Pillar B of the BEDROCK™ Framework: what qualifies an asset to anchor a bond — and what the discipline of appreciation demands

This series opened with a diagnosis: the Caribbean’s growth constraint is not a shortage of viable enterprises but a shortage of appropriate capital structure — and the corporate bond, secured by capital-appreciating assets, is the missing middle between mismatched bank debt and dilutive equity. We introduced BEDROCK™, the Dawgen Asset-Anchored Bond Framework, and named its defining proposition: the inverted credit curve, the property of an instrument whose credit quality strengthens over tenor because its collateral appreciates while its debt is constant or declining.

That proposition stands or falls on its first pillar. If appreciation is asserted rather than evidenced, the inverted credit curve is a marketing slogan; if appreciation is disciplined, demonstrated, and conservatively valued, it is a structural fact that changes how Caribbean credit should be designed and priced. Pillar B — Backing — is the doctrine of that discipline. It answers the question every BEDROCK™ instrument must answer before any other: does the backing asset have a credible, evidenced appreciation pathway that strengthens the credit over the life of the bond?

This article sets out the Backing doctrine in full: what qualifies an asset to anchor a bond, what drives genuine appreciation, what valuation discipline demands, how loan-to-value philosophy should be built, and — in numbers — how appreciating collateral inverts the credit curve. It also sets out, with equal care, what does not qualify. A doctrine that cannot say no is not a doctrine.

Collateral Is Not Backing

Begin with a distinction conventional practice blurs. Collateral, as the regional banking tradition uses the term, is whatever the lender can charge: any asset, in any condition, valued at forced-sale discount, held against the day of default. Backing, in the BEDROCK™ sense, is narrower and more demanding. A backing asset is one selected for the role — an asset whose economic character actively supports the instrument it anchors, whose value pathway is evidenced, and whose appreciation is engineered into the bond’s mechanics rather than left as an unpriced accident.

The distinction matters because it reverses the order of analysis. Conventional secured lending starts with the borrower and asks what security can be taken. The Backing doctrine starts with the asset and asks whether it deserves a bond. Four tests follow, and an asset must pass all four to qualify:

- Long economic life. The asset’s productive and value-bearing life must comfortably exceed the proposed tenor — the foundation of tenor matching, which Pillar E will engineer.

- Evidenced appreciation pathway. There must be a credible, documented basis — market evidence, structural demand drivers, supply constraint — for expecting the asset’s value to rise over the instrument’s life. Hope is not a pathway; comparable transaction history, demonstrable scarcity, and durable demand fundamentals are.

- Independent valuability. The asset must be capable of credible, repeatable, third-party valuation on a recognised methodology. An asset that cannot be independently valued cannot be transparently revalued — and revaluation, as we shall see, is where the inverted credit curve becomes contractual rather than rhetorical.

- Income alignment. The asset must generate, or directly enable, the cash flows that service the bond. Backing protects the debt; it does not pay the coupon. An appreciating asset with no income story is a speculation, not an anchor.

Conventional lending asks what security can be taken from the borrower. The Backing doctrine asks whether the asset deserves a bond. The order of analysis is the doctrine.

The Qualifying Asset Classes

Applied to the Caribbean’s economic geography, the four tests admit four broad asset classes — each with its own appreciation logic and its own discipline requirements.

Tourism and Hospitality Real Estate

Beachfront and resort-adjacent property in established corridors is the region’s signature appreciating asset. The appreciation logic is structural: coastline is finite, planning regimes constrain supply in mature corridors, and long-haul tourism demand has shown durable secular growth across decades, recovering even from severe shocks. The discipline requirement is equally structural: tourism assets carry the region’s highest catastrophe and demand-cycle exposure, which is why Pillar R — Resilience — exists, and why the income test must be stressed against cyclical downside rather than averaged across good years.

Logistics and Trade Infrastructure

Warehousing, distribution facilities, cold-chain capacity, and port-adjacent industrial property ride two durable currents: the structural growth of regional trade and e-commerce fulfilment, and the scarcity of serviced industrial land near the region’s ports and airports. Appreciation evidence here rests on land scarcity and replacement-cost dynamics; the discipline requirement is tenant quality and lease tenor, since logistics income is only as durable as the contracts behind it.

Energy and Utility Installations

Renewable generation — solar, wind, and increasingly storage — occupies a distinctive position in the doctrine. The underlying plant depreciates physically, but the asset as an economic unit — site, interconnection, licence, and long-term offtake arrangement — can appreciate as regional energy economics shift and as contracted cash flows season. Backing analysis here is therefore a composite: the appreciation pathway attaches to the rights and contracts as much as to the hardware, and valuation discipline must separate the two honestly.

Prime Commercial and Mixed-Use Property

Well-located office, retail, and mixed-use assets in the region’s capital-city cores and growth corridors qualify where location scarcity and replacement cost support the pathway. The discipline requirement is candour about secular occupancy trends: a building’s location may appreciate while its current configuration does not, and the valuation must price the asset, not the nostalgia.

These four classes are the doctrine’s centre of gravity, not its boundary. Agricultural land with irrigation and title security, marina and yachting infrastructure, and education and healthcare campuses can each qualify where the four tests are genuinely met. The tests govern; the list illustrates.

The Appreciation Evidence Standard

Pillar B’s most important sentence is also its most uncomfortable: appreciation must be evidenced, not asserted. Every offering document in history has claimed its asset would rise in value. The BEDROCK™ standard asks the issuer to show the machinery, and recognises four legitimate appreciation drivers — each of which can be documented, and none of which is “the market always goes up”:

- Scarcity — the asset class faces binding physical or regulatory supply constraint in its corridor — finite coastline, zoning limits, serviced-land scarcity — demonstrable from planning data and development pipelines.

- Structural demand — demand for the asset’s use rests on durable structural currents — tourism’s long-run growth, trade and fulfilment expansion, energy transition economics — evidenced from published market data rather than issuer projection alone.

- Replacement-cost dynamics — construction cost inflation raises the cost of replicating the asset, supporting the value of existing stock — evidenced from published cost indices and comparable development budgets.

- Infrastructure uplift — committed public or private investment — highways, airport expansion, port deepening, utility upgrades — demonstrably raises the value of assets in its catchment, evidenced from announced and funded projects rather than speculation.

The evidence package supporting a BEDROCK™ issuance should document the applicable drivers with sources an institutional investor can verify: comparable transactions over a meaningful period, published market studies, planning and development data, and regulatory or infrastructure commitments. Where the evidence is thin, the honest conclusions are lower assumed appreciation, lower issuance loan-to-value, or no issuance. The doctrine’s credibility is bought with the deals it declines.

Valuation Discipline: The Doctrine’s Spine

Everything in the Backing doctrine routes through valuation, because the inverted credit curve is only as real as the numbers that measure it. Four rules constitute the discipline.

Independence Without Exception

Valuation at issuance and at every revaluation must be performed by a qualified, independent valuer with no economic interest in the transaction, on a recognised professional standard, with methodology and key assumptions disclosed to investors. The issuer may commission the valuation; the issuer may not shape it.

Conservatism by Construction

The doctrine prices prudence into the inputs: valuations for backing purposes should rest on current evidenced value — not projected value, not “on completion” value for operating assets, and not the upper end of a range. Where a development or expansion component exists, the structure should distinguish as-is value from on-completion value and advance against each on its own discipline, with milestone mechanics governed under Pillar O.

Dual-Basis Honesty

Backing valuations should disclose both market value and a stressed disposal basis. The first measures the inverted credit curve; the second tells investors what protection survives a bad day. An issuer reluctant to show the second number is telling investors something important.

Contractual Revaluation Cadence

Revaluation on a fixed cadence — the doctrine’s default is every three years, with event-driven revaluations for material changes — must be written into the bond’s terms, not left to issuer discretion. This is the mechanism that converts appreciation from narrative into covenant: each revaluation recalculates loan-to-value, and the recalculation drives the consequences — step-downs, releases, or top-ups — that Pillar K will govern.

Loan-to-Value Philosophy: Headroom as Doctrine

Loan-to-value is where Backing becomes arithmetic. The BEDROCK™ philosophy rests on three principles.

First, the issuance ceiling is the safety architecture. Because the doctrine claims the credit will strengthen, it must begin from a position that survives being wrong. A disciplined issuance loan-to-value — for most qualifying classes, materially below the levels aggressive bank lending will sometimes reach — ensures that even a multi-year stall in appreciation, or a sharp one-time shock, leaves the instrument covered. The ceiling is not a concession to nervous investors; it is the premise that makes every other claim honest.

Second, the trajectory is the product. What the issuer is selling, and what the investor is buying, is not merely a ratio at issuance but a designed path: a loan-to-value that begins conservative and — under evidenced appreciation with the debt constant or amortising — declines year by year. The offering should present that trajectory explicitly, under base and stressed assumptions, so that the inverted credit curve is a disclosed, testable feature of the instrument.

Third, headroom has uses. The widening gap between asset value and debt is not decorative: it is the raw material of the instrument’s later life — pricing step-downs earned at revaluation, partial security releases, or refinancing capacity for the next phase of growth. Pillar K — Kinetics — will set out the mechanics; Pillar B’s contribution is to design the headroom in from the start.

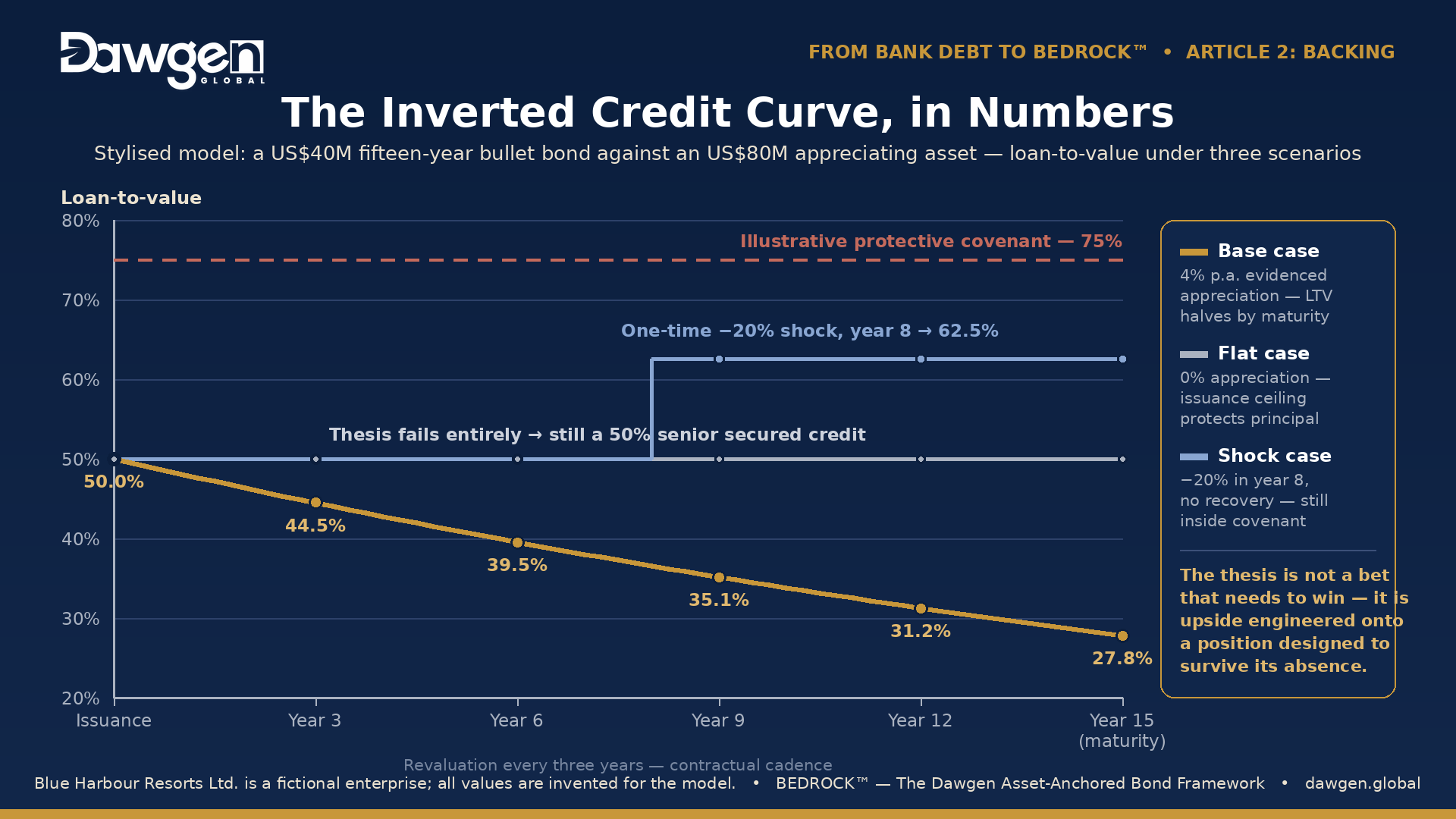

The Inverted Credit Curve, in Numbers

Return to Blue Harbour Resorts Ltd., the stylised hospitality company introduced in Article 1. Blue Harbour issues a fifteen-year senior secured bullet bond of US$40 million against its expanded beachfront property, independently valued at US$80 million at issuance — an issuance loan-to-value of 50%. The evidence package supports a conservative base-case appreciation assumption of 4% per annum for the corridor; the offering also discloses a flat case (no appreciation for the full term) and a shock case (a one-time 20% value decline in year eight, with no other growth). The debt is a bullet: it does not amortise at all. Every improvement in the ratio below is the work of the asset alone.

| Year | Base case: 4% p.a. | Flat case: 0% p.a. | Shock case: −20% in yr 8 |

| Issuance | 50.0% | 50.0% | 50.0% |

| Year 3 (revaluation) | 44.5% | 50.0% | 50.0% |

| Year 6 (revaluation) | 39.5% | 50.0% | 50.0% |

| Year 9 (revaluation) | 35.1% | 50.0% | 62.5% |

| Year 12 (revaluation) | 31.2% | 50.0% | 62.5% |

| Year 15 (maturity) | 27.8% | 50.0% | 62.5% |

Read the three columns as the doctrine in miniature. In the base case, the bond matures at a loan-to-value below 28% — a credit roughly twice as covered as the day it was issued, with every revaluation contractually recording the improvement and, under well-engineered terms, rewarding it. In the flat case — fifteen years in which the evidenced appreciation simply fails to materialise — the investor still holds a 50% loan-to-value senior secured instrument for the full term: the issuance ceiling means being wrong about appreciation costs the thesis, not the principal. And in the shock case, a one-time 20% collapse in year eight — with no recovery ever — takes the ratio only to 62.5%, still comfortably inside the protective covenant levels a disciplined structure would set. The appreciating-asset thesis, built properly, is not a bet that needs to win. It is an upside engineered onto a position designed to survive its absence.

Blue Harbour Resorts Ltd. is a fictional enterprise created for illustrative purposes. All values, percentages, and assumptions are invented for the model and do not reference any actual company, property, or engagement.

What Does Not Qualify

A doctrine that cannot say no is not a doctrine. The following fail the Backing tests, and no structuring ingenuity should be spent rescuing them:

- Depreciating operational assets — vehicles, standard plant and equipment, IT estates, and similar wasting assets. They are legitimate collateral for matched-tenor bank and lease finance; they cannot anchor an instrument whose premise is appreciation.

- Speculative land — raw land with no income, no development consent, and an appreciation case resting on hope. It fails the income test and usually the evidence test; it is land banking, not backing.

- Volatile or intangible primary security — inventory, receivables, and brand valuations as primary anchors. Some may strengthen a wider security package under Pillar E, but none can carry the appreciating-asset premise on its own.

- Clouded title — assets with unresolved title, unregistrable charges, informal tenure, or material boundary and probate disputes. If the security cannot be perfected cleanly, the analysis never reaches valuation.

- Unmitigated single-point dependence — backing concentrated in a single asset whose value depends on a single counterparty, a single licence, or a single individual’s involvement, without structural mitigants. Appreciation evidence cannot cure a concentration the structure refuses to address.

Declining these is not conservatism for its own sake. Every weak instrument that reaches the regional market raises the risk premium demanded of the next strong one. Pillar B protects the issuer and the investor — and, just as deliberately, the market.

Defined Terms

Pillar B adds four terms to the series vocabulary:

Qualifying backing asset. An asset that passes the four Backing tests — long economic life, evidenced appreciation pathway, independent valuability, and income alignment — and is therefore eligible to anchor a BEDROCK™ instrument.

Appreciation evidence standard. The documentation discipline requiring every claimed appreciation pathway to rest on verifiable drivers — scarcity, structural demand, replacement-cost dynamics, or infrastructure uplift — supported by sources an institutional investor can independently check.

Issuance LTV ceiling. The conservative maximum loan-to-value at which an asset-anchored bond may be issued — set so that the instrument remains protected even if the appreciation thesis fails entirely.

LTV trajectory. The disclosed, designed path of an instrument’s loan-to-value over its life under base and stressed assumptions — the testable expression of the inverted credit curve.

The Pillar in One Question

Every pillar of the BEDROCK™ Framework reduces to a governing question, and Backing’s is the one on which all the others stand: does the backing asset have a credible, evidenced appreciation pathway that strengthens the credit over the life of the bond? Answered honestly — with the four tests, the evidence standard, independent valuation, and a ceiling that survives being wrong — that question turns the Caribbean’s most abundant endowment, its appreciating real assets, into the foundation of its missing capital market.

But a qualifying asset is only the beginning. An anchor needs an instrument built to hold it: seniority that means something, tenor that matches the asset, covenants that breathe with the credit, and reserves that buy time when the cycle turns. That is structural engineering — and it is next week’s subject: Article 3, Engineering: Designing Bonds That Match the Asset, including the doctrine’s answer for issuers whose balance sheets must be repaired before they can be anchored.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning. Enquiries: [email protected].

Next in the series: Article 3 — Engineering: Designing Bonds That Match the Asset. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210