Almost every Caribbean territory runs a national social security scheme, and almost all face the same arithmetic: an ageing population, a shrinking contributor base, and benefits that will one day outrun the money coming in. The actuary’s task is to say when — and what it would take to change the answer.

Nearly every nation in the Caribbean operates a national insurance or social security scheme, and for millions of people across the region these schemes are the foundation of financial security in old age, sickness, injury and bereavement. They are among the most important institutions a small state maintains. They are also, in most cases, built on a financing model that the region’s changing demography is steadily undermining. The question that hangs over them is simple to ask and uncomfortable to answer: will the fund last?

It is not a rhetorical question, and it is not unanswerable. Social security schemes are among the most thoroughly modelled institutions in any economy, subject to regular actuarial review precisely so that their long-term health can be measured before it becomes a crisis. Those reviews, across the region and beyond, increasingly tell a consistent story: schemes designed in an era of young, growing populations are now ageing alongside the societies they serve, and on present settings many will spend more than they receive, draw down their reserves, and eventually face a financing gap. The value of the actuary’s work is that it converts that trajectory from a vague anxiety into a dated, quantified forecast — and shows what it would take to bend the curve.

How a pay-as-you-go scheme actually works

Most Caribbean social security schemes are financed on a pay-as-you-go basis. The contributions collected from today’s workers and their employers are used, in large part, to pay the benefits of today’s pensioners and claimants. This is fundamentally different from a funded pension, where each member’s contributions are invested to pay that member’s own future benefits. In a pay-as-you-go scheme there is an intergenerational promise at the centre: the current generation funds the last, in the expectation that the next generation will fund it in turn.

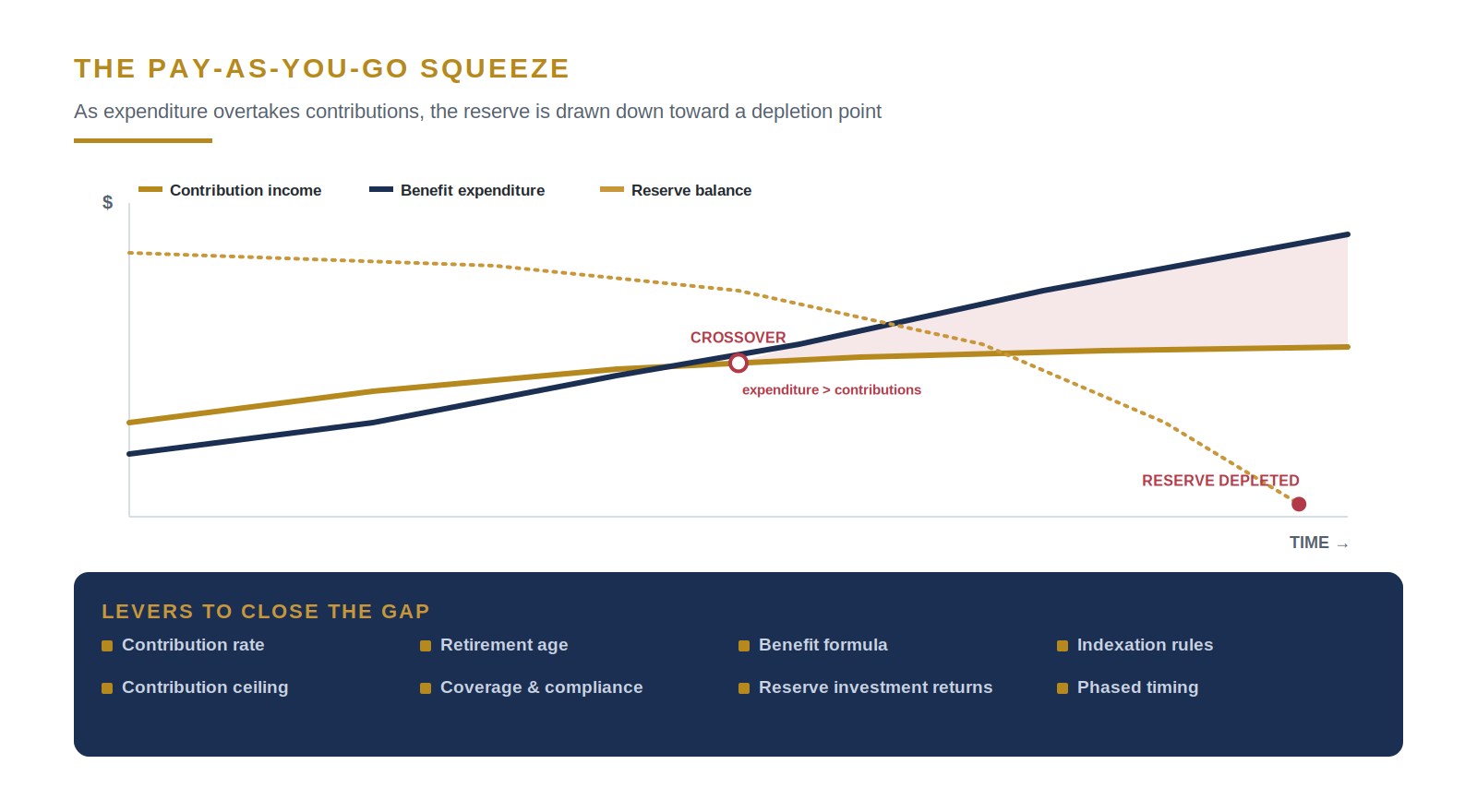

Figure 1 · As benefit expenditure overtakes contribution income, the reserve is drawn down toward depletion — unless the levers of reform are pulled in time.

Many schemes are not purely pay-as-you-go; they are partially funded, having accumulated a reserve during the decades when contributions comfortably exceeded benefits. That reserve, and the investment income it earns, is meant to cushion the system as it matures — to be drawn upon when contributions alone no longer cover benefits. The health of such a scheme therefore depends on three flows: the contributions coming in, the benefits going out, and the investment return on the reserve. As long as the first and third together cover the second, the scheme is sustainable. The difficulty is that the demographic forces now at work push all three in the wrong direction at once.

The demographic squeeze

The arithmetic of a pay-as-you-go scheme rests on the ratio of contributors to beneficiaries — how many working, contributing people there are for each person drawing a pension. When schemes were designed, that ratio was high: large young workforces supported relatively few retirees, and contributions easily covered benefits. Across the Caribbean, that ratio is falling, and for several reasons at once. People are living longer, so pensions are drawn for more years than the original design assumed. Fertility has declined, so each new generation entering the workforce is smaller than the one before. And emigration removes working-age contributors in particular, often the very people whose contributions the scheme most needs.

Each of these forces would strain a pay-as-you-go scheme on its own; together they compound. A longer-living, lower-fertility, high-emigration society produces exactly the demographic profile a pay-as-you-go scheme is least able to sustain: more beneficiaries, drawing for longer, supported by fewer contributors. This is not a failure of management or a sign of fraud. It is the predictable consequence of building a promise on a population structure that has since changed. The schemes are not broken; the demography beneath them has shifted, and the financing must shift with it.

| A pay-as-you-go scheme is only as strong as the ratio of contributors to pensioners — and across the region, that ratio is quietly falling. |

What the actuarial review reveals

The instrument that measures all of this is the statutory actuarial review, conducted periodically for every well-run scheme. The actuary projects the scheme’s income and expenditure decades into the future, on explicit assumptions about demography, the economy and the scheme’s own rules, and produces a small set of figures that tell the board and the government exactly where the scheme stands. The most important of these are easy to grasp. The pay-as-you-go cost rate is the contribution rate that would be needed, in any given year, for contributions alone to cover benefits; when it rises above the actual rate, the scheme is running an operating deficit and must draw on its reserve. The reserve-depletion year is the year that reserve is projected to run out on current settings. And the required long-term contribution rate is the level at which contributions would have to be set, today, to keep the promise sustainable over the projection horizon.

These figures are not predictions of doom; they are early-warning indicators, and their whole purpose is to give decision-makers time. A review that identifies a reserve-depletion year two or three decades away is not announcing a catastrophe — it is granting the breathing room to act gradually, while the options are still wide and the adjustments still gentle. The danger lies not in the numbers themselves but in ignoring them, because every year of inaction narrows the choices and sharpens the eventual remedy. A scheme that reads its actuarial reviews and acts on them can secure its future with modest, phased changes. A scheme that files them away cannot.

The levers of reform

When a review shows a scheme drifting toward imbalance, the response is a set of well-understood levers, each of which closes part of the gap and each of which carries a cost. Contributions can be raised, increasing the burden on workers and employers today. The retirement age can be increased, reflecting longer lives but extending working years. The benefit formula can be adjusted — the accrual rate, the earnings on which pensions are based, the way benefits are calculated — changing what future pensioners receive. Indexation rules, which govern how pensions rise after they begin, can be made less generous. The ceiling on insurable earnings can be raised, broadening the contribution base. Coverage and compliance can be improved, bringing the self-employed and the informal sector more fully into the system. And the reserve can be invested for better long-term returns within prudent limits.

No single lever is sufficient or painless, and each redistributes the cost of adjustment differently — between workers and pensioners, between today’s generation and tomorrow’s, between higher and lower earners. This is what makes reform politically difficult: there is no option that asks nothing of anyone. But the actuary’s role is not to make the political choice; it is to quantify each option and combination so that the choice can be made with open eyes. A well-modelled reform package typically blends several levers, each pulled modestly, so that no group bears the whole weight and the change is absorbed gradually rather than imposed abruptly.

| There is no reform that asks nothing of anyone. The actuary’s task is not to choose — it is to show, precisely, what each choice would cost and to whom. |

The cost of waiting

The single most important variable in social security reform is time, because the levers behave very differently depending on when they are pulled. A small increase in the contribution rate or a gradual rise in the retirement age, phased in over many years and applied mainly to those still far from retirement, can close a substantial gap with little disruption to any individual. The same adjustment forced through in a hurry, once a reserve is nearly exhausted, falls heavily and suddenly on people with no time to prepare — and may require cuts to benefits already in payment, the most painful and contested option of all.

Delay therefore does not preserve options; it destroys them. Each year a known imbalance goes unaddressed, the reserve that could have cushioned the transition shrinks, the cohort that could have absorbed a gentle change moves closer to retirement, and the eventual remedy grows larger. Reform undertaken early is a matter of fine-tuning; reform undertaken late is a matter of damage control. The schemes that will navigate the coming decades most successfully are not those with the most favourable demography — that is largely fixed — but those that read the warning early and acted while the adjustments were still small.

The Caribbean dimension

Several features sharpen the challenge in the regional context. Populations are small, so schemes lack the scale that lets larger systems absorb demographic shocks, and a single wave of emigration can move the contributor base materially. Informal and self-employed work is widespread, leaving many outside the contribution net and narrowing the base that must support a widening benefit obligation. And the reserves that are meant to cushion the transition are, in many territories, heavily invested in government securities — a concentration that ties the scheme’s financial health to the fiscal health of the very state that may need to call on it, and that limits the diversification a prudent reserve would otherwise seek.

There is also a direct fiscal dimension that boards and ministries cannot ignore. Because these schemes are public promises, a financing gap does not stay within the scheme; it becomes a contingent liability of the state, and ultimately a claim on the public purse. A social security shortfall and a fiscal crisis are not separate problems but two views of the same one. That linkage makes the sustainability of these schemes a matter of national economic management, not merely of social policy — and makes the early, quantified warning the actuary provides a strategic asset for the whole of government, not just for the scheme’s trustees.

What stewards should do

The first responsibility of those who govern these schemes is to commission rigorous, regular actuarial reviews and — crucially — to act on them rather than receive them. The second is to model reform options early and in combination, so that when adjustment is needed the menu of phased, balanced packages is already understood rather than improvised under pressure. The third is to broaden coverage and strengthen compliance, drawing the informal and self-employed into the system both to widen the contribution base and to extend protection to those who most need it.

The fourth is to manage the reserve with genuine diversification and a long-term investment discipline, reducing the concentration that ties the scheme too tightly to a single issuer. And the fifth is to communicate honestly: the public will accept gradual, fair, well-explained reform far more readily than a sudden shock, and the legitimacy of any change depends on the trust that candour builds. Stewardship of a social security scheme is, in the end, an exercise in honouring a promise across generations — and a promise can only be kept if its true cost is measured and met in time.

Will the fund last? On present settings, for many schemes, the honest answer is: not without change. But that is not a counsel of despair; it is a call to foresight. The demography is known, the trajectory is measurable, and the levers are understood. What remains is the will to read the warning while it is still early and to make the modest, fair adjustments that secure the promise for the generations still to come. A scheme that does this will endure. The only schemes genuinely at risk are those that mistake the quiet of an undepleted reserve for the absence of a problem — and wait, as the arithmetic compounds, for the day the question answers itself.

| TAKE THE NEXT STEP

Request a Scheme Sustainability Briefing We will help you read your scheme’s actuarial position — its pay-as-you-go cost rate, reserve-depletion outlook and required contribution rate — and model phased, balanced reform options that secure the promise without abrupt shocks. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210