Cost-to-Serve and Why Your “Best Customers” May Be Unprofitable

Executive Summary

Many organisations believe they know which customers, products, and channels are profitable. In practice, what leaders often know is gross margin, not true margin. The difference is cost-to-serve—the full set of costs required to sell, deliver, support, and service a customer or channel.

Cost-to-serve is one of the most overlooked drivers of profitability erosion. It hides inside delivery patterns, order frequency, returns, credit behaviour, service exceptions, and internal handling costs. In high-cost environments—where logistics, labour, and financing costs are elevated—cost-to-serve can quietly turn high-revenue customers into loss-makers.

This article explains:

-

What cost-to-serve is (and what it is not)

-

Why “revenue” and even “gross margin” can be dangerously misleading

-

The five common cost-to-serve multipliers that destroy margin

-

How to build a cost-to-serve view using practical data (even if systems are imperfect)

-

How to apply the Dawgen V.A.L.U.E.-Chain Cost Advantage Framework™ to identify, prioritise, and act on cost-to-serve opportunities—without damaging customer relationships

Cost-to-serve is not about cutting service blindly. It is about ensuring service levels are designed intentionally, priced correctly, and delivered efficiently. When done well, cost-to-serve analysis becomes a pathway to sustainable margin improvement, better customer discipline, and a stronger value proposition.

The Profitability Illusion: When “Best Customers” Aren’t

Most businesses can list their “top customers” quickly. Typically, the list is based on revenue volume or brand significance. But high revenue doesn’t equal high profit. In many cases, the most demanding customers generate the highest invisible service costs.

Here’s how the illusion forms:

-

Leadership reviews sales by customer and sees large revenue numbers.

-

Finance reviews gross margin and sees acceptable product margins.

-

The organisation assumes the account is “good business.”

-

Meanwhile, operational teams are running frequent deliveries, managing exceptions, processing returns, and expediting stock—often absorbing cost that is not clearly traced to the customer.

Over time, cost-to-serve becomes a silent margin killer, especially when:

-

logistics costs rise

-

labour productivity is constrained

-

working capital becomes expensive

-

customer expectations increase

-

product/service complexity expands

If you want sustainable cost advantage, you must be able to answer a simple but powerful question:

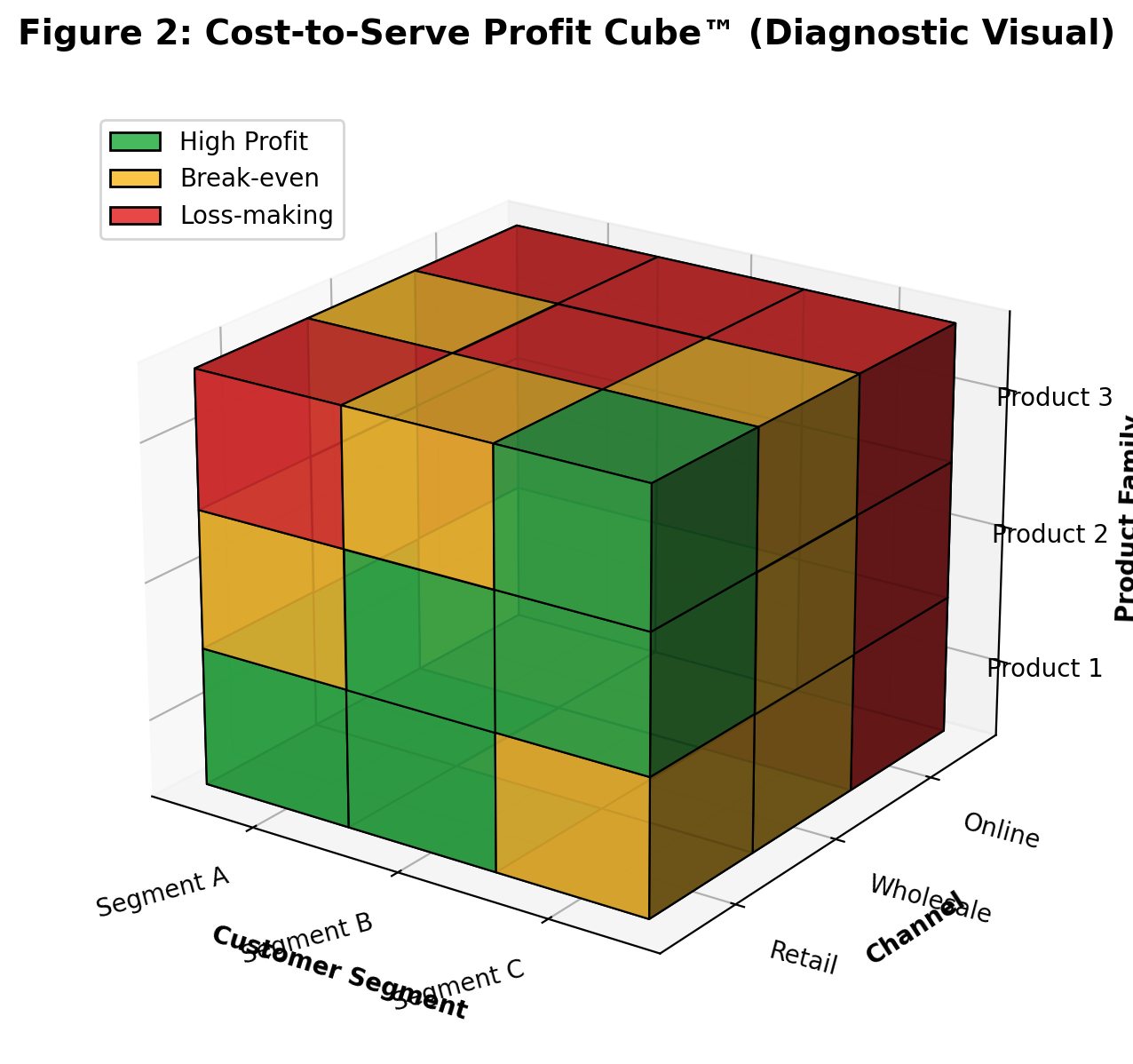

Which customers, products, and channels create value—and which consume it?

What Cost-to-Serve Really Means

Cost-to-serve is the full cost of serving a specific customer, segment, product, or channel—from the moment an order is received to the moment the customer is supported after delivery.

It typically includes costs such as:

-

order processing and customer service time

-

picking, packing, warehousing, and dispatch handling

-

delivery frequency, routing, fuel, and last-mile complexity

-

returns processing, credit notes, and reverse logistics

-

account management time and sales support

-

special packaging, labelling, compliance handling, and documentation

-

claims management and service recovery costs

-

credit risk costs, collections effort, and financing cost of receivables

-

inventory carrying costs driven by service expectations (e.g., “always in stock”)

Cost-to-serve is not “overhead.” It is the operational reality of how you fulfil your promise to customers.

Why Cost-to-Serve Is More Dangerous Today

Even if you have operated successfully for years without formal cost-to-serve analysis, the current environment makes it more critical.

1) Logistics and last-mile costs have increased

Delivery is often one of the most variable cost pools—and customer behaviour can multiply it quickly:

-

small orders

-

frequent deliveries

-

rigid delivery windows

-

special handling needs

-

multiple delivery points per customer

2) Working capital costs are higher

In higher interest rate environments, generous credit terms and slow-paying customers create real financial drag. Two customers with identical revenue can have very different profitability if one pays in 15 days and the other in 90.

3) Service expectations are rising

Customers often want:

-

faster fulfilment

-

more flexibility

-

higher availability

-

exceptions accommodated as “standard”

If service levels are not disciplined, the business becomes a custom service factory—at scale.

4) Complexity is creeping

Every “special” requirement becomes cost:

-

unique packaging

-

customer-specific labels

-

bespoke reports

-

special product variants

-

tailored delivery patterns

-

one-off pricing exceptions

Complexity is one of the biggest drivers of hidden cost-to-serve.

The Five Cost-to-Serve Multipliers That Destroy Margin

Cost-to-serve is driven by a handful of behaviours that multiply cost more than leaders realise.

Multiplier 1: Order frequency and small order sizes

Frequent small orders increase:

-

order processing cost

-

picking/packing cost

-

delivery cost

-

reconciliation and invoicing cost

A high-revenue customer with fragmented ordering patterns can cost more to serve than a mid-sized customer with disciplined ordering.

Multiplier 2: Delivery exceptions and rigid service windows

If you are running:

-

“urgent deliveries”

-

weekend drops

-

fixed time-slot deliveries

-

multiple delivery locations

-

special handling requirements

…then the customer is effectively increasing your logistics cost structure.

Multiplier 3: Returns, claims, and credit notes

Returns create cost in three ways:

-

reverse logistics and handling

-

write-offs, damages, and rework

-

admin processing and customer service time

High returns can erase margin quickly—even when gross margin looks healthy.

Multiplier 4: Customisation and complexity

Customisation multiplies cost across the chain:

-

procurement complexity

-

inventory fragmentation

-

operational changeovers

-

quality variability

-

service and support complexity

Often, the organisation doesn’t price this complexity—so it becomes margin leakage.

Multiplier 5: Credit behaviour and collections effort

Slow payers cost money:

-

financing cost of receivables

-

collections labour

-

higher bad debt risk

-

constrained cash for operations and growth

Cost-to-serve must include the cost of capital reality, not just direct operating costs.

How to Build a Cost-to-Serve View (Even If Your Data Isn’t Perfect)

Many leaders assume cost-to-serve requires sophisticated activity-based costing. In practice, you can start with a practical view using the 80/20 approach.

Step 1: Choose the “unit of analysis”

Start with one:

-

customer (top 30–50 accounts)

-

channel (retail, wholesale, online, institutional)

-

customer segment (by size/behaviour)

-

product family

Step 2: Capture the main cost drivers

You don’t need every cost. Focus on the drivers that explain most variance:

-

number of orders per month

-

average order size

-

number of deliveries per month

-

kilometres per delivery or route complexity proxy

-

returns rate and claims incidents

-

customer service touches (calls, complaints, escalations)

-

credit days outstanding and collections effort

Step 3: Allocate variable costs first

Variable costs are where the signal is strongest:

-

delivery costs per stop / per route

-

warehouse handling per order line

-

returns processing per return event

-

customer service time per interaction

Step 4: Layer working capital cost

Include:

-

DSO impact (days sales outstanding)

-

implied financing cost of receivables (using your cost of capital or funding rate)

Step 5: Produce a “profit bridge” per customer/segment

Start with:

-

revenue

-

gross margin

Then subtract: -

delivery and handling

-

service and support

-

returns and claims

-

credit/working capital cost

Arrive at: -

true margin (net contribution)

Once you see the results, the conversations become very different.

Cost-to-Serve Is Not About Cutting Customers—It’s About Designing Profitability

When organisations discover that certain customers are unprofitable, the worst response is to panic and “cut service.” The right response is to redesign the commercial and service model.

Typical strategies include:

1) Service level redesign (with transparency)

-

standard delivery cycles

-

minimum order quantities

-

consolidated delivery days

-

tiered service offerings (standard vs premium)

2) Pricing and terms discipline

-

price to reflect service complexity

-

surcharge for special deliveries or handling

-

revise discounting and rebates

-

tighten credit terms for slow payers

3) Operational efficiency improvements

-

route optimisation

-

improved picking and warehouse layout

-

automation of order capture and invoicing

-

claims reduction and quality stabilisation

4) Customer behaviour change

-

incentives for larger, less frequent orders

-

digital ordering portals to reduce admin load

-

shared forecasting and planning with key accounts

The goal is not to lose customers—it is to serve them profitably.

How V.A.L.U.E.™ Applies to Cost-to-Serve

Cost-to-serve becomes powerful when embedded into a disciplined cost advantage programme.

V — Validate the Profitability Challenge

-

confirm margin erosion drivers (logistics, labour, discounts, returns, DSO)

-

establish baseline: true contribution margin by segment

A — Analyse the Value Chain and Cost-to-Serve

-

map end-to-end service cost drivers

-

identify hotspots (returns, deliveries, exceptions, slow payment)

L — Locate Levers and Build Opportunity Portfolio

-

levers across commercial, logistics, operations, and controls

-

quantify savings and margin opportunities

U — Uplift & Prioritise

-

prioritise actions that improve true margin quickly

-

define customer negotiation strategy and change plan

E — Execute with Governance & Controls

-

implement service rules (MOQ, delivery cycles, exceptions approvals)

-

track benefits and enforce compliance

™ — Transform for Sustainability

-

embed cost-to-serve as a recurring profitability discipline

-

prevent “exception creep” and discount leakage

Case Snapshot: The “Top Customer” That Was Losing Money

A distributor believed its largest customer was its anchor account. Revenue was high, and product gross margin looked healthy.

But a cost-to-serve analysis showed:

-

frequent small orders (high handling cost)

-

rigid delivery windows (inefficient routes)

-

high returns (claims and credit notes)

-

extended payment terms (higher financing cost)

True contribution was negative.

The solution was not to drop the customer. The organisation:

-

shifted to scheduled delivery days

-

introduced minimum order thresholds

-

tightened returns policy and improved quality checks

-

renegotiated terms to reduce DSO

The customer remained—now profitable—with improved operational stability.

If You Don’t Measure Cost-to-Serve, You Don’t Control Margin

Cost-to-serve is one of the most practical ways to uncover hidden margin leakage. It reveals where complexity, exceptions, and service patterns are silently consuming profitability.

In today’s environment, organisations that can:

-

see true profitability

-

redesign service models intelligently

-

enforce governance and controls

-

reduce cost without eroding value

…will build cost advantage that competitors struggle to match.

Next Step!

Ready to uncover value-protected cost reduction across your value chain—and identify your true profit customers?

Email [email protected] with the subject line “V.A.L.U.E. – Cost-to-Serve Scan” to request an initial discussion and our data intake checklist.

WhatsApp Global: +1 555 795 9071 | Contact form: https://www.dawgen.global/contact-us/

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements