WC-PULSE Framework™ | Working Capital Thought Series

Executive Summary

Accounts payable is often treated as the easiest working-capital lever: “extend terms and keep cash longer.” That framing is dangerous. Payables is a liquidity lever, but also a supply-chain risk lever. Pull it too hard and you may trigger price increases, allocation deprioritisation, quality slippage, stock-outs, supplier failures, or reputational damage that raises your long-term cost base. In the WC-PULSE Framework™, payables is managed as “funding without borrowing” — a disciplined operating system that balances cash preservation with supplier continuity, pricing power, and operational resilience.

This article shows how to run payables like a portfolio, not a blunt instrument: segment suppliers by criticality and fragility; calculate the true cost of terms; deploy three payables engines (terms optimisation, dynamic discounting, supply-chain finance); and align governance to Trigger Zones. In RED, protect liquidity without collapsing supply. In AMBER, release trapped value while improving supplier health. In GREEN, convert liquidity strength into strategic advantage through repricing, allocation priority, and disciplined capital redeployment.

1) Why Payables Is Not “Free Cash”

Payables can create immediate relief because extending payment timing reduces near-term outflows. But in real markets, suppliers respond. They may not respond with an email that says “you are now paying 8% financing cost embedded in price.” They respond quietly through commercial behaviour.

The hidden costs of aggressive payables extension

When buyers extend terms indiscriminately, suppliers typically react via one or more of the following:

-

Price creep: A supplier silently builds financing cost into pricing at renewal, or reduces the rate of discounting.

-

Allocation deprioritisation: In shortages, the supplier allocates scarce supply to customers who pay reliably.

-

Service deterioration: Lead times extend, flexibility drops, rush orders become expensive, returns become harder.

-

Quality drift: Suppliers under cash strain cut corners—less QC, less packaging quality, more defects.

-

Vendor concentration risk: Smaller suppliers fail, forcing you into fewer alternatives (and less leverage).

-

Reputational damage: In vendor markets, word travels. You become known as a slow payer, limiting access to top-tier suppliers.

Key point: Extending DPO can improve cash today while increasing the cost of goods and operational risk tomorrow. WC-PULSE treats that trade-off explicitly.

2) The CFO’s Real Job: Optimise Payables Without Breaking Supply

A strong payables strategy is not “maximize DPO.” It is “maximize resilience-adjusted liquidity.”

That means the CFO must answer three questions:

-

Which suppliers can safely finance us — and at what cost?

-

Which suppliers should we finance — because it strengthens our supply chain?

-

Which suppliers must be protected — because failure is existential?

This is portfolio logic. Just like receivables is managed as a risk-adjusted cash portfolio, payables must be managed as a risk-adjusted funding portfolio.

3) Step 1: Build the Supplier Criticality Map

Before you touch terms, build a supplier segmentation that reflects operational reality, not only spend.

Supplier segmentation (recommended)

You can segment suppliers across four practical categories:

A) Critical suppliers

-

If supply fails, operations stop or customer impact is severe.

-

Substitutes are limited, qualification is slow, switching costs are high.

Examples: key raw materials, essential packaging, sole-source parts, utilities, mission-critical IT services.

B) Strategic suppliers

-

Large spend, meaningful pricing leverage exists.

-

Switching is possible, but requires planning and negotiation.

Examples: major logistics partners, large commodity suppliers, core outsourced functions.

C) Tactical suppliers

-

Many substitutes exist; switching cost is low.

Examples: office supplies, non-critical services, general consumables.

D) Fragile suppliers

-

Small vendors with weak balance sheets or high dependence on your payments.

-

Their failure creates disruption even if they are not “critical” by spend.

How to score suppliers quickly

Use a simple 1–5 scoring on three dimensions:

-

Criticality: how badly does failure hurt operations/service?

-

Substitutability: how quickly can we switch without pain?

-

Fragility: how sensitive is the supplier to late payments?

Output: A heat map that tells you:

-

where to extend terms,

-

where to protect payments,

-

where to deploy supply-chain finance,

-

where early-pay discounts create leverage.

4) Step 2: The “True Cost of Terms” — A CFO Calculation

Payables decisions must be treated like financing decisions.

The concept

If you extend a supplier from net-30 to net-60, you are effectively asking the supplier to finance you for 30 days. The supplier will price that financing in some way (explicitly or implicitly).

So the CFO should ask:

-

What is the supplier’s implied cost of financing?

-

Is it more expensive than our own funding?

-

If yes, can we achieve the same liquidity benefit more efficiently through SCF or facility use?

A practical CFO test

If a supplier increases prices by 2% in response to longer terms, and your annual spend is significant, that “2%” might be far more expensive than using a bank facility for the same period.

This is why WC-PULSE separates cash visibility from cash economics.

5) Step 3: The Three Payables Engines

WC-PULSE treats payables improvement as three engines. Most organisations only use Engine 1 and do it bluntly.

Engine 1: Terms optimisation (commercial engine)

This is the traditional lever:

-

renegotiate terms by segment,

-

align contracts and POs,

-

enforce approvals for exceptions,

-

stop leakage.

Risk: if done indiscriminately, it becomes supplier destabilisation.

Engine 2: Dynamic discounting (treasury engine)

This flips the logic: pay early when it’s economically beneficial.

-

You use surplus liquidity to earn an implied return (discount) that exceeds your cost of capital.

-

You can target only strategic/fragile suppliers.

-

You can vary behaviour by Trigger Zone.

Dynamic discounting is a way to turn working capital into an investment decision, not just a payment decision.

Engine 3: Supply-Chain Finance (SCF) (ecosystem engine)

SCF allows:

-

suppliers to get paid early by a financer (bank/platform),

-

while you maintain your payment terms (or extend them responsibly).

This supports supplier liquidity without forcing you to accelerate outflows. It can stabilize supply chains during volatility.

Key discipline: SCF must be implemented transparently and ethically, with governance and supplier choice.

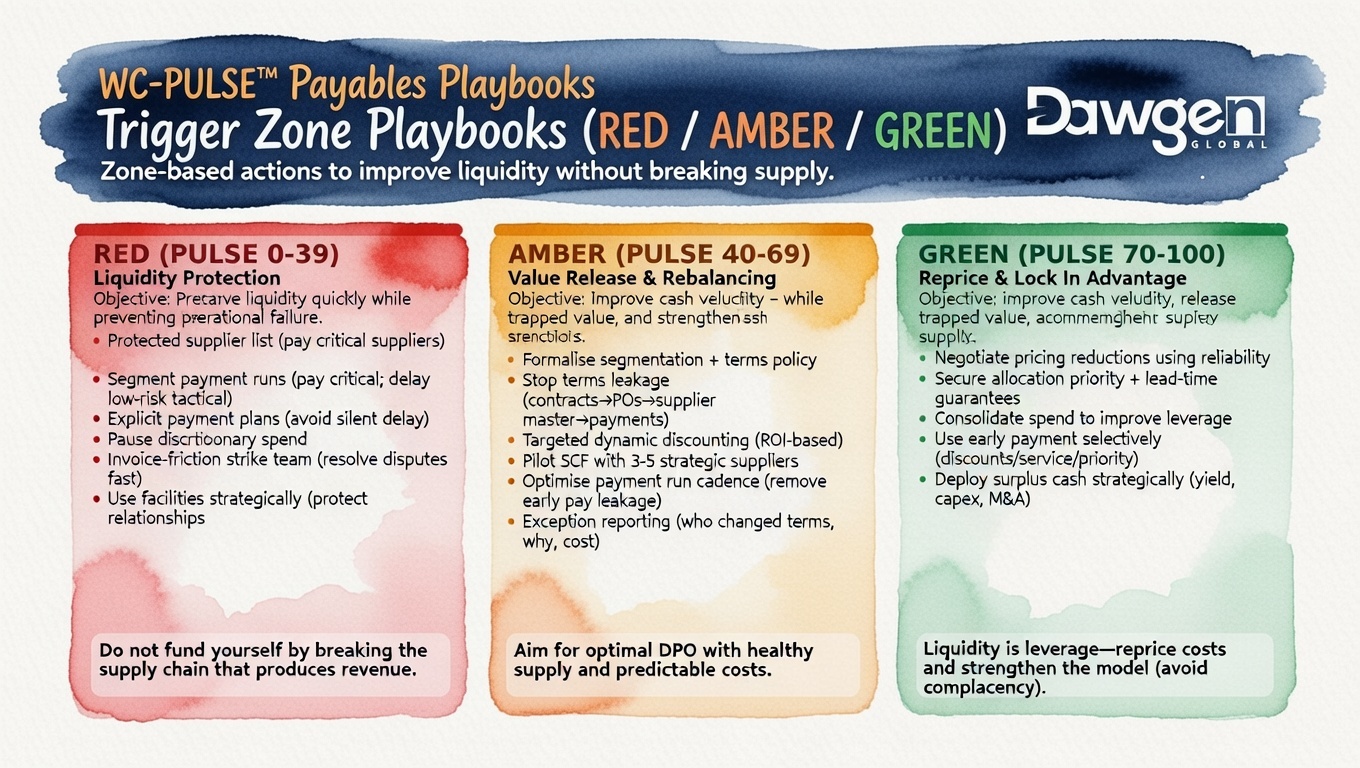

6) Trigger Zone Payables Playbooks (RED / AMBER / GREEN)

RED Zone (PULSE 0–39): Liquidity Protection Without Supply Collapse

Objective: Preserve liquidity quickly while preventing operational failure.

In RED, the CFO is in “Cash War Room” mode, but payables decisions must be surgical.

What to do immediately (first 7–14 days)

-

Create a “protected supplier list.”

Critical suppliers must be protected to keep the business alive. -

Segment payment runs.

-

Run payments for critical suppliers on time (or per negotiated plan).

-

Delay tactical suppliers only where substitutes exist and risk is low.

-

-

Negotiate explicit payment plans.

Silent delay creates distrust. Structured plans preserve relationships. -

Pause discretionary spend.

Cut noise from the payables queue so finance focuses on survival payments. -

Fix invoice friction.

In RED, unresolved invoice disputes are self-inflicted cash chaos. Assign a strike team. -

Use facilities strategically.

If the company has access to overdraft/credit lines, use them to avoid damaging supplier relationships that will cost more later.

RED rule: Do not fund yourself by breaking the supply chain that produces revenue.

AMBER Zone (PULSE 40–69): Value Release and Rebalancing

Objective: Improve cash velocity, release trapped value, and strengthen supplier economics.

This is the zone where most CFOs can create the biggest sustainable gains.

AMBER actions (30–90 days)

-

Formalise supplier segmentation and terms policy.

Critical ≠ Tactical. Fragile ≠ Strategic. Apply different rules. -

Stop terms leakage.

Align contracts → POs → supplier master → payment system. -

Launch dynamic discounting (targeted).

Pay early only where ROI is attractive and supplier benefit is real. -

Pilot SCF with 3–5 strategic suppliers.

Especially where supplier liquidity is constraining supply reliability. -

Optimise payment run cadence.

Many organisations accidentally pay early due to process timing. Fixing this creates “free cash” without harming suppliers. -

Build exception reporting.

Show who changed terms, why, and what it cost.

AMBER rule: The goal is not maximum DPO — it is optimal DPO with healthy supply and predictable costs.

GREEN Zone (PULSE 70–100): Reprice and Lock in Advantage

Objective: Use liquidity strength as commercial leverage.

GREEN is where the CFO can convert liquidity into structural advantage.

GREEN actions (30–180 days)

-

Negotiate pricing reductions using reliability.

Supplier economics improve when the buyer is predictable. -

Secure allocation priority and lead-time guarantees.

In volatile markets, reliability buys preferential treatment. -

Consolidate spend where it improves leverage.

Reduce fragmentation and unlock volume pricing. -

Use early payment selectively.

Not to be generous — to buy discounts, service, or priority. -

Deploy surplus cash strategically.

Over-buffering suppresses returns. Treasury can invest surplus in yield-bearing instruments within policy, or fund growth capex/M&A.

GREEN rule: Liquidity is leverage — use it to reprice costs and strengthen the operating model, not to drift into complacency.

7) Governance: Stop Payables Leakage (Where Most Programs Fail)

Most payables strategies fail because “terms on paper” are not “terms in cash.”

Common leakage points

-

Contracts contain terms that never reach the PO.

-

Supplier master data is inaccurate or editable without approval.

-

AP overrides payment dates “to be helpful.”

-

Urgent business requests bypass procurement discipline.

-

Disputes are unresolved, causing unpredictable payment timing.

Controls that actually work

-

Supplier master governance

-

Locked fields for terms

-

Approval workflows for changes

-

Audit trail

-

-

Exception reporting

-

early payments

-

term overrides

-

payments outside the run cycle

-

supplier bank changes

-

-

Payment policy by Trigger Zone

-

RED: protection list + tight approvals

-

AMBER: optimisation rules + ROI checks

-

GREEN: strategic levers + renegotiation agenda

-

-

Procurement + Finance alignment

Procurement negotiates; Finance enforces; both must share governance.

8) A Composite Case Study: The DPO Extension That Backfired

A company under liquidity stress extended terms from 30 to 60 days across all suppliers. Within two months:

-

Small suppliers struggled and missed deliveries.

-

A key supplier raised prices 3% at renewal and reduced flexibility.

-

The company experienced stock-outs and paid for expedited freight.

-

Margin compression and operational disruption outweighed the cash benefit.

When the firm adopted WC-PULSE segmentation:

-

critical suppliers were protected,

-

tactical suppliers were extended responsibly,

-

SCF was used for strategic suppliers,

-

dynamic discounting stabilised fragile suppliers.

Result: cash improved sustainably, and service levels recovered.

9) Implementation Roadmap (45–60 Days)

If you want to operationalise this without a multi-year project:

Week 1–2: Diagnostic + segmentation

-

build supplier criticality map

-

identify top 20 suppliers by spend + criticality

-

measure current DPO, early payment leakage, exceptions

Week 3–4: Policy + governance

-

set terms policy by segment

-

lock supplier master governance

-

implement exception reporting

Week 5–6: Payables engines

-

dynamic discounting rules (ROI thresholds, approval triggers)

-

SCF pilot design (select vendors + platform/bank engagement)

-

payment run optimisation and workflow fixes

Ongoing: KPIs that matter

-

DPO (but not alone)

-

supplier OTIF (on-time-in-full)

-

price drift vs baseline

-

stock-out incidents linked to supplier issues

-

exceptions rate (terms/payment overrides)

-

supplier concentration and fragility indicators

Payables is not just a cash lever. It’s a strategic instrument that can either strengthen your operating model or quietly weaken it. WC-PULSE turns payables into funding without borrowing by applying segmentation, economics, and zone-based governance. The best CFOs don’t simply extend terms — they design a payables system that preserves liquidity while improving supplier stability and pricing power.

Next Step!

If you want to implement the WC-PULSE payables operating model — segmentation, dynamic discounting, supply-chain finance design, and zone-based governance — Dawgen Global can help.

🔗 https://www.dawgen.global/contact-us/

📧 [email protected]

📞 💬 WhatsApp Global: +1 555 795 9071

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements