The most significant change to insurance accounting in a generation is also the region’s largest untapped source of management insight — if insurers stop treating it as a reporting chore.

IFRS 17 is the most significant change to insurance accounting in a generation, and for most Caribbean insurers it arrived as the largest financial-reporting project they had ever undertaken. Years of preparation, new systems, new data, new actuarial models — all to comply with a single standard. Now that it is live and the first reporting cycles are behind them, a more important question is coming into view: was all that effort spent building a compliance machine, or a management tool? For the insurers who recognise that it can be both, IFRS 17 is about to start repaying the investment it demanded.

The distinction matters because IFRS 17 did something earlier standards never did. It moved actuarial measurement out of the regulatory return and into the heart of reported earnings. The numbers an actuary produces now shape the profit an insurer announces, the equity on its balance sheet, and the story it tells investors, rating agencies and members. That makes IFRS 17 not merely an accounting obligation but a lens on the business — and the insurers who learn to look through it will see things their competitors do not.

What IFRS 17 actually changed

Under the standard it replaced, insurers across the region measured their contracts in a patchwork of ways, often locking in assumptions set when a policy was first written. IFRS 17 sweeps that away in favour of a single, current-value model. Liabilities are re-measured each period using up-to-date assumptions about future cash flows, discounted for the time value of money. On top of that sits an explicit risk adjustment — the cost, expressed in money, of the uncertainty the insurer carries — and a contractual service margin, or CSM, which represents the unearned profit in a group of contracts and is released into earnings as cover is provided over time.

Two features deserve a board’s attention. The first is that contracts are grouped into annual cohorts and sorted by profitability, so that profitable and loss-making business can no longer hide inside the same aggregate. If a group of contracts is onerous — expected to lose money — the loss must be recognised immediately rather than quietly deferred. The second is that the choices made at transition, including how the CSM was established for business already on the books, shape the pattern of reported profit for years to come. These were not mechanical decisions; they were matters of actuarial judgement with long shadows.

Depending on the nature of the business, insurers apply a general measurement model, a simplified premium-allocation approach for short-duration contracts, or a variable-fee approach for participating business — each with its own mechanics, and each demanding assumptions that must be set, governed and defended. The common thread is that judgement, once buried in a footnote, now drives the headline number.

There is a further consequence that boards in the region are only beginning to feel. By imposing a common measurement model, IFRS 17 makes insurers far more comparable to one another and to their international peers than they have ever been. Analysts, rating agencies and prospective partners can now read a Caribbean insurer’s results against a global yardstick. That comparability is an opportunity for the well-run insurer whose discipline finally shows, and an exposure for the one whose performance the old patchwork of standards used to flatter.

The compliance scramble — and the cost of stopping there

Faced with a standard of this complexity and a tight implementation window, most insurers did the rational thing: they built the machinery required to produce the disclosures and secure a clean audit. Systems were configured, models were built, data was assembled — all aimed at generating the reconciliations and statements the standard demands. That was a considerable achievement, and for many organisations it consumed the entire IFRS 17 budget and the patience of every team involved.

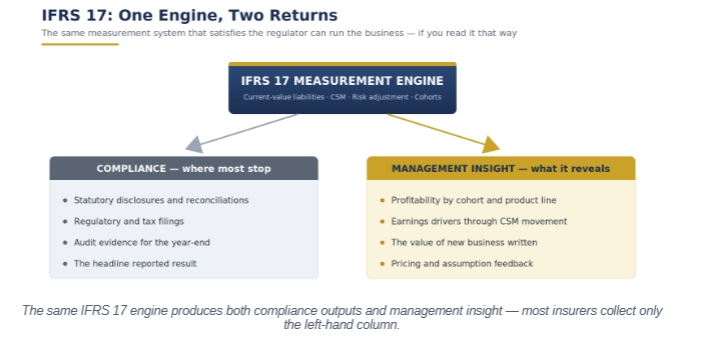

But producing the disclosures is only the visible half of what the engine can do. An insurer that switches the machinery off once the audit is signed has paid the full cost of IFRS 17 and collected only its compliance value. The same models that generated the accounts also hold a detailed, current-value picture of where the business makes money and where it quietly loses it — and in most organisations that picture is simply left unread.

The same IFRS 17 engine produces both compliance outputs and management insight — most insurers collect only the left-hand column.

The insight hiding inside the engine

Consider what the engine already knows. Because contracts are grouped and measured by cohort, IFRS 17 reveals profitability at a granularity most insurers never had before — which products, which years of business, which segments are creating value and which are destroying it. The contractual service margin is, in effect, a store of future profit; watching how it moves from period to period shows whether new business is replenishing that store or running it down. This is as close to a forward indicator of earnings as an insurer is likely to get.

The same machinery quantifies the value of new business written in the period, exposes the gap between what the insurer expected to happen and what actually did — the experience variances that flag where assumptions or pricing need attention — and isolates the financial effect of changes in discount rates and other economic factors outside management’s control. Read together, these are not accounting curiosities. They are the raw material of management: a feedback loop running from results back into pricing, product design and strategy.

There is a particularly valuable signal in the onerous-contract test. Because IFRS 17 forces an insurer to recognise an expected loss immediately, a group of contracts tipping into onerous territory becomes an early and unambiguous warning that a product is mispriced or that assumptions have drifted — surfaced now, while there is still time to act, rather than years later when the claims finally arrive. Insurers that monitor which cohorts are approaching the onerous threshold gain a forward view of pricing problems their competitors will only discover in hindsight.

None of this requires new systems. It requires asking the engine different questions, and presenting the answers to the people who run the business rather than only to those who file the accounts.

The Caribbean challenges that make this harder

Extracting that value is harder in this region than the standard’s authors assumed, for reasons that are practical rather than conceptual. Data is the first obstacle: granular, reliable history is difficult to assemble where policy-administration systems were never designed with IFRS 17 in mind, and the cohort and grouping requirements are unforgiving of gaps. Resourcing is the second: the experienced actuarial and reporting talent that IFRS 17 demands is scarce across the Caribbean, and competition for it is intense.

The third challenge is the one most easily underestimated. The transition approach an insurer adopted — full retrospective, modified retrospective or fair value — together with the assumptions embedded at that point, locks in the trajectory of reported results for years. An insurer that treated transition as a mechanical exercise may have unknowingly fixed a profit profile it would not have chosen, while one that approached it with judgement gave itself room to report its performance faithfully. These are not problems to be solved once and forgotten; they shape every subsequent reporting cycle.

From numbers to decisions

Turning IFRS 17 into a management tool begins with the questions the board asks. Is our contractual service margin growing or shrinking, and what does that tell us about the durability of our earnings? Which cohorts are onerous, and why did we write them? Where are experience variances largest, and what are they telling us about our assumptions? How much of this year’s result came from genuine performance, and how much from movements in discount rates we do not control? A board that asks these questions consistently turns IFRS 17 from a reporting burden into a quarterly diagnostic of the business.

A short illustration makes the point. Picture an insurer whose reported profit held steady for two consecutive years while, beneath the surface, its contractual service margin was quietly declining. The headline reassured the board; the CSM told the real story — that the business was consuming its stock of future profit faster than new contracts were replenishing it. An insurer reading only the headline would have continued comfortably toward a cliff. One reading the CSM saw the problem early enough to reprice and rebalance its new business. Same standard, same numbers, a very different outcome — decided entirely by which figure the board chose to watch.

The answers point directly to action. Profitability by cohort shows management where to grow and where to retrench. CSM movement warns when new business is failing to replace the profit being earned out. Experience variances feed back into the next round of pricing. The insurers that build this loop — results informing decisions informing the next results — are the ones for whom IFRS 17 becomes a source of advantage rather than a permanent cost centre.

Why an integrated firm changes the economics

Much of the friction in IFRS 17 lives in the seams between disciplines — between the actuaries who build the models, the finance teams who assemble the accounts, the technologists who maintain the systems, and the auditors who must be satisfied. When those functions sit in separate organisations, every handoff becomes a source of delay, cost and risk. When actuarial, accounting-advisory, technology and audit perspectives operate within a single firm and a single quality framework, the handoffs largely disappear, and the same effort produces both a cleaner audit and a richer set of management information. That is the practical meaning of an integrated advisor, and it is where much of the wasted cost of IFRS 17 can be recovered.

IFRS 17 will be, for every Caribbean insurer, either a permanent cost centre or a strategic asset. The standard itself is neutral; the difference lies entirely in whether the organisation reads its output as a return to be filed or as intelligence to be used. The machinery is already built and the data already flows. The only remaining question is whether anyone is looking — and that is a choice a board makes, not a limitation of the system.

| TAKE THE NEXT STEP

Schedule an IFRS 17 Readiness Diagnostic Whether you are still refining transition or already reporting, we will review your measurement models, transition choices and disclosure process — and show you how to turn the same engine into a source of profitability and earnings insight for your board. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210