The market infrastructure that turns individual issues into an asset class — standardisation, ratings, benchmarks, and the regulatory architecture of a deeper market

The previous article established that the demand exists: substantial pools of long-dated Caribbean capital, in pension funds and insurers, structurally suited to the asset-anchored bond and largely unable to find it. The article before it established that the supply can be built: the seven pillars of BEDROCK™ set out how. Demand on one side, supply on the other — and yet a transaction does not happen automatically when willing buyers and capable sellers exist. They must meet somewhere, on terms both can trust, in a venue both can use. That somewhere is the market, and in the Caribbean the market itself is the missing piece.

This article is about market infrastructure — the standards, institutions, and rules that turn a handful of individual transactions into an asset class. It is written with regulators, securities exchanges, policymakers, and development institutions in mind, because while issuers and advisers can build instruments and investors can hold them, only the architects of market infrastructure can build the venue in which they trade. The deepening of the Caribbean bond market is a public undertaking as much as a private one, and it deserves to be seen as a development priority, not merely a financial-sector technicality.

The argument proceeds in three movements: why a deep domestic bond market matters for the region’s development; what infrastructure a deep market requires and where the gaps currently lie; and how a standard like BEDROCK™ contributes to the deepening. The through-line is a conviction this series has held throughout: the shallowness of the Caribbean bond market is not a fixed feature of a small region but a solvable problem of infrastructure — and solving it is among the highest-leverage development investments the region can make.

Why a Deep Bond Market Matters

A deep domestic bond market is not a luxury of advanced economies; it is a foundation of resilient development. Its absence imposes costs the region pays quietly every day, and its presence delivers benefits that compound across the whole economy.

Consider what a deep market provides. It gives enterprises an alternative to bank dependence — the long-tenor, appropriately-structured capital this series has described — reducing the refinancing fragility that Article 1 identified as a systemic Caribbean weakness. It gives institutional investors the domestic assets their liabilities require, keeping pension and insurance savings invested productively at home rather than exported in search of matching assets abroad. It diversifies the financial system itself, reducing the economy’s dependence on bank lending and the concentration risk that dependence creates. It deepens the transmission of capital from savers to productive enterprises without the bank’s balance sheet standing in the middle. And it builds the financial sovereignty of a region whose development has too often been hostage to the availability and pricing of external capital.

The shallowness of the Caribbean bond market is not a fixed feature of a small region. It is a solvable problem of infrastructure — and solving it is among the highest-leverage development investments the region can make.

These are not abstract benefits. A region that can fund its hotels, its renewable energy, its ports and logistics, its productive enterprises through its own institutional capital is a region that captures the returns on its own growth, employs its own people building its own assets, and weathers external shocks from a position of structural strength. Deepening the bond market is, in the end, a question of who finances the Caribbean’s future — and on whose terms.

The Infrastructure a Deep Market Requires

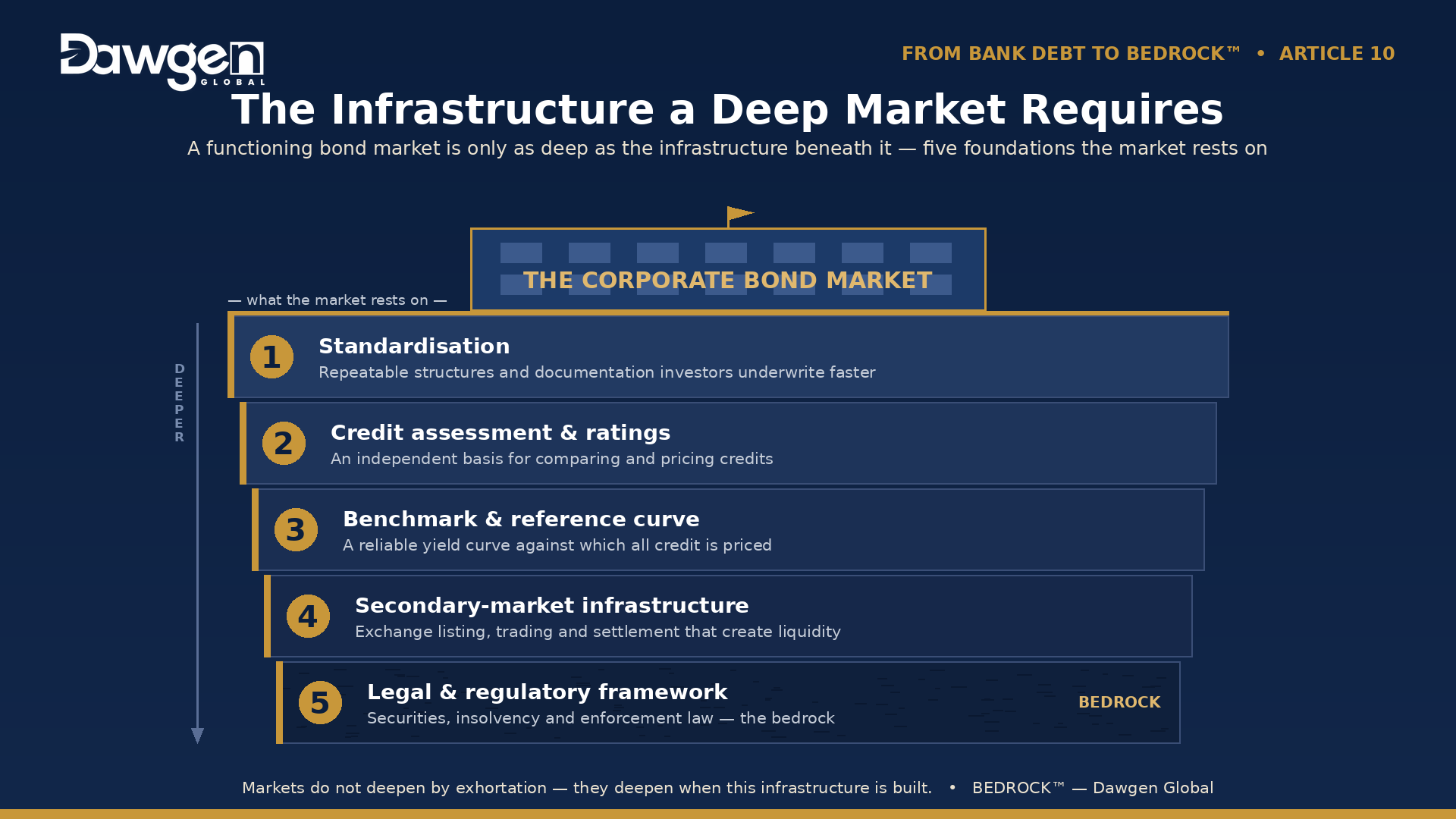

Markets do not deepen by exhortation; they deepen when specific infrastructure is built. A functioning corporate bond market rests on a set of enabling components, several of which are underdeveloped across much of the region. Naming them is the first step to building them.

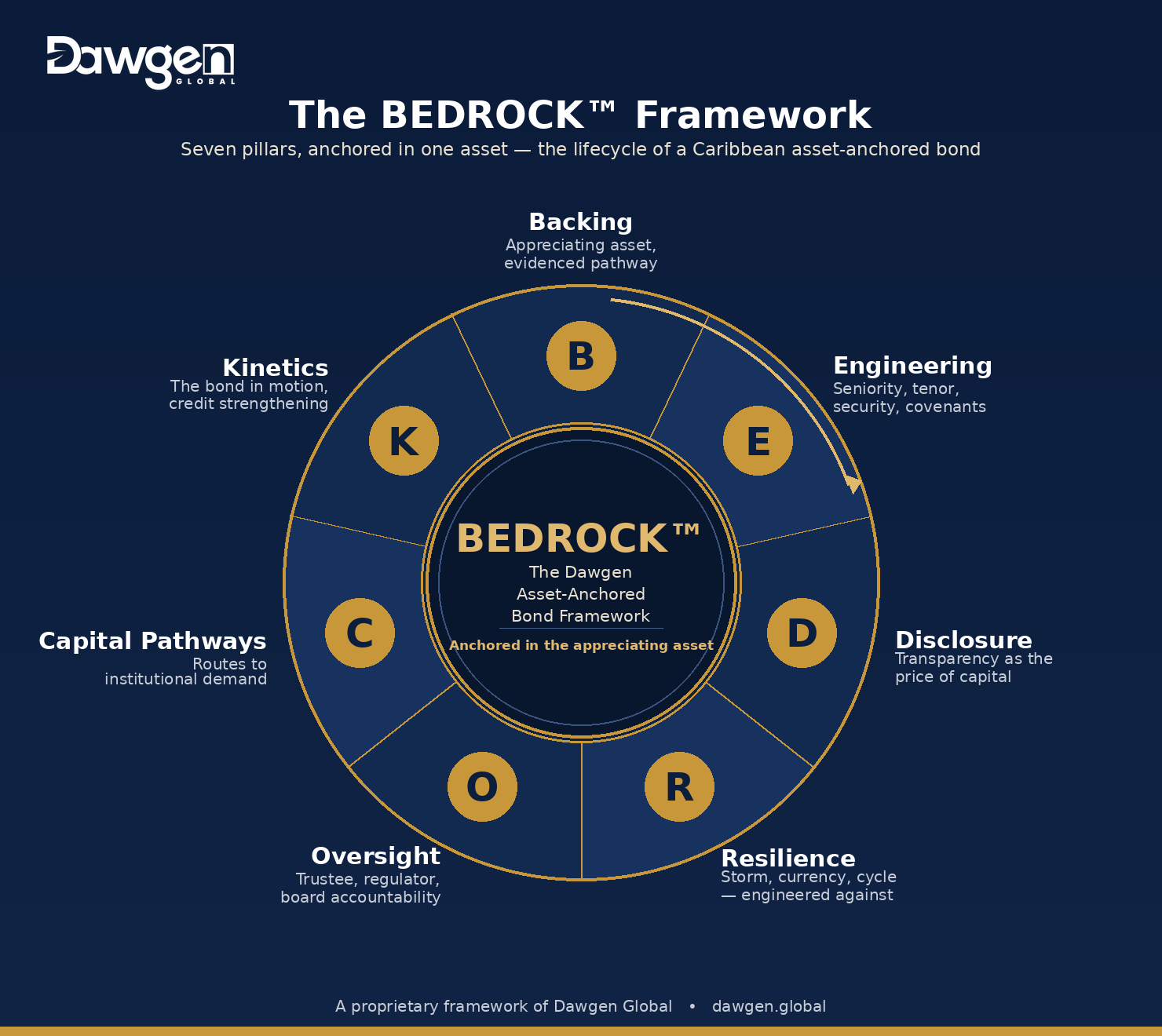

Standardisation

A market in which every instrument is bespoke is a market that cannot scale. Investors underwrite faster, and price more competitively, when structures follow recognised templates — standard covenant packages, standard security architectures, standard disclosure formats. A framework like BEDROCK™ contributes precisely here: by offering a coherent, repeatable standard for how an asset-anchored bond is built and documented, it lowers the cost of underwriting each new issue and accelerates the familiarity the demand side requires.

Credit Assessment and Ratings

Investors need an independent basis for comparing credits. In deep markets, this is supplied by credit rating agencies; in the regional context, ratings capacity is thinner, and the development of credible domestic or regional credit assessment — whether through rating agencies, scoring methodologies, or trusted advisory assessment — is a precondition of scale. The disclosure and structural discipline of the BEDROCK™ framework is designed to make credits assessable; a market also needs the institutions that do the assessing.

Benchmarks and a Reference Curve

Pricing requires a reference. A functioning market needs a reliable benchmark yield curve — typically built from government securities across tenors — against which corporate credit can be priced, as Article 7 described. Where the sovereign curve is incomplete or illiquid, corporate pricing loses its anchor. Building and maintaining a credible benchmark curve is a public-good function that underpins all private issuance.

Secondary Market and Trading Infrastructure

A bond an investor cannot sell is worth less than one they can. Secondary-market infrastructure — exchange listing, trading platforms, market-makers, settlement systems — converts a static holding into a liquid asset, and liquidity, as Article 8 noted, is part of what the investor buys. Regional exchanges have a central role here: every step that makes listed bonds easier to trade widens the investor base willing to hold them in the first place.

The Regulatory and Legal Framework

Underpinning all of it is the legal and regulatory architecture: securities law that enables efficient issuance while protecting investors; insolvency and security-enforcement law that makes the security perimeter of Article 3 reliable in practice; and prudential rules for institutional investors that permit — rather than inadvertently obstruct — allocation to well-structured corporate bonds. This is the domain where policymakers and regulators hold the decisive levers, and where modernisation can unlock disproportionate private activity.

How a Standard Deepens the Market

A framework cannot, by itself, build an exchange or write a securities law. But a widely-adopted standard contributes to market deepening in ways that complement the infrastructure only public actors can provide — and understanding the complementarity clarifies the respective roles.

A standard supplies the common language. When issuers, advisers, and investors share a vocabulary — the seven pillars, the defined terms this series has accumulated, the recognisable structure of an asset-anchored bond — each transaction becomes legible to all parties faster and more cheaply. A standard supplies the template that makes standardisation real, the disclosure discipline that makes credits assessable, and the structural quality that makes secondary buyers willing to trade. And a standard supplies precedent: each issue built to a recognised framework is not only a financing but a contribution to the shared infrastructure, a worked example that the next issuer, the next investor, and the next regulator can learn from.

This is the complementarity at the heart of market deepening. Public actors build the venue — the exchange, the benchmark, the legal framework, the prudential rules. Private actors build the instruments and the standards that make those instruments consistent and trustworthy. Neither substitutes for the other. A pristine exchange with no quality issuance is empty; excellent issuance with no venue to trade in is trapped. The Caribbean bond market will deepen when both are built together — which is why this article addresses itself to the public architects of market infrastructure as deliberately as the rest of the series addresses issuers and investors.

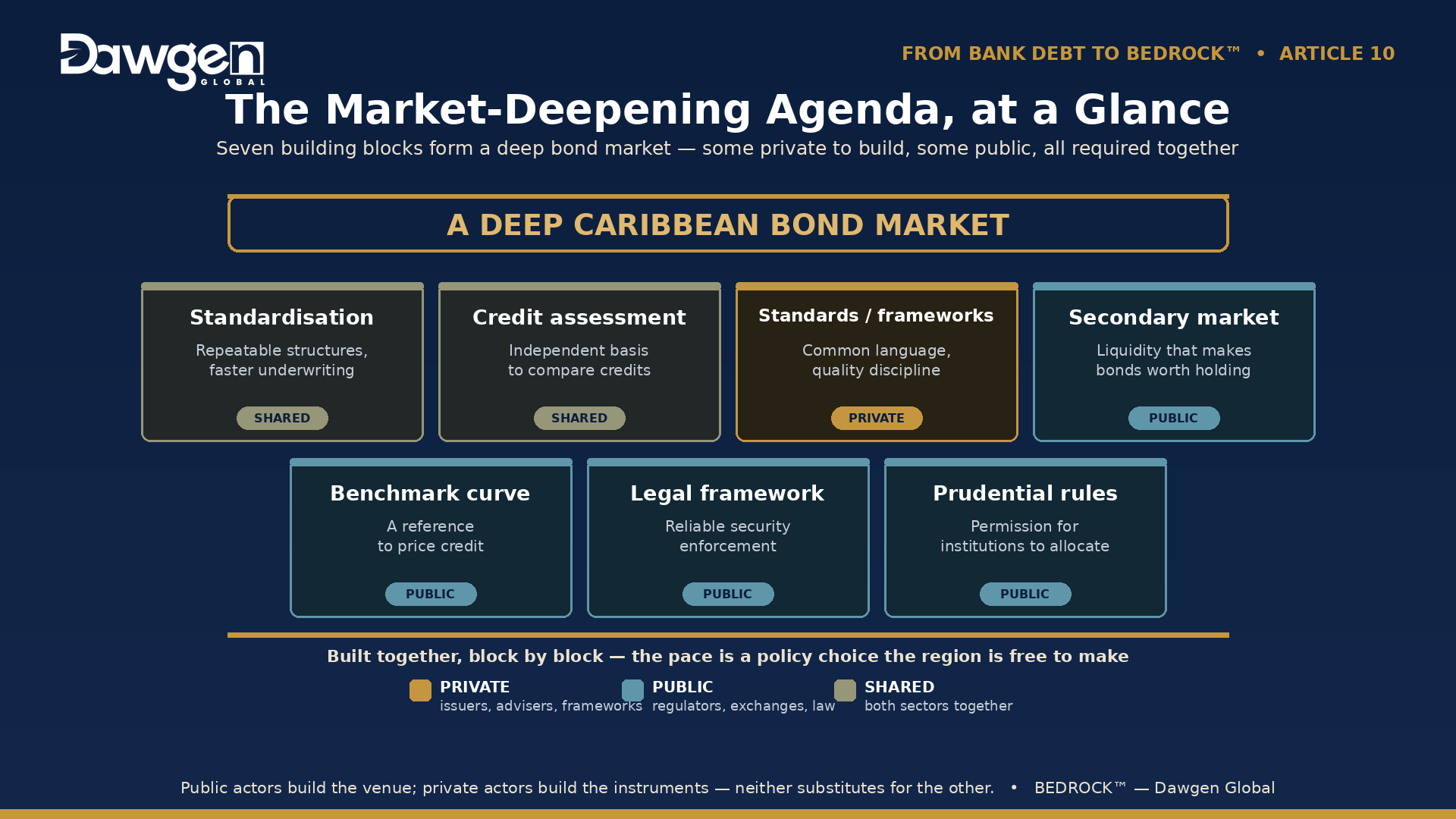

The Market-Deepening Agenda, at a Glance

The building blocks of a deep corporate bond market, the role each plays, and where the principal effort lies:

| Building Block | What It Provides | Where the Effort Lies |

| Standardisation | Repeatable structures investors underwrite faster | Adoption of common frameworks and documentation |

| Credit assessment | Independent basis for comparing credits | Building regional ratings and assessment capacity |

| Benchmark curve | A reference against which to price credit | Maintaining a liquid sovereign yield curve |

| Secondary market | Liquidity that makes bonds worth more to hold | Exchange listing, trading and settlement infrastructure |

| Legal framework | Reliable security enforcement and issuance | Securities, insolvency, and enforcement law |

| Prudential rules | Permission for institutions to allocate | Modernising investment rules for the asset class |

| Standards / frameworks | Common language and quality discipline | Private adoption; public recognition |

Read across the table and the division of labour is clear: the private sector can supply standardisation, quality, and frameworks; the public sector holds the levers on benchmarks, legal architecture, prudential rules, and the exchange infrastructure. The deepening happens where the two are pursued together — and the pace of it is a policy choice the region is free to make.

Defined Terms

This article adds two terms to the series vocabulary:

Market deepening. The building of the infrastructure — standardisation, credit assessment, benchmark curves, secondary-market and legal architecture, and prudential permission — that turns isolated bond issues into a functioning, liquid asset class capable of channelling domestic savings to domestic enterprise.

Public-private complementarity. The division of labour in which public actors build the market’s venue and rules while private actors build the instruments and standards — neither substituting for the other, both required for a corporate bond market to deepen.

A Market Worth Building

The deepening of the Caribbean bond market is a generational opportunity disguised as a technical agenda. Behind the standardisation and the benchmark curves and the prudential rules lies a simple proposition: a region that builds the infrastructure to channel its own institutional savings into its own appreciating assets changes the terms on which it develops. It becomes less dependent on external capital, more resilient to external shocks, and more fully the author of its own growth. That prize justifies treating market infrastructure as the development priority it is.

The standard this series has built is one private contribution to that public undertaking — a coherent, repeatable framework that makes the instruments consistent, the credits assessable, and the asset class legible. But standards and instruments need somewhere to exist. The market must be deepened by those who hold its levers, and the invitation of this article is to see that deepening as worth the effort. With demand mapped and the market addressed, one question remains for the supply side: where, across the Caribbean economy, do the appreciating assets that can anchor these bonds actually lie? That is next week’s subject: Article 11, Where Bedrock Works: Sector Applications.

For policymakers, regulators, exchanges and institutional investors: deepening the regional bond market is a shared undertaking, and Dawgen Global works across the ecosystem — advising issuers on bond readiness, supporting institutions on credit assessment and allocation, and contributing to the standards that make a deeper market possible. For issuers weighing whether their enterprise is ready to participate, the BEDROCK™ Bond Readiness Index, introduced in Article 12, offers a structured assessment. Enquiries: [email protected].

Next in the series: Article 11 — Where Bedrock Works: Sector Applications. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210