The bank loan is one tool in the financing toolbox. Across the Caribbean, it is treated as the whole toolbox — and growth is being rationed to fit it.

The Problem, Lived

“Natalie” built her Kingston agro-processing company — sauces and seasonings — from a home kitchen to a small factory over nine years. Then came the letter every founder dreams about: a regional supermarket group wants her products across four territories. The order would roughly double the business. It requires new equipment, larger inventory, more staff, and months of working capital before the first payment lands.

Her bank — the one that has held her accounts for nine years and watched every deposit — offers less than half of what the expansion needs, at a rate that makes her wince, secured by a personal guarantee and real estate collateral she does not have. The order book, the signed letter of intent, the nine years of growth: none of it counts. “Bring land title,” is the polite summary.

So Natalie is now seriously considering the most expensive financial decision available to her: declining the growth. And here is the part that should trouble every business owner reading this — at no point has anyone shown her the other two-thirds of the financing menu. Not because it does not exist, but because in our financial culture, the bank loan is not one option among many. It is the only option most owners have ever been taught to see.

Why It Happens Here

The Caribbean’s financing reflex is bank-shaped for understandable reasons. Banks are visible, familiar and everywhere; generations of business owners were raised on the sequence save–borrow–repay. But the region’s commercial banking model leans heavily toward collateral-based lending — money advanced against real estate, not against order books or cash flows — which structurally excludes exactly the businesses growing fastest: asset-light companies whose value lives in contracts, brands and customers rather than land titles.

On the other side of the ledger sits an equally powerful cultural force: equity aversion. “I’m not giving away my business” ends the conversation before the arithmetic begins — before anyone asks whether owning seventy percent of a company five times larger might beat owning all of one that cannot grow. Add genuine unfamiliarity with the rest of the menu — development finance institutions, credit unions’ commercial windows, leasing, receivables and trade finance, private credit, corporate bonds and private placements, junior stock market listings — and a final, self-inflicted barrier: most small businesses lack the audited financials, governance and documentation that these alternatives require. The options exist; the business simply is not dressed for them. The result is growth rationed to whatever retained earnings plus one bank will permit — which is to say, rationed.

| The Most Expensive Capital of All

Owners compare interest rates to the decimal point, yet rarely price the alternative that costs the most: the growth declined. The contract not taken, the market not entered, the capacity not built — compounding, year after year, invisibly. Before concluding that financing is “too expensive,” calculate what saying no is costing. It is almost always the dearest money you will never see leave your account. |

Why Generic Advice Fails

Search “how to fund business growth” and you will land in Silicon Valley: venture capital rounds, SAFEs, pitch decks for software startups burning money by design. None of it maps to a profitable sauce manufacturer in Kingston, a distributor in Bridgetown or a logistics firm in Port of Spain. Meanwhile the instruments that actually exist in the region — DFI facilities, junior exchange listings with their incentives, private placements to regional investors, structured trade finance — barely appear in the global content, because global content is not written for our capital markets. The Caribbean financing menu is real, but it must be read by someone who knows the restaurant.

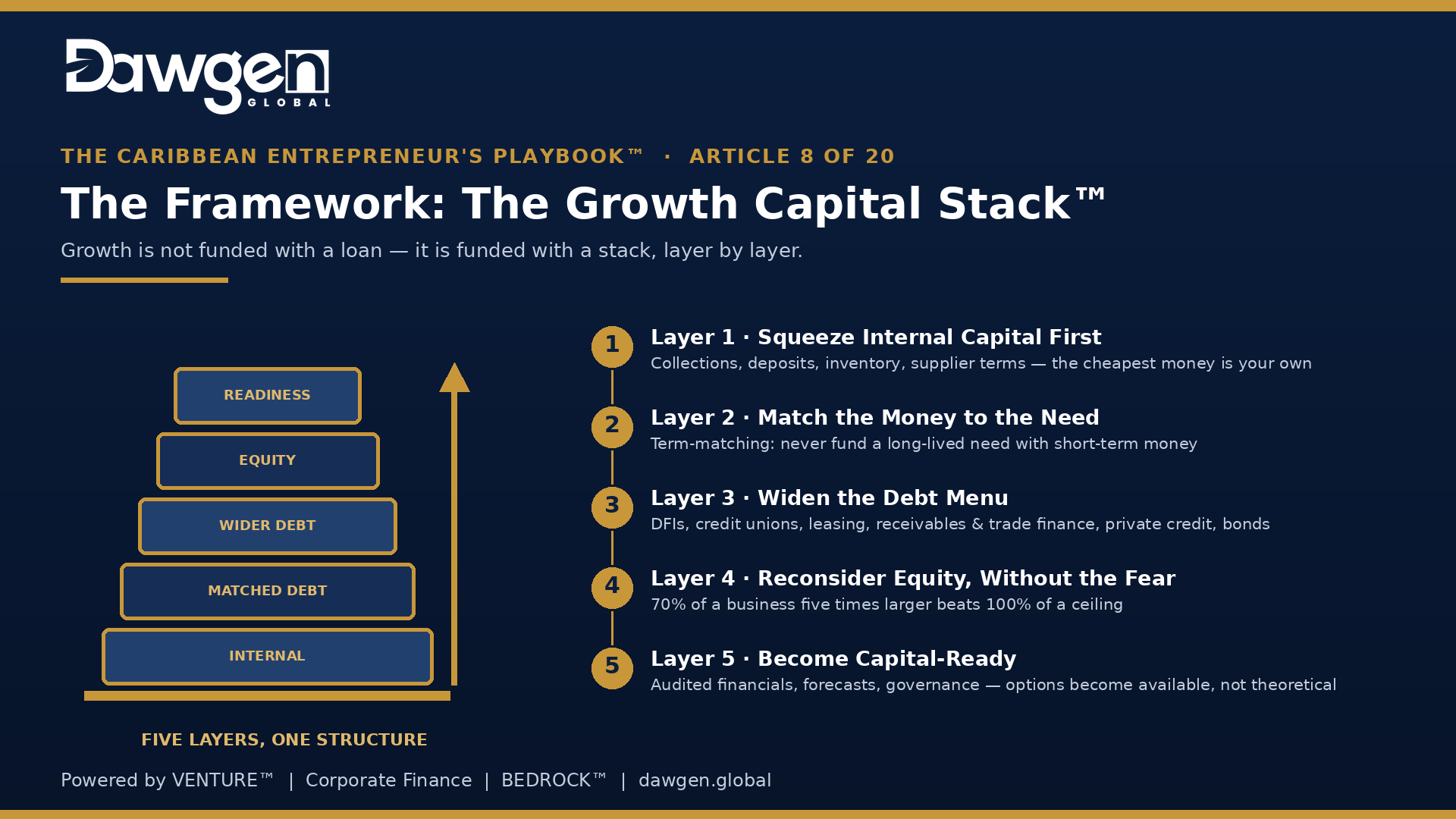

The Framework: The Growth Capital Stack™, Step by Step

Sophisticated companies do not fund growth with a loan; they fund it with a stack — layers of capital, each matched to its purpose. Build yours in five layers, in order:

- Layer 1 · Squeeze Internal Capital First — The cheapest financing on earth is the money already trapped in your own business. Before approaching any lender or investor, run the disciplines of Articles 5 and 6 of this series: accelerate collections, negotiate customer deposits and milestone payments, right-size inventory, extend supplier terms. Every dollar released internally is a dollar you neither pay interest on nor sell ownership for — and every financier you later approach will check whether you have done this before taking you seriously.

- Layer 2 · Match the Money to the Need — Name what the capital is actually for, because different needs take different money: short-term working capital (inventory, receivables) suits revolving and trade facilities; equipment suits leasing or asset finance, where the asset itself is the collateral; long-term expansion suits long-term capital — term debt, bonds or equity. The iron rule is term-matching: never fund a long-lived need with short-term money. Financing a factory line on an overdraft is how healthy businesses strangle themselves — the asset earns over ten years while the money is due in ninety days.

- Layer 3 · Widen the Debt Menu — Commercial banks are one aisle of the debt supermarket. Walk the others: development finance institutions with mandates (and pricing) built for productive-sector growth; credit unions’ business lending windows; leasing companies for equipment; receivables and trade finance that lend against your invoices and orders — the very things the bank ignored; and for established firms with real scale, private credit and corporate bonds, where investors lend against your cash flows on terms a balance sheet like Natalie’s can actually carry. Our From Bank Debt to Bedrock™ series covers the bond route in depth; the point here is simpler — most owners have been shopping one aisle their whole lives.

- Layer 4 · Reconsider Equity, Without the Fear — Run the arithmetic the folklore skips. Selling a minority stake is not “giving away your business”; it is exchanging a slice of ownership for fuel — permanent capital with no repayments, no collateral and, with the right partner, expertise and market access money cannot buy. The control question is legitimate and manageable: shareholder agreements, share classes and reserved matters exist precisely to let founders take capital while keeping the wheel. The real question is never “do I want to own less?” It is “less of what?” Seventy percent of a business five times larger is a great deal more than one hundred percent of a ceiling.

- Layer 5 · Become Capital-Ready — Every layer above depends on this one. Alternatives to the bank do not require less documentation — they require better: audited or professionally prepared financial statements, credible forecasts, clean corporate records, defined governance, a data room that answers questions before they are asked. Capital readiness is what converts the financing menu from theoretical to available; it is the difference between a business that has options and a business that has anecdotes about options. It is also, not coincidentally, everything this series has been building since Article 1.

The Framework in Action: A Worked Scenario

The following scenario is a fictional composite created for this series to illustrate the framework. It does not depict any actual business or client of the firm.

Natalie’s stack comes together layer by layer. Internally, the supermarket group — which wants her product on its shelves — agrees to a deposit against the opening order and shortened payment terms for the first year: her customer becomes her first financier. The filling and labeling line goes on an equipment lease, the machine itself standing as collateral, no land title required. A receivables facility is arranged against the group’s invoices — lending against exactly the asset her bank had waved away.

The remaining expansion capital comes from a private placement: a regional investor takes a minority stake under a shareholder agreement that leaves Natalie firmly in control, and brings with it distribution relationships in two of the four new territories. In this illustration, the expansion proceeds without a single dollar secured on her home. Eighteen months later — audited statements in hand, governance installed, a track record across four markets — her original bank calls, keen to lend to the company it declined. She takes the meeting. This time, she is reading from the whole menu.

Self-Diagnostic: How Wide Is Your Financing Menu?

One point for every “no”:

- Could you name three realistic financing sources for your business other than a commercial bank?

- Is every piece of your current financing term-matched to what it funds?

- Have you quantified what declined or delayed growth has cost you in the last three years?

- Could you produce audited or professionally prepared financials and a credible forecast within thirty days?

- Have you ever priced what a minority equity partner would actually cost — and bring?

Two or more points means your growth is being sized to your bank’s appetite rather than your market’s — and those are rarely the same number.

When to Call In Help

Capital structuring is one of the places where professional guidance pays for itself most visibly: when a bank has declined you or offered a fraction of the need; when an order or opportunity is larger than your balance sheet; when you are contemplating equity without an independent valuation or a shareholder agreement; when existing debt is mismatched to what it funds; or when you know alternatives exist but not how to become eligible for them. Each instrument on the wider menu has its own gatekeepers, documents and negotiating norms — and arriving well-advised changes both the terms you are offered and the seriousness with which you are received.

| REQUEST A CAPITAL STRUCTURE CONSULTATION

Dawgen Global’s Corporate Finance team builds Growth Capital Stacks™ for Caribbean businesses: we assess your true capital need, match instruments to purposes, prepare you for the wider menu — from DFI facilities and receivables finance to private placements and the bond market under our BEDROCK™ framework — and stand beside you in the negotiations. Our Audit and Virtual CFO teams make you capital-ready; our Corporate Finance team makes you capital-connected. Contact us today to request your consultation. 📩 [email protected] | 📞 876-929-3670 / 876-665-5926 | 🇺🇸 855-354-2447 | 🌐 dawgen.global GET THE FULL PLAYBOOK This is Article 8 of The Caribbean Entrepreneur’s Playbook™ — 20 problems, 20 how-to frameworks, one system. Pre-register at dawgen.global to receive the complete Playbook e-book on release, free. |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210