In Article 3 of this series, I argued that the Caribbean firms that will compound earnings over the next decade are the ones rebuilding their workforce around AI fluency. This week, the series turns from the internal to the external — from talent and productivity to the most important structural opportunity now opening in front of our region.

Chapter 2 of the IDB’s 2026 Macroeconomic Report is devoted entirely to a single subject: critical minerals. The chapter’s title is *A Window of Opportunity*, and the choice of metaphor is exact. Windows close. The Caribbean’s exposure to the global energy transition is meaningful, but the time in which our region can position itself to capture durable value from it is finite. Boards that treat critical minerals as “someone else’s story” will miss the supply-chain, services, and capital-flow opportunities that ripple into the Caribbean. Boards that engage seriously with it now will be making the most consequential capital allocation decisions of the next decade.

The energy transition’s mineral physics

Most boardroom discussions of the energy transition focus on the demand side: solar, wind, electric vehicles, batteries, grid modernisation. The IDB’s chapter focuses on the supply side, and the picture it paints is striking.

Every electric vehicle requires meaningful quantities of lithium, nickel, cobalt, and graphite for its battery, and copper and aluminium for its wiring and motors. Every wind turbine requires rare earth elements. Every solar installation requires copper, silver, and specialised alloys. Every digital and defence system depends on gallium, germanium, and rare earths. With limited substitutes, modest recycling rates, and long project lead times, the global stock of these inputs cannot scale up quickly. The IDB documents that:

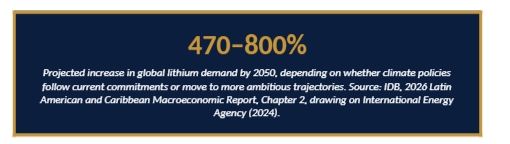

- Lithium: global lithium demand is projected to rise between 470% and 800% by 2050;

- Copper: demand is projected to expand substantially through 2050 to support electrification of grids, vehicles, and buildings — copper is widely produced but systemically critical, and the IDB notes that prices have already responded to rising demand expectations;

- Nickel: demand growth is sharp through the 2030s, with global supply concentrated in a small group of countries headed by Indonesia;

- Rare earths: demand is being driven by wind turbines, electric motors, and digital systems — and global production and especially refining is dominated by China, creating a structural concentration risk that importing economies are now actively trying to diversify away from.

Two features of these demand projections matter for Caribbean boards. First, the projections are consistent across most credible forecasters even when they disagree on the exact numbers — directionally, demand is rising sharply for the next two decades. Second, supply is highly concentrated in a small number of countries with a small number of operators, which means importing economies (the EU, Japan, the United States) are paying premia to diversify their supply base. The Caribbean and the wider Latin American region holds meaningful reserves. The window the IDB describes is the window in which our region can position itself to be part of that diversification.

The Caribbean’s position in the critical minerals map

The Caribbean is not the lithium epicentre — that distinction belongs to the so-called Lithium Triangle of Argentina, Bolivia, and Chile. We are not the rare-earths centre — Brazil holds reserves the IDB values at roughly twice its GDP. But our exposure is real, multi-layered, and in several specific cases substantial. The IDB’s regional production tables explicitly include Jamaica, Guyana, Suriname, and Venezuela in bauxite and aluminium, and the broader macroeconomic spillovers reach every CARICOM economy. Here is the map:

| Country | Position in critical-minerals chain | Direct exposure | Spillover exposure |

| Jamaica | Bauxite & alumina (long-standing major producer) | Aluminium upstream input demand; export prices; royalty regime under review | Service sector, port logistics, financial services to mining counterparties |

| Guyana | Oil & adjacent extraction; emerging mining services hub | Sovereign-fund design; capital project pipeline; FX absorption capacity | Regional service-sector contracts; cross-border banking & professional services |

| Suriname | Oil production from 2028; gold; bauxite history | Pre-production fiscal framework decisions; institutional buildout in progress | Service-sector positioning ahead of 2028 production start |

| Trinidad & Tobago | Hydrocarbon mature producer; transition exposure | Energy-sector capital re-allocation; pivot to lower-emission portfolios | Energy-services firms repositioning toward critical-minerals adjacencies |

| Wider CARICOM | Service & financial hubs; tourism economies | Limited direct extraction; meaningful financial-services exposure | Capital flows into the region; talent, banking, legal, audit demand |

Source: Dawgen Global analysis based on IDB 2026 Macroeconomic Report, IMF country projections, and regional production data.

Three observations land hardest in this table for me.

First, Jamaica’s bauxite-and-alumina position is far more strategically relevant in 2026 than it was in 2016. The energy transition’s demand for aluminium — for EV chassis, transmission lines, structural components — is rising in lockstep with the broader electrification push. Jamaica’s long-standing producers are operating in a market with a meaningfully better demand outlook than the one for which their last major capital plans were sized.

Second, Guyana’s projected 23% GDP growth in 2026 — and Suriname’s projected 29% in 2028 when oil production is expected to commence — is creating capital project pipelines, professional services demand, and cross-border financial flows on a scale the region has not seen in a generation. Both economies are actively building the institutional infrastructure (sovereign wealth funds, fiscal frameworks, environmental regulation) that determine whether resource booms produce durable development or boom-and-bust cycles. The decisions being made now will shape the next twenty years.

Third, the wider CARICOM exposure — through professional services, banking, legal, audit, insurance, and logistics — is meaningful and easy to underestimate. Capital does not stay where it is extracted. It flows through regional service hubs. Caribbean enterprises that position themselves now to serve this flow will compound earnings from it for the next decade.

What history teaches: why “resource window” is not the same as “resource boom”

The IDB’s chapter is unusually direct about the historical pattern. The headline observation is that previous commodity cycles in Latin America and the Caribbean produced “short-lived booms, limited spillovers, and modest productivity gains.” The reason was not the geology. It was the institutional infrastructure surrounding the geology.

Three patterns repeat in the resource-cycle literature, and the IDB chapter walks through each. First, governments tax cyclically rather than counter-cyclically — they spend the windfall during the boom and run into fiscal stress during the bust. Second, the boom amplifies institutional weaknesses rather than building them — rent-seeking and corruption flourish in environments with weak governance, which is why the IDB notes that resource booms can “weaken incentives for institutional development.” Third, the boom does not generate durable productivity gains in the wider economy because forward and backward linkages — to local services, local manufacturing, and local human capital — never get built. The mining or oil sector becomes an enclave.

Each of these failures is preventable. Each is a function of choices made early in the cycle, not of geology or commodity prices. The IDB’s chapter argues, and I agree, that translating mineral wealth into durable development is conditional on six interlocking institutional preconditions. Caribbean boards making capital allocation decisions today should evaluate every counterparty country, every project, and every contract against this checklist.

The six institutional preconditions

Here is the framework the IDB chapter constructs, restated in operating terms for Caribbean boards:

| Precondition | What “good” looks like at country and firm level |

| 1. Predictable fiscal frameworks | Royalty rules, tax stability clauses, and ring-fencing provisions that survive electoral cycles. Investors price uncertainty harshly; predictable modest fiscal terms attract more durable capital than aggressive but unstable terms. |

| 2. Environmental governance | Robust permitting, monitoring, and enforcement at basin level. Importing markets, particularly the EU, increasingly differentiate supply chains by environmental performance — and pay premia for verified low-impact production. |

| 3. Social licence | Genuine, continuous engagement with affected communities; transparent benefit-sharing; predictable royalty distribution to producing regions; independent grievance mechanisms. The IDB calls social licence “a first-order determinant” of whether mineral potential translates into actual production. |

| 4. Regulatory clarity | Streamlined permitting that does not weaken safeguards. Coordinated environmental, fiscal, and labour regulation. Investors value clarity over speed. |

| 5. Infrastructure | Port capacity, road and rail to extraction sites, reliable power supply, water management, and grid resilience. Caribbean infrastructure gaps are real but addressable; multilaterals are actively financing exactly this category of project. |

| 6. Human capital | Geological, mining-engineering, and environmental-management expertise at scale. The Caribbean’s talent gap here is significant; partnerships with experienced operators and structured technology transfer are non-optional. |

Source: Dawgen Global synthesis of IDB 2026 Macroeconomic Report, Chapter 2.

These six preconditions are the difference between a resource window that produces durable growth and a resource boom that produces a hangover. They are also — and this is the central practical point of this article — assessable by any board with the right advisory support. Country risk on each precondition is now publicly tracked, regulatory frameworks are documented, environmental performance data are increasingly transparent, and institutional capacity can be measured. The board that runs every regional capital allocation decision through this six-question checklist will systematically avoid the projects that will destroy capital and identify the ones that will compound it.

What this means for Caribbean boards

Critical minerals reach the Caribbean firm through five operating channels. Each one carries specific board-level decisions. I want to walk through them precisely, because the discussion in our region tends to default to one or two of these channels and miss the others.

Channel 1 — Direct extraction and production. For Jamaican producers in bauxite and alumina, for Guyanese and Surinamese operators across the extractive sector, and for Trinidadian energy companies repositioning toward lower-emission portfolios, the operating decisions are immediate: how to size capital expenditure against price volatility, how to negotiate long-term offtake contracts that capture the demand premium, how to manage royalty regimes likely to be revisited as governments re-evaluate fiscal frameworks. Boards in this category should be commissioning detailed scenario analyses against the IDB’s projected demand bands — not against single-point forecasts.

Channel 2 — Supply-chain participation. Most Caribbean firms will not extract minerals directly. Many will participate in the supply chain — through logistics, port operations, equipment supply, environmental services, technical consulting, legal and audit, financial services, and insurance. The window for positioning here is now, not later. The firms that build credentials and capacity in 2026-2027 will be the ones contracted on the major projects that come to commercial scale in 2028-2030.

Channel 3 — M&A optionality. Capital is being deployed across the region’s extractive and adjacent sectors at a pace that has not been seen in decades. Caribbean firms with strong regional positions in services, logistics, or infrastructure are increasingly attractive acquisition targets for international operators looking to enter the region. The flip side is also true: well-capitalised Caribbean firms have a window to acquire complementary capabilities — technical expertise, geological assessment, environmental engineering — that would otherwise take years to build organically.

Channel 4 — Tax and structural exposure. Mineral and energy royalty regimes across the region are being actively reviewed. Jurisdictions are competing on stability terms. Cross-border flows are increasing in scale and complexity. The tax planning around extractive contracts, ring-fencing provisions, transfer pricing exposure, and incentive-regime mapping is now substantially more consequential than it was three years ago — and a meaningful source of preserved value for firms that engage with it proactively.

Channel 5 — ESG assurance readiness. Importing markets — particularly the European Union — are tightening sustainability standards on imported critical minerals and processed metals. Producers and supply-chain participants who can demonstrate verified environmental and social performance increasingly capture premium pricing. Caribbean firms preparing to participate in this supply chain need ESG assurance frameworks in place now, not in 2028 when the contract is being negotiated. The cost of being assurance-ready ahead of demand is meaningfully lower than the cost of scrambling to retrofit.

Five questions every Caribbean board with critical-minerals exposure should be asking

If this article does its work, every Caribbean board with material direct or indirect critical-minerals exposure will spend a meaningful portion of its next strategic session on five questions:

- Has our capital plan been stress-tested against the IDB’s projected demand bands? If our 2026 capital plan was built before the IDB’s projected demand band for our specific minerals or adjacencies became visible, we are sizing our investments to the wrong scenario.

- Have we assessed each jurisdiction we operate in against the six institutional preconditions? If we have customer or supplier concentrations in jurisdictions that score poorly on these dimensions, our durable-value exposure is meaningfully different from our current valuation assumptions.

- Are we, or should we be, an M&A counterparty in the next 36 months? If the answer is no — for either side of this question — we are leaving optionality on the table.

- Is our tax structure aligned to where extractive and adjacent contracts are heading? If our tax positioning still reflects 2022 thinking, we are likely either over-paying or under-protected against regulatory change.

- Are we ESG assurance-ready for the supply-chain demands of 2028? If the answer is “we’ll handle it when a customer asks,” we are already behind. Customers will ask, and they will pay premia to firms that can answer immediately.

How Dawgen Global supports this work

Critical minerals and the broader resource window represent the most multi-disciplinary opportunity in the entire IDB report. Action across the five operating channels described above engages, in my view, more of our practice areas simultaneously than any other theme in this series.

- M&A: for the M&A optionality work — buy-side and sell-side advisory, valuations, due diligence, and post-merger integration across regional extractive, services, and adjacent sectors.

- Tax Advisory: for the structural and ring-fencing work, royalty regime navigation, transfer pricing exposure, and incentive-regime mapping across multiple Caribbean jurisdictions.

- Risk Management: for systematic country-risk assessment against the six institutional preconditions, supply-chain risk diagnostics, and counterparty risk frameworks.

- Audit & Assurance: for ESG assurance, including the firm’s DESGAF™ ESG Internal Audit framework and the existing 12-article ESG Internal Audit Series, which together provide the assurance infrastructure exporters and supply-chain participants now need.

- Business Advisory: for the strategic positioning work, scenario planning against the IDB’s projected demand bands, and capital allocation framework design.

The firm’s pan-Caribbean footprint across more than fifteen territories means we operate where the work is happening — in Kingston, Port of Spain, Bridgetown, Georgetown, Paramaribo, and across the wider CARICOM bloc. The integrated multidisciplinary model — where M&A, Tax, Risk, and Audit work in coordinated teams on the same engagement — is built precisely for opportunities of this scale and complexity.

Next week

Article 5 turns to a different kind of question: how Caribbean firms should stress-test their balance sheets for the next global risk-off episode. The IDB’s Chapter 3 quantifies what happens to Latin American and Caribbean economies when global risk sentiment shifts — and the effects, the report notes, are sizable, asymmetric across countries, and especially pronounced for commodity exporters with weaker policy frameworks. The Article 4 reader is, by definition, exposed to exactly these dynamics. The Article 5 reader will need to know how to prepare for them.

Closing

The window the IDB describes is real. The lithium demand growth band of 470% to 800% is not a forecast outlier — it is the centre of the credible projection range. The energy transition is not a theme that may or may not happen. It is happening, it is increasing demand for the minerals our region holds, and it is creating capital flows and institutional decisions that will shape Caribbean development for the next twenty years.

It is also a window. Resource cycles in Latin America and the Caribbean have historically failed to translate mineral wealth into durable development not because the geology was wrong but because the institutional preconditions were absent. The Caribbean firms that engage seriously with this opportunity now — with rigorous capital planning, with deliberate jurisdictional diligence, with ESG-assurance readiness, with the right tax structure, and with the right M&A posture — will be the ones that compound earnings from it for the next decade. The Caribbean firms that wait for it to land on their balance sheet without preparation will see other regions and other operators capture the value.

Critical minerals are a window, not a guarantee. Caribbean boards that stress-test their exposure to this window now — supply-chain, capital, regulatory — will capture far more value than those who watch.

— ◆ —

About the author

Dr. Dawkins Brown is the Executive Chairman and Founder of Dawgen Global, an independent, integrated multidisciplinary professional services firm headquartered in Kingston, Jamaica, and operating across more than fifteen Caribbean territories.

Continue the conversation

Subscribe to The Caribbean Advisory Brief on the Dawgen Global LinkedIn page for the next instalment.

Direct enquiries: [email protected] | +1-876-929-3670 | dawgen.global

Source

Ayres, J. and Juvenal, L. (2026). Resilience and Growth Prospects in a Shifting Global Economy: 2026 Latin American and Caribbean Macroeconomic Report. Inter-American Development Bank, Chapter 2: Critical Minerals — A Window of Opportunity, pp. 17–43.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements