The demand side of the asset-anchored bond: the pension funds and insurers whose liabilities make them the natural holders — and what stands between them and the supply

The first eight articles of this series built an instrument and a framework. From Backing through Kinetics, the seven pillars of BEDROCK™ set out how a Caribbean asset-anchored bond should be selected, engineered, disclosed, stress-proofed, governed, distributed, and managed. The instrument is complete. But an instrument, however well built, needs a buyer — and the next three articles turn from the supply of these bonds to the market that must receive them: the institutional capital that buys them, the regional market that trades them, and the sectors that issue them.

We begin with demand, because it is the part of the story most often misunderstood. The conventional assumption is that the Caribbean’s capital-market problem is a shortage of money — that the region is simply too small or too poor to fund its own growth. This series has argued the opposite from its first article, and this is where the argument is settled: the Caribbean does not lack capital. It holds substantial pools of long-dated institutional money, accumulated over decades, sitting in the portfolios of pension funds and insurers — institutions whose defining problem is not too little money but too few assets that match their liabilities.

This article maps that demand: who holds it, why the asset-anchored bond is built for them, what currently stands in the way of the connection, and what it would take to mobilise it. Because the central insight of the demand side is uncomfortable and liberating in equal measure: the capital to fund the Caribbean’s appreciating assets is already here, already regional, already searching for exactly the instrument this series has spent eight articles building. The task is not to create demand. It is to release it.

The Asset-Liability Mismatch, From the Other Side

This series has dwelt on the issuer’s mismatch: long-life assets funded by short-tenor bank debt. The institutional investor suffers the mirror image of the same disease. A pension fund or life insurer holds liabilities measured in decades — pensions to be paid, policies to be honoured, far into the future. Sound asset-liability management requires matching those long liabilities with long-duration, income-generating assets. The problem, across much of the Caribbean, is that the menu of such assets is desperately thin.

In the absence of long-dated corporate instruments, regional institutional portfolios concentrate where they can: in government securities, in bank deposits, in a narrow band of listed equities, and in direct real estate. This concentration is not a preference; it is a constraint. It exposes these institutions to a heavy weighting in sovereign risk, to reinvestment risk as shorter instruments mature, and to a structural shortfall of the long-duration, secured, predictable income their liabilities demand. The regulators who supervise these institutions have observed the concentration repeatedly; the institutions themselves feel it as a perennial search for assets that simply are not being issued.

The issuer’s problem is long assets funded by short debt. The institution’s problem is long liabilities funded by short assets. The asset-anchored bond resolves both at once — it is the same mismatch, solved from both ends.

This is the deep logic of the demand side. The asset-anchored bond is not merely a product an institution might tolerate; it is close to the asset such an institution would design if it could. Long tenor to match long liabilities. Fixed, predictable income to match actuarial assumptions. Senior security to satisfy prudential caution. And a loan-to-value (LTV) ratio that declines over the instrument’s life — the credit strengthening precisely as the liability it funds draws nearer. The fit is not approximate. It is structural.

Who Holds the Capital

Caribbean institutional demand is concentrated in a small number of investor classes, each with a distinct liability profile and a distinct reason the asset-anchored bond suits it.

Pension Funds

Occupational and national pension schemes carry the longest and most predictable liabilities in the region — obligations to pay retirees over horizons of twenty, thirty, forty years. Their need is for long-duration, income-generating assets that can be held to match those obligations without forcing reinvestment in uncertain future markets. A fifteen-year, fixed-coupon, senior secured bond is, for a pension fund, a near-ideal building block — and one the region’s pension sector has too few of.

Life and General Insurers

Life insurers, in particular, hold obligations stretching a generation forward and are governed by prudential capital rules that reward secured, long-duration, well-structured assets. The features those rules demand — security, coverage, governance, transparency — are precisely the features the BEDROCK™ framework engineers across its pillars. For a life insurer, a properly structured asset-anchored bond is not a compliance compromise; it is a capital-efficient holding that improves the matching of assets to long-tail liabilities.

Credit Unions and Cooperative Financial Institutions

The region’s substantial cooperative financial sector holds stable member deposits seeking yield above bank rates without undue risk. A senior secured bond with a declining LTV offers exactly that profile — a secured, income-producing asset that out-yields deposits while remaining within prudent risk tolerances — and broadens the issuer’s demand base beyond the largest institutions.

Asset Managers, Development Finance, and Private Wealth

Beyond these, regional asset managers building fixed-income portfolios, development finance institutions with explicit mandates to deepen local capital markets, and high-net-worth and family-office capital seeking secured regional exposure all extend the demand base. Development finance institutions are particularly significant: their mandate is not merely to earn a return but to catalyse the very market this series advocates, and an anchor commitment from such an institution can be the catalyst that brings a first issue to market and a new asset class into being.

What Stands Between Demand and Supply

If the demand is real and the instrument is built for it, why does the connection not already exist at scale? The honest answer is a set of frictions — none insurmountable, all addressable — that have kept latent demand from meeting potential supply.

- Unfamiliarity — the asset class is new to the region, and new asset classes face a familiarity problem: institutions cannot allocate to instruments they have not seen, underwritten, or held. The first issues must do the work of education as well as financing.

- Underwriting capacity — an institution may have the appetite but lack the internal frameworks to underwrite a structured asset-anchored bond — the credit analysis, the monitoring capacity, the board comfort. Mobilising demand means building the institutional capability to assess it.

- Regulatory clarity — prudential and investment rules shape what institutions may hold. Where those rules were written before the asset class existed, they may inadvertently constrain it — or, properly understood, may already permit it. Mapping the regulatory eligibility of asset-anchored bonds for each investor class is a precondition of mobilisation.

- Absence of precedent — a market needs precedents — standard structures, shared vocabulary, a track record of issues that performed. The absence of these is precisely the shallowness this series addresses, and the remedy is the cumulative one of Article 7: each well-built issue makes the next easier to underwrite.

None of these frictions is a shortage of capital. Each is a shortage of connection — of familiarity, capability, clarity, or precedent. And each is removable. That is what makes the demand side a matter of mobilisation rather than creation: the capital exists; the work is to clear the channel between it and the supply.

Mobilising the Demand

Mobilisation is a shared task, and it falls on several parties at once. Issuers mobilise demand by bringing instruments built to institutional standard — the seven pillars are, read from the investor’s side, a specification of what institutional capital requires. Advisers mobilise it by structuring, disclosing, and presenting issues in the form institutions can underwrite, and by helping institutions build the frameworks to assess them. Regulators mobilise it by clarifying — and where appropriate, prudently modernising — the rules that govern institutional investment, so that capital is neither forced into concentration nor barred from the assets its liabilities need. And anchor investors, especially development finance institutions, mobilise it by committing early to first issues, absorbing the familiarity risk that later investors will not have to.

The prize is large and mutual. For institutions, mobilisation means access to the long-duration, secured, income-generating assets their liabilities have always needed — better matching, lower reinvestment risk, reduced sovereign concentration. For issuers, it means access to patient, appropriately-structured growth capital. For the region, it means domestic savings funding domestic growth: pension and insurance capital, accumulated from Caribbean incomes, financing the Caribbean assets that will appreciate and the enterprises that will employ the next generation. The asset-anchored bond is, in this light, more than a financing instrument. It is a mechanism for keeping the region’s capital at work within the region.

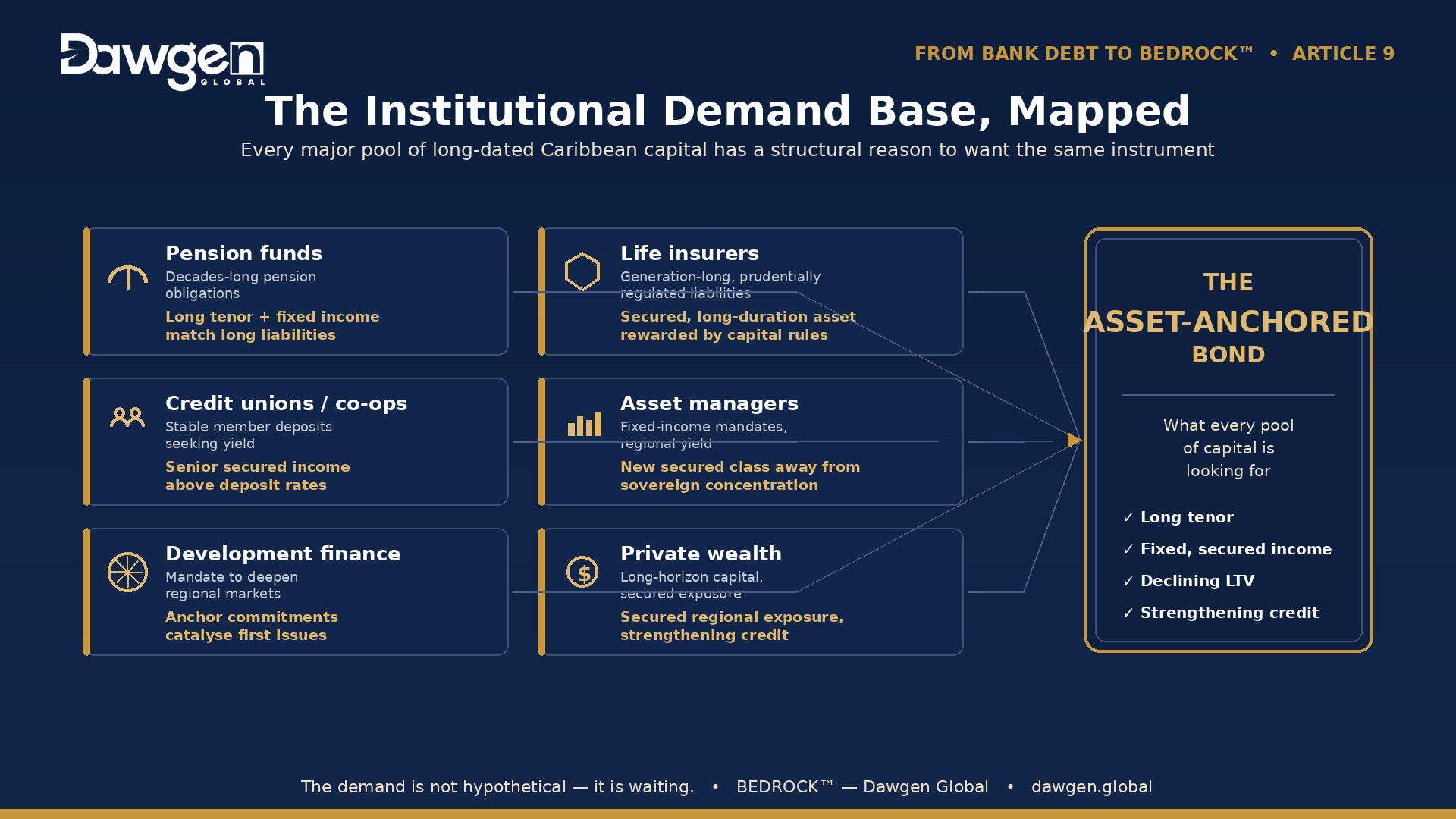

The Institutional Demand Base, Mapped

The principal investor classes, their liability profiles, and why the asset-anchored bond fits:

| Investor Class | Liability / Mandate Profile | Why the Asset-Anchored Bond Fits |

| Pension funds | Decades-long, predictable pension obligations | Long tenor and fixed income match long liabilities; declining LTV de-risks toward payout |

| Life insurers | Generation-long, prudentially regulated liabilities | Secured, long-duration, well-governed asset that rewards prudential capital treatment |

| Credit unions / co-ops | Stable member deposits seeking yield | Senior secured income above deposit rates within prudent risk limits |

| Asset managers | Fixed-income mandates seeking regional yield | A new secured asset class diversifying away from sovereign concentration |

| Development finance | Mandate to deepen regional capital markets | Anchor commitments catalyse first issues and build the asset class |

| Private wealth / family offices | Long-horizon capital seeking secured exposure | Secured regional exposure with a strengthening credit profile |

Read down the right-hand column and a single fact emerges: every major pool of long-dated Caribbean capital has a structural reason to want this instrument. The demand is not hypothetical. It is waiting.

Defined Terms

This article adds two terms to the series vocabulary:

Mirror mismatch. The structural complement between the issuer’s problem (long assets funded by short debt) and the institution’s problem (long liabilities funded by short assets) — both resolved by the same long-tenor, asset-anchored bond.

Demand mobilisation. The clearing of the frictions — unfamiliarity, underwriting capacity, regulatory clarity, and absence of precedent — that separate the Caribbean’s existing pools of long-dated institutional capital from the asset-anchored bonds their liabilities require.

The Capital Is Ready

The demand side of the Caribbean asset-anchored bond is not a problem to be solved but an opportunity to be released. The capital exists, in the region, in the hands of institutions whose liabilities make them the natural holders of these instruments. What stands between them and the supply is not scarcity but friction — and friction, unlike scarcity, can be cleared. The issuer who brings a soundly built instrument to a market this hungry is not asking for a favour; they are offering an institution exactly the asset it has been unable to find.

Which raises the question every prospective issuer should now be asking: is my enterprise ready to meet this demand? Is the asset, the structure, the disclosure, the governance — the seven pillars — at the standard institutional capital requires? That question of readiness is the one this series will close on, with a structured diagnostic that assesses an enterprise against each dimension of the framework. We will return to it in Article 12. First, the demand we have mapped needs a market deep enough to transact in — the regional bond market itself, which must be widened, standardised, and deepened to carry this capital to these assets. That is next week’s subject: Article 10, Deepening the Caribbean Bond Market.

For issuers and CFOs: the demand for well-structured Caribbean asset-anchored bonds is real and largely unmet. The question is whether your enterprise is ready to meet it. Dawgen Global’s Corporate Finance, Advisory and Restructuring teams help Caribbean issuers assess and build bond readiness across capital structure, disclosure, governance and resilience — and the BEDROCK™ Bond Readiness Index, introduced in Article 12 of this series, offers a structured assessment of where your enterprise stands. Enquiries: [email protected].

Next in the series: Article 10 — Deepening the Caribbean Bond Market. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210