For the credit unions at the heart of Caribbean finance, IFRS 9’s expected-credit-loss model can feel like institutionalised guessing. Done with discipline, it is the opposite — and a powerful early-warning system.

Across the Caribbean, credit unions and cooperatives are not a financial-sector afterthought — they are a cornerstone. They hold the savings of hundreds of thousands of members, finance homes, vehicles, education and small enterprise, and reach communities that commercial banks often do not. So when the global accounting standard for financial instruments changed how every lender must account for the losses hidden in its loan book, it landed squarely on institutions that were, in many cases, least equipped for the complexity. For many cooperatives, the result was a sense that expected credit loss had introduced an uncomfortable amount of guesswork into their accounts.

That perception is understandable, but it is also the heart of the misunderstanding. The expected-credit-loss model is not an invitation to guess; it is a discipline for replacing guesswork with structured, forward-looking, defensible estimation. Done poorly, it produces numbers no one can explain and an auditor cannot accept. Done well, it produces a provision the board can stand behind — and, as a valuable by-product, one of the earliest warning systems a lender can have of trouble building in its portfolio.

From incurred loss to expected loss

To understand expected credit loss, it helps to understand what it replaced. Under the previous standard, a lender provided for a loss only once there was objective evidence that it had been incurred — a missed payment, a clear sign of distress. The logic looked conservative but was dangerous in practice: provisions arrived late, after the deterioration was already visible, and often in the depths of a downturn when capital was most scarce. The global financial crisis exposed the flaw starkly — provisions that were, in the regulators’ phrase, too little and too late.

Expected credit loss inverts that logic. Rather than waiting for a loss to be incurred, a lender must now estimate, from the moment a loan is made, the losses it can expect over a defined horizon — and adjust that estimate continuously as conditions change. It is a forward-looking model imposed on a discipline that had always been backward-looking, and that single shift is the source of both its power and its difficulty.

The three-stage model

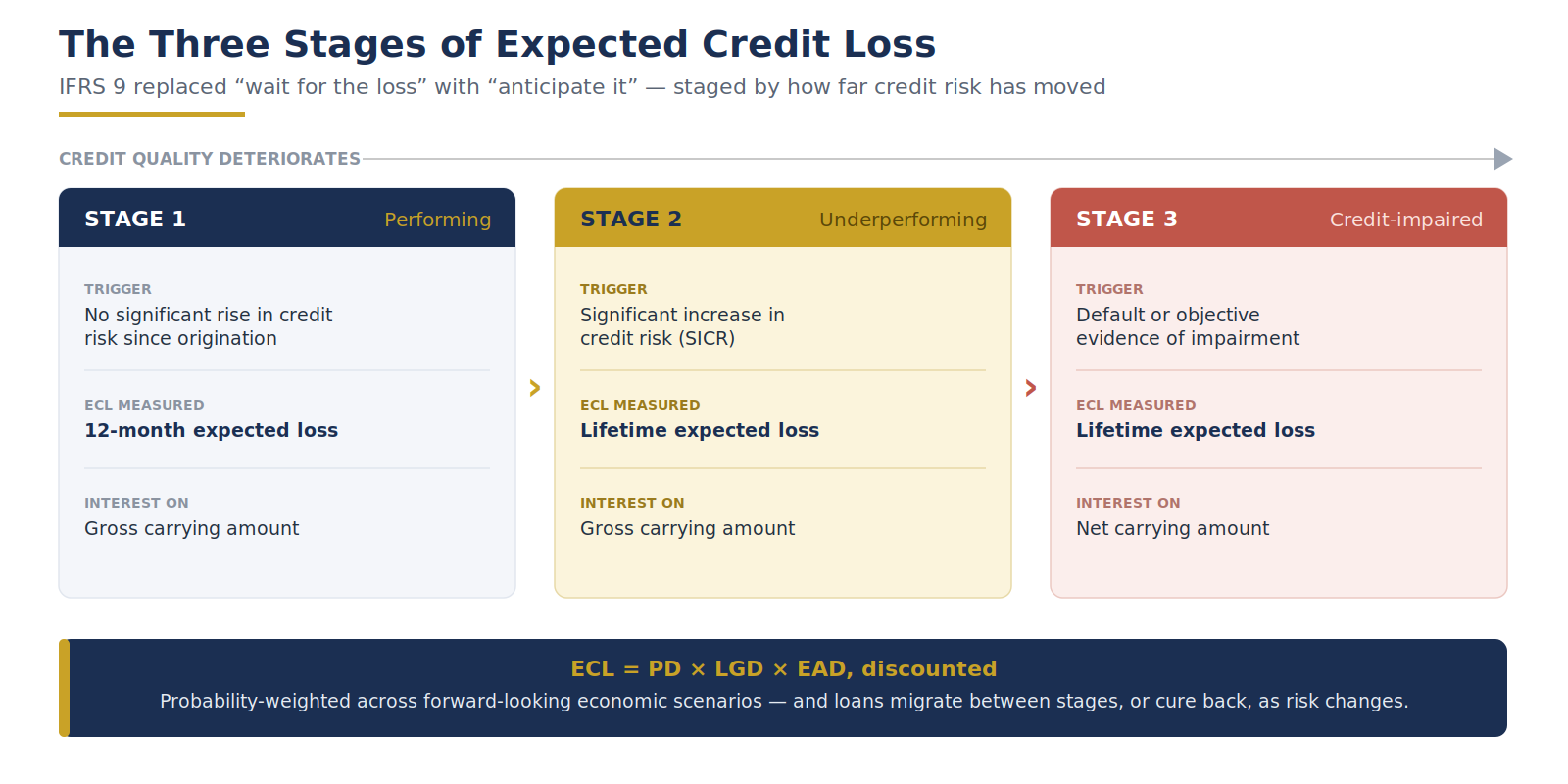

The standard organises this around three stages, defined by how much a borrower’s credit risk has changed since the loan was originated. A performing loan with no significant increase in credit risk sits in Stage 1, where the lender provides for the losses expected from defaults in the next twelve months. When credit risk increases significantly — the borrower is not yet in default, but the warning signs are there — the loan moves to Stage 2, and the provision expands to cover expected losses over the entire remaining life of the loan. When the loan becomes credit-impaired, it enters Stage 3, where it stays on a lifetime-loss basis and interest is recognised only on the net amount the lender still expects to recover.

The three-stage model: provisioning expands from a 12-month to a lifetime view as a loan’s credit risk deteriorates.

The mechanism that drives this — the judgement about when credit risk has increased significantly, often abbreviated to SICR — is the hinge on which the whole model turns. Set the trigger too high and loans languish in Stage 1 until they default, defeating the purpose; set it too low and provisions become volatile and overstated. Defining, documenting and consistently applying that trigger is among the most consequential decisions a cooperative makes in its entire ECL framework.

The building blocks

Beneath the staging sits the actual calculation, and it is more intuitive than its acronyms suggest. An expected loss is, at heart, the product of three things: how likely the borrower is to default (the probability of default), how much the lender would lose if they did (the loss given default, after collateral and recoveries), and how much would be owed at that point (the exposure at default). Multiply them together, discount for the time value of money, and you have an expected loss for a single exposure.

Two features turn this simple arithmetic into something more demanding. The first is that the inputs must be forward-looking: they cannot rest on historical averages alone but must reflect a reasonable and supportable view of future conditions. The second is that the standard requires this view to span multiple scenarios — a base case, a more optimistic one, a more adverse one — each weighted by its probability, so the final number reflects a range of possible futures rather than a single bet. This is where rigour matters most, and where undisciplined practice most often slips back into guesswork.

Where the guesswork creeps in

If expected credit loss has a reputation for subjectivity, it is because it contains several points where judgement is unavoidable — and where undocumented judgement looks exactly like guessing. The definition of a significant increase in credit risk is one. The choice and weighting of economic scenarios is another. So-called management overlays — adjustments applied on top of the model to capture risks the model does not — are a third, and the most easily abused. None of these is illegitimate; judgement is a proper part of the process. What separates discipline from guesswork is whether each judgement is defined in advance, grounded in evidence, documented, and applied consistently from one period to the next.

The test is simple: could the institution explain to its auditor and its regulator exactly why each number is what it is, and would it arrive at the same answer next year by the same logic? Where the answer is yes, the judgement is sound. Where the methodology is quietly reinvented each reporting date to land on a convenient figure, the guesswork is real — and it is precisely what a credible ECL framework exists to eliminate.

The Caribbean cooperative challenge

The difficulties that make ECL demanding everywhere are sharper for Caribbean cooperatives. Loss-history data is often short and incomplete, making the estimation of default and recovery rates genuinely hard. Specialist modelling capacity is scarce and expensive. Portfolios can be concentrated — in a few large members, a single sector, or one local economy — so that the comfortable assumptions of large, diversified books simply do not hold. And the forward-looking scenarios the standard demands must be built for small, open, often tourism- or commodity-dependent economies, for which off-the-shelf macroeconomic forecasts are a poor fit.

None of this puts sound ECL out of reach. The standard allows for proportionality — simpler approaches are acceptable for smaller or less complex institutions, provided they remain defensible — and a well-designed, appropriately simple model built on genuine local understanding will serve a cooperative far better than an elaborate one bolted on without it. The goal is not sophistication for its own sake; it is an estimate that is reasonable, supportable and consistent, scaled sensibly to the institution that produces it.

There is also a governance dimension peculiar to the sector. Many cooperatives are overseen by member-elected, often volunteer boards whose strength is community knowledge rather than technical finance, yet ECL asks them to take responsibility for a highly technical estimate. That makes clear explanation essential: a framework the board cannot understand is one it cannot properly oversee, however elegant its mathematics. Translating the model into terms a member-director can interrogate — and challenge — is not a courtesy but a core part of doing ECL properly, and it is where an advisor who can speak to both the actuary and the boardroom earns its place.

From compliance to early warning

The most overlooked truth about expected credit loss is that the discipline it demands also delivers something genuinely useful. Because the model is forward-looking and continuously updated, it functions as a live dashboard of portfolio credit quality. The migration of loans from Stage 1 into Stage 2 is, in effect, an early-warning signal — a measurable indication that credit risk is rising across a segment before it shows up as actual defaults. A cooperative that watches its staging migration, rather than merely reporting it once a year, can tighten lending, strengthen collections or shore up capital while there is still time to act.

Consider a credit union that, reviewing its quarterly staging, notices a steady drift of loans from Stage 1 into Stage 2 concentrated among members employed in a single struggling industry. No defaults have yet occurred, and the headline arrears still look normal. But the migration is unambiguous, and it prompts the union to tighten new lending to that sector, step up collections and set capital aside before the defaults arrive. A year later, when the downturn bites, the union is provisioned and prepared while less attentive lenders are scrambling. The model did not merely measure the risk — it surfaced it early enough to be managed.

Read this way, ECL stops being a cost imposed by accountants and becomes an instrument of management. The same numbers that satisfy the auditor also tell the board where the loan book is heading — which is exactly the transformation, from compliance to insight, that runs through this entire series.

What good ECL looks like

A credible expected-credit-loss framework rests on a few foundations. A clearly documented methodology, so that the board, the auditor and the regulator can all follow how a number was reached. Defined, evidence-based staging criteria, applied consistently over time. Economic scenarios genuinely relevant to the institution’s own markets, with transparent weights. Governance that owns the assumptions and the overlays rather than leaving them to be set quietly at the margin. And periodic back-testing — comparing what the model predicted against what actually happened — so that the framework learns and improves. Build on those foundations and the guesswork disappears, replaced by an estimate that is defensible today and better tomorrow.

Expected credit loss arrived in the Caribbean cooperative sector as a source of anxiety, and for institutions that approached it as a box to be ticked, the anxiety was justified — undocumented judgement is fragile, and an auditor will find it. But the standard, properly understood, is not an exercise in guessing at all. It is a discipline for thinking clearly and honestly about the losses a loan book will produce, before it produces them. Cooperatives that embrace that discipline gain three things at once: provisions they can defend, regulators and auditors they can satisfy, and an early-warning system that protects the members whose savings they hold. That is expected credit loss without the guesswork — and it is well within reach.

| TAKE THE NEXT STEP

Book an ECL Model Health-Check We will review your staging criteria, scenario design, model inputs and governance against the standard and your auditor’s expectations — and show you how to turn a compliance burden into a defensible provision and a genuine early-warning tool for your loan book. Speak with our Actuarial Advisory team: [email protected] · 876-929-3670 · 876-665-5926 · dawgen.global About Dawgen GlobalDawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing. The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress. To explore a partnership, reach out:

|