Pillar K of the BEDROCK™ Framework: monitoring, revaluation, secondary liquidity, and the optionality of a strengthening credit — the bond in motion

There is a temptation, once a bond is placed, to regard the work as finished. The asset was selected, the structure engineered, the disclosures made, the resilience built, the governance installed, the capital raised. The documents are signed and filed. For a conventional bond, treated as a static obligation that simply runs to maturity, that filing is nearly the end of the story.

For an asset-anchored bond, it is the beginning. The entire premise of the BEDROCK™ Framework — the inverted credit curve of Article 2 — is that the instrument changes over its life: the asset appreciates, the loan-to-value (LTV) declines, the security cover compounds, the credit strengthens year by year. A credit that strengthens is not a document to be filed; it is a position to be managed. Pillar K — Kinetics — is the doctrine of that management: the discipline of the bond in motion, from the day after issuance to the day of maturity.

Kinetics completes the framework, and it does so by closing the loop the first pillar opened. Backing made a claim — that the asset would strengthen the credit over time. Kinetics is where that claim is monitored, measured, recognised, rewarded, and ultimately recycled into the next phase of growth. This article sets out the lifecycle doctrine across its four domains — monitoring, revaluation, secondary liquidity, and maturity optionality — and then steps back to synthesise the whole framework, because Pillar K is the last of the seven, and the place to see how all of them work together.

Monitoring: The Credit Under Continuous Watch

A managed credit is a watched credit. The monitoring architecture of Pillar K turns the disclosure regime of Article 4 and the covenant ladder of Article 3 into a living surveillance system — not to burden a performing issuer, but to ensure that the first sign of deterioration is seen early, while responses are still cheap and options still open.

Three layers compose the monitoring discipline. The first is covenant tracking: the systematic testing of the LTV and debt service coverage ratio (DSCR) maintenance covenants at each measurement date, against the certificates the issuer provides and the trustee administers. The second is asset performance monitoring: watching the operating reality behind the covenants — occupancy, rate, volume, the income drivers that ultimately determine whether the appreciation thesis is holding. The third is early-warning indicators: the leading signals that precede a covenant breach — a softening trend before it crosses a threshold, a counterparty under strain, an insurance renewal in doubt — so that the structure responds to the approach of trouble rather than only to its arrival. The doctrine’s principle is that surveillance exists to make problems small: a deterioration caught at the early-warning stage is a conversation; the same deterioration caught at default is a crisis.

Revaluation: Making the Strengthening Credit Visible

Revaluation is the mechanism at the heart of Kinetics, because it is where the inverted credit curve stops being a thesis and becomes a measured fact. The Backing pillar required revaluation on a contractual cadence — the doctrine’s default every three years, with event-driven revaluations for material changes. Pillar K is where those revaluations do their work.

Each revaluation performs three functions. It measures: an independent valuer reassesses the backing asset, and the recalculated LTV records, in hard numbers, whether the appreciation thesis is holding — the gold line of the Article 2 chart, plotted point by point across the bond’s life. It informs: the revaluation report flows to the trustee and the investors (Pillar D), converting the strengthening credit from the issuer’s private knowledge into the market’s shared record. And it triggers: the recalculated LTV drives the consequences the structure was engineered to deliver — the step-down coupon that rewards an improving ratio, the partial security release that returns over-collateralisation, or, if the ratio has deteriorated, the springing cash sweep or coupon step-up that protects the investor. Revaluation is the moment the structure acts on what has actually happened, rather than on what was assumed at issuance.

A credit that strengthens is not a document to be filed; it is a position to be managed. Revaluation is the moment the structure acts on what has actually happened.

Secondary Liquidity: The Instrument in the Market

A bond’s value to its holder depends not only on its coupon and its safety but on the holder’s ability to sell it if circumstances change. Secondary liquidity — the capacity to trade the instrument after issuance — is therefore part of what the investor buys, and a dimension Pillar K manages deliberately rather than leaving to chance.

The doctrine recognises that liquidity is built, not assumed. The placement route of Article 7 shapes it: a listed bond trades more readily than a privately placed one. The disclosure regime of Article 4 supports it: a buyer in the secondary market can underwrite the credit only because the continuing-disclosure standard lets them see it. And the revaluation record builds it: an instrument with a documented history of a strengthening credit and clean compliance certificates is one a secondary buyer can assess with confidence — which is precisely what makes it tradable at a fair price. There is a virtuous circle here: the same disclosure and revaluation discipline that earns the pricing dividend at issuance sustains the liquidity that protects the holder throughout the bond’s life. The doctrine’s contribution is to recognise that the management practices of Kinetics are also liquidity practices — that a well-managed bond is, for that reason alone, a more valuable one.

Maturity Optionality: Recycling the Strengthened Credit

Here the framework completes its arc. The appreciating-asset thesis predicted that, by the later years of the bond, the credit would be markedly stronger than at issuance — the LTV well below where it started, the security cover substantially expanded. Pillar K’s final discipline is to ensure that this accumulated strength is not merely admired but used. The widening gap between asset value and outstanding debt — the headroom designed in by Backing and Engineering — is an asset in its own right, and the doctrine identifies the ways an issuer can put it to work.

- Refinance on strength — an instrument that has demonstrably de-risked can be refinanced on better terms well before maturity — the strengthened credit commanding a tighter spread than the original — turning the appreciation into a lower cost of capital.

- Release surplus collateral — where the structure permits, a portion of the now-surplus security can be released back to the issuer, freeing collateral that conservative issuance had tied up — capital made available precisely because the thesis worked.

- Upsize for the next phase — the headroom can support a larger refinancing that funds the next phase of growth — the appreciated asset, having repaid its first bond, anchoring a larger second one. The balance sheet itself becomes a renewable source of expansion capital.

- Redeem from strength — the issuer may simply redeem the bond at maturity from a position of strength — the cleanest outcome, and one available precisely because the instrument was built to reach maturity stronger than it began.

This is the inverted credit curve’s ultimate payoff: a financing structure that does not merely survive its term but generates optionality at the end of it. The conventional bond is a liability discharged; the well-managed asset-anchored bond is a liability that, in being discharged, leaves the issuer better capitalised, more creditworthy, and ready to build again. Kinetics is how the strengthening the framework promised becomes growth the issuer can use.

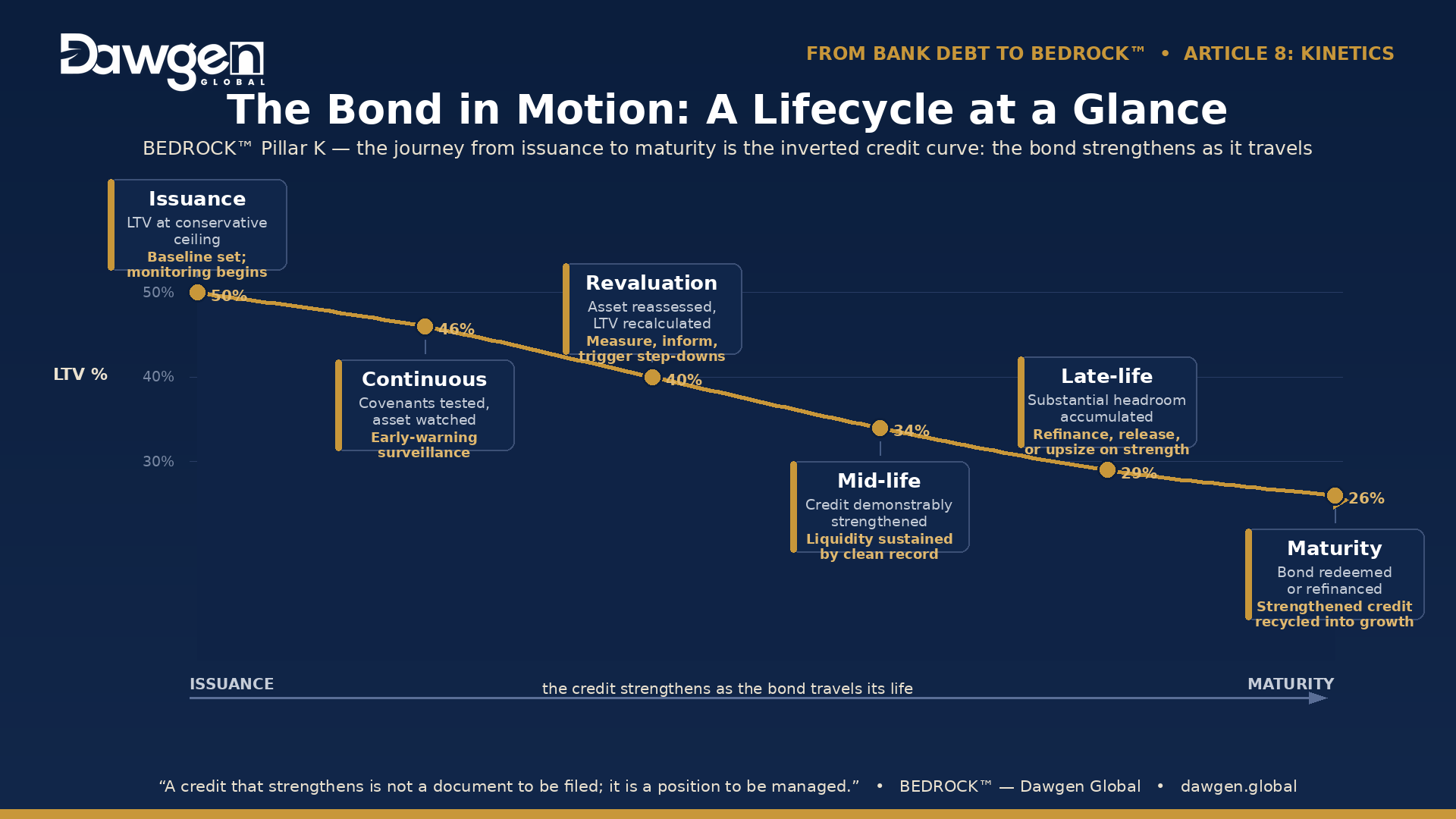

The Bond in Motion: A Lifecycle at a Glance

The kinetic life of a BEDROCK™ instrument, from issuance to maturity:

| Stage | What Happens | Kinetic Discipline |

| Issuance | Instrument placed; LTV at conservative ceiling | Baseline set; monitoring begins |

| Continuous | Covenants tested; asset performance watched | Early-warning surveillance |

| Revaluation (recurring) | Asset reassessed; LTV recalculated and reported | Measure, inform, trigger step-downs or protections |

| Mid-life | Credit demonstrably strengthened; record built | Secondary liquidity sustained by clean history |

| Late-life | Substantial headroom accumulated | Refinance, release, or upsize on strength |

| Maturity | Bond redeemed or refinanced | Strengthened credit recycled into next growth |

Read down the right-hand column and the doctrine of Kinetics appears in sequence: a credit that is set conservatively, watched continuously, measured and acted upon at each revaluation, kept liquid by its own clean record, and finally recycled — its accumulated strength converted into the issuer’s next chapter. This lifecycle capability is one of the dimensions the BEDROCK™ Bond Readiness Index assesses, because an issuer’s ability to manage an instrument across its life is as material to a successful issue as its ability to launch one.

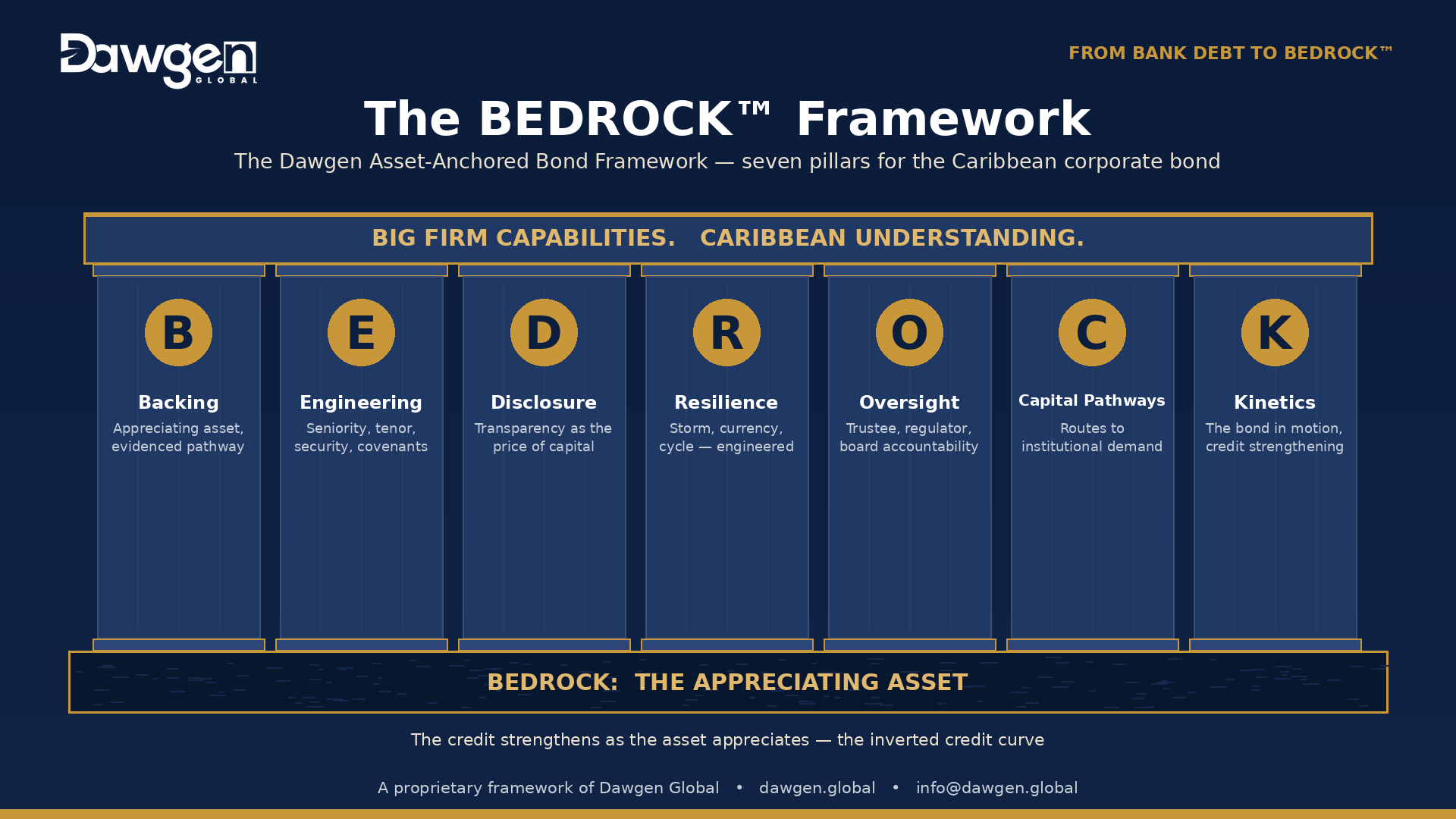

The Seven Pillars, Complete

Kinetics is the seventh and final pillar, and with it the BEDROCK™ Framework stands whole. It is worth seeing, now, how the seven work as one architecture rather than as a list.

Backing selects an appreciating asset and proves its pathway. Engineering builds the instrument — seniority, tenor, security, covenants, reserves — around that asset. Disclosure makes the instrument visible to the institutional capital that will hold it, earning the pricing dividend. Resilience stress-engineers it against the Caribbean’s storms, currency shocks, and cycles. Oversight installs the independent machinery — trustee, regulator, board — that enforces every promise. Capital Pathways connects the finished instrument to the regional demand built to hold it. And Kinetics manages the credit across its life, recognising the strengthening the first pillar promised and recycling it into the next phase of growth.

The seven are not independent. Each depends on the others: the inverted credit curve that Backing claims is engineered by Engineering, made visible by Disclosure, protected by Resilience, enforced by Oversight, priced by Capital Pathways, and realised by Kinetics. Remove any pillar and the structure weakens — an appreciating asset with no disclosure is unfinanceable; a well-disclosed instrument with no resilience fails in the first storm; a resilient bond with no governance is a set of unenforceable promises. The framework is a system precisely because its parts are interdependent. That interdependence is also why assessing an issuer’s readiness requires looking across all seven dimensions at once — which is the work of the diagnostic this series will close with.

Defined Terms

Pillar K adds three terms to the series vocabulary:

Kinetic management. The discipline of managing an asset-anchored bond across its life as a strengthening position rather than a static obligation — monitoring, revaluing, sustaining liquidity, and recycling accumulated credit strength into the next phase of growth.

Maturity optionality. The set of choices a strengthened credit creates near the end of its term — refinancing on better terms, releasing surplus collateral, upsizing for the next phase, or redeeming from strength — the ultimate payoff of the inverted credit curve.

Early-warning surveillance. The monitoring of leading indicators that precede a covenant breach — softening trends, counterparty strain, insurance lapse — so that the structure responds to the approach of trouble while responses are still cheap and options still open.

The Pillar in One Question

Kinetics’ governing question is the one that separates a bond that merely survives from one that builds: is the instrument actively managed so that the strengthening credit is recognised, rewarded, and recycled into the next phase of growth? Answered well — with continuous monitoring, contractual revaluation, sustained liquidity, and the optionality of a strengthened credit deliberately used — that question turns the bond from a liability that runs to maturity into an engine that, across its life, leaves the issuer stronger than it found them. That is the whole promise of the framework, realised.

The seven pillars are complete; the instrument is built and the framework is whole. What remains is to widen the lens. The next three articles turn from the single instrument to the market around it: the institutional capital that must be mobilised to buy these bonds, the regional bond market that must be deepened to trade them, and the sectors across the Caribbean where appreciating assets await the structure this series has built. We begin next week with the demand side: Article 9, Mobilising Caribbean Institutional Capital.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning — including the post-issuance monitoring, revaluation and refinancing strategy that manages an instrument across its life. Enquiries: [email protected].

Next in the series: Article 9 — Mobilising Caribbean Institutional Capital. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210