C | Context

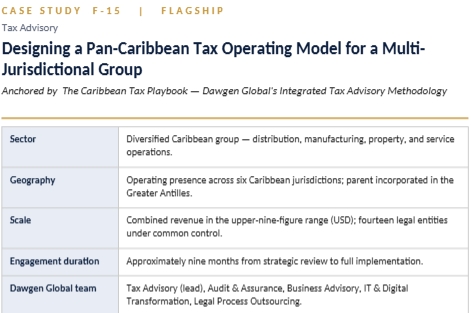

A diversified Caribbean group, built over three decades through a combination of organic expansion and strategic acquisition, had accumulated a multi-jurisdictional footprint whose tax management had not kept pace with its commercial development. The group’s fourteen legal entities, spread across six Caribbean jurisdictions, were each managed by local finance teams operating under local tax advisors, with a small central tax resource whose role had effectively become compliance coordination rather than tax strategy. Transfer pricing between entities had been handled informally, with arm’s-length documentation absent in several relationships. Tax incentive certifications had been obtained where available but not actively maintained against their conditions. Indirect tax positions across the six jurisdictions had never been reviewed comprehensively. Effective tax rate varied materially between entities without clear strategic rationale.

Two external developments brought matters to a decision point. First, the global shift toward BEPS Pillar Two minimum taxation — while the group itself was below the Pillar Two thresholds, the jurisdictional reforms implementing Pillar Two were restructuring Caribbean tax regimes in ways that would affect the group’s position through 2026 and beyond. Second, a potential future strategic transaction — not imminent but credibly within a three-year horizon — required that the group present itself, when that transaction arrived, with a defensible, documented, and optimised tax position. The cost of retrofitting a tax operating model under transaction pressure would be substantially higher than building it now.

Dawgen Global was retained to design and operationalise a pan-Caribbean tax operating model for the group: a single, coherent, strategically-governed approach to the group’s tax position across all six jurisdictions, operationalised through a redefined central tax function, supported by consistent methodology, documentation, and technology.

A | Approach — The Caribbean Tax Playbook

Dawgen Global deployed its Caribbean Tax Playbook body of work — a comprehensive methodology covering the full Caribbean tax spectrum, including corporate income tax, indirect taxes, transfer pricing, tax incentive regimes, employment taxes, international tax considerations, and the emerging BEPS-related reforms across Caribbean jurisdictions. The Playbook is not a single framework but an integrated methodology whose elements are selectively applied to address the specific tax challenges of a Caribbean enterprise. In this engagement, the Playbook was deployed across six domains.

| 1. Tax Strategy & Governance

Tax strategy statement, governance architecture, tax risk appetite, and board reporting cadence. |

2. Structure & Positioning

Group structure review, holding company positioning, and tax-efficient flow architecture. |

3. Transfer Pricing Discipline

Intercompany pricing policies, documentation, functional analysis, and BEPS-aligned methodology. |

| 4. Incentive Preservation

Tax incentive certificate review, condition compliance, and strategic incentive utilisation. |

5. Indirect Tax Optimisation

Multi-jurisdictional VAT/GCT review, input recovery, and supply-chain tax efficiency. |

6. Technology & Evidence

Tax management platform, compliance calendar, evidence register, and authority-ready documentation. |

S | Solution

Tax Strategy & Governance — elevating tax to a board-governed activity

The engagement opened by elevating tax from a compliance-managed function to a board-governed activity. A formal Tax Strategy Statement was produced, approved by the group’s board, articulating the group’s approach to tax: compliant, transparent, appropriately efficient, and explicitly non-aggressive. A Tax Risk Appetite Statement defined the positions the group was prepared and not prepared to take. A board-level tax reporting cadence was established, with quarterly updates to the audit committee and an annual strategic review at the full board. A redefined central tax function was established with a named Head of Tax reporting to the Chief Financial Officer, with tactical support co-sourced from Dawgen Global for specialist matters.

Structure & Positioning — the group structure review

The Structure & Positioning domain reviewed the group’s entity structure for strategic fit. Fourteen legal entities across six jurisdictions had accumulated for historical reasons that in several cases no longer reflected current commercial realities. Without making radical structural change — the group’s operational and regulatory relationships in each jurisdiction had real value that should not be disturbed — targeted simplifications were identified and executed: consolidation of dormant entities, alignment of intermediate holding structures, and positioning of certain intellectual property and shared-services activities in the jurisdiction where they created real economic substance and attracted appropriate fiscal treatment. Each structural change was designed with commercial substance first and tax efficiency second.

Holding company positioning was reviewed against the group’s actual and prospective commercial activities. The intermediate holding structures were aligned to provide efficient flow of intra-group dividends, appropriate access to jurisdictional tax treaty networks where relevant, and clean optionality for a future strategic transaction. The positioning was designed to withstand scrutiny from any tax authority on the grounds that each element of the structure served a genuine commercial purpose, with tax-efficiency as a consequential rather than principal design driver.

Transfer Pricing Discipline — the BEPS-aligned methodology

Transfer Pricing Discipline was the single most operationally consequential domain. The group had, over its three-decade history, developed an extensive network of intercompany transactions — shared services, intellectual property licensing, goods flows, financing — that had been priced informally and documented only partially. BEPS-aligned transfer pricing methodology was applied across every material intercompany relationship, with formal functional analyses, benchmarking studies, and contemporaneous documentation prepared to a standard that would satisfy both current Caribbean transfer pricing requirements and the evolving international standards.

For each intercompany relationship, the transfer pricing documentation addressed the five dimensions required under BEPS-aligned standards: the functional profile of each party, the appropriate arm’s-length method, benchmarking evidence, the actual pricing applied, and the periodic review cadence. Where existing pricing was out of range, adjustments were designed and implemented prospectively. Where pricing was defensible but poorly documented, the documentation gap was remediated. Where pricing reflected legacy arrangements that no longer made commercial sense, the arrangements themselves were renegotiated intra-group. The result was a transfer pricing posture that was both defensible and, in several areas, materially more efficient than the pre-engagement position.

Incentive Preservation — active management of tax incentives

Tax incentive regimes vary across the Caribbean, and each of the six jurisdictions in which the group operated offered some combination of manufacturing incentives, export incentives, capital allowances, tourism incentives, and special economic zone regimes. The group held certifications under several of these regimes, but the certifications had been treated as one-time events rather than as commitments requiring active maintenance. The Incentive Preservation domain catalogued every incentive certification held, confirmed current compliance with the conditions of each, identified those certifications where continued compliance required specific action, and — for strategic certifications — produced a compliance-management plan that ensured incentive value would not be inadvertently lost. For several incentives that the group had been eligible for but had not obtained, a structured application path was developed.

Indirect Tax Optimisation

The Indirect Tax Optimisation domain reviewed the group’s VAT and General Consumption Tax positions across all six jurisdictions. Input tax recovery was reviewed systematically, identifying recovery positions that had been inadvertently foregone. Intra-group supply chains were reviewed for indirect-tax efficiency, with several goods flows restructured to eliminate unnecessary cascading of irrecoverable tax. Registration and compliance calendars were harmonised across the jurisdictions, eliminating the compliance gaps that had arisen from six separate local finance teams managing six separate compliance regimes without central visibility. The cumulative effect was a material reduction in indirect tax leakage across the group.

Technology & Evidence

The final domain addressed the infrastructure that would sustain the new tax operating model. A tax management platform was deployed — integrated with the group’s ERP environment — that provided single-source visibility of the group’s tax position across jurisdictions. A centralised compliance calendar replaced six jurisdiction-specific calendars, with automated alerts for key deadlines and structured evidence capture for each filing. An evidence register was established, capturing the contemporaneous support for each material tax position, such that any tax authority inquiry could be responded to with evidence rather than reconstruction. The technology platform was deliberately configured for the incoming Head of Tax rather than for Dawgen Global, ensuring that the capability was internalised in the group rather than retained by the advisor.

E | Effect

Within the nine-month engagement, the group transitioned from a tax management posture that was competent at jurisdictional level but fragmented at group level, to a tax operating model that was governed centrally, coherent across jurisdictions, defensible on documentation, and optimised within the explicit boundaries of the Tax Strategy Statement approved at board level. Transfer pricing documentation was brought to a standard that would satisfy both current Caribbean requirements and the evolving international standards. Tax incentive certifications were being actively managed rather than passively held. The central tax function, redefined during the engagement, began operating with the authority and visibility that its importance to the group warranted. The group’s subsequent interactions with tax authorities in two of the six jurisdictions benefited directly from the rigour of the new documentation regime, resolving long-standing positions that had not previously been capable of clean resolution. The group is now positioned to engage, if and when a strategic transaction arises, from a documented, defensible, and optimised tax position rather than under the time pressure of transaction diligence.

Insight Lens — From the Engagement Partner

| The tax lesson for Caribbean groups

Tax operating models are built during periods of relative calm and retrofitted under transaction pressure at multiple times the cost. The Caribbean multi-jurisdictional group that has treated tax as a sequence of local compliance activities, rather than as a group-level strategic capability, will discover — when its first material strategic transaction arrives, or when its first BEPS-related regulatory inquiry lands, or when its first serious transfer pricing audit begins — that the cost of retrofit is material. The Caribbean Tax Playbook exists because the tax challenges of Caribbean enterprises require Caribbean-specific methodology: fourteen entities across six jurisdictions, each with its own tax regime, each with its own incentives, each with its own authority culture. There is no template to download. The Playbook is the methodology. |

Cross-disciplinary Footprint

- Audit & Assurance — independent verification of the tax positions underlying the new operating model.

- Business Advisory — tax governance architecture and board-level reporting design.

- IT & Digital Transformation — tax management platform deployment and ERP integration.

- Legal Process Outsourcing — intercompany agreements, transfer pricing documentation, and authority engagement support.

- M&A Advisory (MERIDIAN™) — positioning of structure for future strategic optionality.

Take the next step with Dawgen Global

| THE SIGNAL

If you are a Chief Financial Officer, Head of Tax, Chief Executive, or board audit committee chair of a Caribbean group operating across multiple jurisdictions — and your group’s tax management is currently fragmented across local finance teams without a governed central tax operating model — the cost of inaction compounds with every compliance cycle, every intercompany transaction, and every reform of the evolving Caribbean tax landscape. The right time to build the tax operating model is before it is required under pressure. THE OFFER Dawgen Global offers a confidential Caribbean Tax Playbook Diagnostic: a structured six-week engagement that assesses your group’s current tax operating model against all six domains of the Playbook, identifies the gaps and exposures across your jurisdictional footprint, and produces a prioritised roadmap to a governed pan-Caribbean tax operating model. The diagnostic is delivered under confidentiality and without obligation to proceed. THE CHANNEL Email [email protected]

|

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements