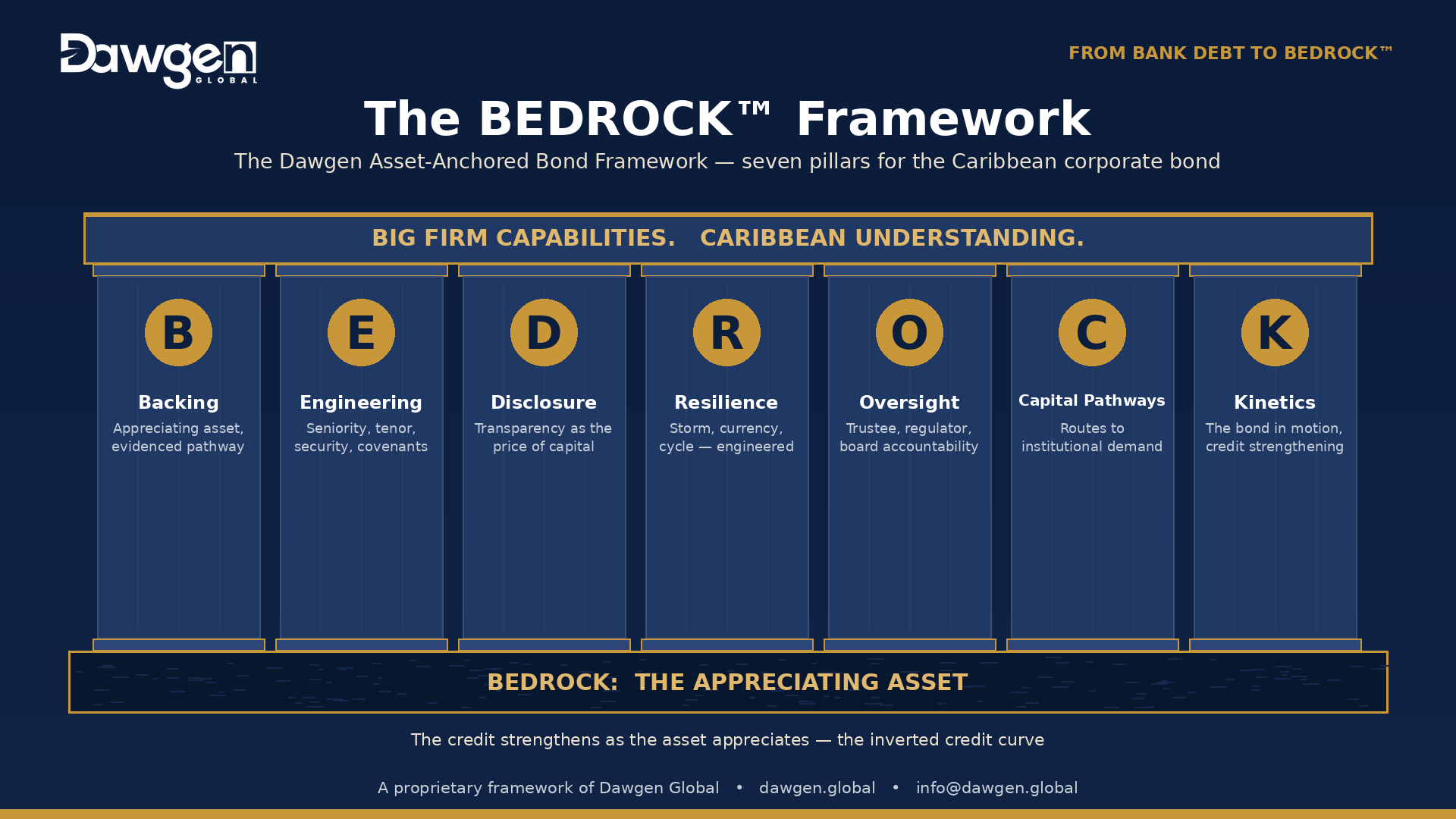

Pillar D of the BEDROCK™ Framework: transparency as the admission ticket to institutional pricing — offering standards, reporting cadence, and compliance certification

The first three pillars of the BEDROCK™ Framework built an instrument. Backing selected an appreciating asset and proved its pathway; Engineering gave the asset a structure — seniority, tenor, security, covenants, reserves. By the close of Article 3 we had a reference term sheet: a fifteen-year senior secured bond, conservatively structured, protected by a perfected security perimeter and a funded reserve stack. On paper, an excellent instrument.

On paper is precisely the problem. Everything engineered into that term sheet — every loan-to-value (LTV) ratio, every debt service coverage ratio (DSCR) test, every revaluation, every reserve — is a promise. An institutional investor does not buy promises; it buys verified, monitorable, enforceable promises. The mechanism that converts the one into the other is disclosure, and Pillar D — Disclosure — holds that transparency is not a regulatory burden grudgingly borne but the literal price of admission to institutional capital and institutional pricing.

This is the pillar Caribbean issuers most often underestimate, because it asks for something harder than a good asset or a clever structure: it asks for a permanent change in how the enterprise reports itself. This article sets out the Disclosure doctrine across the life of an instrument — the offering standard at issuance, the continuing standard through the bond’s life, the certification regime that makes covenants self-policing, and, at the centre, the pricing dividend that makes the whole discipline pay for itself.

The Wall Between Good and Financeable

Between a good business and a financeable bond stands a wall, and the wall is made of information asymmetry. The issuer knows its asset, its cash flows, its risks; the institutional investor knows only what the issuer chooses to show, in the form the issuer chooses to show it. Every gap between what the issuer knows and what the investor can verify is a risk the investor must price — and an investor who cannot quantify a risk does not ignore it. The investor assumes the worst and prices accordingly, or declines entirely.

This is why two issuers with identical assets and identical structures can face entirely different markets. The opaque issuer — audited late, reporting thinly, disclosing reluctantly — is priced as though its undisclosed risks are real, because the investor cannot prove they are not. The transparent issuer — audited cleanly and promptly, reporting richly, disclosing before being asked — is priced on its actual risk, because the investor can see it. The difference between those two prices, on a fifteen-year instrument, dwarfs the entire cost of the disclosure that produces it. Disclosure is the cheapest yield the issuer will ever buy.

An institutional investor does not buy promises; it buys verified, monitorable, enforceable promises. Disclosure is what converts the one into the other — and the cheapest yield an issuer will ever buy.

The Offering Standard: Disclosure at Issuance

The first disclosure obligation is the offering document — the prospectus or information memorandum through which the instrument is sold. For an asset-anchored bond, the doctrine requires that the offering document do more than satisfy the minimum content rules of the relevant securities regime; it must tell the appreciating-asset story completely enough that a prudent institutional investor can underwrite the credit without privileged access. Five disclosure domains define the standard.

The Asset and Its Pathway

The backing asset must be described with the evidence package Pillar B demands: independent valuation with methodology and assumptions disclosed, the documented appreciation drivers, comparable transaction evidence, and — critically — both the market-value and stressed-disposal-value bases. The LTV trajectory under base and stressed assumptions, the chart at the heart of Article 2, belongs in the offering document, not in a private model.

The Structure and Its Protections

Every structural feature engineered under Pillar E must be set out plainly: seniority and ranking, the full security perimeter and its perfection status, the covenant package with each threshold stated, the reserve stack and its funding, and the revaluation mechanics. An investor should be able to read the term sheet and the offering document together and find no gap between what was designed and what is disclosed.

The Cash Flows and Their Coverage

Historical and projected cash flows, the DSCR under base and stressed cases, the income alignment between the asset and the debt service, and a candid account of cash-flow concentration — by tenant, counterparty, season, or currency. The income story carries the coupon; it must be shown, not summarised.

The Risks, Named by the Issuer

The doctrine’s rule on risk disclosure is counter-intuitive but decisive: the issuer should name its own risks, fully and first. Catastrophe exposure, currency mismatch, tourism-cycle sensitivity, refinancing dependence, key-counterparty reliance — every risk an investor would eventually find should be disclosed and addressed before the investor finds it. A risk the issuer names and mitigates is a managed risk; the same risk discovered by the investor in due diligence is a credibility failure that reprices the whole instrument.

The People and the Governance

The issuer’s ownership, group structure, board, management, and related-party arrangements — the governance reality that Pillar O will govern — disclosed clearly enough that the investor understands who controls the asset and the cash flows, and how their interests are aligned with the bondholders’.

The Continuing Standard: Disclosure Through the Life

Issuance disclosure opens the relationship; continuing disclosure sustains it. An asset-anchored bond is a fifteen-year promise, and the investor’s confidence — and the instrument’s secondary-market value, the subject of Pillar K — depends on a continuing flow of information that lets the holder re-underwrite the credit at any time. The doctrine sets a continuing standard in four layers.

- Annual — audited annual financial statements prepared to a recognised standard — for most Caribbean issuers, International Financial Reporting Standards (IFRS) — delivered within a defined and demanding window after year-end. Late accounts are themselves a disclosure: they tell the market the issuer cannot close its books promptly, and the market prices that signal.

- Semi-annual or quarterly — management accounts and a covenant compliance report — LTV and DSCR against their thresholds, reserve balances, and material developments — so the investor sees the credit’s trajectory between annual anchors rather than only at year-end.

- On the revaluation cycle — the revaluation cadence of Pillar B — the doctrine’s default every three years — reported to investors with the methodology and the recalculated LTV, converting the inverted credit curve from a claim at issuance into a documented record over the life.

- On occurrence — a defined obligation to disclose material events promptly — damage to the asset, loss of a key counterparty, breach or near-breach of a covenant, change of control. The discipline is timeliness: a material event disclosed late is worse than one disclosed badly, because lateness destroys the trust the whole regime exists to build.

Compliance Certification: Making Covenants Self-Policing

Covenants engineered under Pillar E are only as strong as the regime that proves compliance. The doctrine’s instrument is the compliance certificate: a periodic, signed statement from the issuer’s directors or chief financial officer certifying — with the supporting calculations attached — that each covenant has been tested and either met or breached. Three features make certification more than a formality.

First, it shifts the burden of proof. Without certification, the investor must detect a breach; with it, the issuer must affirmatively declare compliance, on the record, with personal accountability attached. That reversal is the difference between a covenant that is monitored and one that is merely written.

Second, it creates a documentary trail that makes both enforcement and trust possible. A history of clean, timely certificates is an asset — it lowers the perceived risk of the instrument and supports the secondary-market value and the pricing step-downs of later articles. A pattern of late or qualified certificates is an early-warning system that lets investors and trustees act under Pillar O before a manageable problem becomes a default.

Third, when paired with the springing covenants of Article 3, certification becomes the trigger mechanism: the certificate that reports an LTV above the springing threshold is the document that activates the cash sweep or the coupon step-up automatically. Certification is how the structure’s nervous system actually fires.

The Pricing Dividend: Why Disclosure Pays for Itself

Everything in this pillar costs the issuer something — audit fees, reporting infrastructure, the discipline of timeliness, the discomfort of naming one’s own risks. The doctrine’s central claim is that this cost is not a cost at all but an investment with a measurable return: the pricing dividend, the reduction in the risk premium an issuer pays when it removes the investor’s uncertainty rather than asking the investor to price around it.

Recall the wall of information asymmetry. The risk premium an investor demands has two components: compensation for risks that genuinely exist, and compensation for risks that might exist but cannot be ruled out. Disclosure cannot touch the first — a catastrophe-exposed asset is catastrophe-exposed however well disclosed. But disclosure eliminates the second entirely. The transparent issuer pays only for its real risks; the opaque issuer pays for its real risks plus the shadow of every risk it has left the investor to imagine.

On a long-dated instrument, that shadow premium is the difference between a financeable coupon and an unfinanceable one — and it compounds across the full tenor. An issuer who spends to disclose well is buying down its cost of capital for fifteen years. This is why the doctrine treats disclosure quality not as compliance overhead but as a financing decision, and one of the highest-return financing decisions an issuer will make: the marginal dollar spent on credible transparency returns multiples in reduced coupon over the life of the bond.

The Disclosure Standard, at a Glance

The Disclosure doctrine assembles into a standard the issuer commits to at issuance and sustains for the life of the instrument:

Defined Terms

Pillar D adds three terms to the series vocabulary:

Pricing dividend. The reduction in the risk premium an issuer pays when credible disclosure removes the investor’s uncertainty — so that the issuer is priced on its real risks alone, not on the shadow of risks left unverified. The measurable return on disclosure quality.

Compliance certificate. A periodic signed statement from the issuer’s directors or chief financial officer (CFO), with supporting calculations, certifying that each covenant has been tested and met — shifting the burden of proof from investor detection to issuer declaration, and serving as the trigger document for springing covenants.

Continuing disclosure standard. The defined, ongoing flow of information — audited financials, management reporting, revaluation reports, and material-event notices — that allows an institutional investor to re-underwrite an asset-anchored bond at any point in its life.

The Pillar in One Question

Disclosure’s governing question is the one an issuer should ask of every page it puts before the market: would a prudent institutional investor receive everything needed to underwrite, monitor, and re-underwrite this credit? Answered honestly — with a complete offering document, a demanding continuing standard, a certification regime that makes covenants self-policing, and the willingness to name one’s own risks first — that question turns information from the issuer’s liability into the issuer’s cheapest source of yield.

Yet there is one category of risk that disclosure can describe but not dissolve — the risks peculiar to operating in the Caribbean itself: the hurricane season, the currency mismatch, the tourism cycle, the single-market concentration. Disclosing these honestly is necessary, but it is not sufficient. They must be engineered against. That is the work of the pillar that makes BEDROCK™ unmistakably Caribbean, and it is next week’s subject: Article 5, Resilience: Stress-Engineering Bonds for the Caribbean.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning — including the disclosure, reporting and governance build-out that brings an issuer to institutional standard. Enquiries: [email protected].

Next in the series: Article 5 — Resilience: Stress-Engineering Bonds for the Caribbean. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210