The first three articles in this series established why Jamaica’s Segregated Accounts Companies Act, 2024 matters: it converts asset segregation from a contractual promise into a property of the law, drawing on a quarter-century of Caribbean cell-company practice. This article — the first of the series’ second arc, on the rules themselves — moves from why to how. If you are a director who will operate a segregated accounts company (SAC), a lender or investor who will face one across a transaction, or an adviser who will document one, the mechanics below are the working knowledge the vehicle demands. As throughout this series, the detailed machinery is drawn from the regional model on which Jamaica’s statute is built, with the usual counsel to verify execution-critical points against the Jamaican text and regulations.

The Anatomy: One Person, Many Funds

Begin with the anatomy, because every rule that follows operates on it. A SAC is one legal person with, in effect, many purses. The first element is the company itself — an ordinary company that has registered under the Act, still governed by general company law except where the SAC statute overrides it. The second is the general account: everything the company owns and owes that is not assigned to any segregated account. The third is the segregated accounts themselves: separate, identified pools of assets and liabilities, each ring-fenced from the others and from the general account. Two declarations in the statute anchor the whole design. Establishing a segregated account does not create a separate legal person — the walls are internal. And yet each account’s linked assets are deemed to be held by the company as a separate fund that is not part of the general account and not part of the company’s own assets — language that gives the internal walls external, proprietary force.

Linking: The Connective Tissue

Nothing in a SAC belongs to an account by vague intention; it belongs by linking. An asset, right, contribution, liability or obligation becomes part of a segregated account in one of two ways: through an instrument in writing — a governing instrument or a contract — that identifies it as pertaining to that account, or through an entry or notation in the company’s records made in respect of a transaction. Linking is therefore both a legal act and a bookkeeping act, and the statute treats the bookkeeping with corresponding seriousness. The company must maintain records, in accordance with generally accepted accounting principles, that clearly show for each account the capital, securities, reserves, assets, liabilities, income, expenses and distributions linked to it; must record every transaction; and must keep a general account of everything unlinked. The directors carry a personal, continuing duty to keep each account’s assets and liabilities separate and separately identifiable from every other account’s and from the general account’s.

The model does allow one deliberate exception to the one-account principle: an asset or liability may be apportioned across two or more accounts (or an account and the general account), provided the instrument effecting the apportionment clearly states the extent to which it is linked to each. What the regime never forgives is ambiguity by neglect — and, as we shall see, it resolves genuine ambiguity with presumptions that are deliberately uncomfortable for the careless.

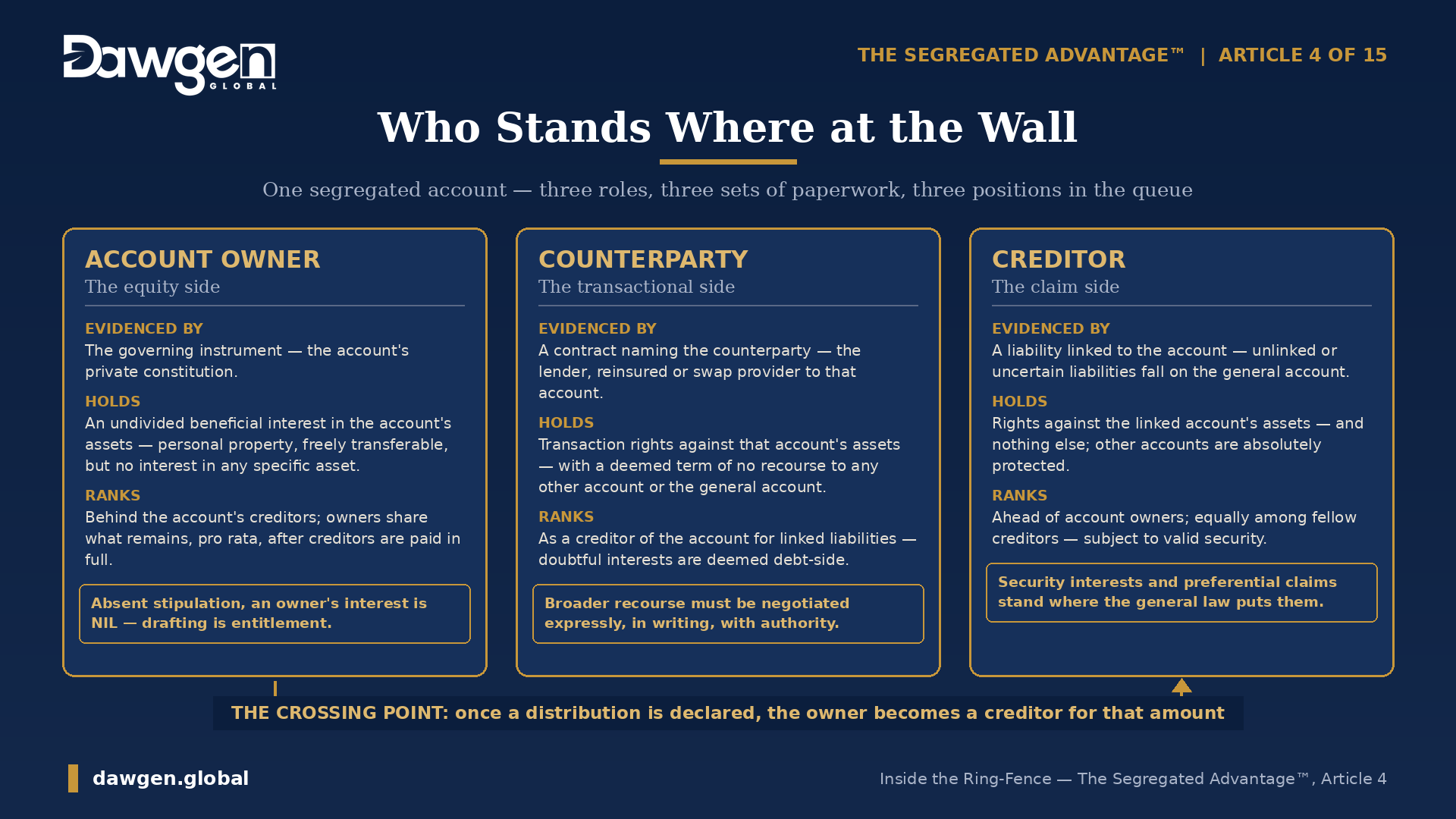

Who Stands Where: Owners, Counterparties, Creditors

Three roles populate the world of a segregated account, and the paperwork differs for each. The account owner is the equity-side participant: the registered holder of shares linked to the account, or a person identified as an owner in the governing instrument or the company’s records. Owners hold an undivided beneficial interest in the account’s assets — personal property, freely transferable unless restricted — but, absent contrary agreement, no interest in any specific asset. Their rights, interests and obligations must be evidenced in a governing instrument, the account’s private constitution, which can allocate voting rights, management arrangements, classes of holdings and much else, and which fills any silence with the statute’s extensive default rules. One default deserves a professional’s respect: an owner takes the interest stipulated for him, and absent stipulation or other compelling indication, the extent of his interest is nil. In this regime, drafting is entitlement.

The counterparty is the transactional participant: any party (other than the company itself) to a transaction under which assets or liabilities are linked to an account — the lender to Project A, the reinsured of Programme B, the swap provider to Series C. Counterparty rights are evidenced in contracts, which must name the counterparty and, unless otherwise agreed, are treated as governed by domestic law with submission to the domestic courts. The creditor, finally, is anyone to whom a liability linked to the account (or to the general account) is owed. The categories are kept deliberately distinct — an account owner, in that capacity, is neither counterparty nor creditor — with one important crossing point: the moment an owner becomes entitled to a declared payment, distribution or dividend, the statute elevates him to creditor status for that amount, with all of a creditor’s remedies. Until declaration, owners stand behind the account’s creditors; after it, they stand among them for what was declared.

The Law of Recourse: What a Claimant Can Reach

Now the core operating rule, which Article 2 introduced and can here be stated with precision. A liability linked to a segregated account extends only to, and its claimant may have recourse only to, the assets linked to that account — not to any other account, and not to the general account. A liability that arises otherwise than in respect of a particular account is a claim on the general account alone. General shareholders have no rights to any segregated account’s assets by reason only of being general shareholders, and the general account’s assets are the only assets available for unlinked liabilities.

The statute then does something quietly powerful: it writes the wall into every deal automatically. Unless the parties expressly agree otherwise in a properly authorised writing, every contract pertaining to a transaction is deemed to contain a statement that the counterparty’s rights do not extend, and the counterparty has no recourse, to assets linked to any other account or to the general account. A counterparty who wants broader recourse must negotiate for it, in writing, executed by parties with authority over the accounts being exposed. And for the cases the paperwork failed to settle, two presumptions apply: where it is reasonably uncertain whether an interest is that of a counterparty or an account owner, it is deemed a counterparty (debt-side) interest; and where a liability is not linked to a particular account, or its linkage is reasonably uncertain, it is deemed a liability of the general account. Both presumptions protect outsiders — and both punish sloppy linking, the first by ranking the doubtful interest ahead of owners, the second by throwing the doubtful liability onto the company’s own core.

When an Account Cannot Pay: The Priority Ladder

Solvency in a SAC is tested account by account: an account is solvent if it can pay its own liabilities (excluding obligations to owners in that capacity) as they fall due, and the company is solvent if the general account can do the same without reference to the segregated accounts. When a particular account cannot pay everything, the statute supplies the ladder. Valid security interests over the account’s assets, and any valid preferential claims, stand where the general law puts them. Below that, the order and priority of rights is determined by the governing instrument and the contracts pertaining to the account — the parties’ own architecture governs first. Whatever ambiguity remains is resolved by three default rungs: creditors rank ahead of account owners; creditors rank equally among themselves; and account owners rank equally among themselves. On termination of an account (or dissolution of the company), once the account’s creditors are paid, remaining linked property goes pro rata to its owners — and if there are none, it falls into the general account.

Dealing Across the Walls

The walls are firm, but the regime is not a prison: assets and dealings can cross, on stated conditions. Transfers between accounts are consent-and-solvency events. Moving an asset out of a segregated account — to another account or to the general account — requires the written consent of all that account’s owners and of the counterparties who are creditors with linked claims, and the account must remain solvent after the transfer. Moving assets from the general account into a segregated account requires either that the general account remains solvent taking the transfer into account, or the written concurrence of all shareholders and general-account creditors. Transfers in breach are voidable by the court at the instance of an affected party, subject always to bona fide purchasers for value without notice. An asset validly transferred ceases to be linked to its source account on the date of transfer — linking is dynamic, not tattooed.

More strikingly, a SAC may transact with itself. The company acting for the general account may deal with itself acting for an account; accounts may deal with each other — services shared between project accounts, funding advanced from one series to another — and the transaction has the same legal effect as if made with a third party, including voidability under any rule of law that would have applied to a genuine third-party dealing. Owners, counterparties and receivers are given standing to pursue an account’s rights of action. Officers may act on both sides of such internal dealings despite the evident conflict, but the safe harbour is conditional: written disclosure of the interest, plus authorisation in the governing instrument or the written consent of a majority of the account’s owners. Internal disputes between accounts may be referred to court or arbitration — and if the representatives of the competing accounts cannot agree on the forum, court it is.

The Mesh: How the Statute Defends Its Own Walls

Finally, the enforcement mesh — the layer that makes the ring-fence more than a polite request. Every contract and governing instrument is deemed to include three terms unless expressly excluded in writing: that no party will seek, in any proceedings or by any means, anywhere, to make one account’s assets answer for a liability not attributable to that account; that a party who nevertheless succeeds must pay the company a sum equal to the benefit obtained; and that a party who seizes, attaches or executes against such assets holds them, or their proceeds, on trust for the company, kept separate and identifiable. Sums recovered are applied to compensate the affected account. And where assets are lost to wrongful execution and cannot otherwise be restored, the company’s auditor — acting as expert, not arbitrator — certifies the value lost, and the company must restore that value to the affected account out of the account that properly owed the liability, in priority to all other claims against it. The trust-law backdrop is deliberately curated: the Act generally excludes trust rules from the regime, but expressly preserves tracing in law and equity, and constructive-trust remedies, where one account’s assets are commingled with another’s or with the general account. Commingle, in other words, and equity follows the money.

Taken together, these mechanics reward exactly one operating style: precise linkage at the moment of every transaction, account identification in every document, records that can answer “whose asset, whose liability” instantly, and governing instruments drafted as if entitlement depends on them — because it does. The next article turns to the door of the regime itself: who may register a SAC, which regulator holds the key, and how the application process runs from incorporation to certificate.

Frequently Asked Questions

What does “linked” mean in a segregated accounts company?

Linking is how an asset, right, liability or obligation becomes part of a particular segregated account — either through a written instrument (a governing instrument or contract) identifying it as pertaining to that account, or through an entry in the company’s records. Everything in the regime, from creditor recourse to receivership, operates on what is linked to which account.

What is the general account of a SAC?

The general account — the “core” — holds all assets and liabilities not linked to any segregated account. It is the only pool available to creditors whose claims are not linked to an account, and company-level solvency is tested on the general account alone, without reference to the segregated accounts.

What is the difference between an account owner and a counterparty?

An account owner is the equity-side participant, holding an undivided beneficial interest under a governing instrument. A counterparty is the transactional participant — a lender, reinsured or swap provider — whose rights are evidenced in contracts with recourse to that account’s assets. An owner in that capacity is not a creditor, except that once a distribution is declared the owner becomes a creditor of the account for that amount.

Who gets paid first when a segregated account is insolvent?

Valid security interests and preferential claims come first; then the priority set by the governing instrument and contracts; and any remaining ambiguity is resolved by default rules — creditors ahead of account owners, creditors ranking equally among themselves, and owners ranking equally among themselves.

Can assets be moved between segregated accounts?

Yes, but only solvently and consensually: transfers out of an account require the written consent of all its owners and linked creditors and continued solvency of the account; transfers from the general account require its continued solvency or unanimous stakeholder concurrence. Transfers in breach are voidable by the court, protecting bona fide purchasers.

What happens if a creditor attacks the wrong account’s assets?

Deemed contractual terms make the boundary self-enforcing: a party who makes one account’s assets answer for another’s liability must disgorge the benefit, holds seized assets on trust for the company, and the affected account is made whole — with the auditor certifying the value lost — out of the account that properly owed the liability, in priority to other claims.

How can Dawgen Global help?

Dawgen Global designs the operational side of the ring-fence: linkage protocols, account-coded ledger architecture, governing-instrument and contract drafting support, recourse analysis for lenders, and assurance over segregation integrity. Contact [email protected] to discuss your structure.

Previously in the series: Article 3 — The Cell Company Comes Home: What Bermuda and The Bahamas Taught the Caribbean About Ring-Fencing Risk.

Next in the series: Article 5 — The Gateway: Regulators, Consents and the Path to SAC Registration in Jamaica.

This article is provided for general information and is not legal or tax advice. Specific structures should be verified against the current text of the Segregated Accounts Companies Act, 2024, its regulations, and the requirements of the relevant Jamaican regulators.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210