| Executive Summary

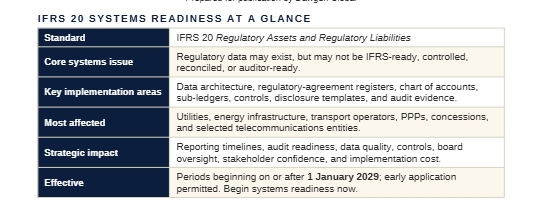

IFRS 20, Regulatory Assets and Regulatory Liabilities, is often discussed as an accounting standard. But for affected companies, one of the greatest implementation challenges may not be technical accounting alone — it may be systems, data, controls, documentation, and audit readiness. For rate-regulated entities, IFRS 20 requires the identification, measurement, presentation, and disclosure of regulatory assets, regulatory liabilities, regulatory income, and regulatory expense arising from differences in timing between when regulated goods or services are supplied and when compensation is charged to, or deducted from, customers through regulated rates. Companies will need reliable data on regulatory agreements, tariff mechanisms, cost-recovery arrangements, future rate adjustments, regulatory interest, recovery and fulfilment schedules, classification, maturity analysis, and balance movements. Many companies already collect regulatory information, but it may not be organised, controlled, reconciled, or documented in a way that supports IFRS financial reporting and external audit. That creates a hidden implementation challenge, requiring close collaboration between finance, regulatory affairs, legal, operations, treasury, tax, internal audit, IT, and external auditors — and changes to chart of accounts design, regulatory reporting systems, consolidation, management reporting, forecasting models, controls, and disclosure preparation. For utilities, energy infrastructure, transport operators, ports, airports, PPPs, concession entities, and selected telecommunications businesses, early systems readiness will be essential. Companies that wait until the year of adoption may face data gaps, audit-evidence challenges, weak controls, delayed reporting, and communication risk. Dawgen Global can assist with systems readiness reviews, data gap assessments, control design, audit preparedness, implementation roadmaps, accounting policy development, disclosure templates, and board-level training. |

1 IFRS 20 Is Not Only an Accounting Project

Many companies approach a new accounting standard by asking, “What is the accounting treatment?” That is important, but for IFRS 20 it is not enough. The standard requires companies to identify and measure regulatory assets and liabilities arising from regulatory agreements, present regulatory income and expense, and provide detailed disclosures about balances, movements, recovery and fulfilment patterns, and significant judgements.

These requirements depend on data. A technically correct accounting conclusion cannot be implemented unless the company has the data, systems, processes, and controls to produce reliable numbers. Yet many regulated entities do not currently capture information the way IFRS 20 requires it to be reported. Some maintain detailed regulatory records for tariff submissions or regulator filings — but those records may not be reconciled to the general ledger, may not be prepared under IFRS concepts, may not be subject to financial reporting controls, and may not be supported by documentation sufficient for external audit.

IFRS 20 implementation should be treated as a multidisciplinary transformation project, not merely an accounting memo.

2 Why Systems Readiness Matters

IFRS 20 creates new reporting requirements that may require companies to track regulatory balances over time. For each regulatory asset or liability, management may need to understand:

| • Why the balance arose

• Which regulatory agreement created the right or obligation • When the timing difference originated • How the balance will be recovered or fulfilled • Whether recovery or fulfilment is within 12 months or longer |

• Whether regulatory interest applies

• What assumptions affect future cash flows • What uncertainties affect measurement • How the balance moved during the period • How the balance should be disclosed |

If this information is not captured systematically, finance teams may be forced to rely on spreadsheets, manual reconciliations, or ad hoc extracts from regulatory departments. That may work during an early diagnostic, but it is unlikely to be sustainable for recurring IFRS reporting. Systems readiness matters because IFRS 20 will become part of the annual reporting cycle — embedded into month-end, quarter-end, year-end, budgeting, forecasting, audit, management reporting, and board reporting.

3 The Data Gap: Regulatory Information Is Not Always IFRS-Ready

Many regulated entities already prepare information for regulators — tariff applications, cost-recovery schedules, fuel-adjustment calculations, infrastructure investment plans, regulatory capital base calculations, performance-incentive reports, and over- or under-recovery schedules. But regulatory data is not automatically IFRS-ready: it may be designed to satisfy the regulator’s methodology, not IFRS measurement, presentation, or disclosure requirements, and the timing, classification, level of aggregation, control environment, and documentation standards may differ.

COMMON DATA GAPS

| • Regulatory balances not reconciled to the general ledger

• Tariff models not linked to accounting records • Incomplete history of timing differences • Lack of clear origination and reversal tracking • Limited documentation of enforceable rights and obligations • Weak linkage between regulatory decisions and accounting entries |

• Inconsistent classification of cost-recovery items

• Absence of a current and non-current split • Incomplete maturity analysis • No formal process for regulatory interest calculations • Insufficient evidence to support management judgements • Reliance on individuals rather than controlled systems |

These gaps can create significant implementation risk.

4 The IFRS 20 Data Architecture Companies May Need

A well-designed IFRS 20 data architecture should let the company identify, measure, track, reconcile, and disclose regulatory assets and liabilities.

| Data category | Examples of information to capture |

| Regulatory source | Regulatory agreement reference, regulator or responsible authority, regulated activity or business unit, type of regulatory mechanism. |

| Timing difference | Origin of the timing difference, related IFRS line item, origination date, expected recovery or fulfilment period. |

| Classification & measurement | Regulatory asset or liability classification, current / non-current split, expected future tariff effect, regulatory interest rate. |

| Movement analysis | Opening balance, originations, recoveries or fulfilments, regulatory interest, changes in estimates, closing balance. |

| Disclosure & governance | Maturity-analysis category, disclosure category, judgement references, and approval references. |

This may require changes to existing systems or the development of controlled sub-ledgers, regulatory reporting modules, consolidation schedules, or IFRS 20 reporting templates. The goal is not complexity for its own sake, but to ensure IFRS 20 numbers are traceable, auditable, repeatable, and explainable.

5 Spreadsheet Risk: Useful Tool or Control Weakness?

Spreadsheets are often useful during early IFRS 20 analysis — they let management model scenarios, assess impact, and test accounting approaches. But heavy reliance on spreadsheets for recurring financial reporting can create risk.

| Spreadsheet risk | Why it matters under IFRS 20 |

| Formula or link errors | Can distort regulatory asset, liability, income, expense, maturity, and interest calculations. |

| Version-control problems | Different teams may rely on different versions of the same regulatory model. |

| Manual input errors | High-volume or judgemental data may be entered inconsistently. |

| Weak audit trail | Management may struggle to prove who changed what, when, and why. |

| Limited scalability | Manual files may not support recurring group reporting across multiple regulated activities. |

Where spreadsheets are used, companies should introduce controls over ownership, access, versioning, formula review, reconciliations, change tracking, and approval. For material regulatory balances, management should consider whether spreadsheet-based reporting is sustainable or whether a more formal system solution is required.

6 Chart of Accounts and General Ledger Considerations

IFRS 20 may require changes to the chart of accounts and general ledger structure. Companies may need separate accounts for:

| • Regulatory assets and regulatory liabilities

• Current and non-current regulatory assets • Current and non-current regulatory liabilities • Regulatory income and regulatory expense |

• Regulatory interest income and expense

• Recovery of regulatory assets and fulfilment of regulatory liabilities • Remeasurement adjustments and transition adjustments |

A well-structured chart of accounts can make reporting more efficient and reduce manual reclassification, while supporting management reporting, audit evidence, consolidation, and disclosure preparation. Companies with multiple regulated activities, subsidiaries, jurisdictions, or tariff mechanisms may need more granular coding to analyse balances by business unit, regulatory agreement, activity type, or recovery mechanism.

7 Controls Over Identifying Regulatory Agreements

The first systems challenge is completeness. A company cannot account for regulatory assets and liabilities if it has not identified all relevant regulatory agreements — not only formal rate orders, but licences, concession agreements, tariff frameworks, regulator decisions, legislation, PPP contracts, and other enforceable arrangements. Possible controls include:

| • Maintain a central register of regulatory agreements

• Perform periodic legal and regulatory review of contracts and licences • Create a formal notification process when tariff arrangements change • Require finance review of regulator decisions and rate orders |

• Use cross-functional review involving legal, regulatory affairs, and finance

• Obtain annual business-unit certification on regulatory arrangements • Report IFRS 20 scope changes to the audit committee |

Completeness is particularly important for groups operating in multiple jurisdictions or with several regulated business lines.

8 Controls Over Recognition and Measurement

IFRS 20 requires management to determine whether regulatory assets and liabilities exist and how they should be measured. These controls should be documented, tested, and subject to appropriate review — especially where significant judgement is required. Controls should address:

| • Assessment of enforceable rights and obligations

• Identification of timing differences • Approval of recognition conclusions • Estimation of future cash flows • Selection or confirmation of regulatory interest rates |

• Assessment of demand risk and credit risk

• Review of regulatory capital base and depreciation implications • Classification as current or non-current • Review of changes in estimates and approval of accounting entries |

Management should consider whether internal audit should include IFRS 20 readiness and controls in its audit plan before adoption.

9 Controls Over Regulatory Interest

Many regulatory agreements provide for interest or financing adjustments on deferred regulatory balances, and IFRS 20 may require regulatory interest income or expense to be included in measurement and presentation. This creates additional data and control requirements:

| • Identify whether regulatory interest applies

• Determine the applicable regulatory interest rate • Calculate interest on opening and closing balances • Account for changes in rates |

• Reconcile interest to regulatory filings

• Separate regulatory interest income and expense from other finance items where required • Review whether interest is recovered or fulfilled through future rates |

If regulatory interest is material, errors can affect revenue, EBITDA, regulatory balances, disclosures, and covenant analysis.

10 Controls Over Current and Non-Current Classification

IFRS 20 requires regulatory assets and liabilities to be classified as current or non-current, unless the entity presents its statement of financial position in order of liquidity. This classification depends on expected recovery or fulfilment timing, and controls should address:

| • Recovery schedules and fulfilment schedules

• Tariff-adjustment timelines and regulatory approval dates • Expected customer billing periods |

• Changes in expected timing

• Consistency between maturity analysis and balance-sheet classification • Management review of classification assumptions |

This is especially important for companies with large long-term infrastructure cost-recovery balances, storm-recovery balances, capital-expenditure recovery mechanisms, or multi-year tariff true-ups.

11 Disclosure Systems: The Often-Underestimated Challenge

IFRS 20 disclosures may be extensive — reconciliations, maturity analyses, explanations of significant movements, information about unrecognised regulatory balances, and details of judgements and uncertainties. Companies should ask whether they can:

| • Produce opening-to-closing reconciliations by category

• Explain originations, recoveries, fulfilments, regulatory interest, and other changes • Produce maturity analysis by expected recovery or fulfilment period • Identify unrecognised regulatory assets and liabilities |

• Explain the relationship between regulatory balances and related items

• Support disclosures with auditable evidence • Produce disclosures consistently across subsidiaries and business units |

Disclosure templates should be developed early and tested before the first reporting period.

12 Audit Readiness: Evidence Before Year-End

External auditors will need evidence to support IFRS 20 balances and disclosures. If companies wait until year-end to assemble documentation, they may face audit delays or difficult late-stage adjustments.

| Auditor-ready documentation | Purpose |

| IFRS 20 scoping assessment and regulatory-agreement register | Supports completeness of the population of regulated arrangements. |

| Legal analysis of enforceability | Supports recognition of enforceable rights and obligations. |

| Accounting policy paper | Documents management’s interpretation and application of IFRS 20. |

| Recognition and measurement support files | Supports balances, assumptions, cash flows, interest, and estimates. |

| Reconciliations to regulatory filings and the general ledger | Supports accuracy, completeness, and audit trail. |

| Disclosure support files and approval records | Supports transparent and controlled financial statement reporting. |

Early auditor engagement is essential. Management should discuss key judgements, data sources, and proposed controls with auditors before the first IFRS 20 reporting deadline.

13 Internal Collaboration: Breaking Down Silos

IFRS 20 cannot be implemented by finance alone. Finance understands IFRS reporting; regulatory affairs understands tariff mechanisms; legal understands enforceability; operations understands the source of costs; treasury understands covenant implications; IT understands systems constraints; internal audit understands control design; investor relations understands communication needs. A strong IFRS 20 project team should include:

| • Finance and financial reporting

• Regulatory affairs • Legal • Operations • Treasury • Tax |

• IT

• Internal audit • Investor relations • External reporting • Business unit leaders |

The team should have clear governance, milestones, issue escalation, documentation standards, and audit-committee oversight.

14 Transition Data: The Clock Is Already Running

IFRS 20 is effective for annual reporting periods beginning on or after 1 January 2029, with earlier application permitted — but transition planning should begin well before then. Companies may need comparative information and opening balances, and even where transition reliefs are available, management may need historical data to determine the impact. Transition data challenges may include:

| • Incomplete historical regulatory balance tracking

• Missing evidence for past regulator decisions • Inconsistent historical tariff calculations • Changes in regulatory frameworks over time • System migrations |

• Business combinations and restructurings

• Changes in chart of accounts • Archived regulatory filings • Lack of documentation for old estimates |

The longer a company waits, the harder it may be to reconstruct reliable transition information.

15 Technology Solutions: What Companies Should Consider

Not every company will need a major technology implementation, but every affected company should assess whether its current systems can handle IFRS 20. Options to consider include:

| • Enhanced general ledger coding

• Regulatory balance sub-ledgers • Controlled IFRS 20 reporting templates • Consolidation system modifications • Data warehouse reporting layers |

• Workflow tools for judgement approvals

• Document management systems • Automated reconciliations • Dashboard reporting for regulatory balances • Integration between regulatory and finance systems |

Technology should be proportionate to the complexity and materiality of the company’s regulatory balances. A small entity with limited balances may need controlled templates; a large utility with multiple tariff mechanisms may need more robust systems integration.

16 Practical IFRS 20 Systems Readiness Checklist

Use the following questions to gauge readiness across four dimensions.

| Area | Readiness questions |

| Data & systems | Have all data sources been identified? Are regulatory balances tracked by origination, recovery, and fulfilment? Can data be reconciled to the general ledger and regulatory filings? Can systems produce current / non-current splits and maturity analysis? |

| Controls | Are controls designed over scoping, recognition, measurement, estimates, and judgements? Are changes in regulatory agreements reviewed for IFRS 20 impact? Are spreadsheets controlled where used? |

| Audit readiness | Has management prepared technical accounting papers? Are enforceability conclusions supported by legal analysis? Has the auditor reviewed the proposed approach? Are disclosure templates ready for dry-run testing? |

| Governance | Has a cross-functional IFRS 20 project team been established? Has the audit committee been briefed? Are implementation milestones documented? Is internal audit involved in control readiness? |

17 Common Mistakes to Avoid

| • Treating IFRS 20 as a finance-only project

• Assuming regulatory data is automatically IFRS-ready • Waiting until 2029 to begin transition work • Underestimating disclosure data requirements • Relying on uncontrolled spreadsheets • Failing to reconcile regulatory data to the general ledger |

• Ignoring current and non-current classification

• Not documenting enforceability and judgement conclusions • Engaging auditors too late • Failing to brief the board and audit committee early • Forgetting the impact on covenants, KPIs, and forecasts • Not aligning external communication with reporting changes |

Avoiding these mistakes can significantly reduce implementation risk.

18 How Dawgen Global Can Help

Dawgen Global assists regulated entities with the full systems, data, controls, and audit-readiness aspects of IFRS 20 implementation. Our services include:

| • IFRS 20 systems readiness assessments

• Regulatory data gap analysis • Regulatory-agreement register design • Chart of accounts and reporting structure review • IFRS 20 sub-ledger and reporting template design • Internal control design and documentation • Spreadsheet control reviews |

• Regulatory balance reconciliation support

• Disclosure template development • Audit preparedness documentation • Accounting policy papers • Board and audit-committee training • Project management support • Stakeholder communication planning |

We help clients build a reliable reporting foundation so IFRS 20 implementation is not a last-minute year-end exercise, but a controlled, auditable, and value-adding process.

19 Conclusion: Data Readiness Is IFRS 20 Readiness

IFRS 20 will require regulated entities to produce financial reporting information that is transparent, comparable, controlled, and auditable — which cannot be achieved through technical accounting analysis alone. Companies will need reliable systems, complete data, well-designed controls, clear documentation, and early auditor engagement, plus collaboration between finance, regulatory affairs, legal, operations, IT, treasury, internal audit, and the board.

The hidden systems challenge of IFRS 20 is that many companies may already have some of the required information — but not in a form that is ready for IFRS reporting. Those that act early will be best positioned to manage transition risk, avoid audit surprises, communicate clearly with stakeholders, and use IFRS 20 as an opportunity to strengthen financial reporting discipline.

Dawgen Global is ready to support regulated entities across the Caribbean and beyond with IFRS 20 systems readiness, data gap assessments, controls design, audit preparedness, and implementation support.

| Is your data and systems environment ready for IFRS 20?

Dawgen Global can help you assess your systems, close data gaps, design controls, prepare auditor-ready documentation, brief your board, and implement IFRS 20 with confidence. Let’s have a conversation. Website: www.dawgen.global/contact-us Email: [email protected]

|

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements