In Article 6 of this series, I argued that the capital structure which worked in 2021 will not work in 2026 — and that the refinance, the hedge, and the equity raise belong on the next board agenda. This week, the series turns to a less visible but equally consequential question: what does it mean to operate a Caribbean enterprise in a monetary environment that has shifted decisively since 2022, and that is now stabilising in ways most firm-level decisions have not yet caught up with?

Chapter 5 of the IDB’s 2026 Macroeconomic Report carries the title “Challenges for Monetary Authorities in Latin America and the Caribbean.” Its central finding is genuinely good news for our region: inflation-targeting regimes — including Jamaica’s, explicitly named in the IDB’s classification — have largely succeeded in returning inflation to target. The disinflation, the chapter notes, was “rapid” and “successful.” The credibility our central banks rebuilt during the surge is now paying compounding dividends.

The chapter also flags a less reassuring finding. Successful disinflation is necessary, but it is not the same as anchored expectations. Economic agents — firms, employees, customers, suppliers — who lived through the 2021-23 inflation surge can keep inflation expectations elevated for years after actual inflation has normalised. The IDB references the Malmendier and Nagel (2016) finding that periods of high inflation influence consumer expectations “for a long time.” The Pedemonte, Toma, and Verdugo (2025) work the chapter cites shows that these persistently elevated expectations have meaningful macroeconomic effects — slower disinflation, higher prices, and continued upward pressure on demand.

For Caribbean entrepreneurs, this finding maps onto a specific risk inside the firm. The pricing assumptions, contract escalators, and wage philosophy that the leadership team locked in during the 2022 inflation panic are almost certainly still in operation. They were calibrated to a world that no longer exists. The firms that recalibrate them this quarter will gain pricing discipline and competitive position. The firms that do not will continue to operate with cost structures and pricing assumptions designed for a problem that has largely been solved.

Where the region’s monetary regimes actually sit

The IDB chapter groups regional economies into three categories based on their monetary policy regimes. The grouping is useful for Caribbean entrepreneurs because it tells you, with precision, how the local environment is likely to behave under future shocks.

Inflation targeters. Brazil, Chile, Colombia, Costa Rica, the Dominican Republic, Guatemala, Jamaica, Mexico, Paraguay, Peru, and Uruguay. These economies have explicit inflation targets and central banks that adjust policy rates to maintain them. The IDB shows that across these economies, inflation has largely returned to target. They have small output gaps. Their monetary authorities have credibility, and that credibility is itself an asset on every Caribbean firm’s balance sheet operating inside these economies.

Fixers. Economies whose currencies are pegged to a reference (typically the U.S. dollar) or operate under a currency board arrangement. The Bahamas, Belize, Bolivia, the Eastern Caribbean Currency Union (Antigua and Barbuda, Dominica, Grenada, Saint Kitts and Nevis, Saint Lucia, Saint Vincent and the Grenadines), and Panama. These economies import the monetary policy of the anchor currency. They have less domestic flexibility but more nominal-exchange-rate stability. Their adjustment to shocks happens through other channels — fiscal policy, capital flows, real-economy adjustment — rather than through the exchange rate.

Others. Economies with alternative monetary policy regimes — managed exchange rates, partial dollarisation, or hybrid arrangements. The IDB notes that many of these economies still face higher inflation, larger output gaps, and lower credibility scores than the inflation-targeting group.

For Caribbean entrepreneurs, the practical implication is direct. The same firm operating across Jamaica, the Bahamas, and the Eastern Caribbean is operating across three meaningfully different monetary policy regimes. The Jamaican unit will see exchange rate flexibility absorb external shocks. The Bahamian unit will see the fixed peg hold; the adjustment will land elsewhere. The OECS units will operate inside a currency board arrangement that has held for decades but constrains domestic policy flexibility. A treasury policy designed for one of these environments may be inappropriate for another. The firm operating across multiple Caribbean jurisdictions needs distinct monetary-regime-aware policies for each.

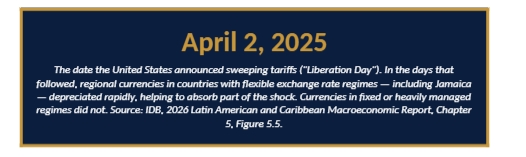

Liberation Day: what the April 2, 2025 episode actually revealed

On April 2, 2025, the United States announced a sweeping package of tariff measures that became known as “Liberation Day.” The IDB chapter examines what happened to regional exchange rates in the days that followed, and the finding is unusually clean.

Currencies in countries with flexible exchange rate regimes — Brazil, Chile, Colombia, Mexico, Peru, Jamaica — depreciated rapidly in the immediate aftermath. The depreciation absorbed part of the external shock. Trade-cost increases that would otherwise have landed directly on local producers were partly offset by the cheaper local currency, which restored some of the price competitiveness lost to the tariff. By contrast, currencies in fixed or heavily managed regimes did not move — the shock landed elsewhere in the economy, typically in the form of softer demand, slower investment, and pressure on fiscal accounts.

This is the cleanest single piece of evidence in the entire IDB report on why flexible exchange rates matter. They are not pretty when they move; they create real volatility for firms with FX exposure; they impose adjustment costs. But the alternative is that the same shock lands more painfully on quantities — on output, employment, and demand — rather than on prices. The chapter notes that exchange rate pass-through (the rate at which a currency depreciation translates into higher consumer prices) is “typically modest and manageable when inflation is stable.” That last clause is consequential. Pass-through has historically been higher in our region than in advanced economies precisely because inflation expectations were not anchored. As they become anchored, pass-through declines — and exchange rate flexibility becomes a more useful policy tool.

The successful disinflation is the central bank’s victory. Anchored expectations are the next, harder battle. Caribbean firms still operating on 2022 inflation assumptions are fighting a war that has largely been won.

The expectations problem, in firm-level terms

The IDB’s most useful finding for Caribbean entrepreneurs is the one most easily missed. Inflation has largely returned to target across inflation-targeting economies. But the firms, employees, customers, and suppliers who lived through the 2021-23 surge can keep behaving as though it has not.

This shows up in five specific places inside the Caribbean enterprise. Recognising each of them is the first step in correcting them.

Place 1 — Annual price reviews. Most Caribbean firms set their 2026 price increases against an internal expectation of 7-9% inflation. The actual 2026 inflation rate in most regional inflation-targeting economies is now closer to 4-5%, with central bank targets typically in the 3-5% range. The firm that has uplifted prices by 8% in a 4% inflation environment has handed competitors a 4-point price umbrella. Some of that price umbrella is being collected by competitors who recalibrated faster.

Place 2 — Customer contracts with embedded CPI escalators. Many multi-year customer contracts signed in 2022-23 contain CPI-linked escalators with no ceiling — set against panic-era inflation forecasts. These escalators are now driving year-over-year price increases that the actual inflation environment does not justify. Sophisticated customers are noticing. Some are renegotiating. Firms that lead the renegotiation — offering predictable, manageable escalator floors and ceilings — preserve the relationship. Firms that are reactive lose it.

Place 3 — Wage bands and cost-of-living philosophy. Several Caribbean firms institutionalised across-the-board 8-12% increases during 2022-23 to retain talent. Three years later, those automatic increases continue, despite an inflation environment that no longer justifies them. The wage pool is being allocated by formula rather than by skill premium. As Article 3 documented, this is exactly the moment to reallocate from formula-based increases toward strategic-skill premia — particularly AI fluency.

Place 4 — Supplier price acceptance. Most Caribbean firms continue to accept supplier price increases of 5-7% annually with limited pushback, because that is the rate of increase the firm has accepted for three years. In an environment where the underlying inflation rate has moderated, the firm that does not negotiate supplier price increases harder is paying for inflation that no longer exists.

Place 5 — Internal budgeting assumptions. The 2026 budget for most Caribbean mid-market firms was prepared in late 2025 using inflation assumptions inherited from the panic period. Revenue is being budgeted to grow at the inflation rate; costs are being budgeted to grow slightly faster. The result is that the firm is planning around a margin that the actual inflation environment does not require it to surrender. A clean recalibration to current target-consistent inflation expectations frees up real margin.

Each of these five places is correctable inside the firm. Each correction yields immediate, measurable margin. The total cumulative effect, across a typical Caribbean mid-market enterprise, is meaningfully more than the cost of the work to find and correct them.

The two-baseline pricing framework

In our work with Caribbean enterprises across more than fifteen territories, the most useful single tool we have built for the post-disinflation environment is a two-baseline pricing framework. It compares, side by side, the pricing decisions the firm is currently making — calibrated to 2022 inflation panic — against the pricing decisions the firm should be making — calibrated to 2026 reality. The visualisation of the gap drives the corrective action. Here is the framework:

| Pricing element | Built into 2022 panic | Calibrated to 2026 reality | Action this quarter |

| Annual price review | Flat-rate increase of 7-9% to catch up with inflation expectations | Differentiated review by product, customer segment, and competitive position | Move from single-rate to tiered increases. Defend premium segments; protect volume in price-sensitive ones. |

| Customer contract escalators | Embedded CPI-linked escalators set against panic-era inflation forecasts | Escalators recalibrated to current inflation target band; ceilings and floors negotiated | Renegotiate all multi-year contracts with embedded escalators above 6%. The customer will accept it if the firm leads the conversation. |

| Wage band design | Across-the-board 8-12% increases to retain talent during the inflation surge | Differentiated by skill premium, role criticality, and AI-fluency (per Article 3) | Freeze flat increases. Reallocate the same wage pool toward strategic skills. |

| Cost-of-living adjustments | Automatic full CPI pass-through to employees | Partial CPI pass-through with productivity-linked top-ups | Replace automatic CPI with a transparent dual-mechanism: partial CPI plus performance bonus. |

Source: Dawgen Global DSPOM™ Strategic Pricing Operating Model.

Two notes on this framework matter operationally.

First, the move from single-rate to differentiated pricing is the highest-margin decision a Caribbean firm can make this year. Most regional firms operate single annual price reviews that apply uniformly across their customer base. The firms that segment their customer base — by price sensitivity, by competitive position, by strategic value — and apply differentiated reviews systematically gain 100-300 basis points of margin without losing volume. The work is in the segmentation, not in the pricing decision itself.

Second, the renegotiation of customer contracts with embedded escalators is uncomfortable but valuable. Many Caribbean CFOs assume customers will resist any conversation that reduces the contractual escalator. In our experience, the opposite is closer to the truth: large institutional customers are aware that their existing escalators are higher than the underlying inflation environment justifies, and they are looking for an opportunity to renegotiate. The firm that leads the conversation — offering a recalibration with a defined floor, a defined ceiling, and a multi-year extension in exchange — preserves the relationship and tightens it. The firm that waits for the customer to initiate the conversation typically loses both margin and goodwill.

Treasury modernisation: what it actually involves in 2026

The second half of this article addresses the treasury function. For most Caribbean mid-market enterprises, the treasury function has been operationally underdeveloped relative to the demands of the current environment. The 2021-23 inflation surge and the higher-for-longer rate environment have raised the cost of operating with a passive treasury well above the cost of modernising it. Here is what modernisation looks like, function by function:

| Treasury function | What modernisation looks like in 2026 |

| Cash and liquidity management | From passive bank-deposit management to active multi-currency, multi-instrument treasury. Money-market funds, short-duration sovereign paper, and term deposits laddered to match cash-flow visibility. Yield differences between passive and active management have widened materially since 2022. |

| FX exposure management | From reactive (“the rate moved, what now?”) to forward-looking policy. Documented FX policy approved by the board; defined open-position limits; hedging instruments matched to the firm’s actual flows; monthly reporting against policy. |

| Counterparty risk | From single-bank dependency to multi-bank, multi-jurisdiction relationships. The cost of the second banking relationship in calm periods is materially less than the cost of being single-banked when conditions tighten. |

| Hedging and derivatives | From “we don’t use them” to selective use of forwards, swaps, and cross-currency arrangements where the firm has genuine economic exposure. The product is not the point; matching genuine exposure with appropriate instruments is. |

| Reporting cadence | From quarterly bank reconciliation to monthly board-grade treasury report covering positions, yields, FX exposure, counterparty concentration, and exception items. The CFO is accountable; the board reviews; the discipline compounds. |

Source: Dawgen Global Treasury Modernisation framework.

The cumulative cost of running each of these five functions at the modernised standard, for a typical mid-market Caribbean firm, is meaningfully less than the cost of operating with one of them at the passive standard. The single highest-return decision most regional firms can make this year is to commission a treasury maturity assessment, identify the two or three functions operating below the modernised standard, and invest in upgrading them.

Trust and the central bank: why credibility is, indirectly, an asset on every Caribbean firm’s balance sheet

There is one section of the IDB chapter that I want Caribbean entrepreneurs to read carefully. It concerns the relationship between central bank credibility and firm-level economic performance — and it explains, with unusual clarity, why credibility is not just a macroeconomic abstraction.

The IDB notes that credible monetary policy reduces exchange rate pass-through, anchors inflation expectations more durably, and gives the central bank more room to use exchange rate flexibility as an adjustment tool without triggering domestic inflation. Each of these is, indirectly, an asset on every Caribbean firm’s balance sheet operating in a credible-central-bank economy.

Lower exchange-rate pass-through means that when the local currency depreciates against the dollar, the firm’s domestic prices rise less than they would in a less-credible regime. The firm’s margin is less squeezed by FX volatility, and the customer’s purchasing power is less eroded.

Better-anchored inflation expectations mean that the firm can sign multi-year contracts, design wage bands, and budget capital expenditure with greater confidence in the inflation environment they will face. The cost of long-term planning declines as credibility rises.

Greater exchange-rate flexibility means that external shocks are absorbed in part by the currency rather than entirely by domestic demand. The firm’s revenue volatility is lower than it would be in a fixed-rate regime experiencing the same shock.

Each of these is a real, measurable, financial benefit. Caribbean firms operating in inflation-targeting economies — Jamaica explicitly — are operating in environments where these benefits compound through the cycle. Firms operating in fixed-rate or alternative regimes face different tradeoffs and need treasury policies calibrated to those tradeoffs. The asymmetry across the region is meaningful.

How Dawgen Global supports this work

Pricing discipline and treasury modernisation are two of the highest-return advisory engagements a Caribbean firm can commission in the post-disinflation environment. Together, they engage three of our practice areas and one of our most established proprietary frameworks.

- DSPOM™: our Strategic Pricing Operating Model. The two-baseline framework introduced in Section 4 is built directly from the DSPOM™ methodology. The framework covers customer segmentation, differentiated price-review architecture, contract escalator renegotiation, supplier price discipline, and the budgeting recalibration described in Section 3. In our experience, firms that adopt DSPOM™ systematically realise 100-300 basis points of margin improvement within twelve to eighteen months.

- Virtual CFO and Treasury Advisory: for the treasury modernisation work — cash and liquidity management, FX policy design, counterparty risk diversification, hedging architecture, and the board-grade monthly reporting cadence described in Section 5.

- Business Advisory: for the multi-jurisdictional view that Caribbean firms operating across inflation-targeting, fixed-rate, and alternative-regime jurisdictions need to operate at one coordinated standard.

- Tax Advisory: for the tax-aware design of treasury structures, particularly for firms operating across multiple Caribbean territories with different tax regimes.

The integrated nature of this work is important. Pricing discipline without treasury modernisation captures margin but does not protect it. Treasury modernisation without pricing discipline protects margin without growing it. The Caribbean firms that commission both, sequenced over twelve to twenty-four months, compound earnings through this environment in ways the firms that commission neither, or only one, cannot match.

Five questions every Caribbean board should ask the leadership team this quarter

If this article does its job, every Caribbean board will spend a meaningful portion of its next strategic session on five questions:

- What inflation assumptions are baked into our 2026 budget, our pricing reviews, and our wage band design? If they were written when inflation was 8% and inflation is now 4%, the firm is operating on assumptions that no longer apply.

- Have we segmented our customer base and applied differentiated price reviews — or are we still using single-rate annual increases? Most Caribbean firms operate uniform annual reviews. The firms that segment systematically gain 100-300 basis points of margin within a year.

- Have we audited every multi-year customer contract for embedded CPI escalators and renegotiated the ones that exceed the current target band? If the answer is no, the firm is paying — every month — for inflation that no longer exists at the rate the contracts assume.

- Where does our treasury function sit on the modernisation maturity scale? Run the maturity assessment against the five functions in the treasury framework. The two or three functions operating below the modernised standard are the operational priority for the next twelve months.

- Are our treasury policies calibrated to the specific monetary regimes of each jurisdiction we operate in? Treasury policy designed for one regime is not appropriate for another. Firms operating across multiple Caribbean jurisdictions need distinct regime-aware policies.

Next !

Article 8 closes the series. The 12-Point Caribbean Resilience Playbook synthesises everything the previous seven articles have established into a single, board-ready framework — structured across four pillars (capital structure, productivity, talent, and risk readiness), with a defined 90-day execution rhythm and explicit calls to action for the conversations the board should be having with the leadership team, the auditor, the bank, and the tax adviser. It is the article designed to be circulated to the executive team, used as the structure of a 2026-2027 strategic review, and kept on the boardroom wall as the operating reference for the cycle ahead.

Closing

The successful disinflation across regional inflation-targeting economies is the central bank’s victory. Anchored expectations are the next, harder battle — and the one that lands on every leadership team and every firm. The pricing assumptions, contract escalators, wage philosophy, supplier price acceptance, and budgeting frameworks that the Caribbean enterprise locked in during the 2022 panic are still in operation, three years later, in environments where they no longer apply.

The firm that recalibrates these elements this quarter — using a structured framework, with a board-sanctioned mandate, supported by the right advisory partners — gains margin and competitive position from firms that do not. The firm that modernises its treasury function in parallel — moving from passive to active management, from single-bank to multi-bank, from reactive to forward-looking — protects that margin and compounds it through the cycle. Pricing discipline without treasury modernisation captures value; treasury modernisation without pricing discipline protects it. Together, they compound.

The pricing assumptions baked into your 2026 budget were probably written in the inflation panic of 2022. They need a rewrite — this quarter.

— ◆ —

About the author

Dr. Dawkins Brown is the Executive Chairman and Founder of Dawgen Global, an independent, integrated multidisciplinary professional services firm headquartered in Kingston, Jamaica, and operating across more than fifteen Caribbean territories. He writes the Caribbean Boardroom Perspectives newsletter on LinkedIn.

Continue the conversation

Subscribe to Caribbean Boardroom Perspectives on LinkedIn for the final instalment of the series.

Direct enquiries: [email protected] | +1-876-929-3670 | dawgen.global

Source

Ayres, J. and Juvenal, L. (2026). Resilience and Growth Prospects in a Shifting Global Economy: 2026 Latin American and Caribbean Macroeconomic Report. Inter-American Development Bank, Chapter 5: Challenges for Monetary Authorities in Latin America and the Caribbean, pp. 65-83. Drawing on Malmendier and Nagel (2016) and Pedemonte, Toma, and Verdugo (2025) on inflation expectation

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements