Climate risk has stopped being an environmental footnote and become a financial one. It reaches the balance sheet through two channels — physical and transition — and the organisations that quantify it early will navigate the decade ahead far better than those that wait to be told.

For most of the last two decades, climate change sat in the corporate consciousness as a matter of reputation and responsibility — a topic for the sustainability report, the corporate-citizenship page, the annual statement of good intentions. It rarely touched the numbers. That separation is now ending. Climate risk has become a financial risk, with direct and measurable consequences for the value of assets, the size of liabilities, the cost of capital and, in the most exposed cases, the viability of the enterprise itself. The question facing Caribbean boards is no longer whether climate belongs in the financial statements, but how large its footprint already is and whether anyone has measured it.

The shift is being driven from several directions at once. Investors and lenders increasingly price climate exposure into the terms they offer. Insurers and reinsurers are repricing or withdrawing from the most exposed risks. Regulators and standard-setters are moving climate disclosure from voluntary to mandatory. And the physical events themselves — stronger storms, higher seas, hotter and drier seasons — are translating directly into impairments, repair bills and lost revenue. For a region as exposed as the Caribbean, the cost of treating climate as someone else’s concern is a balance sheet that no longer reflects reality.

From environmental concern to financial number

The mechanism by which climate becomes a financial number is more concrete than many boards assume. A coastal hotel battered by successive storms faces real impairment of its property and a shortened useful life for assets exposed to salt, wind and flood. A lender to agriculture or fisheries faces rising expected credit losses as borrowers’ livelihoods are disrupted by drought or changing seas. A manufacturer dependent on imported fossil fuel faces a cost base that moves with carbon policy abroad. An insurer faces claims that no longer behave as the historical record predicted. In each case the effect is not abstract; it lands in a specific line of the financial statements, governed by a specific accounting standard, and it can be estimated.

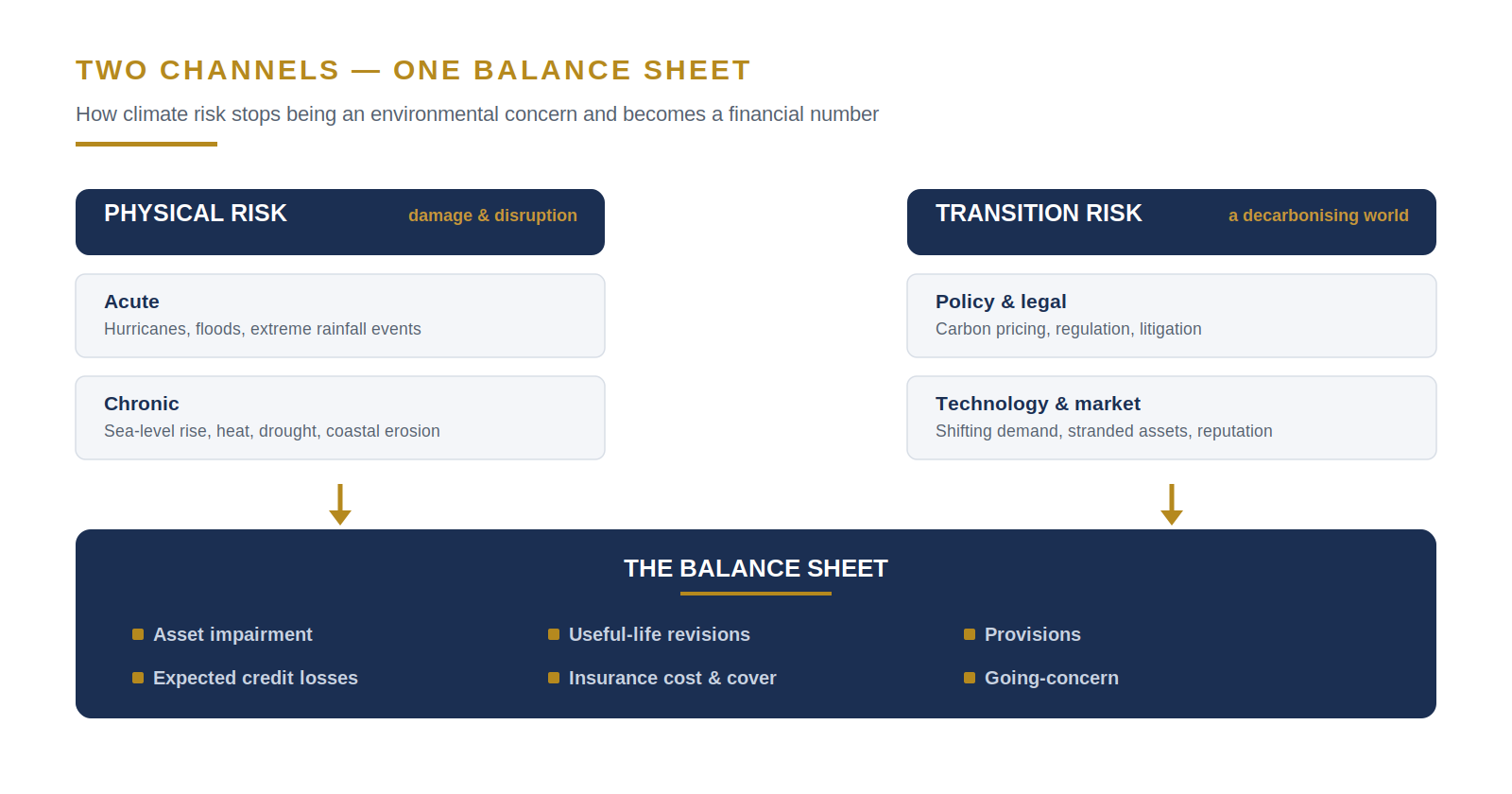

Figure 1 · Climate risk reaches the financial statements through two channels — physical and transition — each with distinct, measurable balance-sheet effects.

What has changed is that these effects can no longer be deferred indefinitely as future possibilities. Accounting standards require entities to reflect conditions that exist at the reporting date and reasonable expectations about the future. As climate impacts move from the speculative to the foreseeable, the accounting that recognises them moves with them. An asset that will plausibly be stranded, a liability that will plausibly crystallise, a loss that is now reasonably expected — these are matters the financial statements are designed to capture, and auditors are increasingly asking whether they have been.

The two channels — physical and transition risk

Climate risk reaches an organisation through two distinct channels, and a board needs to understand both because they behave very differently. Physical risk is the risk of direct harm from a changing climate. It divides into acute risk — discrete, severe events such as hurricanes, floods and extreme rainfall, the perils explored in the preceding article on parametric cover — and chronic risk, the slow, grinding pressures of sea-level rise, rising temperatures, drought and coastal erosion that erode value over years rather than hours. Acute risk threatens sudden loss; chronic risk threatens the long-term usability and worth of assets and locations.

Transition risk is the risk that arises not from the climate itself but from the world’s response to it. As economies decarbonise, policy and legal changes — carbon pricing, emissions regulation, climate litigation — alter the cost of doing business. Technology and market shifts change what customers want and what assets are worth, leaving some investments stranded before the end of their intended lives. Reputation moves with all of it. For a Caribbean economy that contributes little to global emissions, transition risk can feel like someone else’s problem, but it is not: the region imports fuel, vehicles, equipment and capital from economies that are decarbonising, and the cost and availability of all of them will shift as that transition accelerates.

| Physical risk is the climate acting on the business. Transition risk is the world’s response to the climate acting on the business. A complete picture requires both. |

Where climate lands on the balance sheet

The value of framing climate this way is that each channel maps onto identifiable accounting outcomes. Physical and transition risks can impair the carrying value of property, plant and equipment, triggering write-downs under the impairment standard. They can shorten the useful lives or reduce the residual values of long-lived assets, changing depreciation. They can give rise to provisions for obligations such as decommissioning, remediation or restructuring. They can increase the expected credit losses that lenders must recognise against loans to exposed borrowers. They can raise the cost and reduce the availability of insurance, leaving more risk retained on the balance sheet. And in severe cases they bear on the most fundamental judgement of all — whether the entity remains a going concern.

None of these is a new accounting concept. Impairment, useful-life review, provisioning, expected credit losses and going-concern assessment are long-established disciplines. What climate does is supply a powerful new source of the conditions that trigger them, and demand that the assumptions behind them be revisited. A useful life set years ago on the assumption of a stable climate, an impairment test run on cash-flow projections that ignore physical risk, an expected-loss model calibrated only on benign history — each is now potentially wrong, and correcting it is not a matter of new rules but of applying existing ones to a changed world.

Scenario analysis — the actuarial core

Because climate risk unfolds over long and uncertain horizons, it cannot be captured by a single point estimate. The discipline that has emerged to quantify it is scenario analysis: modelling how an organisation’s exposures, cash flows and asset values behave under several plausible climate futures rather than one. A typical framework tests an orderly transition, in which the world decarbonises in a smooth and predictable way; a disorderly transition, in which action is delayed and then abrupt; and a high-physical-risk pathway, in which little is done and the physical consequences dominate. Each pathway implies a different mix of physical and transition effects, and a different impact on the numbers.

This is quantitative, forward-looking, assumption-driven work — the natural territory of the actuary and the climate-risk modeller. Physical risk is quantified using catastrophe models for acute perils and long-range projections for chronic ones, translating hazard into expected damage and loss. Transition risk is quantified by modelling the effect of carbon prices, demand shifts and asset obsolescence on revenue and cost. The outputs are then carried into the financial statements as revised impairment tests, expected-loss estimates and provisions. Scenario analysis does not predict the future; it disciplines the organisation to ask, in concrete financial terms, what each plausible future would do to it — and to act before the answer is forced upon it.

| Scenario analysis does not forecast which future will arrive. It tells a board what each plausible future would cost — which is exactly what a board needs to decide today. |

Disclosure is no longer optional

The expectation that organisations measure and report climate risk is hardening into requirement. The International Sustainability Standards Board has issued global baseline standards for sustainability and climate disclosure, building on the widely adopted recommendations of the Task Force on Climate-related Financial Disclosures, and jurisdictions around the world are moving to adopt or reference them. The direction of travel is unmistakable: climate-related financial disclosure is becoming a mainstream component of corporate reporting, subject to the same expectations of rigour and, increasingly, assurance as the financial statements themselves.

For Caribbean organisations, this matters even where local mandates are still developing, because the requirement often arrives through the market rather than the statute book. Regional firms that raise capital abroad, borrow from international lenders, supply multinational customers or seek reinsurance are increasingly asked to disclose climate exposure on these frameworks regardless of domestic rules. An organisation that has never quantified its climate risk will struggle to answer, and the absence of an answer is itself becoming a competitive and financing disadvantage. Measuring early is no longer caution; it is preparation for questions that are already being asked.

The Caribbean dimension

The Caribbean sits at the sharp end of physical risk. Its economies are concentrated in exactly the assets climate threatens most — coastal tourism, ports, fisheries, agriculture and the infrastructure that supports them — and its geography exposes it to the full force of hurricanes, flooding, sea-level rise and coral and coastal degradation. A single category of risk can touch a large share of the productive base at once, with little internal diversification to absorb it. On the physical channel, few regions have more at stake.

The transition channel cuts in a more complicated way. The region’s direct emissions are small, so the cost of its own decarbonisation is modest; but its dependence on imported fuel and goods means it is highly exposed to how others decarbonise, and to the carbon costs embedded in global supply chains. At the same time, the retreat of insurers from the most exposed risks is widening a protection gap that throws more climate risk back onto corporate and sovereign balance sheets. The combination — acute physical exposure, indirect transition exposure and a narrowing insurance safety net — makes climate quantification not a disclosure exercise imported from abroad but a matter of regional financial self-knowledge, and one that depends on local data and judgement to get right.

What a board should do

The first task is to identify exposure honestly across both channels: where the organisation’s assets, operations, borrowers and markets are vulnerable to physical events and chronic change, and where they are exposed to the costs and shifts of a decarbonising world. The second is to quantify that exposure through scenario analysis, translating each plausible climate future into concrete effects on cash flows, asset values and liabilities rather than leaving it as narrative. The third is to carry those results into the financial statements where they belong — into impairment tests, useful-life and provision reviews, expected-loss models and going-concern assessments — so that the accounts reflect the risks the organisation actually carries.

The fourth is to integrate the findings into strategy and capital allocation, because the purpose of measurement is better decisions, not merely better disclosure. A board that knows which assets are most exposed, which markets are most at risk and which costs will move with the transition can invest, divest, insure and adapt deliberately rather than react to events. And the fifth is to disclose credibly, on the emerging frameworks, both because it will increasingly be required and because the organisations that can show their working will command the confidence of lenders, investors and insurers that those who cannot will steadily lose.

Climate has already arrived on the balance sheet of every exposed Caribbean enterprise, whether or not anyone has written down the number. The storms, the seas and the global transition are not waiting for the accounting to catch up. What an organisation can still choose is whether to measure its exposure deliberately, on its own terms and timetable, or to have it revealed all at once — by an impairment it did not foresee, a loss it did not provide for, an insurer that will no longer cover it, or a lender that has already done the calculation it neglected to do. Quantifying what the region can no longer ignore is not an act of pessimism. It is the discipline of seeing clearly, in financial terms, a future that has already begun — and the first condition of being ready for it.

| TAKE THE NEXT STEP

Request a Climate Risk Exposure Scan We will help you map your climate exposure across both physical and transition channels, quantify it through scenario analysis, and show where it lands on your balance sheet — in impairment, useful lives, provisions, expected credit losses and going-concern judgement. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210