Beyond pensions, IAS 19 captures gratuities, long-service awards, post-retirement medical cover and accumulated leave. Unfunded and long-dated, these obligations are routinely under-provided — until an actuary measures them properly.

Most boards know there is a number on their balance sheet for the pension plan. Far fewer are confident about the other employee-benefit obligations sitting beside it — the retirement gratuity promised after long service, the lump sum paid at twenty-five years, the medical cover that continues into retirement, the accumulated sick or vacation leave that vests and is eventually paid out. These promises are real, they are often unfunded, and they have a way of being recorded at whatever rough figure seemed reasonable years ago, while the true obligation quietly grows beneath them. They are, for many organisations, the liability on the balance sheet most likely to be materially understated.

The accounting standard that governs all of this, IAS 19, is titled simply “Employee Benefits,” and the breadth of that title is the point. It reaches well beyond pensions to capture every form of consideration an entity gives in exchange for service. Some of those benefits are easy to account for and hard to get wrong. Others require the same actuarial machinery as a pension, are highly sensitive to assumptions, and are routinely under-provided precisely because they look smaller and softer than they are.

What IAS 19 actually covers

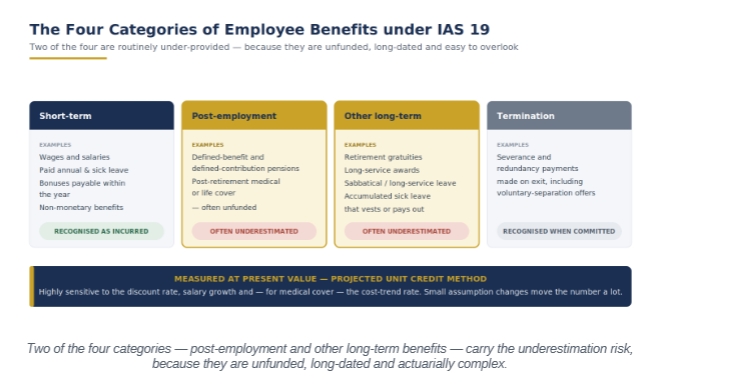

The standard sorts employee benefits into four categories, and the distinction matters because each is measured differently. Short-term benefits — wages, salaries, paid annual and sick leave, and bonuses expected to be settled within the year — are the simplest: they are recognised as the employee renders the service, with little estimation involved. Termination benefits, paid when employment is ended rather than in exchange for service, are recognised when the entity is demonstrably committed to the termination. These two categories rarely cause trouble.

It is the other two that do. Post-employment benefits include not only pensions but post-retirement medical and life cover — promises that extend for the remainder of a member’s life and, in the case of medical cover, rise with the relentless climb of healthcare costs. Other long-term benefits include retirement gratuities, long-service awards, sabbatical and long-service leave, deferred compensation, and accumulated leave that vests. Both categories are typically unfunded, both stretch far into the future, and both must be measured at present value using actuarial techniques. They are where the underestimation lives.

Why these liabilities get underestimated

The reasons these obligations are understated are rarely dishonest; they are structural. The first is that they are unfunded. A pension plan usually has assets, a trustee, an annual valuation and a funding requirement — a whole apparatus that forces attention. A retirement gratuity or a post-retirement medical promise often has none of that. There is no fund, no cash call, no external party insisting on rigour, and so the obligation can sit on the books at a figure that was never properly calculated.

The second reason is that they are long-dated and assumption-driven. The cost of a gratuity payable decades from now, or of medical cover that will be drawn for the rest of a retiree’s life, depends on assumptions about salary growth, how long people will stay, how long they will live, and — for medical benefits — how fast healthcare costs will rise. Small changes in any of these move the number substantially. A liability calculated on a crude basis, or on assumptions set years ago and never revisited, can be wrong by a wide margin without anyone noticing until it is formally valued.

The experience that follows is a familiar one. A company that has carried a retirement-gratuity provision for years at a figure built up from simple accruals commissions its first proper actuarial valuation — often because a new auditor insists. The actuary projects the gratuities that will actually be paid as current employees reach retirement, allowing for salary growth and length of service, and discounts them to today. The resulting obligation is materially larger than the figure on the books, sometimes by a wide margin, and the difference must be recognised. Nothing improper had occurred; the promise had simply never been measured properly, and a rough accrual is no substitute for a projection of what will genuinely be paid.

The medical-cost trap

Post-retirement medical benefits deserve particular attention, because they combine every feature that makes a liability dangerous. They are paid for life, so they are exceptionally long-dated. They are exposed to medical-cost inflation, which has historically outpaced general inflation by a meaningful margin and shows little sign of stopping. And they are highly sensitive to the assumed rate at which those costs will grow — the medical-cost trend rate — which compounds over decades. An organisation that has promised to cover retirees’ health costs, and that values the promise using an optimistic trend assumption or no proper valuation at all, may be carrying a fraction of the true liability on its books. When the obligation is finally measured properly, the increase can be startling.

How it is measured — and why that matters

Each of these obligations is measured using the projected unit credit method, the same actuarial approach used for defined-benefit pensions. In essence, the actuary projects the future benefit payments the entity has promised, allowing for salary increases, withdrawals, mortality and — where relevant — medical inflation, and then discounts those payments back to a present value using a discount rate based on high-quality corporate or government bonds. The result is a single figure that represents, in today’s money, the cost of promises already earned.

What matters for a board is the sensitivity of that figure. Because the obligation is the discounted value of cash flows stretching decades into the future, it moves sharply with the discount rate: a fall in long-term yields inflates the liability, just as it does for pensions. It moves with salary and medical-cost assumptions. And it moves with demographic assumptions about turnover and longevity. A proper valuation does not just produce a number; it shows how that number responds to each assumption — which is exactly the information a board needs to understand the risk it is carrying, and to judge whether the figure on its balance sheet is credible.

As with pensions, the year-to-year changes in these obligations do not all flow through profit. The effect of changes in actuarial assumptions — the remeasurements — is generally recognised in other comprehensive income, while the cost of benefits earned in the year and the interest on the obligation pass through profit and loss. The practical consequence is that a long-understated liability, once corrected, can move the financial statements in ways that surprise readers who were unprepared for it — one more reason to measure early and track the number deliberately rather than confront it all at once.

The Caribbean dimension

These obligations are widespread across the Caribbean, often more so than in larger economies. Retirement gratuities and long-service awards are common features of regional employment, frequently embedded in collective agreements or long-standing practice. Post-retirement medical promises exist in parts of the public sector and in older established companies. Accumulated leave that pays out on retirement is routine. Yet many of these obligations have never been actuarially valued, or were valued once and left to drift, and a significant number of regional employers carry them at figures that would not survive a rigorous assessment.

The regional context sharpens the issue in two ways. Audit and regulatory expectations have risen, and auditors increasingly require these liabilities to be measured properly rather than estimated; a long-ignored obligation can surface as a material adjustment at exactly the wrong moment. At the same time, the data and assumptions needed to value them well — local mortality, withdrawal patterns, medical-cost trends — require genuine regional knowledge rather than imported tables. The combination means that an unmeasured employee-benefit liability is both more likely to exist and more likely to be misjudged when it is finally addressed.

What a board should do

The first step is simply to know what the organisation has promised. Many boards would be unable to list, with confidence, every employee-benefit obligation the entity carries — and an obligation that is not catalogued cannot be measured. A complete inventory of benefits, drawn from contracts, collective agreements, policies and custom, is the foundation. The second step is to have the material long-term and post-employment obligations valued properly, by an actuary, on current and realistic assumptions — and to refresh that valuation regularly rather than treating it as a one-off.

The third step is to treat the result as management information, not merely a disclosure. A board that understands the size of these liabilities, the assumptions behind them and their sensitivities can make better decisions about benefit design, funding and risk — and can avoid the unwelcome surprise of a long-understated number being corrected all at once. The goal is not to discourage generous benefits; it is to ensure the organisation knows the true cost of the promises it has made, and accounts for them honestly.

The promises an organisation makes to its people are among the most honourable commitments it carries — and among the easiest to underestimate. Unlike a pension fund, an unfunded gratuity or a post-retirement medical promise makes no noise, demands no cash today, and sits quietly on the balance sheet at whatever figure it was first given. IAS 19 exists to ensure those promises are measured and reported for what they really are. The organisations that take that seriously — cataloguing what they have promised, valuing it properly, and watching how it moves — protect themselves from an unpleasant surprise and honour their commitments with their eyes open. The liability you may be underestimating is not a reason for alarm. It is simply a number worth knowing before someone else insists that you know it.

| TAKE THE NEXT STEP

Request an Employee-Benefit Liability Assessment We will help you catalogue every employee-benefit promise your organisation carries, value the material long-term and post-employment obligations on realistic assumptions, and show your board the size, drivers and sensitivities of a liability that may be larger than the books suggest. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210