Reserves are the largest number on most insurers’ balance sheets and the least understood by their boards. Getting them wrong is rarely loud — until, suddenly, it is catastrophic.

On the balance sheet of almost any insurer, the single largest figure is also the one the board understands least. It is the provision for claims — the reserve — and it represents the insurer’s best estimate of money it will have to pay out for events that have already happened but are not yet fully settled. Premiums are known. Investments can be counted. The reserve, by contrast, is an estimate of the future cost of the past, and getting it wrong is the quietest and most dangerous mistake an insurer can make.

It is quiet because a reserve that is too low produces no immediate alarm — quite the opposite, it makes the current year look more profitable than it truly is. And it is dangerous because the gap, once opened, tends to be discovered only when the claims arrive and the money to pay them is found to be missing. Reserve adequacy is not a technical footnote; it is, over time, the single factor that most decisively shapes whether an insurer thrives, merely survives, or quietly fails.

What a reserve really is, and why it is hard

When a policyholder suffers a loss, the insurer rarely knows immediately what it will ultimately cost. Some claims are reported quickly and settled slowly; others — injuries that worsen, liabilities that surface years later — are not even reported until long after the event. The actuary’s task is to estimate, today, the ultimate cost of all of this: the claims already reported but not yet paid, and the claims incurred but not yet reported at all, the category actuaries call IBNR. It is, in truth, a forecast dressed as an accounting entry.

The difficulty is that the forecast rests on patterns that may not hold. Actuaries study how past claims developed over time — how an initial estimate grew or shrank as cases matured — and project that experience forward. But the past is an imperfect guide. A change in how quickly claims are settled, a shift in the mix of business, a single unusually large loss, or a quiet trend in claim severity can all bend the development pattern in ways a model calibrated on history will miss. Reserving is therefore irreducibly a matter of judgement, informed by data but never determined by it alone.

It helps to distinguish two kinds of business. Short-tail lines — property damage, motor — are reported and settled relatively quickly, so the reserve is sizeable but resolves within a year or two, and the room for error is contained. Long-tail lines — liability, professional indemnity, and certain health and workers’ exposures — can take many years to develop fully, and it is here that the danger concentrates. A reserve for a long-tail book is, in effect, a bet on conditions a decade away; a small error in the assumed development pattern, compounded over years, becomes a very large error in money.

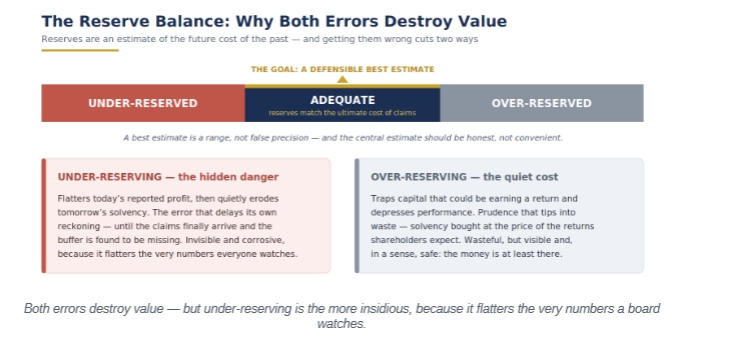

A dangerous asymmetry

The peril of reserves lies in their asymmetry, and it is worth stating plainly because so many boards miss it. Set the reserve too low and today’s profit is flattered: costs that belong to this year are pushed, invisibly, into the future, and the insurer reports earnings it has not truly made. Set it too high and the opposite happens: capital that could be deployed or returned is locked away against liabilities that will never materialise, depressing returns and starving the business of resources it could put to work.

Both errors destroy value — but under-reserving is the more insidious, because it flatters the very numbers a board watches.

Of the two errors, under-reserving is by far the more insidious. Over-reserving is wasteful but visible and, in a sense, safe: the money is at least there. Under-reserving is invisible and corrosive, because it flatters precisely the figures — profit, capital, solvency — that everyone is watching, and it does so in the very years before the shortfall becomes undeniable. By the time an under-reserved book reveals itself, through a wave of adverse development, the cheap opportunities to correct it have usually passed.

Consider a liability book that looked comfortably profitable for several years. Each year’s reserve was set a little optimistically — nothing dramatic, just a consistent lean toward the favourable end of the range — and each year’s reported profit benefited accordingly. The board saw a strong, growing line of business. Then a cohort of older claims developed worse than assumed, several years of under-provisioning surfaced at once, and the reserve had to be strengthened sharply. The profit of those earlier years had, in effect, been borrowed from a future that had now arrived. Nothing dramatic or obviously wrong had happened along the way — which is exactly what makes the pattern so dangerous.

How reserves fail quietly

Reserves rarely fail through a single dramatic miscalculation. They erode through drift. Claims-settlement patterns change as courts, regulators or the insurer’s own processes evolve, and a model still assuming the old pattern slowly falls behind reality. Inflation does its work in two forms: ordinary economic inflation lifting the cost of repairs, medical care and replacement; and the subtler phenomenon of social inflation — rising awards, expanding definitions of liability, more litigious behaviour — that pushes settlement costs above what any price index would predict.

Reinsurance assumptions add another layer of quiet risk. A reserve is usually stated net of expected reinsurance recoveries, and if those recoveries prove slower, smaller or less certain than assumed — because a treaty did not respond as expected, or a reinsurer disputed a claim — the insurer’s true exposure is larger than its books suggest. Each of these factors is individually manageable. Left unmonitored and allowed to accumulate, together they can open a reserve gap that only becomes visible once it is already serious.

The Caribbean reserving challenge

Estimating reserves is harder in this region than the standard techniques assume, and for reasons that compound one another. Data is thinner: many insurers and lines of business simply do not have the long, stable claims history that development-triangle methods were designed for, and short or volatile histories make every projection less certain. Where catastrophe exposure is high, a single hurricane year can dominate the data, distorting the very patterns the actuary is trying to read and making a “normal” year of development hard to define at all.

Smaller portfolios bring their own difficulty: with fewer claims, random variation looms larger, and a handful of large or unusual losses can swing an estimate materially. Currency considerations, the structure of regional reinsurance, and a heavier reliance on judgement all raise the degree of difficulty further. None of this makes sound reserving impossible — but it does mean that mechanical application of a textbook method, without local understanding and seasoned judgement, is especially likely to mislead in Caribbean conditions.

What good reserving looks like

Because reserving is judgement under uncertainty, good practice is less about finding a single clever number and more about disciplined process. The first principle is independence: reserves set or reviewed by someone without a stake in the reported result are more likely to be honest than those produced under pressure to hit a target. The second is to think in ranges rather than false precision. A reserve is genuinely a distribution of possible outcomes, and presenting a best estimate alongside a reasonable range tells the board far more than a single, deceptively exact figure ever could.

The third discipline is back-testing — systematically comparing past estimates against what actually transpired, so that persistent bias is detected and corrected rather than quietly repeated. The fourth is regular monitoring of actual experience against what was expected, which turns reserving from an annual event into a continuous early-warning system: when claims begin to develop worse than assumed, the signal appears long before year-end. Around all of this sits governance — clear ownership, documented assumptions, and a reserving committee that genuinely challenges the numbers rather than ratifying them.

There is particular value, too, in an external, independent reserve review conducted periodically alongside the internal process. An outside actuary brings a different set of benchmarks, no investment in last year’s numbers, and the freedom to ask uncomfortable questions. A board that commissions one is buying more than a second opinion; it is buying evidence — to itself, its auditor and its regulator — that it takes the adequacy of its single largest liability seriously, and a check against the slow, unintentional drift toward optimism that the most disciplined teams are not immune to.

A board’s responsibility

None of this requires directors to become actuaries, but it does require them to engage. A board that understands its reserves asks how prudent or optimistic the central estimate is, how wide the range of reasonable outcomes is, what would have to be wrong for the reserve to prove inadequate, and how this year’s actual experience compared with last year’s expectations. It treats a run of favourable reserve releases not simply as good news but as a question — were we over-reserved before, or are we releasing prudence we will later need? — and it treats adverse development as a signal to investigate, not merely to absorb.

The board that asks these questions holds the most important lever over the insurer’s long-term solvency. The board that does not is trusting its future to a single number it has never truly examined — and, because the number is quiet, it may continue to do so comfortably right up until the moment it cannot.

Reserves decide an insurer’s future more surely than premium growth, market share or investment returns, because they determine whether the promises already made can actually be kept. The danger is precisely that they make so little noise: an inadequate reserve flatters every figure a board looks at, until the day it does the opposite. Understanding reserves — their adequacy, their sensitivities, and the judgement behind them — is therefore not a technical nicety but a core duty of stewardship. It is the quiet risk that, managed well, protects everything else and, ignored, can undo it all.

| TAKE THE NEXT STEP

Request a Reserve Adequacy Review Our actuaries will independently assess your technical provisions, test them against your own development experience, and give your board a clear view of where reserves stand — including the sensitivities and assumptions that matter most for solvency. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210