The Caribbean concentrates more risk per square mile than almost anywhere on earth — and most businesses meet it with an unread policy and a hope. Risk is not weather. It is a portfolio, and portfolios can be engineered.

The Problem, Lived

“Desmond” owns a twenty-four-room boutique hotel and restaurant on the coast of St. Vincent — fifteen years of steady building, the kind of place guests return to by name. Last season, a strengthening storm grazed the island. The damage was real but survivable: a section of roof, water through two floors, six weeks closed for repairs. It was the weeks after the storm that did the deeper damage — because that is when Desmond finally read his insurance policy.

The education came in four installments. His building was insured for the figure set when he bought it, years of construction-cost inflation ago — and because that sum now represented barely more than half the true rebuilding cost, the policy’s average clause scaled his payout down in the same proportion: insured for roughly half, paid roughly half, even on a partial loss. Second, his deductible was not the modest figure in his memory but a percentage of the sum insured, triggered at catastrophe scale. Third — the wound that bled longest — he carried no business interruption cover at all, so the six revenue-less weeks of payroll, loan payments and cancelled bookings, the largest single loss of the entire event, were entirely his. And fourth, he could not honestly say who his insurance was designed by, because it had never been designed: it had been quoted, by whoever was cheapest the year he asked.

Down the coast, a competitor with visibly similar damage reopened in three weeks, staff paid throughout, her interruption cover bridging the darkness. Same storm. Different portfolios. Desmond had treated insurance as a bill and risk as fate — and the storm, indifferent to both attitudes, simply audited them.

Why It Happens Here

Caribbean business risk is structurally concentrated: hurricane and flood exposure, single-island operations where one event hits premises, staff, customers and suppliers simultaneously, hard-currency costs against soft-currency revenue, and dependence on a handful of key customers or one key person (Article 15 already made that case). Correlation is the regional signature — everything goes wrong together — which is precisely the condition insurance exists for, and precisely where casual insurance fails worst.

The failure patterns repeat across the region. Insurance is bought as a commodity on price, not designed as protection. Sums insured are set once and never walked up the escalator of construction inflation and exchange rates — so underinsurance accumulates silently, year by year, until the average clause presents the bill. Business interruption — the cover that protects the cash flow this whole series has been defending — is skipped as a luxury or sized by guesswork. Policies go unread until claim day, when exclusions and definitions (wind versus flood, storm surge versus rain) stage their ambush. And the priorities run backwards: owners insure the routine losses they could comfortably absorb while leaving catastrophic gaps yawning. All of this against a hardening regional market where cover is dearer and tighter every renewal — which makes engineering the risk, not just buying the paper, the only strategy left standing.

| The Underinsurance Escalator

Here is the clause that quietly halves claims across the region. If your property would cost $10 to rebuild today but is insured for $6, the average clause treats you as self-insuring the difference — and pays roughly 60 cents of every dollar of any claim, even a small one. You do not need a total loss to be punished for underinsurance; the penalty rides on every claim. Construction costs and exchange rates move every year. A sum insured that has not been professionally revisited in two years is not a number. It is a countdown. |

Why Generic Advice Fails

Imported guidance assumes another insurance universe: deep competitive markets, government backstop programs, cheap reinsurance, and hazard maps drawn for other people’s geography. Enterprise risk-management frameworks, meanwhile, arrive sized for corporations with risk officers. What the regional owner actually needs sits between the two: an owner-level method for engineering the risk portfolio — with genuine actuarial rigor applied to the insurance layer, because an insurance policy is ultimately a contract made of numbers, and in most claims that go wrong, it was the numbers, not the storm, that were wrong first.

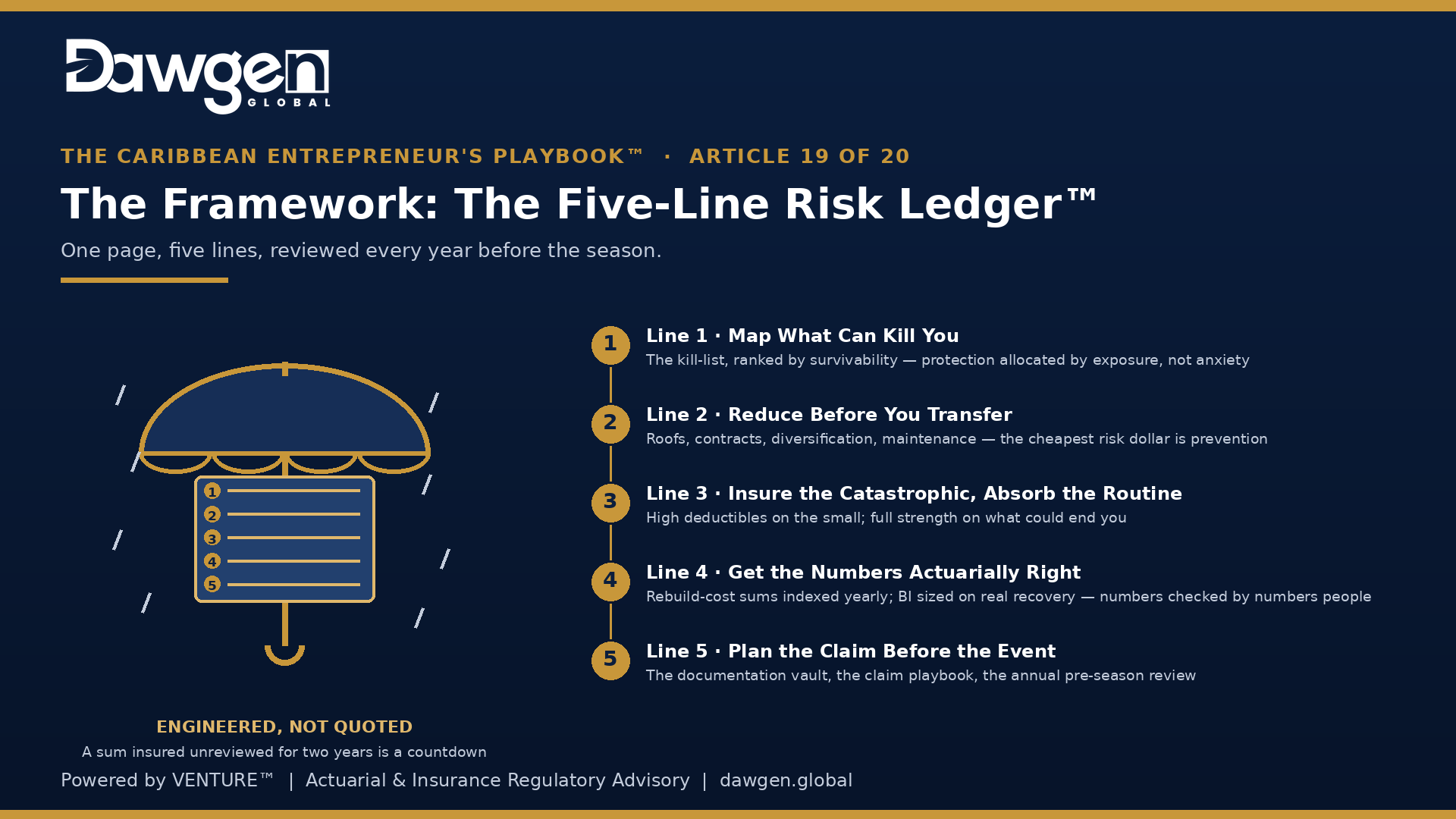

The Framework: The Five-Line Risk Ledger™, Step by Step

One page, five lines, reviewed every year before the season:

- Line 1 · Map What Can Kill You — List every risk that could end the business — not inconvenience it, end it — and rank by survivability, not probability: the storm, the fire, the loss of the key person, the top customer’s departure, the liability claim, the FX shock. Most owners have never written this list, which is why their protection budget is distributed by anxiety rather than by exposure. The kill-list is the foundation; everything else in the ledger allocates effort against it.

- Line 2 · Reduce Before You Transfer — The cheapest risk dollar is the one spent on prevention. Before buying more cover, engineer the exposure down: the roof brought to standard, the fire suppression serviced, the contracts that shift liability where it belongs, the customer and supplier diversification Articles 12 and 16 built, the maintenance that happens on schedule rather than after failure. Insurers increasingly price your discipline — documented risk reduction buys premium as well as safety — and some risks, once reduced, stop needing transfer at all.

- Line 3 · Insure the Catastrophic, Absorb the Routine — Turn the portfolio right side up. Take deductibles high on the small, frequent, survivable losses — you were always going to pay for the fender-benders eventually — and spend the premium saved on full-strength protection against the kill-list. The test for every policy is one question: does this protect me from something that could end us? Self-insure the inconveniences. Never self-insure the hurricane by accident, which is exactly what underinsurance is.

- Line 4 · Get the Numbers Actuarially Right — This is where claims are won years in advance. Sums insured reset to current rebuilding cost — professionally valued, then indexed annually against construction inflation and the exchange rate. Business interruption sized on honest arithmetic: your true fixed costs and margin, over a realistic indemnity period — rebuilding and recovering a market takes twelve to eighteen months, not the three a guess buys. Deductible structures, average clauses, and the wind-flood-surge definitions read and understood before they are tested. An insurance contract is a set of numbers wearing a legal coat; have the numbers checked by people whose profession is numbers.

- Line 5 · Plan the Claim Before the Event — Claims are won with evidence and speed. Build the documentation vault now — dated photographs and video of premises and equipment, inventories, valuations — stored off-site or in the cloud (Article 18’s backups, wearing a second hat). Know your broker and insurer as people before you meet them as a claimant. Write the one-page claim playbook: who notifies, who documents, who mitigates, in what order. And put the annual review on the calendar before each season — because the only good time to discover a gap is when the sky is clear.

The Framework in Action: A Worked Scenario

The following scenario is a fictional composite created for this series to illustrate the framework. It does not depict any actual business or client of the firm.

Desmond rebuilds the portfolio the way he rebuilt the roof — properly, this time. A professional valuation resets his sums insured to true rebuilding cost, indexed annually. Business interruption cover is added, sized on his actual fixed costs across a realistic recovery period. The deductible structure is reorganized: higher on the routine, full strength against the catastrophic. The roof itself is brought above code — and the documented upgrade earns back part of the premium the better cover costs. The vault is assembled in a weekend: every room, every system, photographed and filed off-island.

Two seasons later, another storm grazes the coast — comparable damage, incomparable aftermath. In this illustration, the claim, supported by dated evidence and correct numbers, settles without the war of attrition he remembered; the interruption cover carries payroll and the loan through the dark weeks, and the hotel reopens in three — his neighbor’s timeline, now his own. The storm was the same kind of storm. What changed was that this time, someone had done the arithmetic before the wind did. Desmond keeps the two claim files in the same drawer, he says, as a before-and-after photograph of the only renovation that mattered.

Self-Diagnostic: Would Your Portfolio Survive the Audit?

One point for every “no”:

- Do you have a written kill-list — the risks that could end the business — reviewed this year?

- Have your sums insured been professionally revalued against current rebuilding costs within two years?

- Do you carry business interruption cover sized on real fixed costs and a realistic recovery period?

- Could you state your catastrophe deductible in dollars — and explain your policy’s average clause?

- Does a documentation vault and one-page claim playbook exist, off-site, updated this year?

Two or more points means your protection is a hope wearing a premium. The storm does not read policies — but the claims adjuster will, line by line, and so should someone on your side, first.

When to Call In Help

This is the discipline where sitting alone across from the insurance market costs the most, because the market’s side of the table employs actuaries and yours, usually, does not. Bring in professional support when sums insured, interruption cover or deductibles have never been independently reviewed; when a claim has gone badly and the renewal is approaching; when premiums are hardening and you need to know what to engineer rather than simply absorb; or when your scale opens more sophisticated doors — structured programmes, parametric covers, and beyond. Dawgen Global’s Actuarial & Insurance Regulatory Advisory Division exists to put that rigor on the policyholder’s side of the table — where, in this region, it has always been rarest and needed most.

| REQUEST A RISK & INSURANCE PORTFOLIO REVIEW

Dawgen Global’s Actuarial & Insurance Regulatory Advisory Division delivers the Five-Line Risk Ledger™ as a working engagement: your kill-list mapped, reduction priorities engineered, sums insured and business interruption professionally sized and indexed, deductibles and clauses stress-tested before any storm does it for you, and your claim playbook and documentation vault built — actuarial rigor, on your side of the table. Contact us today, before the season does, to request your review. 📩 [email protected] | 📞 876-929-3670 / 876-665-5926 | 🇺🇸 855-354-2447 | 🌐 dawgen.global GET THE FULL PLAYBOOK This is Article 19 of The Caribbean Entrepreneur’s Playbook™ — 20 problems, 20 how-to frameworks, one system. Pre-register at dawgen.global to receive the complete Playbook e-book on release, free. |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210