as an international financial services centre — alongside the new Trusts Act, the Partnership (General) and Partnership (Limited) Acts, and the Trust and Corporate Services Providers Act, with limited liability company legislation to follow. A Joint Select Committee of Parliament has completed its review of the SAC Act with an explicit objective: expanding Jamaica’s financial services sector by attracting operators from outside Jamaica. Government commentary has singled out insurance, real estate development and investment management as the sectors the vehicle is expected to transform.

Why This Changes the Structuring Conversation

Consider how the arithmetic changes for three familiar Jamaican clients.

The developer. A firm running five developments once needed five special-purpose companies to keep a foundation failure or a contractor dispute in one project from contaminating the others. As a SAC, it runs five segregated accounts. Each project’s lenders take security over, and recourse to, that project’s account alone. Shared services between projects can be documented as internal transactions with full legal effect. The corporate overhead of four extra companies disappears.

The fund manager. An umbrella platform can link each portfolio to its own segregated account with its own share class, pay dividends account-by-account against account-level solvency tests, launch new strategies at the speed of documentation, and give the FSC exactly the segregation its rules have always demanded — statutorily, not cosmetically. If one strategy fails, the Act’s receivership mechanism contains the failure inside that account.

The family enterprise. Working alongside the new Trusts Act, a family SAC can hold the operating business in one account and the investment portfolio in another, with separately designated account owners, governance tailored account-by-account, and a register of account owners that — unlike the company’s own share register — is not open to public inspection.

Across all three, the same three dividends recur: statutory protection that survives insolvency, structural flexibility that moves at the speed of the business, and a step-change reduction in the cost of sophistication.

The Discipline That Comes With the Protection

Candour requires an equal emphasis on the other side of the bargain, because the SAC regime is demanding precisely where it should be. Registration is not automatic: it runs through the consent of the relevant regulator, which may attach conditions. The company’s name must announce its status, and every transaction must disclose that the counterparty is dealing with a SAC and identify which account is involved — a duty the regional model enforces with personal liability for directors who let it slip. Records must show, clearly and continuously, which assets and liabilities are linked to which account; financial statements are prepared account-by-account; and assets move between accounts only solvently and with the required consents. The ring-fence, in short, is only as strong as the discipline of the people operating it.

That is not a defect. It is the design. The statute trades protection for transparency, and businesses that operationalise the discipline — precise linking, faithful disclosure, well-drafted governing instruments — will find the courts and the market treating their walls as real. Businesses that treat the SAC as a label rather than a system will find the protection thinner than they hoped. The difference between the two is advice.

The Window Is Open

Every structural innovation has a first-mover phase, and Jamaica’s SAC regime is in it now. The Act is enacted; the regulations, forms and market practice are still taking shape; and there is, as yet, no crowd. The fund managers, insurers, developers and family enterprises that engage early — understanding the registration gateway, preparing governing instruments properly, building account-coded records from day one — will set the standard the rest of the market follows, and will hold structures their competitors spend years catching up to.

Over the coming weeks, The Segregated Advantage™ series will take each dimension of the regime in turn: the legal mechanics of the ring-fence, the registration pathway, the governing instrument, directors’ duties, receivership, and the sector playbooks for funds, insurance, real estate, structured finance and family wealth. The destination is a practical one — a readiness roadmap for any organisation weighing the structure.

Jamaica has given its businesses a tool the region’s leading financial centres have relied on for a quarter-century. The question is no longer whether statutory segregation is available. It is who will use it well, and first.

Frequently Asked Questions

What is a segregated accounts company (SAC) in Jamaica?

A SAC is a company registered under Jamaica’s Segregated Accounts Companies Act, 2024 that can create multiple segregated accounts — statutorily ring-fenced pools of assets and liabilities — inside a single legal entity. Creditors of one account cannot reach the assets of any other account or of the company generally.

Is a segregated account a separate company?

No. A SAC remains a single legal person; its segregated accounts are protected compartments within it, not separate companies. The compartmentalisation is achieved by statute operating on the company’s internal accounts rather than by incorporating subsidiaries.

How is a SAC different from simply using contracts to separate assets?

Contractual segregation binds only the parties who agree to it and gives no protection against third-party creditors on a winding up. The SAC Act makes the segregation statutory, so the ring-fence holds against creditors generally — including in insolvency, which is when it matters most.

Who should consider a SAC structure?

The vehicle is most immediately relevant to collective investment schemes and umbrella funds, insurers and captive programmes, real estate developers running multiple projects, issuers of series bonds and structured products, family enterprises structuring generational wealth, and multi-line businesses currently maintaining several companies purely for risk separation.

Is the SAC concept new to the Caribbean?

No — and that is a strength. Bermuda introduced the model in 2000 and The Bahamas in 2004 (modernised in 2025), and equivalents operate across the leading international financial centres. Jamaica’s Act brings a regionally proven architecture into domestic law as part of the JIFSA international financial services centre legislative suite.

How can Dawgen Global help?

Dawgen Global advises on SAC feasibility and structuring, the registration pathway and regulator engagement, governing-instrument design, account-level accounting architecture, audit and assurance over segregation integrity, and the tax analysis of accounts and distributions. Contact [email protected] to discuss whether a SAC fits your structure.

Next in the series: Article 2 — From Contract to Statute: The Asset Protection Gap Jamaica Just Closed.

This article is provided for general information and is not legal or tax advice. Specific structures should be verified against the current text of the Segregated Accounts Companies Act, 2024, its regulations, and the requirements of the relevant Jamaican regulators.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210