When a hurricane strikes, money is needed in days but traditional insurance pays in months. Parametric cover closes that gap — paying a pre-agreed sum the instant a measurable trigger is crossed. Its value, and its danger, lie almost entirely in how the trigger is designed.

When a major hurricane crosses a Caribbean island, the damage is visible within hours. The need for cash is just as immediate: emergency shelter, debris clearance, the restoration of power and water, repairs to ports and roads, and support for the businesses and households whose income has suddenly stopped. Yet the money that traditional insurance is meant to provide often arrives months later, once assessors have inspected each claim and losses have been adjusted one by one. For a small-island economy, the gap between when funds are needed and when they actually arrive is not a mere inconvenience. It can be the difference between a swift recovery and a lost year.

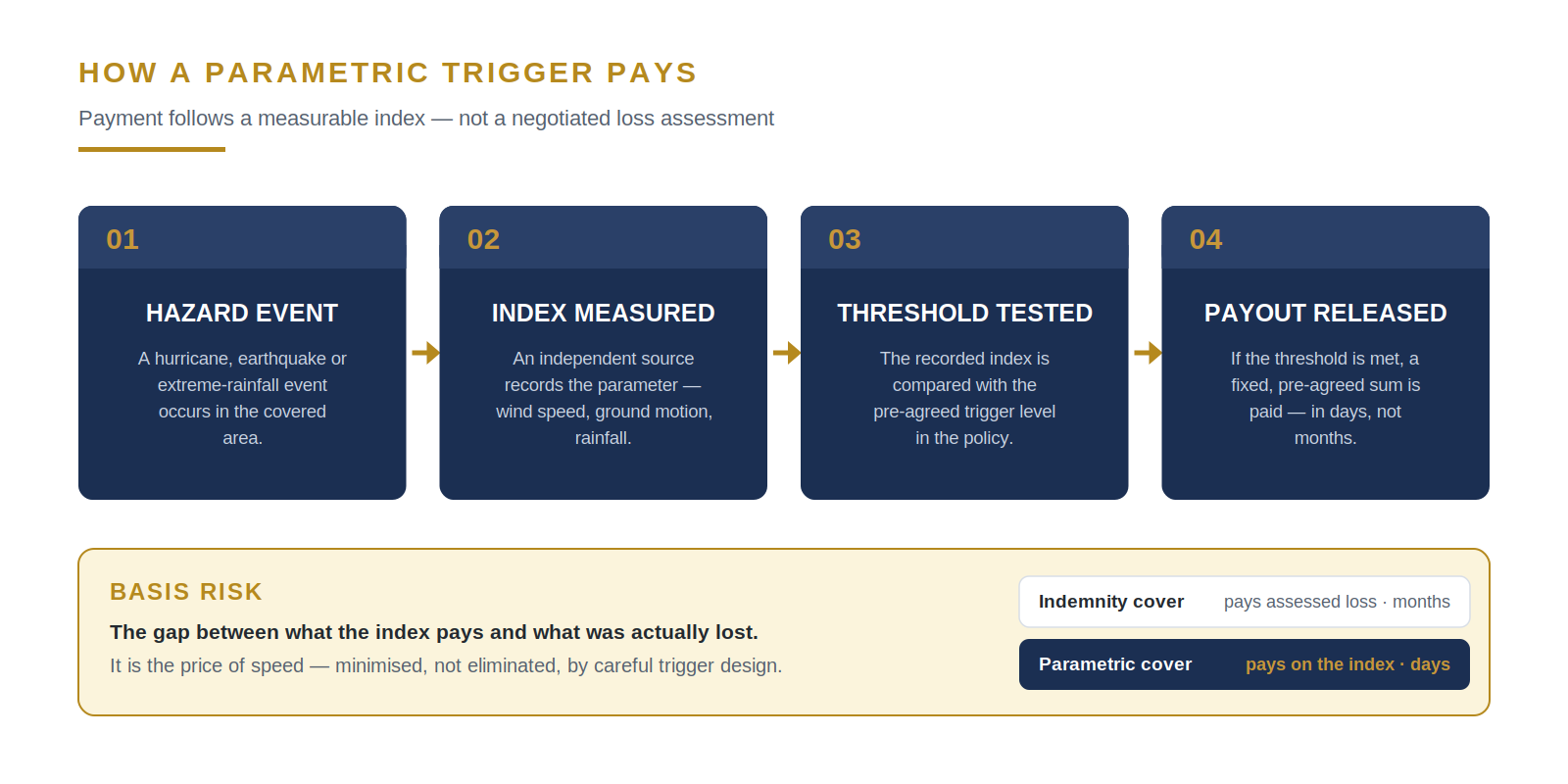

Parametric insurance was designed to close that gap. Instead of paying against the assessed value of what was lost, it pays a pre-agreed amount the moment a measurable trigger — a wind speed, a level of ground shaking, a volume of rainfall — crosses a defined threshold. The payment is fast, certain, and tied to an objective index rather than a negotiated loss. Used well, it gives a government, a utility or a business the liquidity to act in the critical days after a disaster, when speed matters most. Used carelessly, it can pay handsomely when little was lost and fall short when the damage is severe. The difference lies almost entirely in design — which is where the actuary earns the fee.

Figure 1 · A parametric payout follows an objective index, not a negotiated loss — with basis risk as the trade-off for speed.

Why the protection gap is widest in small islands

Caribbean economies sit among the most catastrophe-exposed in the world. They lie in the path of hurricanes, astride active seismic zones, and increasingly in the way of extreme rainfall and flood. What makes the exposure so consequential is not only the frequency of events but the size and shape of the economies that absorb them. A single severe storm can damage assets and disrupt output equivalent to a substantial share of national income in one stroke — a concentration of risk that larger, more diversified economies rarely face. There is nowhere for the loss to be spread internally; the whole island is the portfolio.

Traditional cover responds poorly to this reality. Reinsurance capacity for peak Caribbean perils is expensive and, in hard markets, scarce. Indemnity claims take time to adjust precisely when speed is most valuable, and the administrative effort of assessing thousands of individual losses is itself a casualty of the event. The result is a wide protection gap — the difference between the economic losses a disaster inflicts and the share that is insured — and a fiscal one, as governments are forced to divert budgets, borrow on unfavourable terms, or wait on donor support to fund a recovery that cannot wait. It is into this gap that parametric cover is built to step.

How parametric cover actually works

A parametric, or index-based, policy rests on four elements. The first is the hazard it responds to — wind, earthquake, rainfall or another measurable peril. The second is the index: an objective, independently measured parameter that stands in for the severity of the event, such as maximum sustained wind speed within a defined area, peak ground acceleration at a location, or millimetres of rainfall over a period. The third is the trigger: the threshold the index must cross before the policy responds. The fourth is the payout structure that determines how much is paid once it does.

That structure can take several forms. A binary trigger pays the full sum insured if the threshold is breached and nothing if it is not. A tiered structure pays in steps as the index passes successive levels — a moderate payment for a Category 3 wind, a larger one for a Category 5. A proportional or linear structure scales the payment continuously with the severity of the index between an attachment point, where payments begin, and an exhaustion point, where the full limit is reached. Crucially, the measurement comes from an independent third party — a meteorological agency, a seismic network, satellite data or a recognised catastrophe model — so that neither insurer nor insured can influence the figure that decides the claim.

The consequences of that design are what make the instrument valuable. Because there is no loss to adjust, payment can be made in days rather than months. Because the trigger is objective, there is little to dispute. Administrative cost is low, the timing of cash is predictable, and risks that are difficult or impossible to insure conventionally — highly correlated, hard to assess, or simply too fast-moving — become transferable. For an economy that needs liquidity at the moment of impact, that combination of speed and certainty is the whole point.

Basis risk — the price of speed

The same feature that gives parametric cover its speed creates its central weakness. Because the payout follows an index rather than the actual loss, the two will never match perfectly. The difference between them is called basis risk, and it cuts both ways. Positive basis risk arises when the policy pays more than was lost — a windfall, welcome to the insured but a sign the trigger was set generously. Negative basis risk is the dangerous one: a real and severe loss occurs, but the measured index falls just short of the threshold, or the damage is driven by a peril the index does not capture, and the policy pays little or nothing. A community devastated by flooding from a storm that never reached the trigger wind speed has felt negative basis risk at its worst.

Basis risk cannot be eliminated; it is inherent in the trade of precision for speed. It can, however, be measured and managed. The art of parametric design is to choose an index that tracks actual loss as closely as the available data allow, to calibrate the trigger and payout to the specific vulnerability of what is being protected, and to be honest with the buyer about the residual gap that remains. A well-designed programme does not pretend basis risk away. It makes the trade-off deliberate and visible, so that the board or the finance ministry buying the cover knows exactly what it is — and is not — protected against.

Designing the trigger — where the actuary earns the fee

Good trigger design is a quantitative discipline. It begins with the catastrophe model: a probabilistic representation of how often events of each severity strike, and what damage they cause to the specific exposure in question. From that model the actuary derives the loss exceedance curve — the relationship between the size of a loss and the probability of exceeding it in a year — and from that curve the figures that price the cover: the average annual loss, the losses associated with return periods such as one-in-fifty or one-in-one-hundred years, and the points at which a layer of protection should attach and exhaust. The pure premium is, in essence, the modelled expected payout; the commercial premium adds loadings for uncertainty, capital and expenses.

The harder judgement is choosing the index and structure that make the payout track loss. A trigger that is too simple is robust and cheap to operate but tracks loss loosely, widening basis risk; one that is too elaborate tracks loss well but becomes opaque and harder to trust. Multi-zone triggers, weighting several measurement points across an island, can sharpen the fit. So can blending perils, or using modelled rather than directly measured loss as the index. Each refinement narrows basis risk at the cost of simplicity, and the right balance depends on the exposure, the data available and the buyer’s appetite. This calibration — matching an objective, payable index to a real and irregular pattern of loss — is the heart of the work, and it is unmistakably actuarial.

Where parametric fits — and where it does not

Parametric cover is a complement to traditional insurance, not a replacement for it. It excels at delivering rapid liquidity, at covering peak and correlated risks that indemnity markets price punishingly, and at providing contingent financing that can be relied upon to arrive on a known timetable. It is less suited to being the sole protection for the full, detailed rebuilding of a specific asset, where indemnity cover that pays the actual repair bill remains the better tool. The two are designed to sit together.

The clearest way to see the fit is through the logic of layered disaster-risk financing. Frequent, low-severity losses are best retained — met from reserves, contingency budgets or a contingency line of credit — because insuring them is uneconomic. A middle layer of less frequent, more damaging events suits conventional and parametric insurance. The extreme tail — the rare, economy-shaking catastrophe — can be transferred to the capital markets or a sovereign risk pool. Parametric instruments appear across the middle and upper layers precisely because that is where speed and certainty of payment matter most, and where traditional cover is slowest and dearest.

The instruments — from the household to the sovereign

Parametric design now operates at every scale in the region. At the sovereign level, the Caribbean Catastrophe Risk Insurance Facility — CCRIF SPC, the world’s first multi-country risk pool — provides member governments with parametric cover for hurricanes, earthquakes and excess rainfall, paying out within weeks of a qualifying event to fund the immediate response. By pooling risk across many countries and retaining some while transferring the rest to reinsurers and capital markets, it delivers cover far more cheaply than any single small state could obtain alone.

At the apex of the structure sit catastrophe bonds and other insurance-linked securities, which transfer extreme tail risk directly to investors who receive an attractive yield in return for accepting that their principal may be lost if a defined event occurs; the World Bank has helped bring such instruments to the region. At the other end of the scale, parametric microinsurance extends the same logic to those least able to absorb a shock — smallholder farmers, fisherfolk and micro-enterprises — paying small, fast sums when a wind or rainfall index is triggered. In between, individual corporations — hotels, ports, utilities and agribusinesses — increasingly buy parametric wind, quake or rainfall cover to protect cash flow and bridge business interruption while their conventional claims are still being assessed.

The Caribbean dimension

Two regional forces are pushing parametric cover up the agenda. The first is climate change, which is altering the frequency and intensity of the perils the region faces and steadily raising the cost of doing nothing. The second is the maturing of the institutions, data and expectations around disaster-risk financing: ministries of finance, development lenders and rating agencies increasingly expect a coherent, pre-arranged financing strategy rather than an after-the-event scramble, and parametric instruments are a natural part of that strategy.

The regional context also raises the stakes on design. A trigger calibrated on imported assumptions — generic wind fields, foreign vulnerability curves, mainland rainfall patterns — will fit Caribbean exposure poorly and widen basis risk in exactly the conditions where it must not. Sound parametric cover for the region depends on local hazard data, local knowledge of how Caribbean structures and economies actually fail under stress, and judgement grounded in the territories being protected. It is a field in which regional understanding is not a marketing line but a technical necessity.

What a board — or a finance ministry — should do

The first step is to quantify the exposure and, just as importantly, the liquidity gap a severe event would open: how much cash would be needed, how quickly, and from where it would otherwise come. The second is to decide, layer by layer, what to retain and what to transfer — matching frequent small losses to reserves and contingency credit, and reserving insurance and parametric cover for the layers where they earn their cost. The third is to design any parametric layer properly, with the modelling and trigger calibration needed to keep basis risk within understood and acceptable bounds.

The fourth is to treat parametric cover as one component of a deliberate disaster-risk-financing strategy rather than a product bought in isolation — integrated with reserves, contingent credit and traditional insurance into a single, coherent stack. The fifth is to revisit the whole arrangement regularly, because both the hazard and the exposure are moving: climate is shifting the perils, and economic growth is changing what is at risk. A programme calibrated once and left to drift will, in time, protect against a world that no longer exists.

The storm will come; the only open question is whether the island is financially ready for it. Parametric cover does not stop the wind or still the ground, and it does not replace the patient work of building back what is lost. What it does is put money where it is needed, in the days when nothing else can, and convert a measurable event into immediate, certain support. Designed with care — the right index, an honest reckoning with basis risk, and a place within a wider financing strategy — it is among the most powerful tools a small, exposed economy has to turn the inevitability of catastrophe into something it can plan for, price, and survive.

| TAKE THE NEXT STEP

Request a Catastrophe & Parametric Briefing We will map your catastrophe exposure, quantify the liquidity gap a severe event would open, and show how a well-designed parametric layer — calibrated to minimise basis risk — can sit alongside your reserves, contingency credit and traditional cover. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global About Dawgen GlobalDawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing. The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress. To explore a partnership, reach out:

|