Editor’s Note

This is the fourth article in a twelve-part Dawgen Global series introducing DAGAF™ — the Digital Asset Governance & Assurance Framework. Articles 1 through 3 established the inflection-point argument, mapped the foreign regulatory regimes, and set out the architecture of DAGAF™ itself. This article opens the pillar deep-dives, treating Pillar 1 — Governance and Board Oversight — in detail. It is intended for an audience of board chairs, audit committee chairs, senior independent directors, company secretaries, and the senior executives who advise them on governance matters.

The Approval Moment

There is a moment, increasingly common in Caribbean board meetings, when a chair calls for the vote. The recommendation in front of the board is to proceed with a tokenization initiative — a fractionalised real estate offering, a tokenized debt issuance, a digitised member share register, a tokenized fund interest. Management has presented. Counsel has commented. The audit committee has reviewed the paper. The chair calls for any final questions and, hearing none, asks the board for a resolution.

In a well-functioning Caribbean board, the next sixty seconds are the most important part of the meeting. They are the seconds in which directors determine — each individually, and the board collectively — whether the approval being given satisfies the fiduciary obligation that attaches to it. Was the question fully understood? Were the alternatives genuinely considered? Is the institution operationally and culturally equipped to execute? What happens if the regulatory framework moves against the position? What happens if the technology fails? What happens if a related-party question surfaces six months from now that nobody currently in the room raised?

The questions are not new. They are the questions that attach to every board approval of a material strategic decision. What is new is that tokenization concentrates them — in ways most existing governance frameworks were not designed for. The technology layer is genuinely novel. The regulatory framework is genuinely emerging. The audit and assurance practices are genuinely evolving. The custody and operational risk profile is genuinely different from anything most Caribbean boards have approved before. “Informed approval” is harder to achieve than it looks, and when it is achieved, it requires more documentary evidence than ordinary strategic approvals require.

This article addresses what informed approval actually requires, in the specific context of tokenization decisions facing Caribbean boards. It is anchored in DAGAF™ Pillar 1 — Governance and Board Oversight — the first of the seven pillars set out in Article 3. It is structured in four parts. Part I establishes why tokenization is a board-level decision rather than a delegated technology choice. Part II sets out the nine pre-approval requirements that constitute, in our analysis, the documentary record any Caribbean board should expect to receive before approving a tokenization initiative — set out in a structured Board Approval Checklist. Part III addresses the ongoing oversight obligations that attach after approval. Part IV addresses the role of independent advisory engagement at the approval stage as a hallmark of defensible decision-making.

| “In a well-functioning Caribbean board, the next sixty seconds after the chair calls for the vote are the most important part of the meeting.” | ||

| PART I

Why Tokenization Is a Board Decision, Not a Delegated Technology Choice |

||

There is a strain of thinking, occasionally encountered in Caribbean boardrooms, that treats tokenization as a technology decision properly delegated to management or to the IT function. The reasoning is that tokenization is, at one level, a question of which platform to use, which custody provider to engage, and which operational arrangements to put in place — questions on which the board reasonably defers to executive judgment. The reasoning is wrong, and it is wrong for four specific reasons that warrant explicit identification.

Reason 1 — Tokenization changes the legal characterisation of the underlying asset

When a Caribbean entity tokenizes a portion of its balance sheet, it changes the legal form in which the underlying claim is held, transferred, and enforced. A tokenized debt instrument and an underlying loan are not the same thing in law. A fractionalised tokenized real estate interest and a beneficial interest in a special-purpose vehicle are not the same thing in law. A digitised credit union member share and a traditional book-entry member share are not the same thing in co-operative law. The legal characterisation matters because it determines what rights attach to the holder, what enforcement mechanisms apply, what disclosure obligations exist, and what insolvency treatment results. None of these are technology questions. All of them are questions of fiduciary obligation that the board cannot delegate.

Reason 2 — Tokenization creates new categories of risk that affect the enterprise as a whole

Tokenization introduces operational risks that do not exist in conventional asset structures — smart-contract risk, oracle integrity risk, custody key-management risk, blockchain finality risk, third-party concentration risk in the digital asset ecosystem, regulatory characterisation risk, and the cyber-attack surface that attaches to any cryptographically secured asset. These risks affect the enterprise as a whole, not merely the operational function executing the tokenization. They appear in the enterprise risk register; they require board-level monitoring; they have material consequences if mismanaged. The board cannot reasonably defer the management of these risks to the function that proposed the tokenization in the first place.

Reason 3 — Tokenization triggers fiduciary obligations the board cannot satisfy without information

Caribbean directors operate under fiduciary obligations established by the Companies Act in their jurisdiction (the Jamaican Companies Act 2004, the Barbados Companies Act, the Trinidad and Tobago Companies Act 1995, the OECS Companies Act, and equivalents). These obligations include the duty to act in the best interests of the company, the duty of care, the duty of skill and diligence, and the duty to exercise independent judgment. A director who approves a tokenization initiative without engaging substantively with the legal characterisation, the regulatory exposure, the tax position, the custody architecture, the assurance plan, the risk register, and the conflicts profile cannot, by definition, be exercising independent judgment. The information requirement is the fiduciary requirement.

Reason 4 — Tokenization decisions are increasingly visible to regulators, auditors, and investors

Caribbean supervisory authorities — the FSC Jamaica, the Bank of Jamaica, the Central Bank of Trinidad and Tobago, the ECCB, the Cayman Islands Monetary Authority, the Bermuda Monetary Authority, and others — are increasingly attentive to tokenization-related disclosures. External auditors, applying ISA 315 (Identifying and Assessing the Risks of Material Misstatement), are required to understand and document the entity’s process for approving and overseeing material new initiatives. Listed-entity governance disclosures under JSE and ECSE listing rules increasingly require explanation of how the board has discharged its responsibilities on novel strategic matters. The visibility of the board’s decision-making process is rising. The visibility creates documentary expectations that did not previously exist.

| THE BOARD CANNOT DELEGATE WHAT IT CANNOT DEFEND

If a Caribbean director cannot, twelve months after approval, articulate the substantive basis on which the board approved a tokenization initiative — the strategic rationale, the legal characterisation, the regulatory exposure, the custody architecture, the assurance plan, the conflicts management, the risk profile, the disclosure framework, and the ongoing oversight cadence — then the approval was not, in any meaningful sense, an exercise of fiduciary judgment. It was a deferral. Deferrals do not satisfy fiduciary obligation. The DAGAF™ Board Approval Checklist exists to ensure that what reaches the board is sufficient to support a substantive judgment. |

||

| PART II

The DAGAF™ Board Approval Checklist |

||

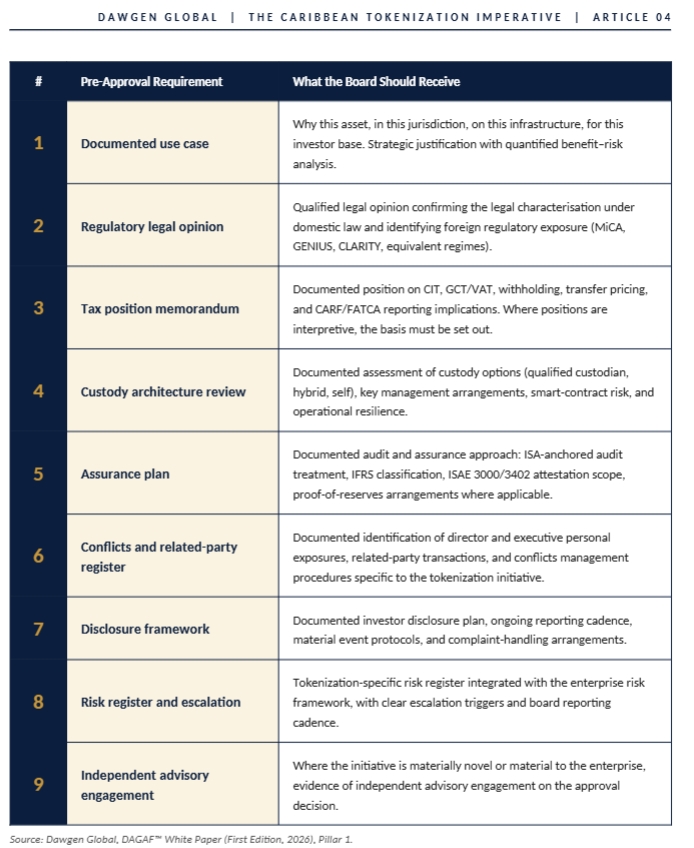

Nine pre-approval requirements, set out below, constitute the documentary record any Caribbean board should expect to receive before approving a tokenization initiative. The list is not aspirational; it is operational. Each requirement reflects a substantive fiduciary obligation; each requirement produces a defensible artefact; each requirement is fully achievable within the existing institutional capacity of a competent Caribbean enterprise. The checklist is the practical expression of DAGAF™ Pillar 1.

Three observations on how the checklist is intended to be used. First, all nine items should be present — not in summary, but in substance. Where a board paper presents an item in single-paragraph form, the underlying analysis should be referenced and available to any director on request. Second, conservative practice is to circulate the full pack, including the underlying analyses, to the audit committee at least one full meeting cycle ahead of the approval meeting, with sufficient time for committee members to engage qualified external advisers if questions arise. Third, where the initiative is material to the enterprise — either by absolute size, by reputational exposure, or by the precedent it sets — the conservative practice is to commission an independent advisory review of the pack before approval. None of this is exotic. All of it is the kind of practice any Caribbean board makes routine for any other major strategic decision. The point is to apply that routine rigour to tokenization specifically.

| “None of this is exotic. All of it is the kind of practice any Caribbean board makes routine for any other major strategic decision. The point is to apply that routine rigour to tokenization specifically.” | ||

| PART III

Ongoing Oversight After Approval |

||

Approval is not the end of the fiduciary obligation; it is the beginning. Once a tokenization initiative is live, the board’s oversight obligations continue — in some respects more intensively than before approval, because the asset is now operational and the regulatory, technological, and market environments around it continue to evolve. Four oversight obligations warrant explicit identification.

Obligation 1 — Regular reporting to the board, with appropriate granularity

The board should receive structured reporting on each material tokenization initiative at no less than quarterly cadence — monthly during the pilot phase. Reporting should cover operational performance against the approved business case, regulatory developments affecting the initiative or its counterparties, assurance findings since the last report, material incidents (technology, regulatory, custody, market), counterparty performance and concentration, and any matters escalated by the audit or risk committee. Reporting should be sufficiently granular to support board-level challenge — not so high-level that it produces only the appearance of oversight.

Obligation 2 — Materiality and escalation thresholds explicitly set and reviewed

The board should set explicit materiality and escalation thresholds for the tokenization initiative — at the level of investment exposure, operational concentration, counterparty change, regulatory development, or assurance finding. Thresholds should be reviewed at least annually. When a threshold is breached, the matter should be escalated through the documented protocol within a defined timeframe. The discipline of explicit thresholds is what distinguishes effective oversight from reactive crisis management.

Obligation 3 — Periodic refresh of director education

The tokenization regulatory environment, the institutional infrastructure, the audit and assurance practices, and the technology underlying tokenized instruments are evolving at pace that exceeds most boards’ organic capacity to keep current. Director education on tokenization should be refreshed at no less than annual cadence — with material updates timed to material developments. The DAGAF™ Board Briefing engagement is one mechanism for delivering this refresh in structured form; in-house training, external CPD programmes, and engagement with industry-association work are others.

Obligation 4 — Periodic external review of governance arrangements

For initiatives of material scale, a periodic external review of the governance arrangements — reviewing the board’s reporting framework, the audit committee’s oversight cadence, the materiality and escalation thresholds, the director-education record, and the documented decision-making history — produces an independent assessment that boards rarely produce of themselves. The review is conventionally performed at no less than three-year cadence, with interim reviews triggered by material change in scope, risk, or institutional environment. External review is a Level 5 (Optimised) maturity practice under the DAGAF™ framework.

| BOARD REPORTING FRAMEWORKS NEED TO EVOLVE

Most Caribbean board reporting frameworks were designed for traditional asset categories and traditional risk profiles. They tend to under-cover the specific risks that attach to tokenized assets — smart-contract integrity, oracle reliability, custody key-management, third-party concentration in the digital asset ecosystem, regulatory characterisation drift, and the operational dependencies on counterparties that the institution does not directly supervise. The conservative practice is to extend the standard reporting framework with a tokenization-specific schedule that addresses these dimensions explicitly. The schedule does not need to be lengthy. It does need to be substantive, current, and structured to support board-level challenge. |

||

| PART IV

Independent Advisory Engagement and Defensible Decision-Making |

||

A pattern is emerging across Caribbean boards that have approved material tokenization initiatives in the past eighteen months. The pattern is the use of independent advisory engagement at the board approval stage — either through a structured external review of the management pack, an opinion-on-process letter from a qualified advisory firm, or a parallel briefing of the audit committee by external counsel and assurance specialists ahead of the board meeting. The pattern is not yet universal. It is, increasingly, the pattern that defensible decision-making follows.

The reasons are structural rather than aspirational. First, tokenization is sufficiently novel that few Caribbean boards have, organically, the depth of expertise across legal characterisation, regulatory exposure, tax position, custody architecture, assurance practice, and operational risk to challenge management presentations effectively at first encounter. Independent advisory engagement supplements board capability where it is genuinely thin. Second, where regulatory or supervisory questions subsequently arise about the basis on which the initiative was approved, the documentary record of independent advisory review materially strengthens the board’s position. Third, where the initiative is observed externally — by investors, by counterparties, by rating agencies — the independent advisory engagement signals institutional seriousness. Fourth, and substantively most important, independent advisory engagement frequently surfaces issues that internal review does not. The friction is the value.

Three forms of independent advisory engagement are commonly used in practice. The first is structured external review of the management approval pack against a published framework — of which DAGAF™ is one option, with comparable frameworks available from international firms. The review produces a written report identifying gaps, areas requiring clarification, and recommendations. The second is the opinion-on-process letter — a more limited engagement in which an independent advisor confirms that the board’s process for approving the initiative met defined standards of fiduciary rigour, without commenting on the substantive merit of the decision itself. The third is parallel external briefing of the audit committee by qualified specialists — usually counsel, an assurance partner, and a tax specialist — before the committee makes its recommendation to the board. Each form has a different cost-and-confidence profile; the choice depends on the materiality of the initiative and the board’s existing internal capability.

Dawgen Global offers each of these advisory forms within DAGAF™. Engagements are scoped to the institution’s circumstances and to the materiality of the initiative under review. The standard entry point is the DAGAF™ Maturity Diagnostic, which establishes baseline governance maturity and identifies the priority gaps a subsequent advisory engagement should address. The DAGAF™ Board Briefing is the focused director-education intensive that frequently precedes a material approval decision. The structured external review and the opinion-on-process letter are typically commissioned separately, on engagement letters scoped to the specific initiative.

The Pillar That Activates the Rest

Pillar 1 of DAGAF™ — Governance and Board Oversight — is the pillar that activates all the others. Without a functioning Pillar 1, there is no defensible basis on which the framework’s other pillars are deployed: the Regulatory and Legal Compliance work (Pillar 2), the Tax Treatment and Reporting work (Pillar 3), the Audit and Assurance work (Pillar 4), the Cyber, Custody and Operational Risk work (Pillar 5), the Investor and Market Conduct work (Pillar 6), and the Strategic Use Case Selection work (Pillar 7) all rest on the foundation of board-level approval and ongoing oversight. The framework is robust because Pillar 1 is robust. The framework is fragile when Pillar 1 is fragile.

The work this article describes is not new work for Caribbean boards. The institutional discipline it requires is the same discipline applied to any other material strategic decision. What is new is that tokenization concentrates that discipline in an area where the regulatory, legal, technological, and operational dimensions are simultaneously evolving. The Caribbean boards that will navigate this landscape effectively are the boards that approach tokenization with the same rigour they apply to any other material strategic decision — and that supplement that rigour, where appropriate, with the independent advisory engagement that defensible decision-making increasingly requires.

| “The framework is robust because Pillar 1 is robust. The framework is fragile when Pillar 1 is fragile.” |

Article 5 — examining Pillar 3, Tokenization and the Caribbean Tax Code — will publish in the next edition. Pillar 3 is the article in this series most consequential to chief financial officers and tax directors wrestling with reporting positions today; Caribbean tax legislation pre-dates tokenization, and the most basic questions — is a token a security or a digital asset for CIT purposes? Is issuance subject to GCT/VAT? Are token transfers withholding events? — have no clean answers under existing law. The full DAGAF™ White Paper, which sets out Pillar 1 in detail and provides the comprehensive 5×7 maturity model in Appendix A, is available now.

ABOUT THE AUTHOR

Dr. Dawkins Brown is the Executive Chairman and Founder of Dawgen Global, an independent integrated multidisciplinary professional services firm headquartered in Kingston, Jamaica, operating across the Caribbean. The firm advises Caribbean enterprises, regulators, and public-sector institutions on audit and assurance, tax, risk management, cybersecurity, IT and digital transformation, corporate recovery, M&A, business advisory and strategy, accounting outsourcing, and human capital. Dr. Brown is the architect of DAGAF™ and is the Founding Editor of Caribbean Boardroom Perspectives.

ABOUT THIS SERIES

The Caribbean Tokenization Imperative is a 12-article series introducing the DAGAF™ framework. Articles 1 to 3 set out the inflection-point argument, mapped the foreign regulatory regimes, and established the architecture of DAGAF™ itself. This article (Article 4) opens the pillar deep-dives, treating Pillar 1 — Governance and Board Oversight — in detail. Article 5 — examining Pillar 3, Tokenization and the Caribbean Tax Code — will publish in the next edition. Subsequent articles will treat each remaining DAGAF™ pillar in turn, examine principal Caribbean use cases, and conclude with a 24-month implementation roadmap. The full DAGAF™ White Paper is available on request.

© 2026 Dawgen Global. All rights reserved. DAGAF™ is a proprietary

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements