Every seasoned Jamaican transaction lawyer has drafted the clause. “The Lender’s recourse shall be limited to the assets of Project A and shall not extend to any other assets of the Borrower.” It is careful, it is customary, and — between the parties who signed it — it works. The uncomfortable truth the market lived with for decades is what happens the day the borrower fails. In that moment, the clause meets insolvency law, and insolvency law wins. The Segregated Accounts Companies Act, 2024 was written for that moment. This second instalment of The Segregated Advantage™ series examines precisely what contractual segregation could and could not do under Jamaican law, why the gap persisted for so long, and how the new statute closes it.

What a Contract Can Do

Start with a fair account of the old tools, because they were not nothing. Freedom of contract is a robust principle in Jamaican law, and a court will hold sophisticated parties to a limited-recourse bargain. A lender who agreed that its claim would be satisfied only from a defined asset pool cannot later sue for general recourse against the company; a fund investor who subscribed on terms confining his entitlement to Portfolio A’s assets is bound by those terms. Layered on top of contract, practitioners deployed trusts (declaring that particular assets were held for particular beneficiaries), security interests (giving a creditor priority over specific collateral), and the blunt but effective instrument of separate incorporation — one company per venture, so that the corporate veil itself did the segregating.

Each tool has real force, and each has a boundary. Contract binds only its parties. A trust protects only what was validly settled into it, demands genuine separation in fact, and sits awkwardly inside an operating company’s balance sheet. Security gives priority, not segregation — it ranks the secured creditor ahead of others against the collateral, but it does not stop the company’s other liabilities from existing against the same estate. And separate incorporation, the only complete answer, multiplies cost with every venture: another company, another board, another registered office, another audit, another annual return. The market’s toolkit, in short, could buy separation — but never cheaply, and never completely.

Where Contract Stops: The Involuntary Creditor and the Winding Up

The boundary shows itself in two places. The first is the creditor who never signed. A limited-recourse clause is invisible to the tort claimant injured on the company’s premises, to the statutory authority with an assessment, to the employee with an award, to the trade supplier whose terms said nothing about recourse. None of them agreed to look only to Project A, and nothing in the general law of Jamaica required them to. Their claims lay against the company — all of it.

The second, decisive boundary is the winding up. Under the Companies Act, 2004, a company in liquidation is a single estate. Its assets — however meticulously the management accounts divided them into “Project A” and “Project B” — form one pool, and its unsecured creditors share that pool pari passu, rateably, according to what they are owed. The liquidator’s duty runs to the general body of creditors, not to the private architecture of the company’s contracts. A limited-recourse clause remains enforceable against the counterparty who gave it — that counterparty cannot prove for more than the agreed pool would yield — but the clause does nothing to fence other creditors out of the pool. Internal segregation, in other words, dissolved at exactly the moment it was needed: the insolvency it was designed to survive.

The funds industry felt this most acutely, and it is worth restating the regulatory mismatch plainly. The Financial Services Commission’s framework for collective investment schemes requires a fund’s assets to be held so that it is clear they belong to that fund and its investors — not to the manager, the custodian, or anyone else. Yet no Jamaican corporate vehicle could make one portfolio’s assets legally unavailable to another portfolio’s creditors within the same company. The Companies Act distinguished investors from operators, but never investors in Portfolio A from investors in Portfolio B. Umbrella structures therefore carried a quiet, structural cross-contamination risk that documentation could narrow but never eliminate.

What the Statute Does Differently

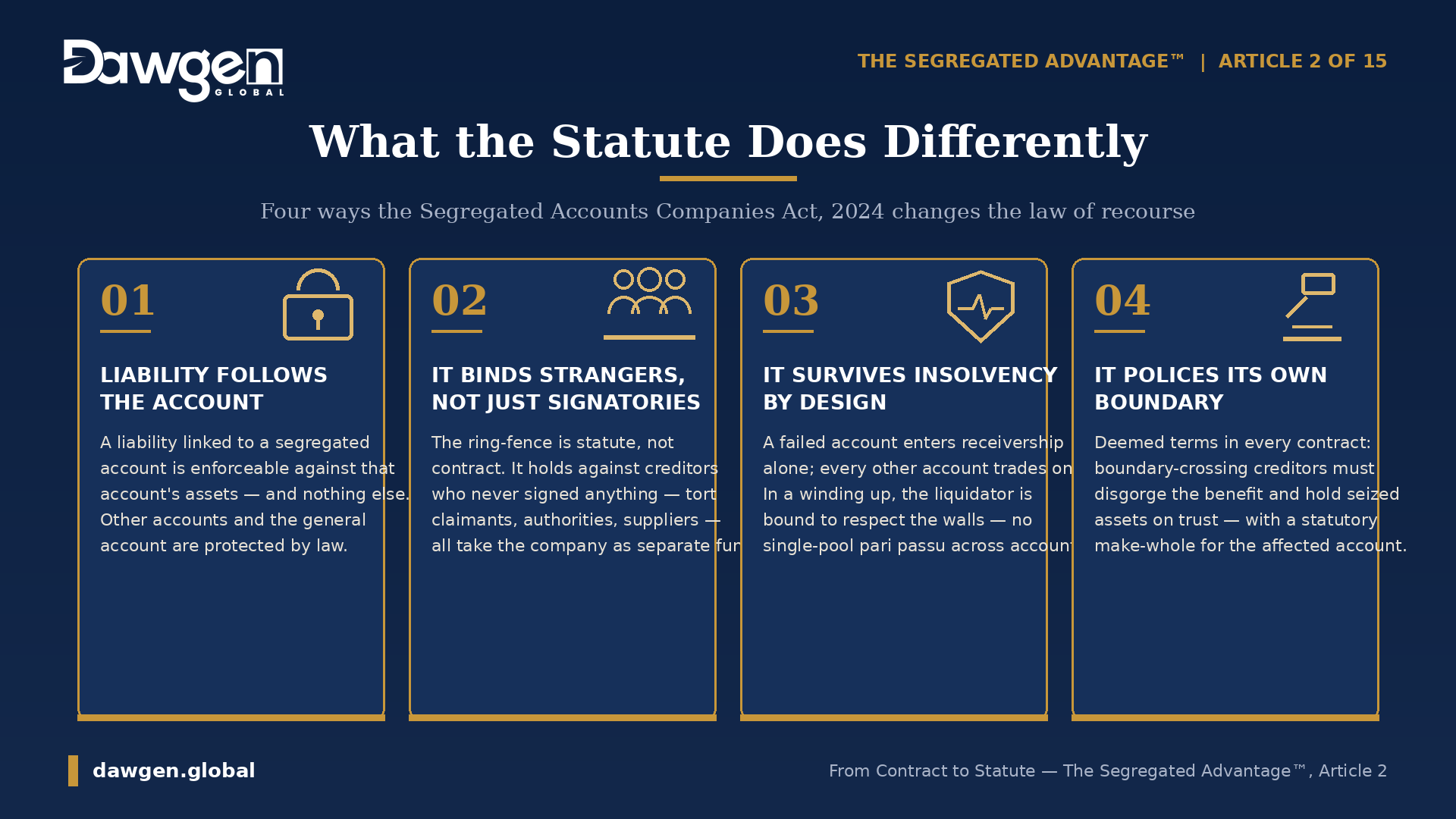

The Segregated Accounts Companies Act attacks the problem at its root: it changes the law of recourse itself, rather than asking contract to simulate it. Under the segregated accounts company (SAC) model, the change operates notwithstanding any other enactment or rule of law to the contrary — statutory language that is aimed directly at the pooling principle of the winding up.

Liability follows the account. A liability linked to a segregated account is a liability of that account alone. The creditor’s rights exist against the assets linked to that account — and against nothing else. Assets linked to other accounts, and the company’s general account, are absolutely and for all purposes protected from that creditor. Conversely, a liability not linked to any account is a claim on the general account only; a general creditor has no path into any segregated account.

It binds strangers, not just signatories. Because the ring-fence is statutory, it does not depend on who agreed to it. The involuntary creditor, the non-signing supplier, the claimant who never read the documents — all take the company as the statute constitutes it: a set of separate funds, each answerable only for its own obligations. The statute supplies the linkage rules, the priority rules on shortfall, and the presumptions for doubtful cases (an uncertain liability falls on the general account; an uncertain interest is treated as a creditor-side interest).

It survives insolvency by design. The regime’s insolvency provisions are built account-by-account. A distressed account is dealt with through a receivership confined to that account, whose costs are borne by that account alone, while every other account trades on. In a winding up of the company itself, the liquidator is statutorily bound to respect the segregation and must not apply one account’s assets to another account’s liabilities — and company-level insolvency is tested on the general account without reference to the segregated accounts at all. The single-estate, pari passu pooling that defeated contractual segregation simply does not apply across the accounts of a SAC.

It polices its own boundary. The model goes further than declaring the wall; it defends it. Every contract and governing instrument carries deemed terms that no party will attempt, anywhere, to make one account’s assets answer for another’s liability; a party who succeeds must disgorge the benefit; and a party who seizes such assets holds them on trust for the company, with a statutory make-whole restoring the affected account. For cross-border dealings — the one arena where a foreign court applying foreign insolvency law might not respect a Jamaican statute — prudent drafting still adds express limited-recourse and non-petition clauses. The difference is that these clauses now reinforce a statutory wall instead of substituting for a missing one.

The Same Journey Other Jurisdictions Made

Jamaica’s path from contract to statute is well-trodden. Bermuda made the crossing in 2000 and The Bahamas in 2004, for exactly the reasons rehearsed above: their insurance and funds industries had stretched contractual and common-law segregation to its limits, and the market demanded walls that would hold in insolvency. Two decades on, the segregated accounts company and its protected-cell cousins are standard infrastructure across the leading international financial centres, and The Bahamas has already modernised into a second-generation statute in 2025. When Jamaican counsel now advises that an account’s assets are beyond the reach of another account’s creditors, that advice stands on the same statutory footing as it would in Hamilton or Nassau — a point of real consequence for the international operators the JIFSA programme is designed to attract.

What This Means in Practice

For structures already living with the old constraints, the Act invites a fresh look. Umbrella funds relying on documentation to separate portfolios can now register vehicles in which the separation is law. Developers maintaining stables of single-purpose companies can weigh consolidation into one SAC with an account per project. Groups that accepted cross-contamination risk as a cost of doing business can price what it would take to eliminate it. And lenders and investors on the other side of these structures should recalibrate too: recourse analysis against a SAC begins with the question which account is this liability linked to — a question the transaction documents, and the company’s records, must now answer with precision.

One caution belongs in every conversation about this transition, and it will recur throughout this series: the statute gives businesses a wall, but businesses must build it straight. The ring-fence operates on what is properly linked, disclosed and recorded. Sloppy linkage, missing disclosures and commingled assets erode statutory protection just as surely as they eroded contractual protection — and the Act adds personal consequences for directors who let the discipline slip. The next articles take up that machinery in detail, beginning with the regional heritage of the cell company and then the registration pathway itself.

For now, the essential point stands on its own. For decades, asset segregation in Jamaica was a promise. It is now a property of the law. That is the gap the Segregated Accounts Companies Act closed — and it is the difference between a clause that persuades a court and a wall that stops a claim.

Frequently Asked Questions

Was asset segregation possible in Jamaica before the SAC Act?

Only partially. Parties could segregate assets by contract, trust, security or separate incorporation, and Jamaican courts enforced those arrangements between the parties. But contractual segregation did not bind third-party creditors, and on a winding up the company’s assets formed a single pool shared rateably among unsecured creditors.

Why does a limited-recourse clause fail in insolvency?

Because it binds only its signatories. A limited-recourse clause stops the counterparty who gave it from claiming beyond the agreed pool, but it cannot fence out creditors who never agreed to it — tort claimants, statutory authorities, employees, suppliers — and it does not displace the pari passu distribution rule that governs a liquidation.

How does the SAC Act change the position?

The Act makes segregation statutory. A liability linked to a segregated account can be enforced only against that account’s assets, other accounts and the general account are protected as a matter of law, the ring-fence binds creditors who never signed anything, and the insolvency regime — account-level receivership and a liquidator bound to respect the segregation — is built to preserve the walls precisely when the company fails.

Do limited-recourse clauses still matter in a SAC structure?

Yes, especially cross-border. Where a SAC contracts under foreign law or holds assets abroad, a foreign court may apply its own insolvency rules, so express limited-recourse and non-petition clauses remain best practice. Within Jamaica, the clauses now reinforce a statutory wall rather than standing in for one.

Does statutory segregation protect a badly run SAC?

Not reliably. The protection operates on assets and liabilities that are properly linked, disclosed and recorded. Poor record-keeping, undisclosed SAC status and commingling weaken the ring-fence and can expose directors personally. The statute supplies the wall; disciplined administration keeps it standing.

How can Dawgen Global help?

Dawgen Global advises on converting contractually segregated structures to SAC registration, recourse and linkage analysis for lenders and investors, governing-instrument and contract drafting, and the accounting and assurance architecture that keeps statutory protection intact. Contact [email protected] to discuss your structure.

Previously in the series: Article 1 — One Company, Many Fortresses: Why Jamaica’s Segregated Accounts Companies Act Changes Everything.

Next in the series: Article 3 — The Cell Company Comes Home: What Bermuda and The Bahamas Taught the Caribbean About Ring-Fencing Risk.

This article is provided for general information and is not legal or tax advice. Specific structures should be verified against the current text of the Segregated Accounts Companies Act, 2024, its regulations, and the requirements of the relevant Jamaican regulators.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210