WC-PULSE Framework™ | Working Capital Thought Series

Executive Summary

Receivables are the most politically sensitive part of working capital—because improving cash usually requires changing customer behaviour, sales incentives, and credit discipline. In the WC-PULSE Framework™, receivables are managed as a risk-adjusted cash portfolio, not a single DSO number. This article sets out a practical receivables operating model that aligns credit policy, collections design, dispute prevention, and pricing power to the organisation’s Trigger Zone. In RED, the priority is immediate cash protection and loss prevention. In AMBER, it’s releasing trapped value without damaging growth. In GREEN, it’s repricing terms and tightening discipline to prevent future stress. We provide a step-by-step playbook and the metrics CFOs should track weekly to keep receivables from becoming a liquidity event.

Why Receivables Break First When Conditions Tighten

When liquidity stress rises, receivables don’t deteriorate gradually—they step down in phases:

-

Payments slow (customers stretch silently)

-

Disputes increase (often as a tactic to delay payment)

-

Partial payments rise (cash rationing)

-

Bad debts follow (when stretched customers fail)

This is why a DSO metric alone is insufficient. DSO is a lag indicator; the CFO needs leading indicators and intervention triggers.

The Core Shift: From “DSO Reduction” to “Cash + Risk Management”

A high-performing receivables model balances three objectives:

-

Cash acceleration (liquidity)

-

Loss prevention (credit risk)

-

Revenue protection (commercial continuity)

Most receivables programmes fail because they over-focus on one objective and break the others:

-

Aggressive collections can trigger customer churn.

-

Lax terms boost sales but silently increase financing and default risk.

-

Dispute chaos destroys both cash and customer experience.

The WC-PULSE approach is to manage receivables like a portfolio with risk tiers, where actions vary by customer condition and company condition.

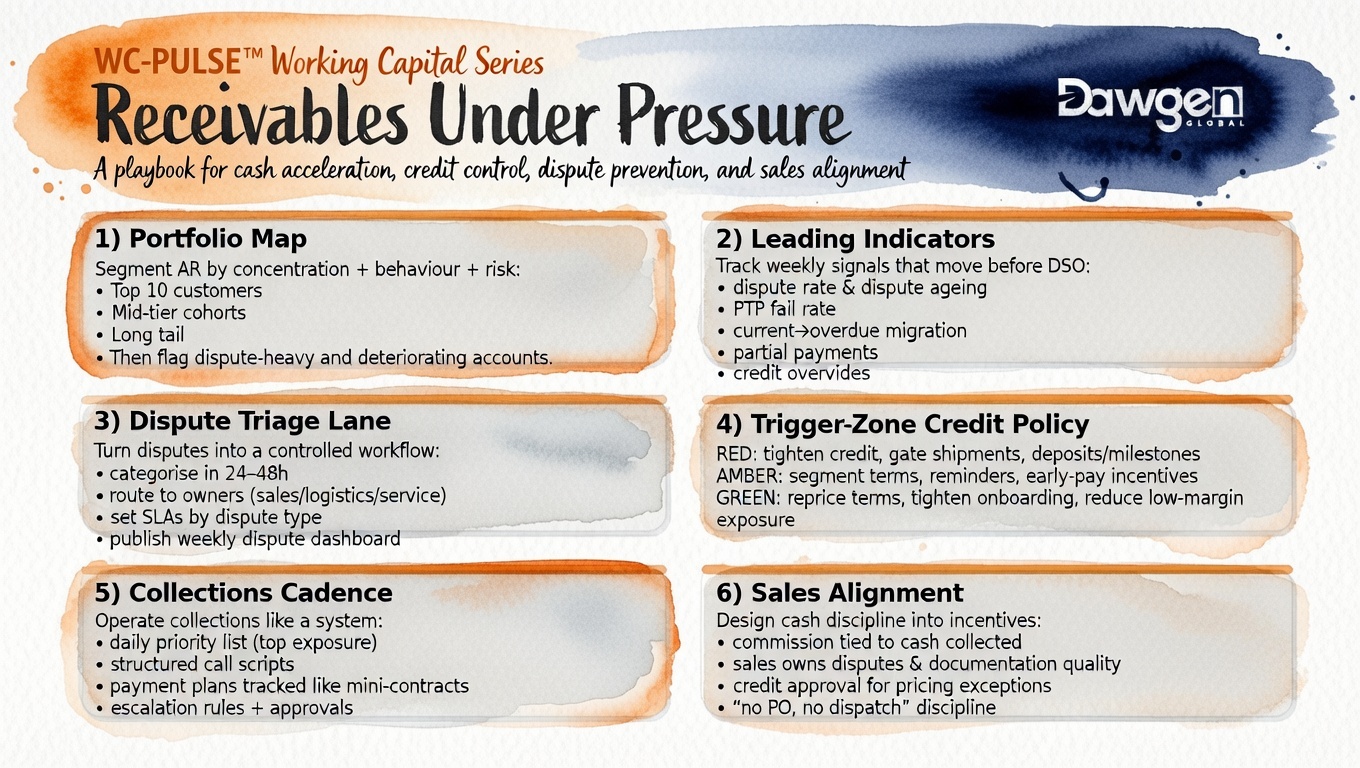

Step 1: Build the Receivables Portfolio Map

Segment the receivables book into meaningful tiers. A useful minimum structure is:

A) By concentration

-

Top 10 customers (usually 50–80% of exposure in many businesses)

-

Mid-tier (next 20–50 customers)

-

Long tail (many small balances)

B) By behaviour

-

“Pays on time”

-

“Pays late but reliably”

-

“Disputes frequently”

-

“Deteriorating / unstable”

C) By risk and leverage

-

strategic customers (high revenue dependence)

-

discretionary customers (high leverage to tighten terms)

-

risky customers (credit watchlist)

Output: a simple heat map that shows where your cash is concentrated, and where your risk is hidden.

Step 2: Install Leading Indicators (What to Watch Weekly)

These signals move before DSO moves:

-

% of invoices disputed (value and count)

-

disputes aged >14 days (unresolved disputes are cash killers)

-

partial payment frequency

-

customer promises-to-pay broken (PTP fail rate)

-

invoice accuracy rate (billing errors drive disputes)

-

“current-to-overdue migration” (how much current AR becomes overdue weekly)

-

top customer payment variance vs historical pattern

-

credit limit breaches and overrides (governance leakage)

If you track these weekly, you can intervene before the book deteriorates.

Step 3: Dispute Prevention is Cash Acceleration

In many organisations, the biggest “collections” lever is not the collections team—it is fixing the dispute root causes:

Common dispute drivers:

-

pricing mismatches / unapproved discounts

-

delivery confirmation gaps

-

missing purchase order references

-

invoice timing errors

-

service-level disputes (quality, returns, claims)

A practical approach:

-

create a “dispute triage lane” (fast categorisation and routing)

-

assign owners by dispute type (sales, logistics, service, finance)

-

set SLAs for resolution (e.g., 48 hours for documentation disputes)

-

publish dispute dashboards weekly

Rule: If disputes are not governed, receivables cannot be controlled.

Step 4: Collections as a System—Not a Reminder Process

High-performing collections functions operate on four disciplines:

1) Cadence discipline

-

Daily focus list for top exposure and ageing buckets

-

Weekly collections huddles with escalations

-

Structured call schedule (not ad hoc chasing)

2) Script discipline

-

Clear sequencing: confirm invoice → confirm acceptance → confirm payment date → confirm bank details

-

“Next action” always defined

3) Negotiation discipline

-

Use structured concessions (early payment discount, structured payment plan)

-

Avoid unmanaged “special deals” that become precedent

4) Governance discipline

-

Credit overrides require approval and documentation

-

Payment plans tracked like mini-contracts (with consequences for breach)

Collections should feel like a controlled operating process, not a firefight.

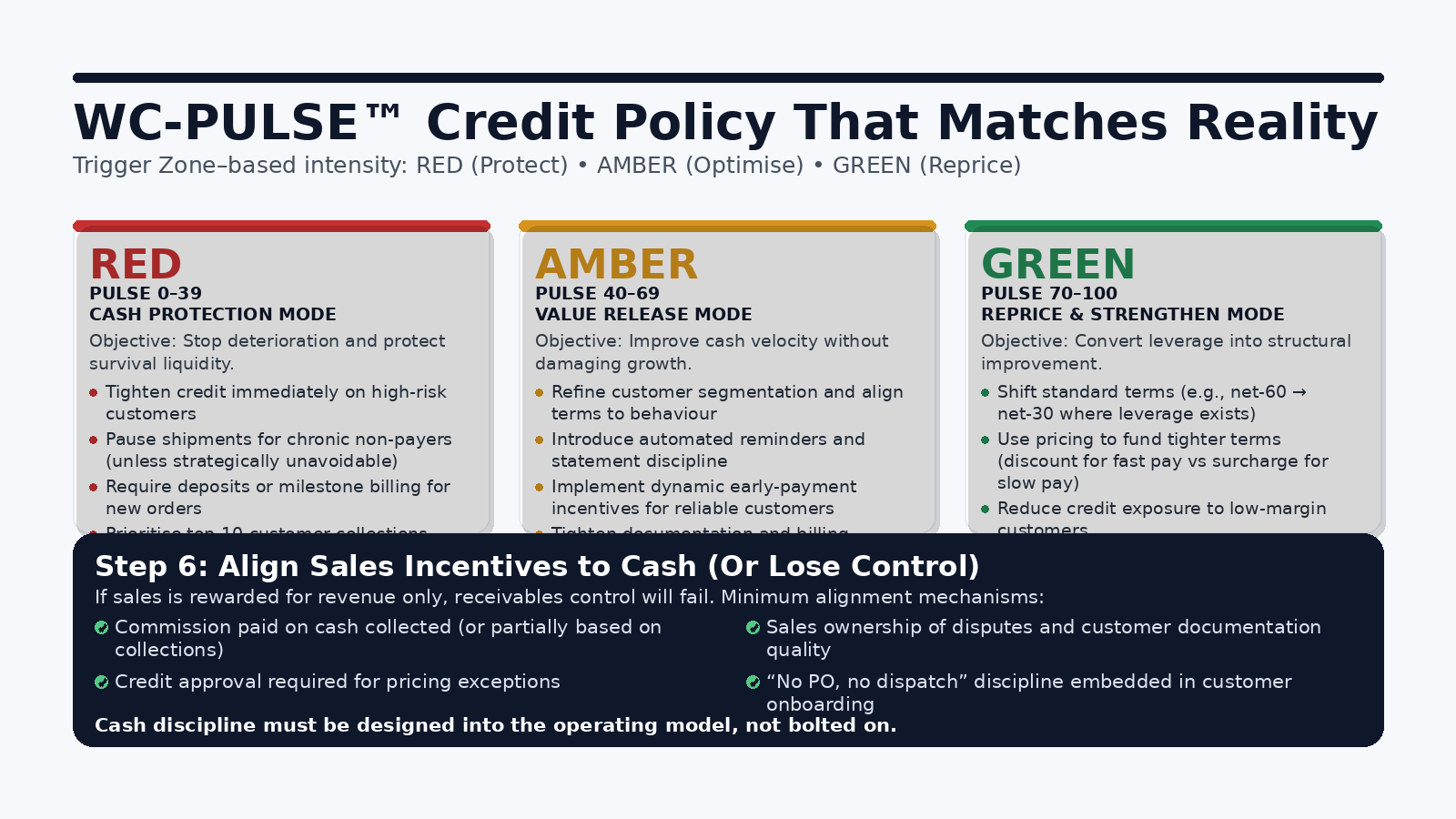

Step 5: Credit Policy That Matches Reality

Many credit policies are written for ideal conditions, not real markets. WC-PULSE requires a policy that changes intensity by Trigger Zone.

RED Zone (PULSE 0–39): Cash Protection Mode

Objective: stop deterioration and protect survival liquidity.

Actions:

-

tighten credit immediately on high-risk customers

-

pause shipments for chronic non-payers (unless strategically unavoidable)

-

require deposits or milestone billing for new orders

-

prioritise top-10 customer collections daily

-

enforce strict credit override governance

-

increase provisions visibility and escalate likely losses early

Practical test: If you can’t enforce “no ship without payment” on at-risk accounts in RED, you do not have control.

AMBER Zone (PULSE 40–69): Value Release Mode

Objective: improve cash velocity without damaging growth.

Actions:

-

refine customer segmentation and align terms to behaviour

-

introduce automated reminders and statement discipline

-

implement dynamic early-payment incentives for reliable customers

-

tighten documentation and billing accuracy for dispute-heavy accounts

-

conduct monthly credit reviews on top exposures

-

renegotiate terms on customers that consistently stretch

GREEN Zone (PULSE 70–100): Reprice and Strengthen Mode

Objective: convert leverage into structural improvement.

Actions:

-

shift standard terms (e.g., net-60 to net-30 where leverage exists)

-

use pricing to fund tighter terms (“discount for fast pay” vs “surcharge for slow pay”)

-

reduce credit exposure to low-margin customers

-

embed receivables discipline into commercial contracts

-

lock in stronger onboarding requirements (KYC, PO rules, credit insurance where relevant)

Step 6: Align Sales Incentives to Cash (Or Lose Control)

If sales is rewarded for revenue only, receivables control will fail.

Minimum alignment mechanisms:

-

commission paid on cash collected (or partially based on collections)

-

sales ownership of disputes and customer documentation quality

-

credit approval required for pricing exceptions

-

“no PO, no dispatch” discipline embedded in customer onboarding

Cash discipline must be designed into the operating model, not bolted on.

Case Study: The Customer That Turned AR Into a Crisis

A business relied on one large customer for 28% of revenue. The customer began stretching payments from 45 days to 75 days. Finance teams assumed it was temporary. Disputes increased and were left unresolved. The company stayed focused on revenue continuity and avoided escalation.

Within a quarter:

-

overdraft reliance increased

-

suppliers tightened terms

-

cash buffer fell into the RED zone

-

the customer demanded further concessions

The turnaround was achieved by:

-

executive-to-executive engagement with structured payment terms

-

dispute strike team to clear documentation issues

-

shipment gating tied to payment milestones

-

revised contract terms at renewal with clearer acceptance criteria

The lesson: concentration plus weak dispute control equals liquidity fragility.

Implementation Checklist (30–45 Days)

-

Build receivables portfolio map (concentration + behaviour + risk)

-

Install weekly leading indicators dashboard

-

Launch dispute triage lane with SLAs and owners

-

Redesign collections cadence and scripts

-

Update credit policy by Trigger Zone (RED/AMBER/GREEN)

-

Align sales incentives to cash and disputes

-

Implement top-customer governance (weekly executive review)

Next Step!

If receivables are becoming unpredictable—or if you want to reduce DSO without harming growth—Dawgen Global can help you implement the WC-PULSE receivables operating model, aligned to your Trigger Zone Matrix and cash engine.

🔗 Contact us: https://www.dawgen.global/contact-us/

📧 [email protected]

💬 WhatsApp Global: +1 555 795 9071

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements