Much of the capital a financial institution holds is trapped — locked away by crude measurement and inefficient structure, not by any genuine requirement. Releasing it, safely, is among the highest-value things actuarial work can do.

Capital is the most expensive resource a financial institution holds. An insurer, a bank, a credit union must keep capital in reserve against the risks it runs — a buffer that stands between an unexpected loss and insolvency, demanded by regulators and by prudence alike. That buffer is essential and non-negotiable. But capital is not free: the shareholders or members who provide it expect a return on every dollar, and a dollar held idle is a dollar that is neither funding growth nor earning that return. The cost of holding capital is one of the largest, and least examined, costs a financial business bears.

Here is the opportunity that follows. A great deal of the capital that institutions hold is held unnecessarily — trapped by crude measurement, conservative assumptions, inefficient structure and unexamined habit, rather than by any genuine requirement of the risks being run. Releasing that trapped capital, safely and without taking on a cent more risk, is among the highest-value things actuarial work can do. It is, in the most literal sense, finding money that was already there — and setting it free to work.

Why capital is the scarcest resource

To see why this matters, start with what capital is for. A financial institution promises to meet obligations — claims, deposits, withdrawals — whose timing and size are uncertain. Capital is the cushion that lets it keep those promises even when experience turns out worse than expected. Regulators set minimum requirements; prudent boards hold more. The amount required rises with the riskiness of the business, which is why measuring that risk accurately is the foundation of everything that follows.

What makes capital scarce is its cost. Equity capital, in particular, carries a high expected return — shareholders accept the risk of ownership only in exchange for it — so capital tied up unproductively is expensive dead weight. Every unit an institution holds beyond what it truly needs is a unit on which it must still earn that return, or accept a lower return on the whole. For the smaller institutions that characterise much of the Caribbean financial sector, where capital is both scarce and dear, the penalty for holding it inefficiently is especially severe — and the prize for freeing it especially large.

How capital gets trapped

Capital becomes trapped in several recognisable ways, and naming them is the first step to releasing it. The most common is crude measurement: an institution that assesses its required capital with blunt, conservative rules of thumb, rather than models that capture its actual risk profile, will almost always conclude it needs more than it does. Closely related is the failure to credit diversification — risks that partly offset one another, so that the whole is less risky than the sum of its parts, but that a simplistic approach adds together as though they would all go wrong at once.

Other traps are structural. Reinsurance bought without regard to its effect on required capital may cost more than the relief it provides, or miss the chance to transfer exactly the risks that consume the most capital. An asset portfolio poorly matched to the liabilities it backs generates market and interest-rate risk — and the capital to support it — that careful matching would remove. Reserves carrying redundant layers of prudence, beyond what a sound best estimate and a reasonable margin require, lock away capital needlessly. And business lines that earn less than their true cost of capital quietly consume the resource without paying for it. Each of these is a place where capital sits trapped, doing no work.

Releasing it: the optimisation levers

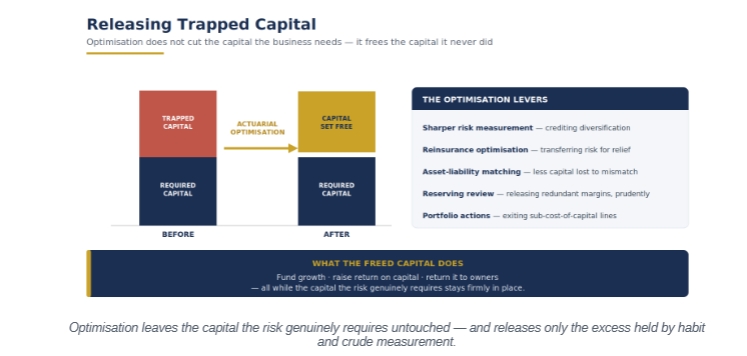

For every way capital becomes trapped, there is a lever to release it — and together these levers are what actuarial capital optimisation deploys. Sharper risk measurement, through economic-capital modelling that captures the true risk profile and credits diversification, often reveals that less capital is genuinely required than crude methods suggested. Reinsurance can be restructured so that it transfers precisely the risks that consume the most capital, releasing the buffer those risks demanded. Asset-liability matching reduces the market and interest-rate risk that mismatch creates, and the capital held against it.

Optimisation leaves the capital the risk genuinely requires untouched — and releases only the excess held by habit and crude measurement.

Two further levers complete the set. A disciplined reserving review can release margins that have accumulated beyond what prudence requires — carefully, and only where genuinely redundant. And portfolio actions — repricing or exiting lines of business that earn below their cost of capital — redirect the resource from where it is wasted to where it works. Applied together, and quantified rigorously, these levers can free a meaningful share of an institution’s capital. The released capital is then available for the uses that create value: funding growth, lifting the return on the capital that remains, or being returned to the owners who provided it.

This is optimisation, not under-capitalisation

A crucial distinction must be drawn clearly, because the whole idea collapses without it. Capital optimisation is not a euphemism for holding too little, for cutting corners, or for gaming a regulator. The capital that the risks genuinely require remains firmly in place; the business stays exactly as safe as it was. What optimisation removes is only the excess — capital held not because the risk demanded it but because the measurement was crude, the structure inefficient, or the margin redundant. Done properly, it makes an institution no riskier; it simply makes it no longer pay to hold capital it never needed.

This is why the work must be rigorous and honest. Releasing capital on the strength of an over-optimistic model, or by stripping out margins that turn out to have been necessary, is not optimisation but its opposite — a hidden weakening that will surface at the worst moment, exactly as earlier articles in this series warned of under-reserving and under-pricing. Genuine optimisation rests on better measurement, not wishful measurement; it withstands the scrutiny of regulators and auditors precisely because the required capital is unchanged. The safety of the institution is the constraint within which optimisation works, never the price it pays.

From holding capital to making it work

Optimisation is ultimately about a shift in mindset: from treating capital as a static buffer to be held, to treating it as a scarce resource to be allocated. The central tool is the return each part of the business earns on the capital it consumes. Measuring profitability per unit of capital — rather than profit alone — changes the questions a board asks. A line of business that looks profitable may be destroying value once the capital it ties up is counted; another that looks modest may be the most efficient user of capital in the institution. Seeing the business through this lens is what turns capital from a constraint into a strategic instrument.

This makes optimisation a continuous discipline rather than a one-off exercise. As the business changes, as risks evolve and opportunities appear, the efficient allocation of capital shifts with them. The institutions that build this thinking into how they run — pricing for it, structuring for it, and steering capital toward its most productive uses — compound an advantage over those that hold capital passively and wonder why their returns disappoint.

The Caribbean opportunity

For Caribbean financial institutions, capital optimisation is an unusually direct route to competitive advantage. These are, for the most part, smaller institutions for which capital is scarce and expensive, operating in markets where the ability to fund growth from freed capital can be decisive. Yet the actuarial and modelling techniques that release trapped capital remain underused across much of the region — which means the opportunity is largely unclaimed, and available to those who move first. An indigenous institution that masters capital efficiency can fund its own expansion, improve its returns, and compete with far larger international players on the strength of how well it uses what it has.

The region’s heavy reliance on reinsurance, often viewed purely as a cost, is itself an underexploited lever: structured thoughtfully, reinsurance is one of the most powerful tools for releasing capital, not merely transferring risk. Combined with sharper internal measurement and disciplined capital allocation, it offers regional institutions a way to do far more with the capital they have — which, in markets where raising fresh capital is hard and costly, may be the most valuable capability of all.

What a board should ask

For directors, capital optimisation begins with a handful of pointed questions. Do we know our true required capital, measured against our actual risk profile rather than a blunt rule? Where, specifically, is our capital trapped — in crude measurement, in unrewarded reinsurance, in mismatch, in redundant margins, in business that does not earn its keep? What return does each part of the institution earn on the capital it consumes? And how much capital could rigorous optimisation release, and to what use would we put it? A board that can answer these questions holds a lever over the institution’s returns that few of its competitors are even using.

Capital set free is not an accounting trick or a flattering of the numbers; it is real resource, released from where it was doing nothing to where it can build, earn and reward — without the institution carrying a cent more risk than before. For a financial business, and especially for a smaller one in a capital-scarce region, few capabilities are more valuable than the disciplined actuarial work that finds trapped capital and puts it to work. The buffer that protects the business stays exactly where it belongs. Everything above it, held only by habit and crude measurement, is value waiting to be released — and very often it is already sitting on the balance sheet, waiting to be set free.

| TAKE THE NEXT STEP

Request a Capital Optimisation Review We will measure your true required capital against your actual risk profile, identify where capital is trapped — in measurement, reinsurance, mismatch, margins or unprofitable lines — and quantify how much rigorous optimisation could release, and to what use, while keeping the business exactly as safe. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210