Executive Summary

Every consequential decision made by a board rests on assumptions about the future. For insurers, pension funds, credit unions, banks, governments and large corporates, those assumptions often relate to uncertain claims, future benefits, expected credit losses, catastrophe exposures, longevity, investment returns, liquidity, solvency and capital adequacy. This is the world of actuarial science.

Historically, many Caribbean organisations treated actuarial work as a technical compliance exercise: something commissioned for the regulator, the auditor or the annual report. That mindset is no longer sufficient. New accounting standards, stricter supervisory expectations, climate-related shocks, demographic pressure, catastrophe risk and volatile capital markets have moved actuarial intelligence from the back office to the boardroom.

The organisations that will lead the next decade will not be those that merely produce actuarial reports. They will be those that use actuarial insight to price products, manage capital, stress-test strategy, protect policyholders, safeguard pension promises and make better long-term decisions.

This is the actuarial advantage: the ability to convert uncertainty into decision-grade foresight.

The Boardroom Problem: Decisions Are Being Made on Uncertain Futures

Every board agenda contains questions that are actuarial in substance, even when they are not labelled that way.

- Can the insurer’s reserves withstand adverse claims development?

- Is the pension scheme truly affordable over the long term?

- Are premiums adequate after claims inflation, expenses, reinsurance costs and capital charges?

- Can a credit union defend its expected credit loss model under IFRS 9?

- What happens to solvency if a major hurricane coincides with an investment market downturn?

- How exposed is the organisation to climate risk, longevity risk, interest rate movement or medical inflation?

- Does the capital held by the business match the risks it is actually running?

These are not purely technical questions. They are governance questions. They are strategy questions. They are solvency questions. They are questions of institutional survival.

Yet in many Caribbean organisations, actuarial work is still seen as a specialist calculation performed periodically by an external professional, often late in the reporting cycle, and often primarily to satisfy a regulatory or audit requirement. The report is received, reviewed briefly, filed and referenced when needed. The numbers enter the financial statements, but the insight does not always enter the boardroom conversation.

That gap is becoming dangerous.

In today’s environment, boards can no longer afford to separate actuarial work from strategic decision-making. The region faces a convergence of pressures that demand deeper, more continuous and more locally informed actuarial analysis. Insurance accounting has changed. Credit impairment modelling has changed. Regulators are becoming more risk-focused. Climate risk is becoming measurable financial exposure. Pension and social security promises are being tested by demographic reality. Catastrophe exposure is intensifying. Capital is scarce, expensive and must be allocated with discipline.

Against that background, the question is no longer whether an organisation needs actuarial support. The question is whether that support is being used merely to comply, or whether it is being used to lead.

Why Actuarial Science Has Become a Strategic Discipline

Actuarial science is the discipline of measuring, modelling and managing financial consequences under uncertainty. At its best, it does not simply produce numbers. It converts uncertain future events into a structured basis for decision-making.

For insurers, actuarial work informs reserves, pricing, capital adequacy, reinsurance, product design, profitability, solvency and policyholder protection. For pension funds and employers, it measures long-term benefit promises and the funding required to honour them. For credit unions and lenders, actuarial-style modelling supports expected credit loss estimates and stress testing. For governments, it helps assess the sustainability of national insurance and social security schemes. For corporates, it quantifies employee benefit obligations, catastrophe exposure, climate risk and long-term financial commitments.

The value of actuarial work lies not only in calculation but in judgement. A model is only as useful as the assumptions behind it. Claims patterns change. Inflation changes. Mortality improves. Investment markets shift. Policyholder behaviour evolves. Catastrophe exposure accumulates. Medical costs rise. Regulatory expectations tighten. Data may be incomplete, inconsistent or distorted by one-off events. The actuary’s role is to interpret uncertainty, not merely process data.

That interpretive role is especially important in the Caribbean. Many global models assume deep datasets, large diversified markets and long historical experience. Caribbean markets often do not fit those assumptions. They are smaller, more concentrated, more catastrophe-exposed and more vulnerable to external shocks. Economic cycles can be sharp. Currency and liquidity considerations matter. Regulatory capacity varies across jurisdictions. Local experience may be thin, but local context is critical.

An actuarial model that is technically elegant but contextually blind can mislead the board. A reserve estimate, capital model, pricing study or stress test that does not properly reflect Caribbean realities may create false comfort. The real value comes from combining international actuarial rigour with regional knowledge.

That combination is the essence of Dawgen Global’s actuarial proposition.

The Three Forces Moving Actuarial Work into the Boardroom

Three forces are accelerating the shift from actuarial compliance to actuarial strategy.

1. Accounting Standards Have Made Actuarial Estimates Central to Reported Performance

IFRS 17 has fundamentally changed how insurance contracts are measured and reported. Insurance liabilities are no longer viewed through a narrow local accounting lens. They are remeasured using current assumptions, explicit risk adjustment and the contractual service margin. Profit recognition is now tied more transparently to the release of insurance service over time. This creates a richer, more demanding view of performance.

For boards, IFRS 17 is not merely an accounting standard. Properly used, it can reveal product profitability, cohort performance, assumption strain, new business value and earnings quality. It can show whether reported profit is being supported by sustainable underwriting or by assumption changes. It can expose products that appear attractive on premium volume but destroy value after risk, expenses and capital are considered.

Similarly, IFRS 9 has raised the bar for lenders, including credit unions and cooperatives. Expected credit loss is forward-looking, probability-weighted and sensitive to economic conditions. It requires more than a simple arrears table. It requires a defensible methodology, credible assumptions, data governance, model validation and board understanding.

IAS 19 has similar implications for corporates and public-sector entities carrying employee benefit obligations. Gratuities, defined benefit pensions, post-employment medical promises and other long-term benefits can be material liabilities. If they are poorly measured, the balance sheet is misstated and management may underestimate future cash requirements.

In each case, actuarial judgement has moved from the technical appendix to the centre of financial reporting.

2. Regulators Are Moving Toward Risk-Based Supervision

Insurance and pension regulators across the region are increasingly focused on solvency, governance, capital adequacy and forward-looking risk assessment. The appointed actuary is no longer merely a certifier of reserves. The role is evolving toward independent professional challenge, financial condition reporting, dynamic capital adequacy testing and early-warning analysis.

Boards should expect supervisors to ask better questions. Are reserves adequate? Are assumptions current? Is reinsurance effective? Does the insurer understand its catastrophe accumulation? Has the board considered adverse scenarios? Does capital match the risk profile? Are policyholders protected under stress?

These questions cannot be answered convincingly by a static annual valuation alone. They require an integrated actuarial view of the organisation’s financial condition.

Risk-based supervision also changes the board’s obligation. Directors must not only receive actuarial reports; they must understand their implications. They must know the sensitivities, the assumptions, the limitations and the management actions available if experience moves adversely.

A board that treats actuarial work as a compliance signature may satisfy the form of oversight while missing the substance.

3. The External Risk Environment Has Become More Volatile

The Caribbean is exposed to risks that are both severe and correlated.

A major hurricane can damage homes, hotels, infrastructure, utilities, agriculture, public finances and insurance balance sheets at the same time. A downturn in tourism can weaken household income, loan performance, government revenue and pension contributions simultaneously. Climate change can affect physical assets, insurance availability, food systems, coastal infrastructure and sovereign risk. Longevity improvement can increase pension and social security costs over decades. Medical inflation can turn a modest post-employment health promise into a material balance sheet liability.

These risks do not arrive neatly, one at a time. They interact. They compound. They test the resilience of institutions.

Traditional planning often assumes a base case with modest sensitivity analysis. That is no longer enough. Boards need stress testing, scenario modelling, reverse stress testing and capital impact analysis. They need to know not only what is expected, but what could happen if several adverse events occur together.

In a small-island context, foresight is not optional. It is a fiduciary necessity.

The Caribbean Actuarial Value Gap

The Caribbean has a clear need for actuarial intelligence, but it also faces a capacity challenge.

Qualified actuarial expertise is scarce. Larger insurers and financial institutions may have access to actuarial professionals, but many smaller insurers, pension funds, credit unions, public-sector bodies and corporates are under-served. Where actuarial services are imported from abroad, the result can be technically sound but insufficiently tailored to local realities.

This creates what may be called the Caribbean actuarial value gap.

The gap is not simply a shortage of actuaries. It is the distance between actuarial work that satisfies a formal requirement and actuarial work that genuinely improves decisions.

- A pension valuation may comply with accounting requirements but fail to help trustees and sponsors understand funding risk.

- An IFRS 17 model may produce disclosures but fail to inform product strategy.

- An ECL model may satisfy a spreadsheet calculation but fail under auditor scrutiny.

- A reserve review may produce a point estimate but fail to communicate uncertainty.

- A catastrophe model may quantify exposure but fail to inform liquidity planning.

- A capital review may confirm solvency but fail to identify trapped capital.

In each case, the organisation has purchased actuarial work, but it has not fully captured actuarial value.

Closing that gap requires a different model: actuarial services that are technically rigorous, locally informed, commercially practical and integrated with governance, accounting, audit, risk, technology and strategy.

This is why Dawgen Global established its Actuarial & Insurance Regulatory Advisory Services Division. The purpose is not simply to provide calculations. It is to help Caribbean organisations turn risk into foresight.

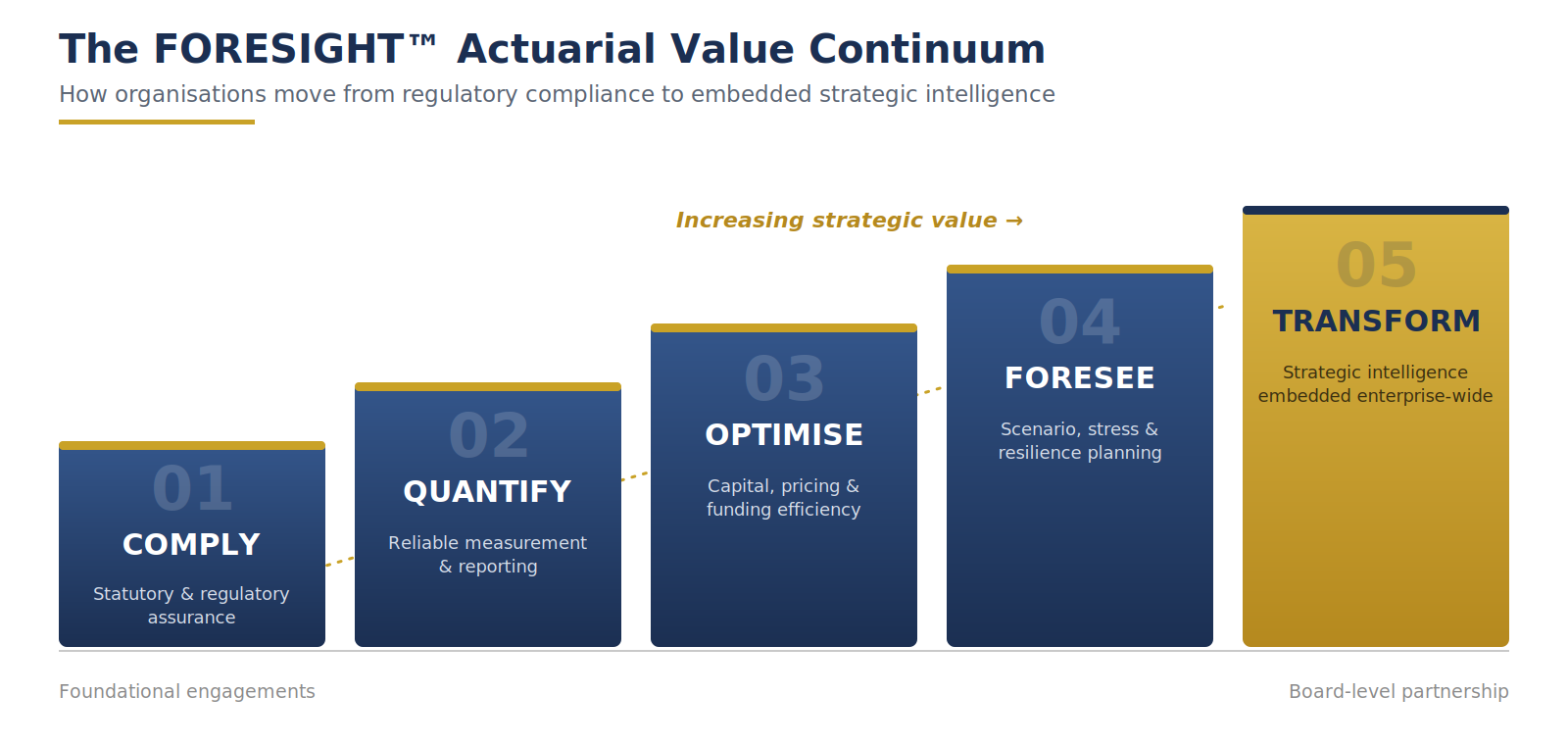

Introducing the FORESIGHT™ Actuarial Value Continuum

Dawgen Global’s FORESIGHT™ Actuarial Value Continuum provides a practical way for boards to understand where their organisation currently sits and how it can move toward higher-value use of actuarial intelligence.

The continuum has five stages: Comply, Quantify, Optimise, Foresee and Transform.

Stage 1: Comply

At the Comply stage, actuarial work is performed to meet external requirements. The organisation obtains statutory valuations, appointed actuary reports, regulatory filings, accounting estimates or audit support. This stage is essential. Without compliance, the organisation risks regulatory sanction, audit qualification, reputational damage or loss of licence.

But compliance is only the starting point. It answers the question: “Have we met the requirement?”

It does not necessarily answer the more important question: “What does this tell us about the business?”

Stage 2: Quantify

At the Quantify stage, the organisation begins to use actuarial work to measure risk reliably. Reserves are assessed with greater discipline. Expected credit losses are modelled more defensibly. Pension and employee benefit liabilities are valued with appropriate assumptions. Sensitivities are understood. The board can see not only the number, but the range around the number.

This stage creates confidence. It allows directors, auditors, regulators and management to rely on the figures being reported. It replaces guesswork with structured measurement.

Stage 3: Optimise

At the Optimise stage, actuarial work begins to improve business performance. Pricing is sharpened. Product profitability is tested. Reinsurance is structured more efficiently. Capital is allocated more intelligently. Pension risk is managed before it becomes a crisis. The organisation begins to ask: “How can we use these insights to improve returns, release trapped capital or reduce volatility?”

This is where actuarial work often pays for itself many times over. The value is no longer defensive only. It becomes commercial.

Stage 4: Foresee

At the Foresee stage, the organisation uses actuarial intelligence to look forward. Stress testing, scenario analysis, catastrophe modelling, climate risk analysis, ORSA support and long-term sustainability projections become part of board decision-making. The organisation does not wait for shocks to expose weakness. It tests itself before the shock arrives.

This stage is especially important in the Caribbean, where catastrophe, climate, demographic and economic risks are central to institutional resilience.

Stage 5: Transform

At the Transform stage, actuarial intelligence is embedded in strategy. The board and executive team use a common language of risk-adjusted return. Actuarial analysis informs acquisitions, market entry, product development, capital planning, risk appetite, investment strategy and long-term transformation.

At this stage, the actuary is not a periodic technical advisor. Actuarial insight becomes part of how the institution thinks.

This is the highest form of the actuarial advantage.

Composite Case Study: The Insurer That Was Compliant but Not Prepared

Consider a composite insurer operating across several Caribbean territories. The company had always obtained its actuarial reserve review on time. It met regulatory filing deadlines. Its financial statements were audited. Its board received the required technical reports annually.

On paper, the organisation was compliant.

However, several warning signs were not being brought together. Claims settlement times were lengthening in one major line of business. Repair costs were rising faster than general inflation. Reinsurance deductibles had increased. A new product line was growing quickly but had not yet produced enough mature claims experience to reveal its true profitability. The investment portfolio was also more exposed to interest rate movement than management appreciated.

Each issue was known somewhere in the organisation. None was being integrated into a board-level actuarial view.

When a major weather event occurred, the insurer faced higher claims, slower recoveries and pressure on liquidity. The event did not create the weaknesses; it revealed them.

A more mature actuarial framework would have helped the board see the pattern earlier. Reserve adequacy testing, pricing review, reinsurance optimisation, stress testing and capital modelling could have been connected into one forward-looking view. The board would have understood not only whether the company was compliant, but whether it was resilient.

That is the difference between actuarial reporting and actuarial foresight.

What Boards Should Now Demand from Actuarial Work

Boards do not need to become actuaries. But they do need to become better users of actuarial intelligence.

At minimum, directors should ask management and advisors the following questions:

- Are our actuarial estimates produced only for compliance, or are they used in strategic decision-making?

- What are the most material actuarial assumptions in our financial statements, and when were they last independently challenged?

- Do we receive point estimates only, or do we receive ranges, sensitivities and adverse scenarios?

- How do actuarial findings influence pricing, capital allocation, reinsurance, investment strategy and risk appetite?

- Are our models calibrated to Caribbean experience, or are they relying heavily on imported assumptions?

- What would happen to solvency, liquidity and earnings under a severe but plausible regional shock?

- Do we have the actuarial capability needed for IFRS 17, IFRS 9, IAS 19, pension sustainability, climate risk and catastrophe exposure?

- Is the appointed actuary or actuarial advisor sufficiently independent, objective and empowered to challenge management?

- Are actuarial insights reaching the full board, or are they confined to technical committees?

- What is the next stage we should move toward on the FORESIGHT™ Actuarial Value Continuum?

These questions help shift the boardroom conversation from passive receipt of actuarial outputs to active use of actuarial insight.

Dawgen Global’s Perspective

Dawgen Global believes the Caribbean requires actuarial advisory services that are both technically robust and regionally grounded.

The region does not need generic actuarial templates detached from local operating realities. It needs actuarial analysis that understands Caribbean insurers, pension funds, credit unions, regulators, public-sector schemes, catastrophe exposure, data limitations, economic concentration and capital constraints.

Dawgen Global’s Actuarial & Insurance Regulatory Advisory Services Division is designed around that need. It brings together actuarial science, insurance regulatory knowledge, financial reporting, audit, risk advisory, technology, corporate finance and strategic insight. This integrated approach matters because actuarial issues rarely stand alone. IFRS 17 affects financial reporting and business strategy. ECL affects audit, credit governance and capital. Pension liabilities affect balance sheets, cash flows and employee relations. Climate risk affects insurance, lending, investment and disclosure. Capital optimisation affects growth, solvency and shareholder value.

The value lies in connecting the dots.

For Caribbean boards, the opportunity is significant. Many organisations are still clustered around the Comply and Quantify stages of actuarial maturity. Moving just one stage higher can release meaningful value: better pricing, stronger reserves, more efficient capital, improved resilience, clearer reporting and greater confidence from regulators, investors and stakeholders.

Actuarial foresight is not reserved for large global institutions. It is available to any organisation prepared to treat uncertainty as something to be measured, governed and managed.

Foresight Is Now a Boardroom Responsibility

The next decade will test Caribbean institutions. Climate volatility, catastrophe risk, demographic change, medical inflation, financial market uncertainty, regulatory development and accounting complexity will all place pressure on organisations that carry long-term financial promises.

Boards that rely on backward-looking reports will find themselves reacting to events after value has already been lost. Boards that embed actuarial intelligence into governance and strategy will be better prepared. They will understand their exposures, challenge their assumptions, allocate capital with discipline, price risk appropriately and act before stress becomes crisis.

That is the actuarial advantage.

It is not the possession of a report. It is the institutional capability to convert uncertainty into foresight and foresight into better decisions.

For Caribbean organisations, that capability is no longer optional. It is becoming one of the defining features of responsible governance, financial resilience and sustainable competitive advantage.

Take the Next Step with Dawgen Global

Book a complimentary Actuarial Readiness Conversation.

Spend 45 minutes with Dawgen Global’s actuarial advisory team to locate your organisation on the FORESIGHT™ Actuarial Value Continuum and identify the one or two moves that could release the most value for your board, your balance sheet and your stakeholders.

At Dawgen Global, we help boards and leadership teams make smarter, more effective decisions by turning uncertainty into decision-grade insight.

🔗 Contact us: https://www.dawgen.global/contact-us/

📧 Email: [email protected]

📞 Caribbean: 876-929-3670 | 876-929-3870

📞 USA: 855-354-2447

WhatsApp Global: +1 555 795 9071

Dawgen Global — Big Firm Capabilities. Caribbean Understanding.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210