Pillar C of the BEDROCK™ Framework: placement routes, institutional eligibility, and the regional market — connecting the finished instrument to the capital built to hold it

Six pillars have built an instrument: an appreciating asset, soundly engineered, fully disclosed, stress-proofed against the region’s risks, and independently governed. It is, by now, an excellent bond. But an excellent bond is not yet financing. Between the finished instrument and the capital it needs lies a question this series has so far deferred: how does the bond reach the investors built to hold it — and is there a market deep enough to receive it?

This is the work of Pillar C — Capital Pathways. It is the pillar that turns a structure into a transaction, connecting the issuer to institutional demand through the right route, into the right hands, at the right price. And it carries a thesis this series has asserted since Article 1 and now must substantiate: that the capital to fund the Caribbean’s appreciating assets already exists, in the region, in the portfolios of institutions structurally hungry for exactly the instrument BEDROCK™ produces. Pillar C is where that latent demand and that engineered supply are introduced to one another.

This article maps the demand that exists, sets out the placement routes by which an issue reaches it, addresses the pricing architecture that determines the issuer’s cost and the investor’s return, and closes on the larger stake: that every well-built Caribbean bond deepens the regional market for the next one. Distribution, in this framework, is never merely a sales exercise. It is the act of building the market itself.

The Demand That Already Exists

Article 1 made the claim; Pillar C grounds it. The Caribbean holds substantial pools of long-dated institutional capital whose defining problem is not a shortage of money but a shortage of assets that match their liabilities. Two investor classes dominate, and the asset-anchored bond is built for both.

Pension Funds

Regional pension funds carry liabilities measured in decades: obligations to pay retirees far into the future, requiring assets that generate predictable, long-duration income. Their structural problem is that the regional menu of such assets is thin — government paper, bank deposits, a narrow set of listed equities, and limited real estate. A fifteen-year, senior secured, fixed-coupon bond against an appreciating asset is close to a designed solution for a pension fund’s liability profile: long tenor matching long liabilities, fixed income matching actuarial assumptions, and a security package whose loan-to-value (LTV) improves over time, reducing risk precisely as the liability approaches.

Insurance Companies

Life insurers, in particular, hold obligations stretching a generation forward and are among the most natural buyers of long-dated secured debt anywhere in the world. Their investment is governed by prudential rules that reward secured, well-rated, long-duration assets — and an asset-anchored bond, properly structured and disclosed, is designed to qualify. The insurer’s discipline is also the issuer’s discipline: the features an insurer’s regulator demands (security, coverage, governance, transparency) are precisely the features BEDROCK™’s six prior pillars engineer.

Beyond these two, the demand base extends to credit unions and cooperative financial institutions seeking yield on stable deposits, asset managers building fixed-income portfolios, development finance institutions with mandates to deepen regional capital markets, and high-net-worth and family-office capital seeking secured regional exposure. The point holds across all of them: this is demand looking for supply. Pillar C’s task is to connect the two without losing, in distribution, the quality the instrument was built to carry.

On one side: institutions with thirty-year liabilities and too few long-dated assets to match them. On the other: enterprises with appreciating assets and too little long-tenor capital. Pillar C is the introduction.

The Placement Routes

How an issue reaches its investors is a structural decision with consequences for cost, speed, disclosure, liquidity, and investor base. The doctrine recognises three principal routes, each suited to a different issuer profile and issue size.

Private Placement

The issue is placed directly with a small number of sophisticated institutional investors — sometimes a single anchor investor, sometimes a club — without a public offering. The advantages are speed, confidentiality, lower issuance cost, and the ability to negotiate terms directly with investors who understand the asset. The trade-offs are a narrower investor base, typically smaller issue size, and limited secondary liquidity. Private placement suits first-time issuers, smaller issues, and assets whose story is best told directly to a few expert buyers.

Exempt Distribution

The issue is distributed more widely but only to qualified or accredited investors, under the exemptions most regional securities regimes provide from full public-offering requirements. This route reaches more of the institutional demand base than a private placement while avoiding the full prospectus and continuing-obligation burden of a public listing. It is often the doctrine’s default for institutional-scale Caribbean issues: broad enough to achieve size and competitive pricing, disciplined enough to maintain quality, and calibrated to the professional investors the instrument is built for.

Public Listed Issuance

The issue is offered publicly and listed on a regional securities exchange, with a full prospectus, exchange listing rules, and continuing obligations. This route reaches the widest investor base, achieves the largest issue sizes, builds secondary liquidity, and — as Article 6 noted — adds the exchange as an independent monitor and the pricing dividend of demonstrated disclosure discipline. The trade-offs are higher cost, longer timelines, and the fullest disclosure burden. Public listing suits larger, established issuers, repeat programmes, and issues where liquidity and market presence justify the additional weight.

The routes are not a hierarchy but a fit decision, and many issuers travel them in sequence — a private placement to establish a track record, an exempt distribution to scale, a public listing as the programme matures. The doctrine’s rule is to match the route to the issue’s size, the issuer’s maturity, and the investor base sought, and never to choose a lighter route to shed protections the instrument should carry regardless.

Pricing Architecture: The Appreciating-Collateral Argument

Pricing is where the issuer’s cost of capital and the investor’s return are set, and where the entire BEDROCK™ thesis is finally tested against the market. The doctrine builds price from a transparent foundation rather than a negotiated guess.

The starting point is a benchmark: the yield on a comparable-tenor sovereign or other reference instrument in the relevant currency — the risk-free anchor against which all credit is priced. To that benchmark the market adds a credit spread reflecting the instrument’s risk: the strength of the asset, the structure, the disclosure, the resilience, and the governance — which is to say, the cumulative quality of the six pillars that precede this one. Every prior pillar, in the end, is a pricing argument: the pricing dividend of disclosure (Article 4), the survival demonstrated by scenario testing (Article 5), the enforceability of the security and governance (Articles 3 and 6) each compresses the spread the investor demands.

And then the argument unique to this framework: the appreciating-collateral case for spread. A conventional secured bond is priced on its loan-to-value at issuance, treated as static or amortising. A BEDROCK™ instrument asks the market to price the trajectory — the inverted credit curve of Article 2, in which the LTV declines and the security cover compounds over the life of the bond. An instrument whose credit demonstrably strengthens, with revaluation making the improvement contractual and the step-down coupon of Article 3 sharing it, merits a different spread conversation than one priced on static-collateral assumptions. The doctrine does not claim this argument wins automatically — markets must be persuaded — but it insists the argument be made explicitly, because an issuer who lets an appreciating-asset bond be priced as though its collateral were wasting has left the framework’s central value on the table.

Deepening the Market With Every Issue

Pillar C carries a responsibility larger than any single transaction. The Caribbean bond market is shallow not because the region lacks issuers or investors but because the connecting infrastructure — the precedents, the standards, the investor familiarity, the secondary-market habits — is still thin. Every well-built issue thickens it.

The mechanism is cumulative. A first asset-anchored issue, soundly structured and successfully placed, becomes a precedent: a template other issuers and their advisers can follow, a structure investors have now underwritten once and can underwrite faster again, a data point in a market that previously had few. Each subsequent issue that meets the standard reinforces it, building the shared vocabulary and the investor confidence that lower the cost and shorten the timeline for the next issuer. A market is not an institution that someone provides; it is a habit that participants build, issue by issue. This is why the doctrine treats every BEDROCK™ placement as partly a public act: the issuer raises its own capital and, in doing so, deepens the channel through which the next Caribbean enterprise will raise its own. The cost of capital the region pays a decade from now is being set, issue by issue, by the quality of the issues placed today.

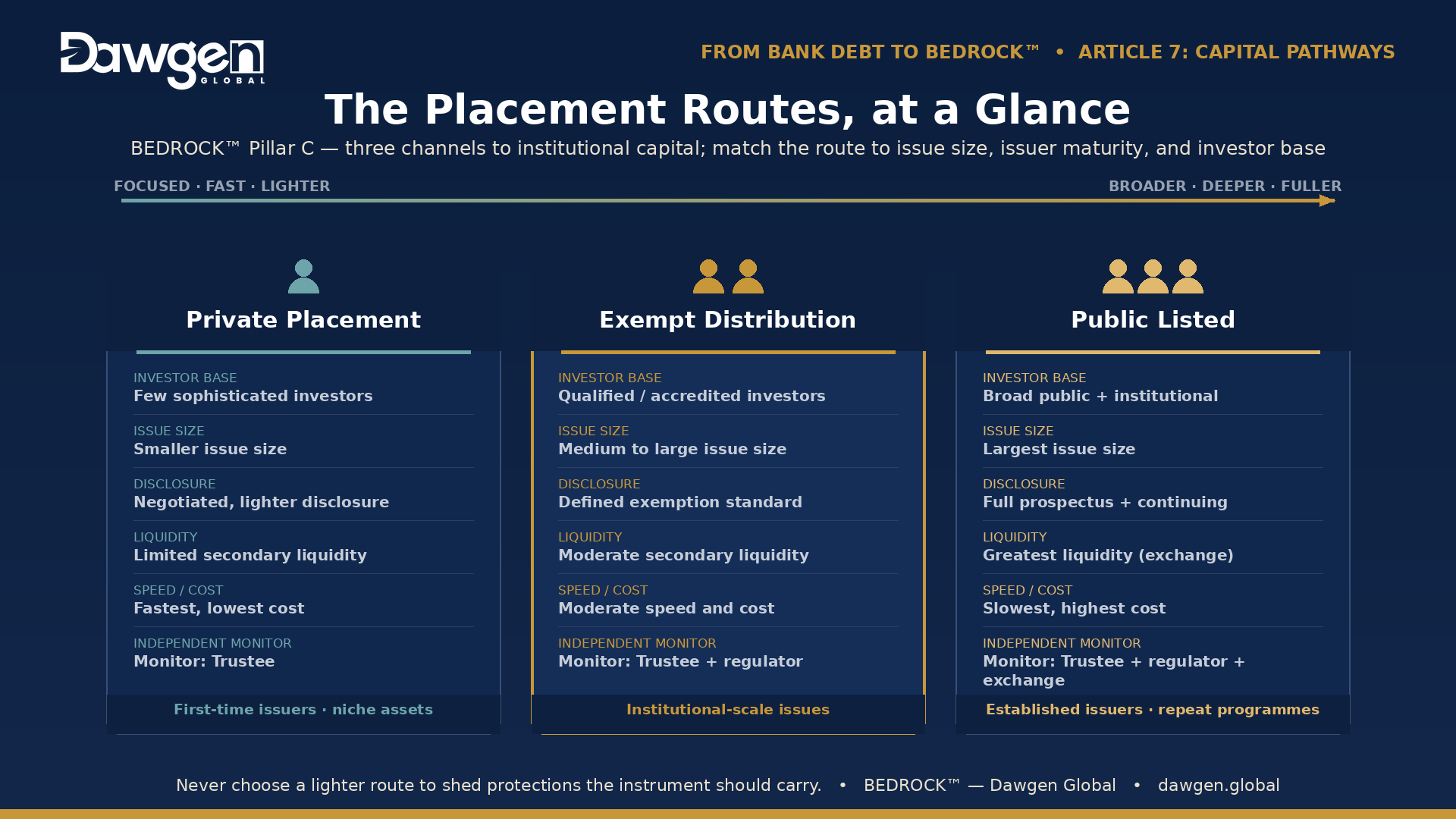

The Placement Routes, at a Glance

The three routes compared across the dimensions that drive the decision:

| Dimension | Private Placement | Exempt Distribution | Public Listed |

| Investor base | Few sophisticated investors | Qualified / accredited investors | Broad public and institutional |

| Typical issue size | Smaller | Medium to large | Largest |

| Disclosure burden | Negotiated, lighter | Defined exemption standard | Full prospectus + continuing |

| Secondary liquidity | Limited | Moderate | Greatest (exchange-traded) |

| Speed / cost | Fastest, lowest cost | Moderate | Slowest, highest cost |

| Independent monitor | Trustee | Trustee + regulator | Trustee + regulator + exchange |

| Best suited to | First-time issuers, niche assets | Institutional-scale issues | Established issuers, repeat programmes |

The right route is rarely obvious from the asset alone; it depends on issue size, issuer maturity, the investor base sought, and the issuer’s appetite for disclosure and liquidity. Matching instrument to route to investor is one of the dimensions the BEDROCK™ Bond Readiness Index assesses, and a frequent reason an issuer with a sound, well-structured instrument routes to Corporate Finance for placement strategy and execution.

Defined Terms

Pillar C adds three terms to the series vocabulary:

Placement route. The structural channel by which an asset-anchored bond reaches its investors — private placement, exempt distribution, or public listed issuance — selected to match issue size, issuer maturity, and the investor base sought, without shedding protections the instrument should carry.

Institutional demand base. The pools of long-dated regional capital — pension funds, insurers, credit unions, asset managers, development finance institutions, and family offices — whose liability profiles make them the natural holders of long-tenor, secured, asset-anchored bonds.

Appreciating-collateral spread argument. The pricing case that an instrument whose loan-to-value declines and security cover compounds over its life — the inverted credit curve — merits a tighter credit spread than one priced on static-collateral assumptions, and must be made explicitly at placement.

The Pillar in One Question

Capital Pathways’ governing question reaches beyond the single transaction: does the instrument reach the institutional capital built to hold it — and leave the market deeper than it found it? Answered well — with demand correctly mapped, the route matched to the issue, the price built transparently, and the appreciating-collateral argument made explicitly — that question turns an excellent instrument into completed financing, and a single placement into a contribution to the regional market’s depth.

Yet a bond’s life does not end at placement; in a sense it begins there. The instrument that reaches the investor must then be managed across fifteen years — monitored, revalued, traded, and ultimately refinanced or redeemed — with the strengthening credit recognised and recycled at each stage. That post-issuance lifecycle is the final pillar of the framework, and it is next week’s subject: Article 8, Kinetics: Managing the Bond as the Credit Strengthens.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning — including placement strategy, investor access, and transaction execution for institutional-scale issues. Enquiries: [email protected].

Next in the series: Article 8 — Kinetics: Managing the Bond as the Credit Strengthens. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210