Pillar E of the BEDROCK™ Framework: seniority, tenor, coupons, security, covenants, and reserves — the architecture that converts an asset thesis into an investable instrument

Pillar B closed with a warning disguised as a transition: a qualifying asset is only the beginning. An appreciating beachfront property, a scarce logistics site, a contracted energy installation — none of these is an investment. They become investable only through structure: the set of design decisions that determine who ranks where, for how long, paid what, protected by which security, governed by which covenants, and cushioned by which reserves. Pillar E — Engineering — is the doctrine of those decisions.

The premise of this pillar is blunt: in credit, structure is the product. Two bonds against the same asset, with the same coupon, issued by the same company, can be radically different investments — one institutional-grade, one an accident in progress — depending entirely on engineering choices that occupy a few dense pages of the trust deed. Instruments rarely fail because the asset was wrong; they fail at their weakest structural decision: the tenor that forced a refinancing in a bad year, the covenant that didn’t spring until the damage was done, the reserve that was never funded, the security that turned out to rank behind a bank facility nobody disclosed.

This article sets out the Engineering doctrine across its six structural domains — seniority, tenor, repayment, coupon, security, and covenants-with-reserves — and closes with the question that precedes them all in Caribbean practice: what to do when the balance sheet, as it stands, cannot yet carry the structure the asset deserves. That is where this series’ sister framework, TRANSCEND™, enters the doctrine.

Seniority: Rank Is the First Promise

The first engineering decision is the oldest question in credit: who stands where in the queue. The BEDROCK™ doctrine’s default is senior secured — the bond ranks ahead of unsecured creditors and holds a first-ranking charge over the backing asset — because the entire appreciating-collateral thesis presumes the bondholder actually owns the benefit of the appreciation. A second-ranking charge behind an undisclosed or elastic bank facility converts the inverted credit curve into someone else’s upside.

Three disciplines make seniority real rather than nominal:

- Intercreditor clarity — where any other secured creditor exists or may exist — a working-capital bank line is the common case — the ranking, standstill, and enforcement rights must be written down in an intercreditor agreement before issuance, not negotiated during a crisis. The doctrine’s rule: the bond’s first claim on the backing asset is non-negotiable; working-capital lenders may rank first on working-capital assets, and nowhere else.

- Negative pledge — a covenant preventing the issuer from granting security over the backing asset, or over the cash flows that service the bond, to any other party. The negative pledge is the perimeter fence of the structure; without it, seniority erodes one facility at a time.

- Structural subordination control — where the backing asset sits in a subsidiary, bondholders must not find themselves structurally behind that subsidiary’s own creditors. The doctrine’s tools are direct issuance from the asset-owning entity, upstream guarantees, or share pledges over the asset owner — chosen case by case, but never omitted.

Tenor: The Calendar Is a Risk Decision

Article 1 named the bank-debt trap’s first distortion: five-to-seven-year facilities against twenty-to-forty-year assets, manufacturing a refinancing event every few years and handing the calendar the power to wreck a sound business. The Engineering answer is the doctrine of tenor matching: the instrument’s life should be set by the asset’s life and the credit’s trajectory, not by the lender’s funding habits.

For most qualifying backing assets, that points to tenors of ten to twenty years — long enough that the appreciating collateral does its compounding work, long enough that no refinancing falls due before the credit has strengthened and aligned with the liability horizons of the pension funds and insurers Pillar C will address. Three refinements complete the doctrine:

- Maturity placed on the curve — the tenor should be chosen so that any refinancing or maturity event arrives when the credit is at its strongest — late in the LTV trajectory — never at a fixed interval that ignores the curve. A fifteen-year bond against a thirty-year asset refinance, if at all, into a position of strength.

- Issuer optionality, priced — long tenor must not become a trap for the issuer. Call protection should be honest — investors are entitled to a period of non-call and to make-whole economics — but the structure should preserve the issuer’s ability to refinance once the credit has demonstrably strengthened, typically through step-down call schedules tied to revaluation outcomes.

- Tranching without trap-building — where institutional demand favours intermediate tenors, a tranched issuance — say, a ten-year and a fifteen-year series against the same security package — can match investor appetite without reintroducing the refinancing trap, provided the shorter tranche matures inside the credit’s strengthening phase.

Repayment Architecture: How the Principal Comes Home

Whether the principal returns in one payment or many is not a detail; it determines the cash-flow burden the asset must carry and the shape of the risk the investor holds. The doctrine recognises three legitimate architectures and matches each to an asset profile:

- Bullet — full principal at maturity. Suits assets whose income comfortably covers coupons but whose value story is the primary protection — the pure expression of the inverted credit curve, as in the Blue Harbour model of Article 2. Discipline requirement: a refinancing or disposal plan disclosed at issuance, and a sinking-fund or cash-sweep trigger if late-life revaluations disappoint.

- Amortising — scheduled principal repayment over the life. Suits assets with strong, stable income — contracted energy, long-leased logistics — where debt service capacity is the credit’s engine. Amortisation accelerates the LTV trajectory from both directions: debt falls while value rises.

- Hybrid — an interest-only period through construction or ramp-up, then amortisation from stabilised cash flows, often with a moderate balloon. Suits expansion and development-linked issuances — with the milestone and escrow mechanics that Pillar O will govern.

Two mechanisms serve all three architectures. A sinking fund — periodic payments into a trustee-held account dedicated to principal — converts a distant bullet into a funded promise. A cash sweep — excess cash flow above a threshold applied to early principal — lets strong years de-risk the structure automatically. The doctrine favours making at least one of them springing: dormant while the credit performs, mandatory when revaluation or coverage tests deteriorate.

Coupon Design: Pricing the Promise

The coupon is where issuer economics meet investor mandate, and the doctrine’s guidance is to design for the holder the instrument is built to attract — the regional institutional investor with long-dated, largely nominal liabilities.

Fixed-rate is the doctrine’s default. It gives the issuer certainty of debt service for the full tenor — eliminating the repricing exposure named in Article 1 — and gives the pension fund or insurer exactly the predictable long-duration income its liability profile demands. Floating-rate paper, the bank market’s habit, simply transfers the system’s interest-rate risk onto the issuer’s balance sheet; in an asset-anchored structure it should be the exception, used only where the asset’s own revenues float with rates.

Two refinements extend the toolkit. Step-down coupons — a contractual coupon reduction earned when revaluation confirms the Loan to value (LTV) trajectory has reached defined milestones — are the purest expression of the inverted credit curve in pricing: the issuer is rewarded, automatically and transparently, for the credit strengthening the offering promised. (The mirror image, step-ups on deterioration, protects investors symmetrically.) Inflation-linked coupons can suit assets whose revenues are themselves inflation-correlated — hospitality rates, indexed leases — and can be attractive to liability-matching investors; the discipline requirement is that the linkage run through both sides, revenue and coupon, or not at all.

Currency belongs to coupon design’s borderland and will be treated fully under Pillar R: the doctrine’s headline is that debt service currency should follow revenue currency, and that hard-currency issuance against local-currency income is a stress test failed at the term sheet.

The Security Perimeter: Building the Package

Pillar B selected the anchor; Engineering builds the full perimeter around it. A BEDROCK™ security package is layered — each layer answering a different failure mode — and the doctrine’s standard composition runs:

- First-ranking charge over the backing asset — the registered mortgage or equivalent over the property, plant, or rights that carry the appreciation thesis. The core layer; everything else supports it.

- Debenture over the issuing entity — fixed and floating charges capturing the business that operates the asset, preventing value from leaking into unsecured corners of the same enterprise.

- Assignment of insurances — the proceeds of property, business-interruption, and catastrophe cover assigned to the security trustee, so that the event that damages the collateral funds its restoration or repays the debt. In the Caribbean this layer is not ancillary; Pillar R will make it central.

- Assignment of key receivables and contracts — management agreements, anchor leases, offtake contracts: the income alignment test of Pillar B, made enforceable.

- Share pledge over the asset-owning entity — the enforcement accelerator: the ability to take the company rather than foreclose on the asset, preserving going-concern value in precisely the scenarios where forced sale destroys it.

The doctrine’s test for the package is enforceability in fact, not in drafting: every charge registrable and registered, every consent (landlord, regulator, counterparty) obtained at issuance, every assignment notified. A security package with an unobtained consent is a literary work.

Covenants and Reserves: The Structure’s Nervous System

Covenants are how the structure perceives and responds; reserves are how it buys time. The doctrine’s covenant architecture is built as a ladder — graduated responses that engage early and escalate — rather than a single tripwire at the edge of default:

- Maintenance covenants — the continuous obligations: maximum loan-to-value tested at each revaluation, minimum debt service coverage tested periodically, insurance maintenance, and information undertakings. These define performing.

- Incurrence covenants — tested only when the issuer acts — additional debt, disposals, distributions. The doctrine’s signature here is the distribution lock: dividends permitted only while coverage and LTV tests are met with headroom, so that equity is paid from genuine surplus, never from the cushion.

- Springing covenants — the ladder’s engine: obligations that lie dormant while the credit performs and activate on defined deterioration — a cash sweep that switches on if Loan to value (LTV) exceeds a threshold at revaluation, a coupon step-up on a missed coverage test, a top-up or partial-redemption obligation if the shock case of Article 2 materialises. Springing covenants let a structure be light in good times without being naked in bad ones.

Beneath the covenant ladder sits the reserve stack — trustee-held accounts funded at or after issuance: a debt service reserve (the doctrine’s default: six months’ debt service, the time a sound issuer needs to manage a shock), an insurance reserve where premium continuity is mission-critical, and a capex or maintenance reserve where the asset’s value depends on a defined investment programme. Reserves are the structure’s honesty about bad years: they convert “it should be fine” into funded time.

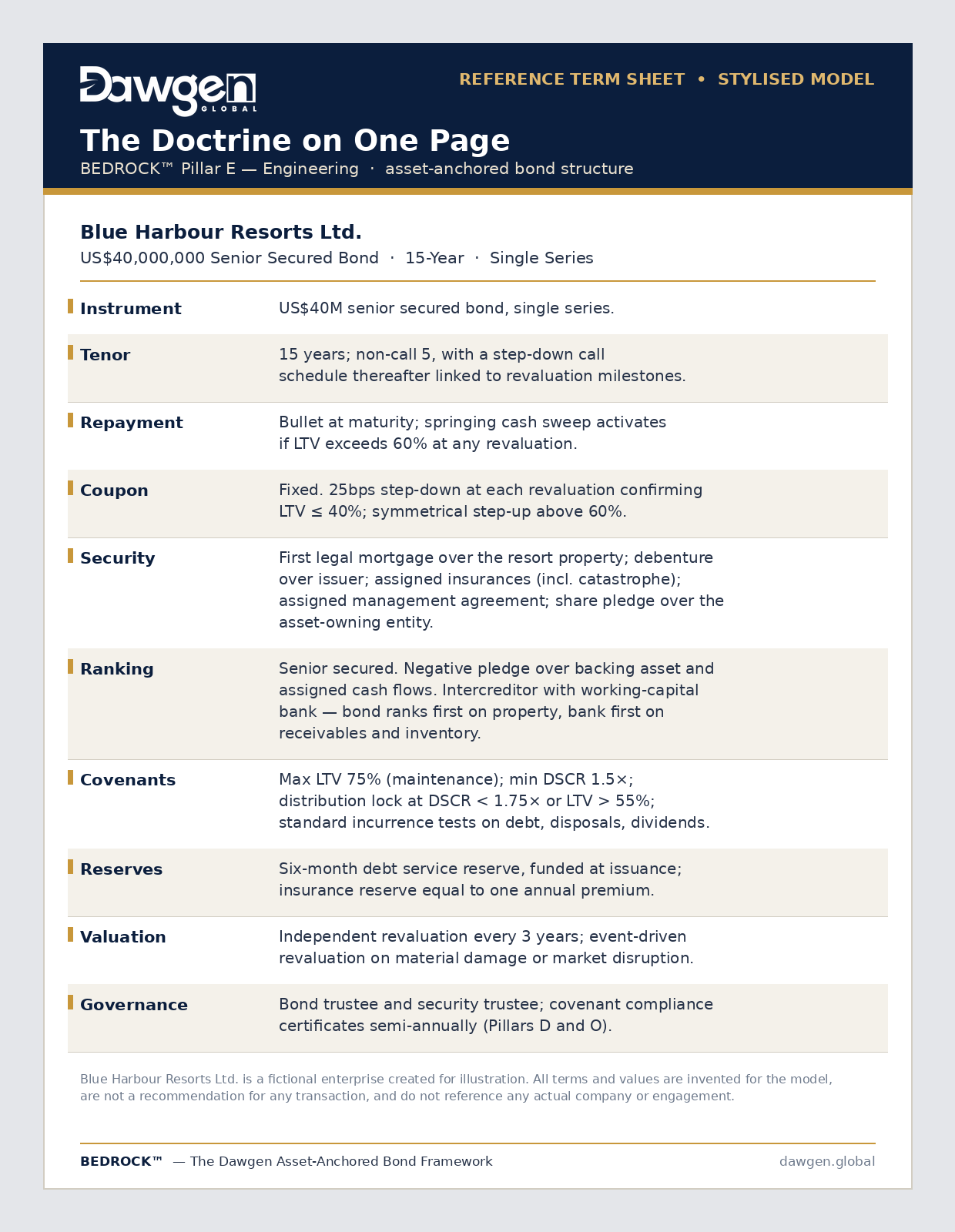

The Doctrine on One Page: A Reference Term Sheet

Assembled, the Engineering doctrine reduces to a term sheet. Here is the Blue Harbour model of Articles 1 and 2, engineered:

Two bonds against the same asset can be radically different investments. In credit, structure is the product — and instruments fail at their weakest structural decision.

Before the Anchor: The TRANSCEND™ Interface

Everything above assumes a balance sheet capable of carrying the structure. Much of the Caribbean’s corporate reality does not start there — and the Engineering doctrine is incomplete without saying so plainly. The common condition: a fundamentally sound enterprise whose qualifying asset is already encumbered by layers of legacy bank security taken over years of facility renewals; whose group structure scatters the asset, the income, and the debt across entities that grew by accident; and whose existing facilities carry cross-defaults and consent rights that make a clean issuance impossible as things stand.

This is not a disqualification. It is a sequencing problem — and it is precisely the territory of TRANSCEND™, Dawgen Global’s corporate restructuring framework. The repair work is itself an engineering discipline: consolidating and refinancing legacy facilities so that security over the backing asset can be released and re-granted cleanly; repositioning the group so the asset, its income, and the new instrument sit in a structure an investor can underwrite; negotiating intercreditor terms with incumbent lenders from a plan rather than from distress; and rebuilding the reporting and governance baseline the bond’s continuing obligations will demand. The sequence is the strategy: TRANSCEND™ repairs the balance sheet; BEDROCK™ funds the growth. An issuer who attempts the second without the first is building the term sheet above on ground that has not been cleared — and the market prices uncleared ground without mercy.

Defined Terms

Pillar E adds four terms to the series vocabulary:

Tenor matching. The engineering principle that an instrument’s life should be set by the backing asset’s economic life and the credit’s LTV trajectory — so that no refinancing event falls due before the credit has strengthened.

Security perimeter. The layered security package of an asset-anchored bond — first charge, debenture, assigned insurances, assigned contracts, and share pledge — each layer answering a distinct failure mode, all perfected in fact at issuance.

Springing covenant. An obligation that lies dormant while the credit performs and activates automatically on defined deterioration — the mechanism that lets a structure be light in good times without being unprotected in bad ones.

Reserve stack. The set of trustee-held, pre-funded accounts — debt service, insurance, and capex reserves — that convert a structure’s resilience claims into funded time.

The Pillar in One Question

Engineering’s governing question gathers the six domains into a single test: is the instrument engineered so that its structure, tenor, and protections match the asset and survive stress? Seniority that is real, tenor placed on the credit’s curve, repayment matched to the income, a coupon designed for its holder, a perimeter perfected in fact, and a covenant ladder with funded reserves beneath it — that is what the question demands, and what the reference term sheet assembles.

But a perfectly engineered instrument that investors cannot see into is unfinanceable. Every structural promise made in this article — every ratio, reserve, and revaluation — is only as credible as the information regime that reports it. That regime is Pillar D, and it is next week’s subject: Article 4, Disclosure: The Price of Institutional Capital.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning — including TRANSCEND™-led restructuring for enterprises whose balance sheets must be repaired before they can be anchored. Enquiries: [email protected].

Next in the series: Article 4 — Disclosure: The Price of Institutional Capital. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ and TRANSCEND™ are proprietary frameworks of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210