| Key Insight: A holding company is not vulnerable merely because it is lean. It becomes vulnerable when it lacks real substance, decision-making autonomy, commercial purpose, and evidence that it controls the income or assets it legally holds. |

Executive Summary

Holding companies remain valuable tools in international tax and corporate structuring. They can support investment management, regional expansion, capital raising, asset protection, group governance, mergers and acquisitions, and succession planning. However, in today’s tax environment, a holding company must be more than a legal entity on a corporate chart. It must be able to demonstrate commercial purpose, decision-making autonomy, economic substance, and control over the income or assets it holds.

The recent Milan First Instance Tax Court ruling involving Luxembourg holding companies offers an important reminder. The Italian Revenue Agency challenged a Luxembourg holding chain, arguing that the entities were interposed companies and that the relevant gain should be taxed in Italy. The court rejected that position, placing weight on the fact that the Luxembourg companies had real offices, staff, governance processes, and independent decision-making. The ruling therefore highlights a broader international tax principle: a holding company is not automatically a conduit simply because it is lean, but it becomes vulnerable where it lacks substance, autonomy, and commercial reality.

For multinational groups, private equity investors, family offices, and Caribbean businesses using cross-border structures, the practical question is no longer whether a holding company exists legally. The more important question is whether it can be defended as the beneficial owner, decision-maker, and genuine participant in the structure.

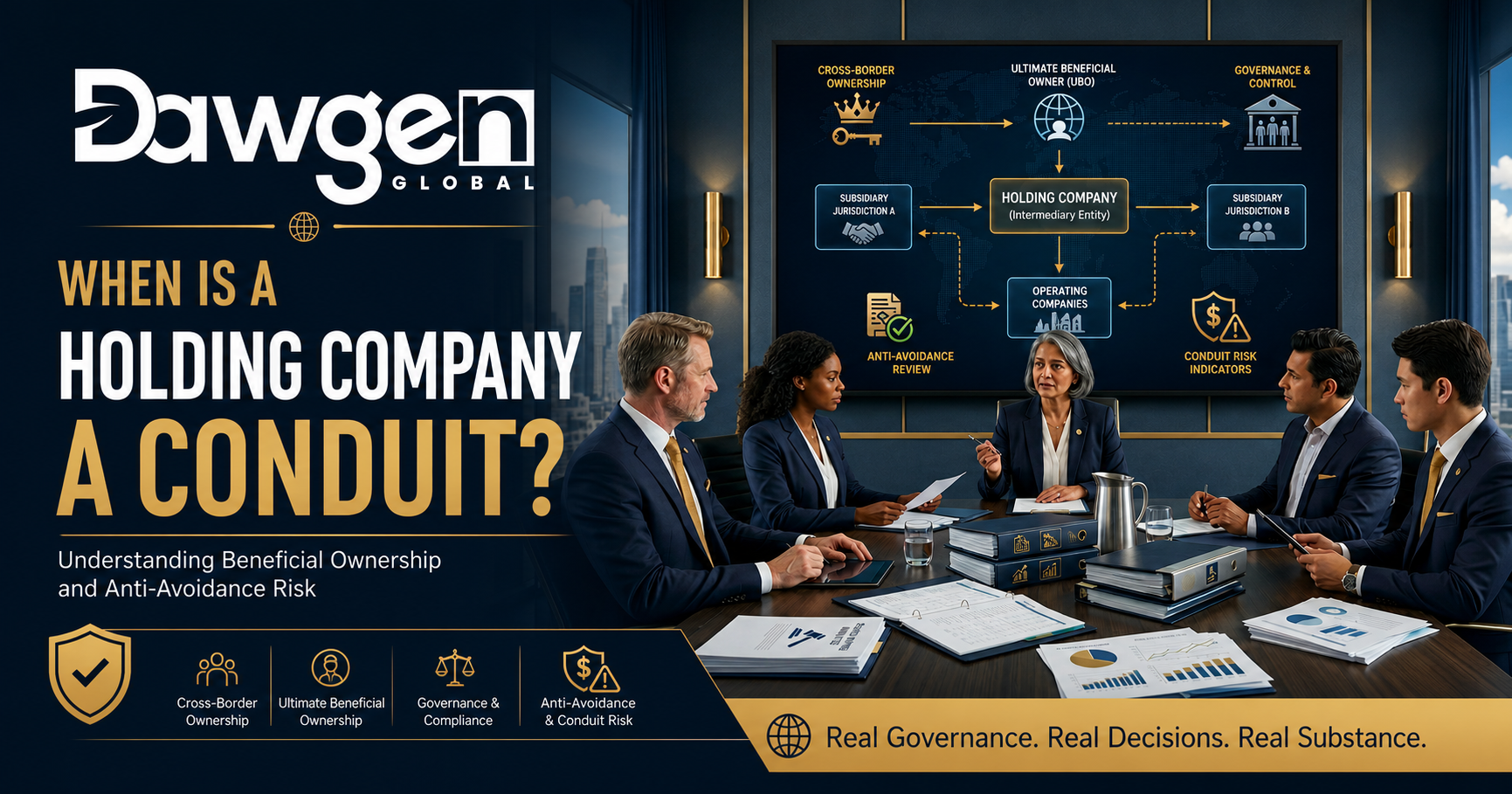

1. Why the Conduit Question Matters

A conduit company is generally understood as an entity that is inserted into a corporate or payment chain but performs little or no meaningful commercial function. It may receive dividends, interest, royalties, capital gains, management fees, or other income, but it does not truly control or enjoy that income. Instead, it merely passes the benefit to another person or entity.

Tax authorities are increasingly alert to conduit arrangements because they may be used to obtain treaty benefits, reduce withholding taxes, avoid capital gains tax, access domestic exemptions, or shift income to low-tax jurisdictions. As a result, holding companies are now examined through the lens of economic reality.

The key questions are: Does the company have a genuine commercial role? Does it control the income it receives? Does it have the right to decide whether to retain, reinvest, distribute, or deploy funds? Does it bear risk? Does it have people, directors, premises, and records appropriate to its function? Is it acting independently or merely following instructions from another party?

Where the answers are weak, the entity may be challenged as a conduit. Where the answers are strong and supported by evidence, the structure becomes significantly more defensible.

2. Holding Company Versus Conduit Company

It is important to distinguish between a genuine holding company and a conduit company.

A genuine holding company may own shares in subsidiaries, supervise investments, approve financing arrangements, manage dividend policy, participate in acquisition and disposal decisions, and provide a governance platform for the group. It may be lean, but it should still have a real role.

A conduit company, by contrast, usually has limited or no independent function. It may have legal ownership of shares or income rights, but it does not exercise meaningful control. It may lack substantive board deliberation, may have no practical discretion over income, and may exist mainly to achieve a tax outcome.

The difference is not always obvious from the legal documents. It must be assessed by examining the full factual pattern, including governance, cash flows, contractual obligations, director conduct, commercial rationale, tax filings, and internal correspondence.

In other words, the corporate chart tells only part of the story. The evidence must show that the company has a mind, function, and purpose of its own.

3. The Beneficial Ownership Dimension

Beneficial ownership is a central issue in many international tax disputes. In treaty-based tax planning, an entity claiming reduced withholding tax on dividends, interest, or royalties may need to demonstrate that it is the beneficial owner of the income.

Beneficial ownership is not limited to legal title. A company may be the legal recipient of income but still fail to qualify as the beneficial owner if it is under a legal, contractual, or practical obligation to pass the income to someone else.

The beneficial ownership analysis commonly looks at whether the recipient has the right to use and enjoy the income; has discretion over whether to retain or distribute the income; bears economic risk; has substantive decision-making authority; is not merely acting as an agent, nominee, or intermediary; and is not contractually or practically bound to pass income onward.

For holding companies, this analysis can be particularly sensitive. If dividends received by the holding company are automatically paid to another entity, if interest income is matched by back-to-back payments, or if sale proceeds are immediately transferred under pre-existing arrangements, tax authorities may argue that the holding company is not the true beneficial owner.

The risk is not created by onward payments alone. A holding company may legitimately distribute profits. The risk arises where the evidence suggests that the company had no real discretion and functioned as a pass-through vehicle.

4. Anti-Avoidance and Substance: The Wider Risk Environment

Modern tax authorities have several tools for challenging holding structures. These may include domestic anti-avoidance rules, beneficial ownership doctrines, principal purpose tests, substance requirements, controlled foreign company rules, transfer pricing rules, and specific anti-conduit provisions.

The common theme is that tax authorities are looking beyond legal form to ask whether the structure has genuine commercial substance.

A structure may be vulnerable where the holding company was inserted shortly before a transaction; there is no commercial rationale for the jurisdiction or entity; directors do not meaningfully participate in decisions; board minutes are generic or formulaic; the company has no employees, premises, or operational support; income is automatically transferred onward; or the documentary evidence was created after the fact.

The risk is magnified in high-value transactions such as exits, reorganisations, dividend repatriations, refinancing, intellectual property migration, or the sale of an operating business.

5. Lessons from the Milan Tax Court Ruling

The Milan First Instance Tax Court ruling is useful because it illustrates that courts may uphold holding structures where the facts support genuine substance. The court reportedly recognised that the Luxembourg companies were not fictitious or merely interposed, placing emphasis on their offices, staff, governance, and independent decision-making.

This is an important point for taxpayers and advisors. The ruling does not suggest that every holding company will be respected. Nor does it suggest that minimal substance is always enough. Rather, it confirms that the analysis is fact-specific.

A holding company does not need to be large to be genuine. But it must be real.

For investment holding entities, substance should be proportionate to function. A company that holds investments may not require hundreds of employees. However, it should have directors who deliberate, records that evidence decision-making, systems for managing its affairs, and control over relevant assets and income.

The ruling therefore supports a practical standard: lean is acceptable; artificial is not.

6. Warning Signs That a Holding Company May Be Treated as a Conduit

Businesses should examine their structures for warning signs. The following indicators do not automatically mean that a holding company is a conduit, but they should trigger careful review.

No real board deliberation. If board minutes merely approve decisions already made elsewhere, the company may appear to be rubber-stamping. Tax authorities may ask whether the directors had sufficient information, authority, and independence to make real decisions.

Automatic flow of funds. Where dividends, interest, royalties, or sale proceeds are received and immediately passed to another party under pre-existing arrangements, the company may be viewed as lacking beneficial ownership.

Lack of commercial rationale. If the only clear reason for the company’s existence is tax efficiency, the structure is more vulnerable. There should be a credible business purpose, such as investor pooling, acquisition financing, regional governance, legal protection, access to capital markets, or operational coordination.

Insufficient local presence. A holding company does not always need extensive physical infrastructure, but it should have arrangements proportionate to its role. This may include premises, local service providers, accounting records, administrative support, and access to relevant expertise.

Directors without real authority. Directors should not be passive signatories. They should understand the business, participate in decisions, review information, challenge recommendations, and exercise independent judgement.

Poor documentation. Even where a company has substance, weak documentation can undermine its position. In tax disputes, what cannot be evidenced may be treated as if it did not happen.

7. Building a Defensible Holding Company

A defensible holding company should be built around substance, governance, and evidence. The following practical measures can materially reduce conduit risk.

Establish a clear commercial purpose. The company’s purpose should be documented from the outset. This may include investment management, acquisition structuring, financing coordination, group governance, asset protection, succession planning, or preparation for future capital raising.

Maintain proper board governance. Board meetings should be held regularly and should involve real discussion. Directors should receive board packs, review transaction documents, consider risks, and record their reasoning.

Ensure decision-making autonomy. The company should be able to make decisions about its assets and income. Even where group strategy is relevant, the holding company’s board should exercise its own judgement.

Avoid mechanical pass-through arrangements. Distributions should be considered and approved based on the company’s financial position, investment strategy, legal obligations, and commercial priorities. Automatic onward payment arrangements increase risk.

Align resources with functions. The company’s resources should match its role. A passive investment holding company may need less infrastructure than an operating company, but it still requires enough support to perform its functions properly.

Keep a contemporaneous evidence file. The company should maintain records showing governance, substance, tax compliance, financial control, and commercial rationale. Evidence prepared contemporaneously is generally more persuasive than documents created after a challenge begins.

8. Practical Implications for Caribbean Businesses and Investors

Caribbean business groups and investors often use international holding structures for legitimate reasons. These may include attracting international investors, acquiring foreign assets, holding regional subsidiaries, preparing for a sale, accessing financing, or managing legal and commercial risks.

However, as cross-border scrutiny increases, these structures must be reviewed through a modern tax-risk lens.

For Caribbean groups, the conduit risk question may arise where a regional group holds overseas subsidiaries through a foreign company; a family office uses a holding company for international investments; a private equity investor exits an operating company through a holding chain; a company receives dividends from foreign subsidiaries; or a group uses financing or intellectual property structures involving multiple jurisdictions.

In each case, the group should ask: can we prove that the holding company is real, commercially justified, and capable of making decisions?

If the answer is uncertain, the structure should be reviewed before a transaction or tax audit forces the issue.

9. A Dawgen Global Framework for Conduit Risk Review

Dawgen Global’s Tax practice can assist clients by applying a structured review framework to identify and mitigate conduit risk.

A practical review may include corporate structure mapping; identification of entities claiming treaty benefits or exemptions; review of dividend, interest, royalty, and capital-gains flows; assessment of beneficial ownership risk; evaluation of board composition and decision-making processes; review of minutes, resolutions, board packs, and transaction files; assessment of premises, employees, service providers, and operational support; review of intercompany agreements and financing arrangements; analysis of whether income is retained, reinvested, or automatically passed onward; evaluation of commercial rationale and non-tax business purpose; preparation of a tax controversy defence file; and recommendations to strengthen substance and documentation.

This type of review is particularly valuable before a sale, refinancing, group restructuring, dividend repatriation, or tax authority enquiry.

10. Conclusion: The Question Is Not Whether the Company Exists, But Whether It Acts

A holding company becomes vulnerable when it exists legally but does not act commercially. It may have incorporation documents, bank accounts, and board minutes, but if it lacks real discretion, substance, and commercial purpose, tax authorities may treat it as a conduit.

The Milan ruling confirms the other side of the principle: where a holding company has real substance, governance, and decision-making autonomy, it may be respected even if it is lean. The issue is not the size of the entity, but the reality of its function.

For businesses with cross-border structures, the message is clear. Build structures that can be defended. Maintain evidence before it is needed. Ensure that holding companies are not merely inserted into ownership chains, but are capable of demonstrating real governance, real decisions, and real substance.

At Dawgen Global, we help clients assess, strengthen, and document their international structures so they are not only tax-efficient, but also resilient under scrutiny.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements