In competitive markets, price is set at the front line — but profit is decided in the assumptions. Without actuarial discipline, insurers grow their way into losses.

There is a seductive logic in insurance that catches even experienced management teams. Write more business and the top line grows; grow the top line and the company looks healthier; a healthier-looking company is rewarded. The trouble is that premium and profit are not the same thing, and the distance between them is decided long before any claim is paid — in the assumptions used to set the price. An insurer that prices without discipline can expand its book impressively for several years and only discover, when the losses finally emerge, that it has been growing its way steadily toward a problem.

This is the central paradox of insurance pricing: the cost of the product is not known when the price is set. A manufacturer knows what its materials cost before it prints a price tag. An insurer sells a promise whose true cost will be revealed only months or years later, as claims arrive. Pricing, therefore, is not an act of measurement but of estimation — and the quality of that estimation, more than almost anything else, determines whether growth creates value or destroys it.

The growth trap

Under-pricing is rarely a deliberate choice. It happens quietly, through a series of individually reasonable decisions. A competitor sets a low rate, and matching it feels necessary to retain the business. Expense loadings are trimmed to win a tender. A few good years of claims experience are mistaken for a permanent improvement rather than ordinary good fortune. Each step seems defensible on its own; together they detach the price from the underlying risk.

What makes the trap so dangerous is the lag. Because claims emerge over time — and, in long-tail lines, over many years — an under-priced cohort can grow large and appear profitable long before its true cost becomes visible. By the time the loss ratios deteriorate, the unprofitable business is already on the books in volume, renewal expectations are set, and unwinding it is painful. The insurer has, in effect, been selling dollars for ninety cents and booking the difference as success.

The pattern is familiar to anyone who has watched an underwriting cycle turn. An insurer, hungry for growth, shaves its motor rates a few points below the market and wins business rapidly; for two or three years the new book looks like a triumph, expanding market share while the early, immature claims still look benign. Then the cohort matures, the claims catch up with the premium, and the loss ratio climbs past the point of profitability. The growth that was celebrated becomes the problem that must be unwound — usually by raising rates sharply and shedding the very customers that were so expensively acquired.

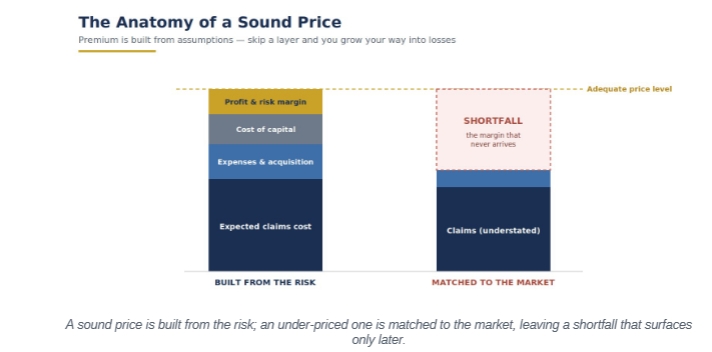

What a sound price is made of

A technically sound price is built from the bottom up, and understanding its layers is the antidote to the growth trap. The foundation is the expected cost of claims — not a guess, but an estimate grounded in the insurer’s own experience and in credible models of how losses occur. On top of that sit the expenses of acquiring and administering the business; then the cost of the capital the insurer must hold to support the risk, which is real money carrying a real return requirement; and finally a margin for profit and for the risk that actual experience will differ from the estimate. Strip out or understate any of these layers, and the price is inadequate by construction — however attractive it may look beside a competitor’s.

The discipline of building a price this way is precisely what gets lost when pricing is driven by the market rather than the risk. A price set to match a rival incorporates the rival’s assumptions, the rival’s appetite, and possibly the rival’s mistakes. A price built from the insurer’s own expected costs and capital requirements is anchored to reality — and it tells management, before a single policy is sold, whether the business is worth writing at all.

The actuarial pricing toolkit

Sound pricing rests on a handful of disciplined practices. The first is grounding assumptions in the insurer’s own experience: claim frequencies and severities, lapse and persistency rates, expense levels — drawn from the book where the data is credible, and supplemented by industry experience where it is not. The second is genuine loss modelling that reflects the full distribution of outcomes, including the tail — the rare, severe events that determine whether a portfolio survives a bad year. Averages alone are a trap; it is the variability around the average that consumes capital.

The third practice is profit testing: projecting, before launch, the return a product is expected to earn across its lifetime and under a range of scenarios, so that management can see not only whether it should be profitable but how sensitive that profitability is to each assumption. A product that makes money only if every assumption proves favourable is not a profitable product; it is a bet. Sensitivity analysis — flexing claims inflation, mortality, lapse and investment return — turns pricing from a single-point calculation into an honest map of the risks being taken, and shows management exactly where a promising-looking product is fragile.

None of this means an insurer must always charge its technical price regardless of the market. There are legitimate reasons to write business below the technical rate for a time — to enter a segment, to retain a valued client, to keep a distribution channel active. The discipline lies in knowing the technical price, measuring the gap, and accepting it consciously rather than discovering it by accident. An insurer that knows it is writing a line ten percent below adequacy can manage that position deliberately; one that has never calculated the technical price simply does not know it is losing money until the results finally tell it so.

Beyond cost-plus: pricing as opportunity

Discipline does not mean timidity, and the purpose of all this rigour is not merely to avoid loss but to enable confident, profitable growth. The same actuarial foundation that prevents under-pricing also unlocks opportunity. Value-based and segmented pricing charges appropriately for genuinely different risks — rewarding the better risks with keener rates and pricing the worse ones adequately — which improves profitability and protects against the adverse selection that punishes insurers who price everyone the same.

In the Caribbean, the opportunity is larger still. Insurance penetration across much of the region remains low by international standards, which means the prize is not only a bigger share of the existing market but the creation of new ones. Well-designed microinsurance can extend affordable cover to households and small businesses currently outside the system; parametric products can offer fast, transparent protection against the catastrophe risk that conventional cover serves poorly. Each depends entirely on sound pricing — on charging enough to be sustainable while remaining affordable enough to be taken up. Properly priced innovation is one of the most powerful levers the region has for deepening insurance penetration.

The Caribbean pricing challenge

Pricing well in the region carries the same difficulties that complicate reserving, compounded by competition. Data is thinner and shorter, making credible experience harder to establish. Catastrophe exposure must be loaded into prices in lines and territories where a single event can dwarf years of premium, and getting that loading wrong in either direction is costly. Small, competitive markets create intense pressure to match a rival’s rate rather than hold to a technical one. And investment-return and currency assumptions, which feed directly into the price of longer-term products, are harder to set with confidence. None of this argues for caution alone — it argues for pricing built on genuine local understanding rather than imported templates.

Discipline is continuous

Pricing is not a one-time calculation; it is a continuous discipline, and the rigour only holds if it is maintained after launch. The essential mechanism is the regular comparison of actual experience against what the price assumed — actual-versus-expected monitoring — which reveals, early and unambiguously, when a product is drifting away from its intended profitability. A pricing committee that genuinely owns this process, reviews the variances and feeds the findings back into the next round of rates turns pricing from a periodic event into a living feedback loop.

That loop has grown sharper with IFRS 17, which, as discussed earlier in this series, exposes profitability at the level of individual cohorts. An insurer that connects its pricing process to that granular view can see which products and segments are genuinely earning their cost of capital and adjust before small problems compound. The insurers that build this loop — price, monitor, learn, reprice — are the ones for whom growth and profit move together rather than apart.

This discipline is hardest, and most valuable, when the market softens. In a soft market, rates fall, competitors chase volume, and the pressure to follow them down is immense. It is precisely then that a clear view of the technical price earns its keep — giving an insurer the confidence to walk away from business that cannot be written profitably, and the patience to wait for the cycle to turn. The insurers that emerge from a soft market intact are almost always those that held their pricing discipline while others quietly abandoned theirs.

Pricing is where actuarial discipline meets the bottom line most directly. Every other strength an insurer builds — sound reserving, efficient capital, careful reinsurance — can be quietly undone by a book of business that was never priced to make money in the first place. The insurers that thrive are not those that grow fastest but those that grow profitably, and the difference between the two lives almost entirely in the assumptions behind the price. Get those right, hold the discipline to defend them, and growth becomes what it should be: not a gamble on volume, but the compounding of well-priced risk.

| TAKE THE NEXT STEP

Book a Pricing & Profitability Clinic Bring us a product line that is underperforming or a launch you are planning. We will pressure-test the assumptions, model the expected return and its sensitivities, and show you where the price is leaving profit — or risk — on the table. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210