Jamaica’s VASP regime introduces a recurring, independently audited proof of reserves for trading platforms and custodians. Here is what it is, why it matters, what makes it credible, and how to be ready.

In short: under Jamaica’s proposed VASP regime, Class A (trading platforms) and Class C (custodians) must demonstrate — at least quarterly — that the virtual assets and fiat they hold for clients fully match what they owe those clients, and must have that demonstration verified by an independent auditor acceptable to the Commission. A credible proof of reserves is not a balance snapshot: it must prove the firm controls the wallets it relies on, that those assets are unencumbered, and that the ledger of client liabilities is complete. Any shortfall must be reported immediately, and failure to conduct or submit a proof-of-reserves report breaches the licence conditions.

What is proof of reserves?

| Definition

Proof of reserves (PoR) is an exercise that demonstrates a virtual-asset business holds enough assets to cover everything it owes its customers. It reconciles two things: the assets the firm actually controls (on-chain holdings and fiat), and the liabilities it owes to clients (the sum of every customer balance). When the regime requires it, an independent auditor verifies that reconciliation and attests to its completeness and accuracy. |

In other words, proof of reserves answers a deceptively simple question that sits at the heart of customer trust: if every client asked for their assets back at once, could the firm return them in full? For exchanges and custodians that hold other people’s money and coins, that question is existential — and historically, it has too often been answered only after a collapse, when the gap between reserves and liabilities was already a hole.

Why does proof of reserves matter?

The virtual-asset sector has learned the value of proof of reserves the hard way. Several high-profile international exchange and custodian failures shared a common pattern: customers believed their assets were safely held, while in reality reserves had been lent out, pledged, traded, or simply never fully existed. Because client assets and corporate assets were commingled and the true liability ledger was opaque, the shortfall only became visible when withdrawals spiked and the firm could not meet them.

Proof of reserves is the discipline designed to surface that risk before it becomes a crisis. Done properly and independently, it gives customers, counterparties and regulators ongoing evidence that client assets are genuinely there, genuinely controlled by the firm, and genuinely sufficient. That is precisely why Jamaica’s regime makes it a recurring, regulator-supervised obligation for the two classes that hold client assets — not a one-off marketing exercise a firm runs when it suits.

Who must provide proof of reserves in Jamaica?

| The headline requirement

Class A (trading platforms) and Class C (custodians) must, at least quarterly, reconcile the client assets they hold against their recorded client liabilities as at a consistent reference date, and engage an independent auditor acceptable to the Commission to verify the exercise and attest to its completeness and accuracy. The verified report is submitted to the FSC within the period it prescribes. A shortfall must be reported immediately and remedied within the period specified, and failure to conduct or submit a report breaches the licence conditions. |

The Commission will set the form, content and submission timeline in supplementary guidance. Separately, the Business Conduct Standards require client assets to be segregated from the firm’s own assets, records capable of immediate reconciliation, and periodic independent audits of client asset holdings — so proof of reserves sits within a broader client-asset-protection framework, not on its own. Classes that do not hold client assets (such as pure advisers) are not subject to proof of reserves, though wallet providers and custodians face related cold-storage and key-management duties.

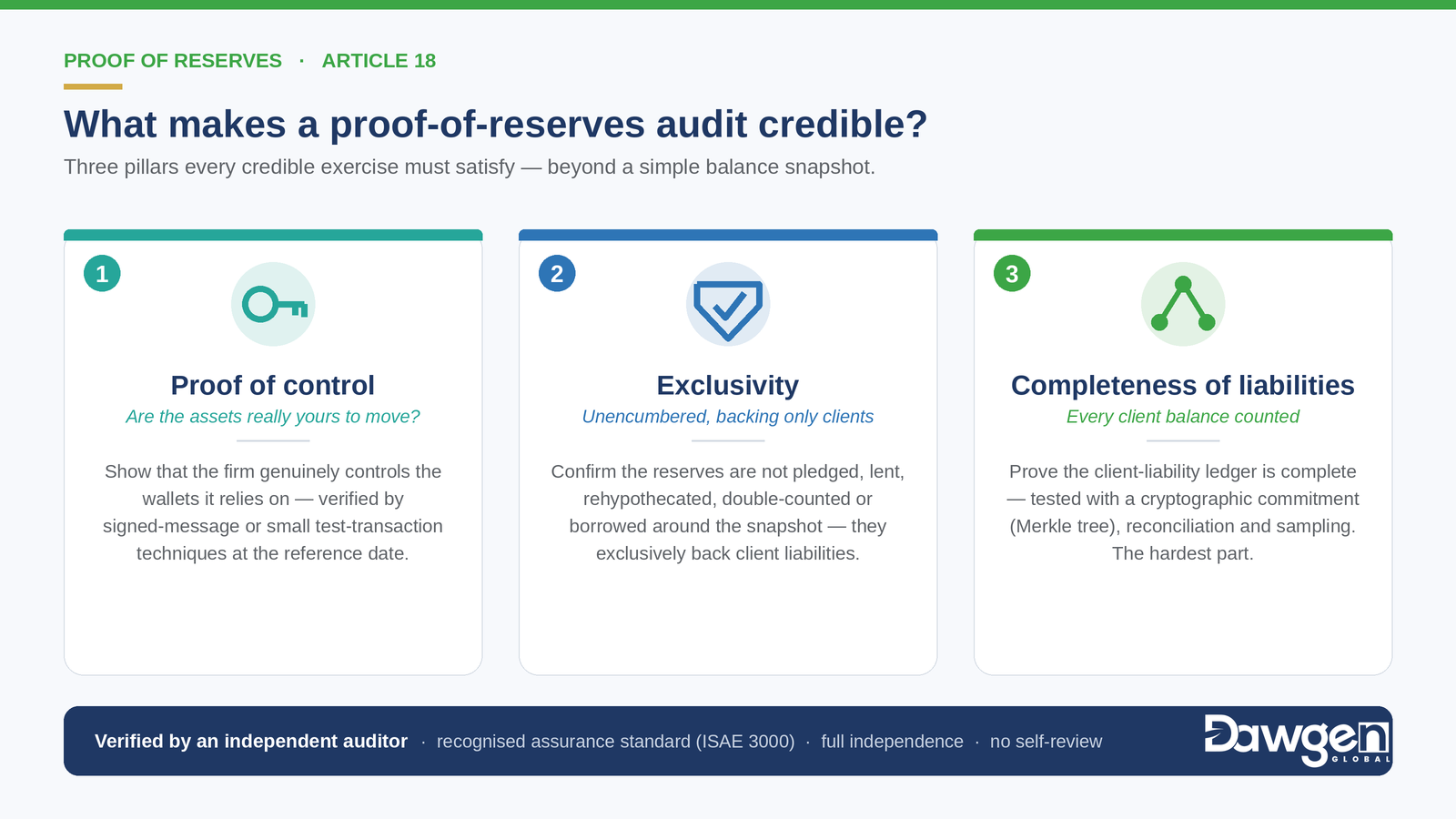

What makes a proof-of-reserves audit credible?

Not all “proof of reserves” is equal. A weak exercise can give false comfort — showing assets that look sufficient while hiding the very risks that sink firms. A credible proof of reserves rests on three pillars.

1. Proof of control — are the assets really yours to move?

Showing a wallet contains assets is not the same as showing the firm controls that wallet. The audit must establish that the firm actually holds the private keys to the addresses it relies on — typically by having it sign a specific message from each address, or move a small, defined test amount on-chain at the reference time. Without proof of control, a firm could point to addresses it does not own, or to assets borrowed for the moment of the snapshot.

2. Exclusivity — are the assets unencumbered?

Assets that are pledged as collateral, lent out, rehypothecated, double-counted across wallets, or borrowed just before the reference date are not truly available to meet client claims. A credible exercise tests that reserves are unencumbered and exclusively backing client liabilities — closing the gap that lets a firm “window-dress” a single point in time. This is also why the reference date and timing discipline matter: a snapshot is only as honest as the controls preventing temporary inflows around it.

3. Completeness of liabilities — the hard part

The most common failure point is not the asset side but the liability side. If a firm understates what it owes — by omitting customer accounts, internal IOUs, or off-ledger obligations — then reserves can appear to match liabilities that are themselves incomplete. A credible audit therefore tests the completeness of the client-liability ledger, often using cryptographic techniques (such as a Merkle-tree commitment that lets individual customers verify their balance is included) alongside conventional reconciliation and sampling. Proving assets exist is comparatively easy; proving you have captured every liability is the real work.

What standard of assurance should apply?

“Verify and attest” can describe very different engagements. At one end, an agreed-upon-procedures engagement (internationally, ISRS 4400) performs a defined set of checks and reports the factual findings without an opinion. At the other, an assurance engagement (ISAE 3000) provides limited or reasonable assurance — an actual conclusion — over defined subject matter against suitable criteria. The difference matters enormously for how much comfort a report really provides, and for comparability across firms.

The Jamaican regime leaves the precise standard to be prescribed in supplementary guidance. In our view, anchoring proof of reserves to a recognised assurance framework — ideally ISAE 3000 (Revised), with clearly published criteria — would give customers and the regulator a dependable, comparable basis. Equally important is independence: the auditor must be independent in fact and appearance (consistent with the IESBA Code of Ethics), and must not be auditing systems it designed, built or operates. A firm cannot credibly mark its own homework.

How a proof-of-reserves engagement works

In practice, a robust engagement runs through a defined sequence. The table summarises the core stages.

| Stage | What happens |

| 1. Scope & criteria | Agree the subject matter, reference date, in-scope assets and the criteria against which completeness and accuracy are judged |

| 2. Wallet identification | Obtain the full inventory of addresses and accounts holding client assets, on-chain and at third parties |

| 3. Control verification | Confirm the firm controls each address via signed-message or test-transaction techniques at the reference time |

| 4. Asset valuation | Capture on-chain balances and fiat at the reference date and value them on a consistent basis |

| 5. Liability extraction | Extract the complete client-liability ledger and test its completeness (e.g. Merkle commitment, reconciliation, sampling) |

| 6. Reconciliation | Compare total controlled, unencumbered assets to total client liabilities and quantify any surplus or shortfall |

| 7. Exceptions | Investigate and resolve differences; a shortfall is reported to the FSC immediately |

| 8. Report | Issue the verified proof-of-reserves report for submission to the Commission |

Proof of reserves is not a financial-statement audit

It is worth being clear about what proof of reserves is and is not. A financial-statement audit gives an opinion on a full set of financials over a period. Proof of reserves is narrower and more frequent: a point-in-time attestation that client assets match client liabilities, repeated each quarter. The two are complementary — a VASP will still have its annual financial statements — but they answer different questions, and a firm should not assume one substitutes for the other.

What VASPs should put in place now

Proof of reserves rewards firms that build for it from the start and penalises those that improvise. Practical readiness steps include:

- A complete wallet and key inventory, with key-management controls (cold storage, multi-signature, secure generation and recovery) that make control verifiable.

- A single, accurate client-liability ledger that can be reconciled immediately and is demonstrably complete — the hardest and most important asset to get right.

- Strict segregation of client assets from corporate assets, with no commingling and clear records of what is held for whom.

- Reference-date discipline and controls that prevent window-dressing around the snapshot, so each quarter is honest and comparable.

- Early engagement of an independent, acceptable auditor, and a documented methodology, so the first regulatory deadline is met with confidence rather than scramble.

What to do next

If you intend to operate as a trading platform or custodian, treat proof of reserves as a design requirement, not an afterthought — build the wallet controls and liability ledger now, and line up independent assurance early. For the deeper methodology, see the companion article “What Makes a Proof-of-Reserves Audit Credible? Control, Completeness and Independence,” and for selecting an auditor, see “Choosing an FSC-Acceptable VASP Auditor.”

Frequently asked questions

What is proof of reserves?

An exercise that demonstrates a virtual-asset firm holds enough assets to cover everything it owes its clients, by reconciling the assets it controls against the sum of all client balances. Under Jamaica’s regime, an independent auditor verifies that reconciliation.

Who has to provide proof of reserves in Jamaica?

Class A (trading platforms) and Class C (custodians). Both must conduct the exercise at least quarterly and have it verified by an independent auditor acceptable to the Commission.

How often is proof of reserves required?

At least quarterly, reconciled as at a consistent reference date, with the verified report submitted to the FSC within the period it prescribes.

What makes a proof-of-reserves report trustworthy?

Three things: proof that the firm controls the wallets relied on; confirmation that the assets are unencumbered; and evidence that the client-liability ledger is complete. Independence of the auditor and a recognised assurance standard are essential.

Is proof of reserves the same as a financial-statement audit?

No. Proof of reserves is a narrower, more frequent, point-in-time attestation that client assets match client liabilities. A financial-statement audit gives an opinion on a full set of financials over a period. They are complementary, not interchangeable.

| How Dawgen Global can help

Proof of reserves is where assurance meets the blockchain — and it demands a firm that understands both. Dawgen Global provides independent proof-of-reserves and client-asset assurance for trading platforms and custodians, applying recognised assurance standards, rigorous control, exclusivity and liability-completeness testing, and strict independence. We are positioning to act as an independent auditor acceptable to the Commission for these engagements. As a matter of independence, where we advise a client on building its custody, reserve or AML systems, a separate, unconflicted team — or a different firm — provides that client’s proof-of-reserves assurance; we do not audit systems we build. We act as adviser and independent auditor to the virtual-asset ecosystem and are not a licence applicant. To discuss proof-of-reserves readiness or independent assurance, contact us at [email protected] or visit dawgen.global. |

This article is part of The Caribbean Virtual Asset Regulation Imperative™ series by Dawgen Global, powered by DAGAF™ — the Dawgen Digital Asset Governance & Assurance Framework. It is general information based on the FSC’s consultation documents of 10 June 2026 and is not legal, regulatory, investment or assurance advice. The proposals remain subject to change following consultation.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210