The Billion-Dollar Blind Spot

Every year, organizations around the world invest billions of dollars in their Internal Audit functions. They hire talented professionals, purchase sophisticated audit management software, and dedicate significant board time to reviewing audit reports. And yet, when you ask most CEOs, CFOs, or board members whether Internal Audit is delivering maximum value to their organization, the answer is almost always the same: a polite but unmistakable “not really.”

This is not because Internal Audit lacks capable people. It is not because the profession lacks rigorous standards. And it is certainly not because organizations face fewer risks than they did a decade ago – quite the opposite. The reason Internal Audit remains chronically undervalued is far more fundamental: most Internal Audit functions are designed to look backward at what went wrong, rather than forward at what could go right.

They are built for compliance, not for competitive advantage. For detection, not for direction. For findings, not for foresight.

The result is what we at Dawgen Global call the Audit Expectation Gap – the widening chasm between what boards and executive leadership need from Internal Audit and what the function actually delivers. Closing this gap is not optional. In an era defined by regulatory acceleration, digital disruption, geopolitical volatility, and stakeholder activism, the organizations that figure out how to unlock the full strategic potential of Internal Audit will have a decisive governance advantage. Those that do not will continue treating one of their most valuable strategic assets as a cost centre to be minimized.

This article – the first in Dawgen Global’s twelve-part IAVANTAGE™ Thought Leadership Series – diagnoses the root causes of Internal Audit’s undervaluation and introduces a new framework designed to permanently close the expectation gap.

Diagnosing the Audit Expectation Gap

The Audit Expectation Gap is not a theoretical concept. It shows up in boardrooms, in audit committee discussions, and in the quiet frustrations of Chief Audit Executives (CAEs) who know their teams are capable of so much more. The gap manifests in several distinct and measurable ways.

The Relevance Gap

Board members and senior executives increasingly face strategic risks – digital transformation failures, cybersecurity breaches, ESG compliance pressures, supply chain disruptions, talent retention crises – that demand insight, foresight, and advisory support. Yet many Internal Audit functions continue to spend the majority of their time on routine financial controls testing, compliance checklist completion, and operational process walkthroughs that, while necessary, do not address the risks keeping the C-suite awake at night.

When the audit plan does not reflect the organization’s most pressing strategic priorities, the function becomes irrelevant in the eyes of those who matter most. The CAE presents findings; the board nods politely; and the cycle continues, with neither side fully engaged.

The Timing Gap

Traditional audit operates on an annual planning cycle. Risk assessments are conducted once per year, audit plans are approved, and engagements are executed over months. By the time findings reach the audit committee, the risk landscape has often shifted significantly. In a world where a single cyber incident can destroy millions in value within hours, an audit function that operates on a 12-month feedback loop is fundamentally misaligned with the speed of risk.

Organizations need real-time assurance, continuous monitoring, and the agility to pivot audit resources toward emerging threats. Most Internal Audit functions are not built for this.

The Communication Gap

Even when Internal Audit identifies significant issues, the way those findings are communicated often undermines their impact. Lengthy, jargon-heavy audit reports that bury critical insights under procedural language do not resonate with time-pressed executives and board members. When the CEO has to wade through forty pages to find the three things that actually matter, Internal Audit has failed its communication mission.

Great audit communication is concise, visually compelling, risk-prioritized, and action-oriented. It tells a story, not just a sequence of findings. It connects control weaknesses to business outcomes. And it does so in a language that executives understand and act upon.

The Value Measurement Gap

Perhaps the most damaging gap of all is the inability of most Internal Audit functions to articulate their value in terms that resonate with the business. When the CFO asks, “What is the return on our audit investment?”, too many CAEs can only point to the number of audits completed, findings issued, and recommendations implemented.

These are activity metrics, not value metrics. They measure effort, not impact. They tell the board what Internal Audit did, not what it achieved. In the absence of a compelling value narrative, it is no surprise that Internal Audit budgets are perennial targets for cost-cutting, and that the function struggles to attract and retain top talent.

The Real Cost of Undervaluing Internal Audit

The consequences of the Audit Expectation Gap extend far beyond the Internal Audit department. When organizations fail to leverage Internal Audit as a strategic asset, the costs ripple across the entire enterprise.

| “Organizations that treat Internal Audit as a compliance checkbox are not just underinvesting in assurance – they are actively accumulating strategic risk.” — Dawgen Global |

Undetected Strategic Risks. When Internal Audit is confined to routine controls testing, it lacks the mandate, resources, and relationships to identify emerging strategic risks. The board’s most sophisticated early warning system goes silent precisely when it is needed most. Major corporate failures – from governance collapses to fraud events to digital transformation disasters – frequently share a common thread: Internal Audit either was not looking in the right places or was not empowered to escalate what it found.

Governance Erosion. The three lines model depends on a strong, independent, and strategically relevant Internal Audit function. When the third line is weak, the entire governance architecture degrades. Management’s risk oversight becomes less disciplined because there is no credible internal challenge function. The audit committee receives less actionable intelligence. And the organization’s ability to demonstrate governance effectiveness to regulators, investors, and rating agencies is diminished.

Talent Drain. The most talented risk and audit professionals want to work in functions that are respected, influential, and strategically positioned. When Internal Audit is perceived as a backwater – a cost centre staffed by compliance checkers rather than business advisors – it becomes impossible to attract or retain the calibre of professionals needed to deliver real value. This creates a vicious cycle: a lower-calibre team delivers less valuable work, which reinforces the perception of Internal Audit as a low-impact function, which makes it even harder to recruit talent.

Missed Value Creation Opportunities. Internal Audit has a unique enterprise-wide perspective. No other function has the mandate to examine every part of the organization, from front-office revenue generation to back-office operations, from boardroom governance to frontline compliance. When this perspective is channelled only toward finding what is wrong, the organization misses enormous opportunities to identify what could be better – process improvements, cost efficiencies, revenue protection, and strategic insights that no other function is positioned to provide.

A New Paradigm: Introducing the IAVANTAGE™ Framework

Closing the Audit Expectation Gap requires more than incremental improvement. It demands a fundamental rethinking of how Internal Audit is designed, deployed, measured, and valued. This is precisely what the IAVANTAGE™ Framework provides.

Developed by Dawgen Global from decades of cross-industry experience advising boards, audit committees, and Internal Audit leaders across the Caribbean, Latin America, and emerging markets, IAVANTAGE™ stands for Internal Audit Value-Aligned Navigation Through Assurance, Governance & Enterprise Excellence.

It is not a set of audit standards. It is not a compliance checklist. It is a comprehensive, integrated framework that transforms Internal Audit from a retrospective assurance function into a forward-looking strategic partner that drives measurable enterprise value.

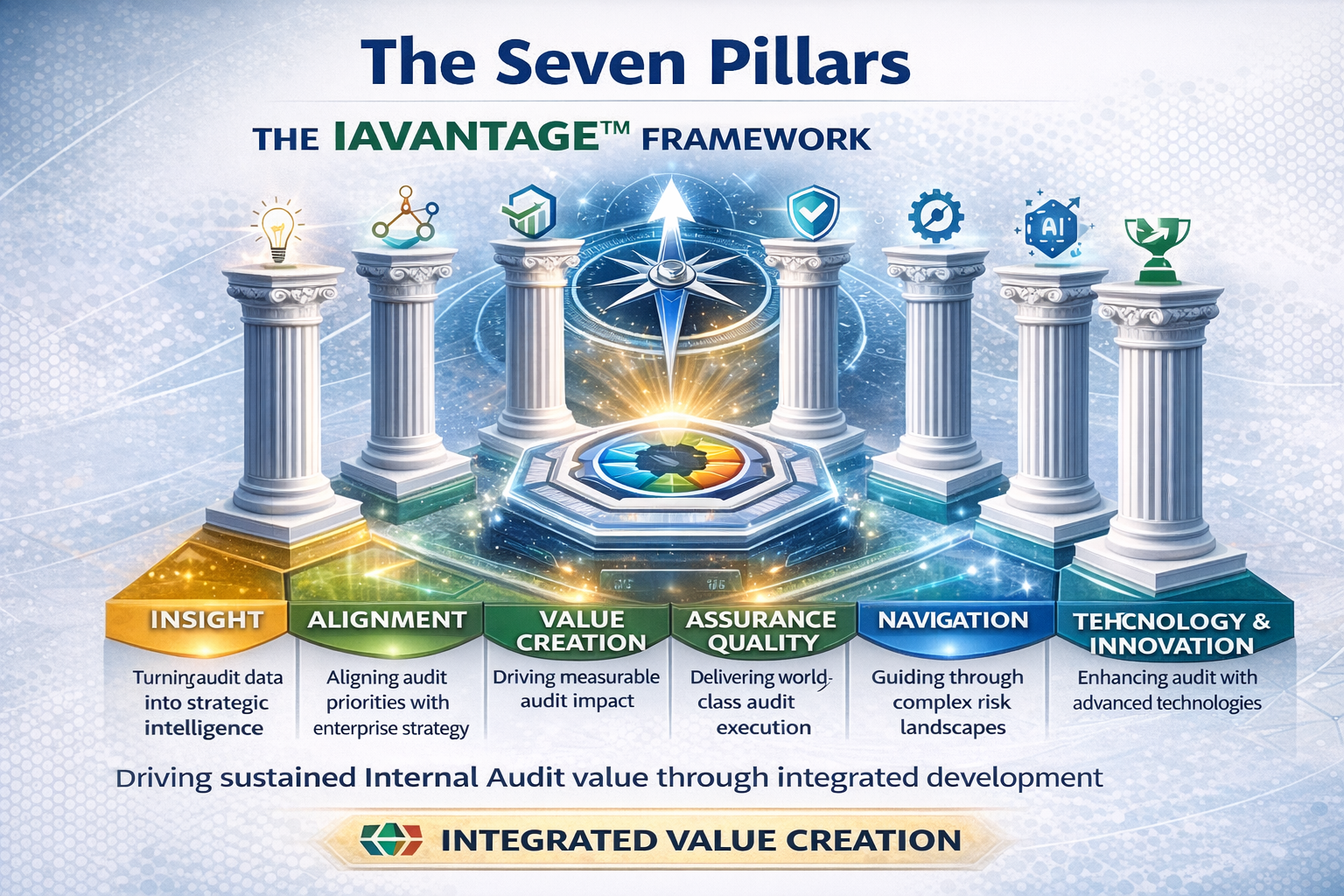

The Seven Pillars

The IAVANTAGE™ Framework is structured around seven interconnected pillars, each addressing a critical dimension of audit value creation:

- Insight – Transforming raw audit data into strategic intelligence that informs board-level decisions, identifies emerging trends, and provides predictive assurance.

- Alignment – Dynamically linking the audit universe, annual plan, and engagement priorities to enterprise strategy, risk appetite, and stakeholder expectations.

- Value Creation – Measuring and communicating audit’s tangible contribution through cost savings, process improvements, risk events prevented, and strategic opportunities surfaced.

- Assurance Quality – Maintaining world-class audit execution through robust methodology, quality assurance, professional development, and adherence to Global Internal Audit Standards.

- Navigation – Guiding organizations through complex risk landscapes including regulatory change, digital transformation, ESG requirements, and emerging threats.

- Technology & Innovation – Leveraging data analytics, continuous auditing, AI-assisted risk assessment, and automation to multiply audit effectiveness and coverage.

- Governance Partnership – Strengthening the three lines model through collaborative engagement, effective audit committee reporting, and governance advisory services.

- Enterprise Excellence – Driving organizational performance through integrated assurance, culture assessment, and embedding risk awareness across the enterprise.

The power of IAVANTAGE™ lies not in any single pillar, but in their integration. Organizations cannot achieve sustained Internal Audit value by excelling in one or two dimensions alone. The framework demands holistic development, with each pillar reinforcing and amplifying the others.

From Compliance to Strategic Partner: The Maturity Journey

A core component of the IAVANTAGE™ Framework is its five-level maturity model, which gives Internal Audit functions a clear, measurable progression path:

| LEVEL | STAGE | WHAT IT MEANS |

| 1 | Foundational | Reactive, compliance-driven. Audit exists to satisfy regulatory requirements. Limited strategic relevance. |

| 2 | Structured | Risk-based planning established. Defined methodology. Consistent delivery, but primarily backward-looking. |

| 3 | Integrated | Audit plan aligned to strategy. Advisory alongside assurance. Collaborative management relationships. Measurable impact. |

| 4 | Advanced | Predictive analytics. Real-time risk monitoring. Trusted advisor to Board and C-suite. Significant demonstrated ROI. |

| 5 | Strategic Partner | Fully embedded in enterprise decision-making. Foresight-driven. Culture and conduct assessment. Indispensable strategic function. |

Most Internal Audit functions in the Caribbean and broader emerging markets currently operate between Levels 1 and 2. The good news? With the right framework, committed leadership, and expert guidance, it is entirely possible to advance one to two maturity levels within 18 to 24 months – delivering transformative value to the organization along the way.

In subsequent articles in this series, we will explore each maturity level in depth, with practical guidance on what it takes to progress and real-world examples of organizations that have made the journey.

The Case for Action: Why Now?

If the Audit Expectation Gap has existed for years, why is closing it more urgent now than ever? Several converging forces are creating a window of both necessity and opportunity for Internal Audit transformation.

Regulatory Intensification. Across the Caribbean and internationally, regulators are raising the bar on governance expectations. From the Bank of Jamaica’s enhanced supervisory framework to evolving AML/CFT requirements to ESG disclosure mandates, organizations face a regulatory environment that demands more sophisticated assurance – not less. Internal Audit functions that cannot step up will leave organizations exposed.

Digital Acceleration. The rapid adoption of digital technologies – cloud migration, AI and machine learning, process automation, digital payments – is creating entirely new risk categories that traditional audit approaches are not equipped to address. Internal Audit must become digitally fluent, data-driven, and technologically enabled or risk becoming obsolete.

Stakeholder Expectations. Investors, rating agencies, and the public are demanding greater transparency and accountability. Audit committees are becoming more sophisticated and assertive in their expectations of the Internal Audit function. The CAE who cannot demonstrate strategic value will find their budgets cut and their influence diminished.

Talent Competition. The war for risk and audit talent is intensifying. The organizations that position Internal Audit as a dynamic, technology-enabled, strategically relevant function will win the talent battle. Those that maintain the status quo will lose their best people to consulting firms, regulators, and competitors.

The convergence of these forces means that the cost of inaction is rising every quarter. Organizations that move now to transform their Internal Audit functions will gain a sustainable governance advantage. Those that wait will find themselves playing a costly and dangerous game of catch-up.

Where to Begin: Three Immediate Actions

While the full IAVANTAGE™ Framework provides a comprehensive roadmap for transformation, there are three actions that every organization can take immediately to begin closing the Audit Expectation Gap.

First, conduct an honest self-assessment. Gather your CAE, audit committee chair, CFO, and CEO in a room and ask one simple question: “On a scale of 1 to 10, how well does our Internal Audit function address the risks and opportunities that matter most to our organization’s success?” If the scores diverge significantly – and in our experience, they almost always do – you have empirical evidence that the expectation gap exists. This honest conversation is the essential first step.

Second, review your audit plan against your strategic plan. Place your current audit plan alongside your organization’s top ten strategic priorities and risk exposures. How much of the audit plan’s capacity is directed at those priorities? If the answer is less than 50%, your audit function is spending the majority of its resources on areas that are not strategically significant. This does not mean routine compliance audits should be eliminated – but it does mean the balance needs to shift.

Third, ask your CAE to present Internal Audit’s value story. Not the activity report – not how many audits were completed or findings issued. The value story: What risks were prevented? What cost savings were identified? What process improvements were recommended and implemented? What strategic insights were provided that management would not have received otherwise? If the CAE struggles to articulate this, you have identified both the problem and the starting point for transformation.

| YOUR NEXT STEP

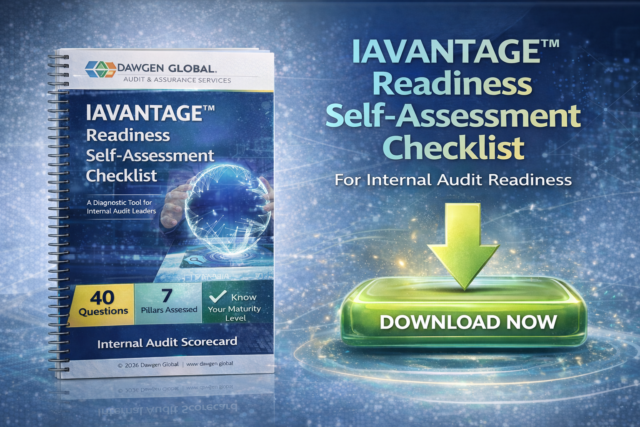

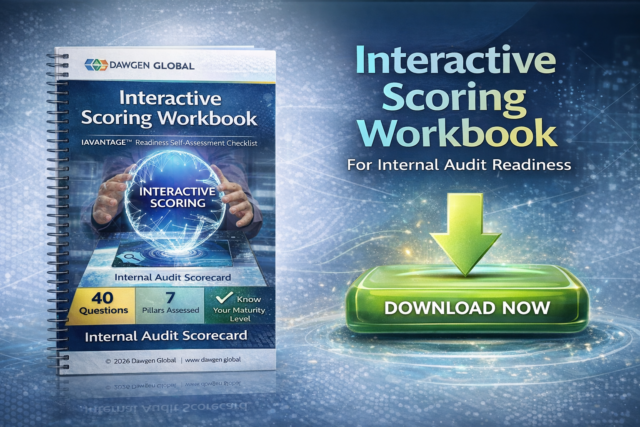

How Ready Is Your Internal Audit Function for Transformation? Dawgen Global has developed the IAVANTAGE™ Readiness Self-Assessment Checklist – a complimentary, confidential diagnostic tool that allows CAEs, audit committee chairs, and risk leaders to evaluate their Internal Audit function across all seven IAVANTAGE™ pillars in under 30 minutes. The checklist provides an immediate snapshot of your current maturity level and identifies the highest-impact areas for improvement – giving you a clear starting point for your transformation journey. ↓ DOWNLOAD YOUR FREE IAVANTAGE™ READINESS CHECKLIST ↓ Or email: [email protected] with subject line “IAVANTAGE Readiness Checklist” |

| PREFER A GUIDED CONVERSATION?

Dawgen Global is a multidisciplinary professional services firm delivering audit, assurance, risk advisory, tax, and business consulting services across the Caribbean, Latin America, and emerging markets. Our Audit & Assurance Services practice is recognized for its deep industry expertise, innovative methodologies, and commitment to helping organizations transform governance from a compliance obligation into a competitive advantage. The IAVANTAGE™ Framework is a proprietary Dawgen Global methodology. © 2026 Dawgen Global. All rights reserved. Dawgen Global Partners are available for a complimentary, no-obligation 30-minute IAVANTAGE™ Discovery Session to discuss your Internal Audit function’s challenges, opportunities, and transformation potential.

Schedule your session:

|

Coming Next in the IAVANTAGE™ Series

Article 2: “From Compliance Cop to Strategic Partner: The 5-Level Journey That Transforms Internal Audit” – A deep dive into the IAVANTAGE™ Maturity Model, with real-world examples of organizations at each level and practical guidance on what it takes to advance. Subscribe to the Dawgen Global IAVANTAGE™ Series to receive each article directly.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements