Why the region’s growth constraint is not a shortage of viable enterprises — but a shortage of appropriate capital structure

Walk into any boardroom from Kingston to Port of Spain to Bridgetown and you will hear a version of the same conversation. The business is sound. The market opportunity is real. The asset — the hotel wing, the logistics hub, the solar installation, the commercial property — would generate returns for twenty years or more. And yet the expansion is deferred, scaled down, or financed in a way that quietly plants the seeds of the next crisis: a five-year bank facility against a twenty-year asset, secured at punishing collateral ratios, refinanced under pressure, repriced at every renewal.

We have taught ourselves to call this a financing environment. It is more accurately described as a capital structure problem — and it is, in our view at Dawgen Global, the single most underdiagnosed constraint on Caribbean enterprise. The region does not lack viable companies. It lacks instruments that match the way Caribbean companies actually create value: patiently, through long-life assets that appreciate.

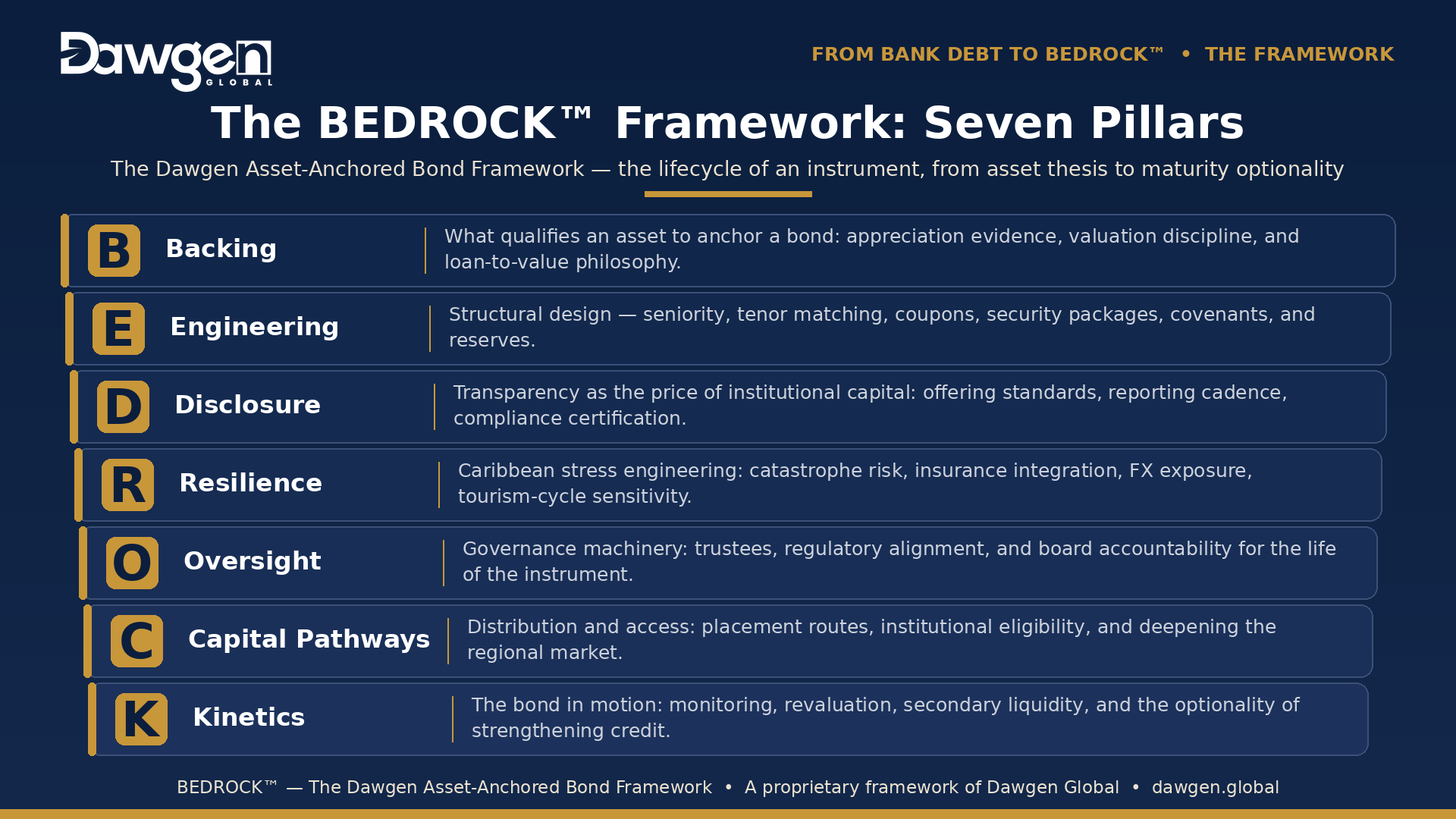

This article opens a twelve-part series advocating a specific remedy: the corporate bond — properly engineered, transparently disclosed, and secured by capital-appreciating assets — as the missing middle of Caribbean corporate finance. The series is built around BEDROCK™, the Dawgen Asset-Anchored Bond Framework: a seven-pillar doctrine for the design, issuance, governance, and lifecycle management of asset-anchored bonds in Jamaica and the wider Caribbean. Before we introduce the framework, we must be honest about the problem it exists to solve.

The Three Failures of Caribbean Capital Structure

Failure One: The Bank-Debt Trap

Caribbean corporate balance sheets are dominated by commercial bank credit to a degree that would be considered structurally unhealthy in deeper capital markets. Bank lending has genuine virtues — relationship knowledge, speed, flexibility — but as the dominant or sole source of growth capital it imposes three systematic distortions.

- Tenor mismatch — a bank typically lends five to seven years against assets whose economic life runs twenty to forty. The borrower must therefore refinance the same asset two, three, four times over its life — and every refinancing is a roll of the dice on prevailing rates, prevailing liquidity, and prevailing bank appetite. The risk is not that the asset fails; it is that the calendar arrives at the wrong moment.

- Collateral overweight — regional bank lending is collateral-heavy, with security demanded at conservative loan-to-value ratios and valued at forced-sale discounts. The paradox is acute: the enterprise pledges an appreciating asset, yet is advanced capital as though the asset were destined to decay. Equity that should be funding growth sits trapped as excess collateral.

- Repricing exposure — floating-rate bank facilities transmit every monetary tightening cycle directly into corporate debt service, while renewal events hand the lender periodic repricing power. The borrower carries the system’s interest rate risk on a balance sheet never designed to absorb it.

None of this is a criticism of Caribbean banks, which lend within their own regulatory and funding constraints. Banks fund themselves short; they must lend accordingly. The criticism is of a corporate finance culture that treats the bank facility as the default instrument for purposes it was never designed to serve.

Failure Two: The Dilution Dilemma

The textbook answer to over-leverage is equity. In the Caribbean, the equity answer collides with two realities. The first is market depth: regional equity markets, for all their genuine progress, remain thin relative to the growth capital requirements of the corporate sector, with concentrated liquidity and episodic appetite for new issues. The second is ownership economics: for the family-held and founder-led enterprises that dominate the regional economy, equity issuance at thin-market valuations means surrendering permanent ownership at the worst possible price to solve a temporary funding problem.

The result is a familiar regional pattern: enterprises that refuse dilution and therefore stay small, or enterprises that accept dilution and spend a generation regretting the terms. Between expensive equity and mismatched bank debt, the Caribbean balance sheet is squeezed from both sides.

Failure Three: The Shallow Middle

Between bank credit and public equity lies the instrument that deep capital markets use to fund exactly the asset profile the Caribbean possesses in abundance: the corporate bond. In developed markets, long-life infrastructure, hospitality real estate, energy installations, and commercial property are routinely funded by long-tenor secured debt placed with institutional investors. In the Caribbean, the corporate bond market — though growing, and though served by capable exchanges and an expanding regulatory architecture — remains shallow relative to both the equity side of the market and the scale of regional funding need.

This is the missing middle. And the most important fact about it is that the capital to fill it already exists — and is already in the region.

The Capital Is Already Here

The Caribbean is home to substantial pools of long-dated institutional capital: pension funds carrying retirement liabilities measured in decades, and insurance companies — life insurers above all — holding obligations that stretch a generation into the future. The defining problem of these institutions is not a shortage of money. It is a shortage of assets that match their liabilities: long-duration, income-generating, secured instruments that out-yield government paper without taking on equity volatility.

In the absence of such instruments, regional institutional portfolios concentrate in sovereign debt, bank deposits, and a thin set of listed equities — a concentration that regulators across the region have repeatedly observed. The institutional investor is structurally hungry for precisely the instrument the Caribbean enterprise is structurally failing to issue.

On one side of the regional balance sheet: enterprises with twenty-year assets funded by five-year debt. On the other: institutions with thirty-year liabilities funded by short-dated paper. The asset-anchored bond is the bridge the Caribbean has not finished building.

This is not a speculative claim about hypothetical demand. It is the basic arithmetic of asset-liability matching, and it is why the advocacy in this series is directed at three audiences simultaneously: issuers, who need to understand what institutional capital requires of them; institutional investors, who need a doctrine for underwriting asset-anchored regional credit; and policymakers, regulators, and exchanges, whose market infrastructure decisions determine how quickly the bridge gets built.

The Appreciating-Asset Thesis: Inverting the Credit Curve

Here we arrive at the intellectual core of this series — the proposition that distinguishes BEDROCK™ from conventional bond commentary.

Conventional credit doctrine treats collateral as static downside protection. The security package exists for the day things go wrong; in the meantime, the lender’s model assumes the collateral depreciates, amortises, or at best holds value. The credit is strongest on the day of issuance and is presumed to require de-risking — through amortisation — from that day forward.

The appreciating-asset thesis inverts this premise. When a bond is secured on an asset class with a credible, evidenced appreciation pathway — prime tourism real estate in supply-constrained coastal corridors, logistics infrastructure serving growing trade flows, renewable energy installations with long-term offtake economics, well-located commercial property — the credit mathematics run in the opposite direction. The asset appreciates while the debt is constant or declining. Loan-to-value improves with every year. The security cover compounds. The instrument is, in credit terms, stronger in year ten than it was at issuance.

We call this the inverted credit curve, and its implications cascade through every element of bond design:

- Tenor logic — if the credit strengthens over time, long tenor stops being a concession the investor grants and becomes a feature the investor wants — more years of holding a de-risking, income-paying secured instrument.

- Pricing logic — an instrument whose collateral cover demonstrably improves merits a different spread conversation than one priced on static-collateral assumptions — particularly where revaluation mechanics make the improvement visible and contractual.

- Lifecycle logic — appreciating collateral creates expanding headroom that disciplined structures can convert into pricing step-downs, partial releases, or refinancing capacity for the next phase of growth — turning the balance sheet itself into a renewable source of expansion capital.

Two honesty clauses belong in this doctrine from the outset, because advocacy without discipline is salesmanship. First: appreciation must be evidenced, not asserted. Not every asset appreciates, and no asset appreciates in a straight line; the thesis demands independent valuation, conservative haircuts, and stress-tested assumptions — disciplines this series will set out in full. Second: appreciation does not pay coupons. Cash flow services debt; collateral protects it. The asset-anchored bond is a cash-flow instrument with a strengthening security package, never a speculation on asset prices dressed as credit.

A Tale of Two Balance Sheets

Consider Blue Harbour Resorts Ltd., a stylised Caribbean hospitality company constructed for illustration. Blue Harbour owns a beachfront property and intends a US$40 million expansion — a new wing whose economic life comfortably exceeds thirty years, on land in a corridor where comparable assets have historically appreciated.

On the conventional path, Blue Harbour negotiates a seven-year bank facility for a portion of the cost, pledges the entire property at a conservative loan-to-value against a forced-sale valuation, funds the balance from shareholders, and accepts a floating rate. Over the asset’s first twenty-one years, the company will refinance three times. Each renewal is exposure to that year’s rates, that year’s bank liquidity, and that year’s sector sentiment — and hospitality being cyclical, at least one renewal will likely fall in a difficult year. The asset will outperform; the balance sheet will wobble anyway. The wobble is manufactured entirely by the structure.

On the BEDROCK™ path, Blue Harbour issues a fifteen-year senior secured bond to regional institutional investors: secured on the expanded property at a disciplined issuance loan-to-value, carrying a fixed coupon matched to institutional appetite, governed by a trustee, supported by a debt service reserve and assigned insurances, with independent revaluation every three years and covenant mechanics that recognise improving collateral cover. The pension fund holding the paper has acquired what its liability profile craves: fifteen years of secured, fixed income from an instrument whose loan-to-value is engineered to improve. Blue Harbour has acquired what its asset deserves: capital that matches its life, at a cost fixed at issuance, with no refinancing event until the asset is mature and the credit at its strongest.

Same company. Same asset. Same market. The difference is not creditworthiness — it is capital structure. That is the entire argument of this series, compressed into a single comparison.

Blue Harbour Resorts Ltd. is a fictional enterprise created for illustrative purposes. All figures are invented for the model and do not reference any actual company or engagement.

Introducing BEDROCK™: The Dawgen Asset-Anchored Bond Framework

Advocacy needs architecture. It is not enough to say the Caribbean should issue more bonds; the region’s history with poorly structured credit — corporate and sovereign alike — demands that the case be made for well-built instruments, with the engineering specified. BEDROCK™ is Dawgen Global’s answer: a seven-pillar doctrine covering the full life of an asset-anchored bond, from the asset thesis through structural design, disclosure, resilience, governance, distribution, and post-issuance management.

Each pillar receives a dedicated article in this series — a complete doctrine treatment with a Caribbean lens — followed by three articles on mobilising institutional capital, deepening the regional bond market, and sector applications. The series concludes with the BEDROCK™ Bond Readiness Index, a structured diagnostic that allows an enterprise to assess, dimension by dimension, how far it stands from issuance-grade — and what the path to bond-readiness looks like.

A note on lineage: readers of our work will recognise the seven-pillar architecture as the Dawgen Global house style, sharing its structural DNA with the DIAMOND™ Framework. They will also recognise a deliberate relationship with TRANSCEND™, our restructuring doctrine. The relationship is sequential and practical: many Caribbean balance sheets must be repaired before they can be anchored — legacy bank debt restructured, security positions untangled, capital structures repositioned. TRANSCEND™ repairs the balance sheet; BEDROCK™ funds the growth. The two frameworks will meet repeatedly across this series, most directly in the Engineering and Resilience pillars.

Defined Terms

This series builds a precise vocabulary. Three definitions anchor everything that follows:

Asset-anchored bond. A corporate bond secured on a specific capital-appreciating asset or asset portfolio, engineered so that tenor matches asset life and structured so that the security package strengthens as the asset appreciates.

Appreciating collateral. Security comprising assets with a credible, independently evidenced appreciation pathway — such that the bond’s loan-to-value ratio improves over the life of the instrument rather than relying solely on amortisation.

The inverted credit curve. The defining property of a well-built asset-anchored bond: credit quality that strengthens over tenor, because appreciating collateral compounds security cover while the debt is constant or declining — the inverse of conventional static-collateral credit logic.

The Series Ahead

The Caribbean’s capital structure problem is solvable, and the solution does not require importing capital, inventing institutions, or waiting on anyone. The assets exist. The institutional demand exists. The exchanges and regulatory architecture exist and are maturing. What the region needs is doctrine: a disciplined, Caribbean-built standard for how asset-anchored bonds should be backed, engineered, disclosed, stress-proofed, governed, distributed, and managed. That is what BEDROCK™ exists to provide, and what the next eleven articles will set out — pillar by pillar, beginning next week with Backing: why appreciating assets change the credit mathematics.

The question this opening article leaves with every Caribbean board is the one that should precede every financing decision: is your capital structure an accident of what was available — or an act of design? Growth built on mismatched debt is growth on rented foundations. The region’s next chapter should be built on bedrock.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning. Enquiries: [email protected].

Next in the series: Article 2 — Backing: Why Appreciating Assets Change the Credit Mathematics. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210