Once a signature at the back of an annual return, the appointed actuary is becoming a strategic guardian of solvency — and regional regulators are steadily raising the bar.

For most of its history, the role of the appointed actuary was easy to summarise and easy to underestimate: value the policy liabilities, certify that the reserves were adequate, sign the statutory return, and step back until the following year. The appointment was real and legally required, but in many insurers it was treated as a once-a-year formality — a signature at the back of a document few directors read closely. That description is now badly out of date, and any board that still holds it is misreading one of its most important relationships.

Across the Caribbean, the appointed actuary is evolving into something closer to a continuous guardian of an insurer’s financial health. Regulators are widening the mandate, deepening their expectations, and leaning on the actuary’s independent judgement as a second line of defence for policyholders. For insurers, this is not a compliance nuisance to be managed. Handled well, it is one of the most valuable safeguards an institution can have; handled poorly, it is a warning system left switched off.

From signature to safeguard

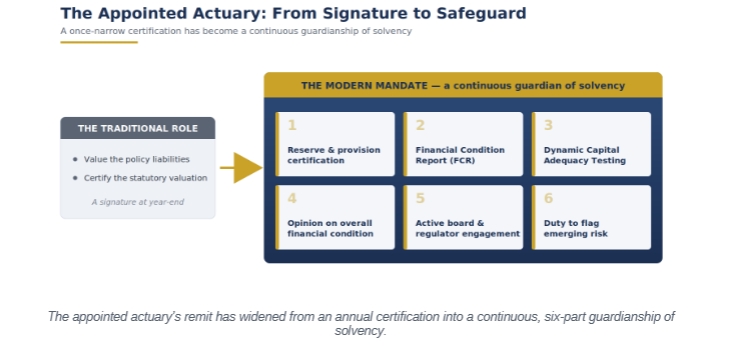

Understanding the change requires understanding what the role used to be. Traditionally, the appointed actuary’s core duty was the valuation of policy liabilities — estimating, with appropriate prudence, the reserves an insurer needed to meet its obligations to policyholders — and the certification of that valuation in the statutory return. It was essential work, because the reserve is the largest and most uncertain number on a life insurer’s balance sheet. But its scope was narrow and its rhythm annual: the actuary measured, certified and moved on.

That narrowness is precisely what regulators and the profession came to see as a weakness. A solvency problem rarely announces itself at year-end on a convenient schedule; it builds quietly across reserves, capital, investment strategy and new-business pricing, in ways an annual reserve certificate was never designed to catch. The modern conception of the role is a direct answer to that gap.

The role also has the deepest history in life insurance, where long-dated liabilities make actuarial judgement unavoidable — but the same logic is steadily extending across the market. General insurers face their own reserving uncertainty in long-tail claims and catastrophe exposure, and supervisors increasingly expect rigorous actuarial sign-off there too. The direction of travel is unmistakable: more of the balance sheet, across more of the industry, now falls squarely within the actuary’s view.

The expanding mandate

Today’s appointed actuary is asked to assess the whole financial condition of the insurer, not just its reserves. The mandate increasingly includes a Financial Condition Report that evaluates the insurer’s current and projected position; Dynamic Capital Adequacy Testing, which projects solvency forward under a range of adverse scenarios to see whether the insurer would survive them; an opinion on the overall financial condition rather than the reserves alone; active engagement with the board and the regulator; and, in many jurisdictions, a statutory duty to raise the alarm directly with the supervisor if the insurer’s position deteriorates dangerously.

Taken together, these responsibilities transform the role from backward-looking certification into forward-looking guardianship. The appointed actuary is no longer simply confirming that last year’s numbers added up; they are testing whether the institution can withstand next year’s shocks — and they carry a professional, and often legal, obligation to speak up when the answer is in doubt.

Of these duties, the forward-looking ones carry the most value for a board. Dynamic Capital Adequacy Testing, in particular, is less a calculation than a rehearsal: it runs the insurer’s balance sheet forward through a series of severe but plausible scenarios — a spike in claims, a fall in asset values, an adverse shift in lapse or mortality experience — and reports how close, and how quickly, the insurer would come to breaching its capital requirements. A board that reads its testing carefully knows not merely that it is solvent today, but how much adversity it could absorb before it was not.

The appointed actuary’s remit has widened from an annual certification into a continuous, six-part guardianship of solvency.

Why supervision is tightening

This expansion is deliberate, and it reflects forces converging on the region’s insurance supervisors. Regulators across the Caribbean are progressively aligning their frameworks with international standards — the insurance core principles promoted by the global community of supervisors — and moving toward risk-based capital regimes that tie an insurer’s required capital to the risks it actually runs. Both shifts place far greater weight on actuarial judgement, and therefore on the actuary the supervisor relies upon.

The lessons of insurer failures elsewhere reinforce the trend. Such failures are almost always preceded by reserves that proved inadequate or capital that was thinner than it appeared — exactly the conditions a vigilant appointed actuary exists to detect. In small markets the stakes are higher still: the collapse of a single insurer can ripple through an entire economy and shake public confidence in the financial system. Tighter expectations of the appointed actuary are, in essence, how supervisors guard against that outcome before it occurs.

Consider how this works in practice. An appointed actuary reviewing an insurer’s projected capital under stress notices that a block of long-dated guarantees — comfortable in benign conditions — would erode the capital base sharply if interest rates moved against it. Raised early, with the board and, if necessary, the supervisor, the finding gives the insurer time to hedge, reprice or restructure while options remain open. Left undetected until it crystallised, the same exposure could have threatened the institution itself. That, in a sentence, is the difference between a guardian and a signature.

What boards should demand

A board that treats the appointed actuary as a compliance signature is wasting its most valuable risk advisor. The relationship should be one of genuine challenge. A good appointed actuary probes assumptions rather than rubber-stamping them, stress-tests solvency rather than assuming it, and tells the board what it needs to hear rather than what it would prefer. Directors should expect — and insist on — direct access to the actuary, clear explanations of the sensitivities behind the headline numbers, and an honest forward view of the risks the institution faces.

This is also a matter of board literacy. Directors need not master the mathematics, but they should be able to ask the right questions: how prudent are our reserves; how much capital stands between us and insolvency under stress; what is the single scenario most likely to threaten us; and is our appointed actuary genuinely independent of management’s preferred narrative? An appointed actuary who welcomes those questions is doing the job well. One who deflects them is a risk in their own right.

The independence question

Independence sits at the heart of the role’s value. The appointed actuary’s opinion is worth most precisely when it is free from the pressures that might soften it — the wish to report a smoother profit, to support a growth ambition, or to avoid an uncomfortable conversation with management. Where the same network both audits an insurer’s financial statements and supplies its actuarial advice, the objectivity that gives the opinion its force can be quietly compromised, even with the best intentions on all sides.

This is one reason an independent appointed actuary — free of network conflicts and reporting candidly to the board and the regulator — carries particular weight. The point is not to impugn anyone’s integrity; it is to recognise that genuine independence is structural, not merely personal, and that boards and supervisors increasingly value an actuarial opinion they know no other commercial relationship could colour.

It is worth distinguishing the appointed actuary from the external auditor, with whom the role is sometimes confused. The auditor expresses an opinion on whether the financial statements are fairly stated; the appointed actuary forms a forward-looking judgement on whether the insurer can keep the promises behind them. The two are complementary, but they are not interchangeable, and an insurer that leans on one to do the work of the other leaves a gap exactly where its solvency is ultimately decided.

Choosing an appointed actuary

Selecting an appointed actuary is therefore a more consequential decision than it once appeared. Credentials matter — fellowship-level qualification and the professional standards that come with it — but so do judgement, regional understanding and the willingness to challenge. An appointed actuary who understands Caribbean data, regulation and economic conditions will reach different and better conclusions than one applying a template from elsewhere; and one who communicates clearly with directors turns a technical obligation into genuine board-level insight.

There is value, too, in continuity. An appointed actuary who has followed an insurer’s experience over several years understands its book in a way no incoming reviewer can replicate quickly — which assumptions have held, where the surprises have come from, and how the business behaves under pressure. That accumulated judgement is itself a safeguard, and it argues for treating the appointment as a long-term professional relationship rather than a service to be re-tendered on price alone.

The best appointments combine all of these: international-standard technical rigour, real familiarity with the region, structural independence, and the communication skills to make the analysis useful to the people who must act on it. That combination is precisely what transforms the appointed actuary from a regulatory requirement into a strategic safeguard — and what a board should look for when the appointment next comes up for review.

The evolution of the appointed actuary mirrors a broader truth running through this series: actuarial work delivers its greatest value when it is forward-looking, independent and connected to the decisions that shape an institution’s future. The supervisor’s growing reliance on the role is not red tape; it is recognition that a well-chosen appointed actuary is one of the most effective early-warning systems an insurer can have. The boards that embrace that relationship — demanding challenge, valuing independence, and listening when the actuary raises a concern — protect their policyholders, their licence and their institution. Those that treat the appointment as a signature will, sooner or later, discover precisely what it was meant to prevent.

| TAKE THE NEXT STEP

Arrange an Appointed Actuary consultation If your appointment is up for review, your supervisor is raising its expectations, or you simply want an independent, conflict-free voice on solvency, our actuarial leadership will walk you through what a modern appointed-actuary relationship should deliver for your board. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210