New legal vehicles usually arrive as strangers. Jamaica’s segregated accounts company (SAC) arrives as family. The SAC that entered Jamaican law in 2024 is the newest member of a lineage that runs back a quarter-century through Nassau and Hamilton to the captive insurance boards of the mid-1990s — a lineage in which every major design choice in Jamaica’s statute was proposed, tested, litigated and refined somewhere else first. That heritage is not a footnote. It is one of the new regime’s most valuable assets, because Jamaica gets the benefit of every lesson the pioneers paid to learn. This third instalment of The Segregated Advantage™ series traces where the cell company came from, what two decades of regional practice taught its architects, and what that inheritance means for the operators Jamaica now hopes to attract.

Born in the Insurance Boardroom

The cell company was not invented by legislators; it was demanded by insurers. By the 1990s, the offshore captive insurance industry had built a thriving business around the “rent-a-captive”: a single licensed insurer whose capital and licence were shared by many unrelated clients, each running its own underwriting programme inside the vehicle. The economics were compelling — a client got captive-style risk financing without incorporating and capitalising a licensed company of its own — but the legal architecture was fragile in a familiar way. Each client’s programme was separated from the others by contract and bookkeeping, and nothing more. If one participant’s losses blew through its allocated funds, or the vehicle itself failed, every participant’s assets stood behind every participant’s liabilities. The industry was selling separation it could not legally guarantee.

Guernsey answered first, enacting the world’s inaugural protected cell company legislation in 1997 and giving the rent-a-captive what contract never could: statutory cells whose assets were legally unavailable to other cells’ creditors. The idea travelled at remarkable speed. Cayman adapted it for insurers as the segregated portfolio company; Delaware had already sketched a cousin in the series LLC; and jurisdiction after jurisdiction recognised that the concept solved problems far beyond insurance — umbrella funds, structured finance programmes, shipping fleets, any business of parallel risk pools inside one operator.

Bermuda’s Refinement: The Segregated Accounts Model

Bermuda’s contribution, after years of granting segregation through company-specific private acts, was the Segregated Accounts Companies Act 2000 — the statute that gives Jamaica’s vehicle its name and much of its grammar. Where the protected cell company reads as a structure of cells, Bermuda’s draftsmen built the model around accounting reality: assets and liabilities become part of a segregated account by being “linked” to it through instruments or entries in the company’s records, participants are classified as account owners (the equity side, holding interests under a governing instrument) or counterparties (the transactional side, contracting with a specific account), and the company remains, unambiguously, a single legal person whose internal walls are erected by statute rather than by multiplied incorporation. It was Bermuda’s model that hard-wired the disclosure discipline — tell every counterparty it is dealing with a segregated structure, and identify the account — and backed it with director accountability.

The Bahamas Adaptation: The Regulator at the Gate

The Bahamas took the Bermuda framework in 2004 and made a design decision that Caribbean policymakers have favoured ever since: it put the regulator at the gateway. A Bahamian company cannot simply elect into segregated status; it must obtain the written consent of its primary regulator — the securities regulator for funds and issuers, the insurance regulator for insurers, the central bank for relevant subsidiaries — and that regulator may attach conditions, require identity verification of account owners, and demand ongoing reporting through a licensed segregated accounts representative with a statutory duty to blow the whistle on insolvency risk or non-compliance. The Bahamian statute also elaborated the protective mesh around conversion of existing businesses: directors’ solvency declarations, creditor notice, supermajority stakeholder consents and a court-annulment remedy for dissenters. The message of the 2004 Act was that segregation is a privilege wrapped in supervision — a philosophy calibrated to protect the jurisdiction’s reputation as much as any individual creditor, and one that visibly shapes Jamaica’s approach.

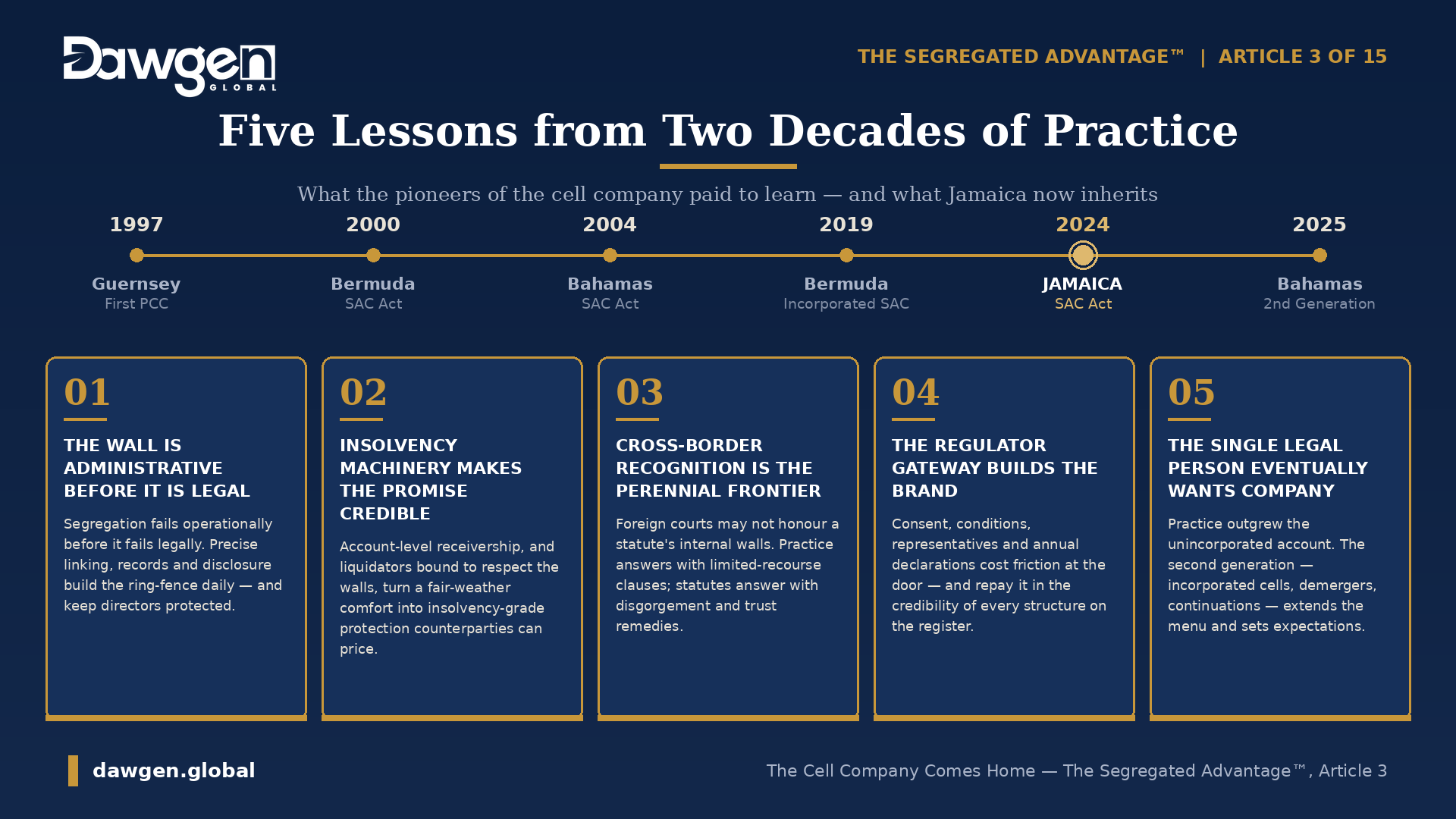

Five Lessons from Two Decades of Practice

The wall is administrative before it is legal. The earliest and most repeated lesson of cell practice is that segregation fails operationally before it fails legally. Cells whose assets were commingled, whose transactions never identified the cell, whose records could not show what was linked where — these were the structures that ended up in court, and the structures courts struggled to protect. Every mature statute has responded by hardening the record-keeping and disclosure duties and by making directors personally answerable for silence. The ring-fence, in other words, is built daily, by administration.

Insolvency machinery makes the promise credible. A wall matters only when someone is pressing against it. The model’s account-level receivership — a court-supervised workout of a single distressed account while the rest of the platform trades on, with the liquidator of the company itself statutorily bound to respect the segregation — is what converts the ring-fence from a fair-weather comfort into an insolvency-grade protection. Jurisdictions that skipped or skimped on this machinery found their vehicles discounted by sophisticated counterparties.

Cross-border recognition is the perennial frontier. A cell is a creature of its enacting statute, and the recurring anxiety of cell practice is the foreign court: a judge abroad, applying foreign insolvency law to assets situated there, is not automatically bound to honour the internal walls of a single foreign legal person. Practice answered with belt-and-braces drafting — express limited-recourse and non-petition clauses in every cross-border contract — and the statutes answered with anti-avoidance machinery: deemed contractual terms, disgorgement of benefits obtained by boundary-crossing, constructive trusts over seized assets, and make-whole mechanisms funded from the account that properly owed the liability. Jamaica’s regime inherits this entire defensive toolkit.

The regulator gateway builds the brand. Jurisdictions learned that the value of a segregated vehicle is reputational as much as legal: it is worth exactly what counterparties believe the jurisdiction’s supervision is worth. The consent-gated Caribbean model — regulator approval, conditions, representatives, annual compliance declarations — costs sponsors some friction at the door and repays it in the credibility of every structure on the register.

The single legal person eventually wants company. The most important recent lesson is structural. For all its elegance, the unincorporated account has limits that practice kept bumping into: an account cannot itself own assets in its own name, cannot contract as itself, and cannot always be exported, merged or continued independently. The answer was the incorporated cell. Bermuda legislated for incorporated segregated accounts companies in 2019, giving individual accounts separate legal personality within the family structure, and The Bahamas made the same leap in its Segregated Accounts Companies Act, 2025 — which also added de-registration and restoration mechanics, account-level liquidation, demergers, mergers and cross-regime continuations. The second generation does not replace the classic SAC; it extends the menu, and it signals where regional expectations now sit.

What Jamaica Inherits

Arriving twenty-five years into this story, Jamaica’s Segregated Accounts Companies Act, 2024 starts where the pioneers finished. The linking architecture, the account owner and counterparty classifications, the governing instrument, the disclosure discipline, the regulator gateway, the account-level insolvency machinery, the anti-avoidance mesh — all of it enters Jamaican law pre-tested by two decades of Caribbean practice, and regional commentary on the Jamaican framework already discusses both classic SACs and incorporated segregated accounts. For the international fund managers, insurers and structurers that the JIFSA programme is built to attract, this familiarity is the point: counsel in London, New York or Toronto reviewing a Jamaican SAC will recognise the model immediately, price it accordingly, and advise on it with confidence.

Jamaica also brings something to the lineage that the classic offshore centres cannot: scale and substance. A jurisdiction of nearly three million people, a deep professional services bench, a functioning domestic capital market, and real operating businesses — developers, conglomerates, credit unions, family groups — that can use the vehicle at home rather than merely booking it offshore. The cell company was born to serve non-residents. In Jamaica, for the first time in the Caribbean at this scale, it will also serve the domestic economy that hosts it. That is what it means for the cell company to come home.

The next article in the series turns from heritage to machinery, opening up the ring-fence itself: how linking works, what the general account does, how priority runs when an account cannot pay, and exactly what a creditor of a Jamaican SAC can — and cannot — reach.

Frequently Asked Questions

Where did the cell company concept originate?

In the offshore captive insurance industry. Rent-a-captive structures of the early 1990s separated clients’ programmes only by contract and bookkeeping, and Guernsey answered the resulting risk with the world’s first protected cell company legislation in 1997. Bermuda’s Segregated Accounts Companies Act 2000 and The Bahamas’ 2004 Act adapted and refined the model for the wider Caribbean.

What is the difference between a protected cell company and a segregated accounts company?

They are variants of the same idea — statutorily ring-fenced pools inside one entity. The segregated accounts model, which Jamaica follows, is built around “linking” assets and liabilities to accounts through instruments and records, and classifies participants as account owners (under a governing instrument) or counterparties (under contracts), all within a single legal person.

What is an incorporated segregated account?

A second-generation development in which individual accounts are given separate legal personality within the family structure — legislated by Bermuda in 2019 and adopted by The Bahamas in its 2025 Act. Incorporated accounts can hold assets in their own name, be wound up individually, and in some regimes be demerged or continued as standalone companies. Regional commentary on Jamaica’s framework discusses both classic and incorporated forms.

Have cell structures survived insolvency in practice?

The mature statutes were built precisely for that test: account-level receivership, liquidators bound to respect the segregation, and anti-avoidance terms against boundary-crossing creditors. The consistent lesson of regional practice is that well-administered structures hold, while commingled and poorly documented ones invite challenge — which is why disclosure and record-keeping duties carry personal consequences for directors.

Why does this history matter to a Jamaican business?

Because Jamaica’s Act inherits a pre-tested design that international counsel and counterparties already understand, which lowers the cost and friction of using Jamaican structures in cross-border transactions — and because the lessons of that history, especially administrative discipline, tell Jamaican boards exactly what keeping the protection requires.

How can Dawgen Global help?

Dawgen Global brings regional benchmark knowledge of the Bermuda and Bahamas frameworks to Jamaican SAC structuring — feasibility, registration, governing instruments, account-level accounting and assurance, and cross-border documentation. Contact [email protected] to discuss your structure.

Next in the series: Article 4 — Inside the Ring-Fence: How Statutory Segregation Actually Works in a SAC.

This article is provided for general information and is not legal or tax advice. Specific structures should be verified against the current text of the Segregated Accounts Companies Act, 2024, its regulations, and the requirements of the relevant Jamaican regulators.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210