Ask most Caribbean internal audit functions for their annual audit plan and a document will appear within the hour — a schedule of engagements, a staffing grid, perhaps a risk-ranking matrix behind it. Ask the same functions for their internal audit strategy and the response is usually a pause. That pause is the subject of this article, because under the Global Internal Audit Standards the strategy is no longer an optional nicety for large, sophisticated functions. It is a binding requirement for every function, of every size — and it is the single document most Caribbean internal audit functions do not yet have.

The requirement deserves to be understood as more than paperwork. The mandated strategy is the instrument through which the Standards convert internal audit from a watchdog — reactive, engagement-by-engagement, reporting what went wrong — into a strategist: a function with a deliberate, multi-year view of where assurance effort will create the most value, what capabilities it must build to deliver that assurance, and how it will prove its own effectiveness to the board. This fourth article in The Internal Audit Imperative™ explains what the strategy must contain, how to build one, and the failure modes that turn strategies into shelfware.

A Plan Is Not a Strategy

The distinction matters because many functions believe they already comply. An audit plan answers the question: what engagements will we perform in the next twelve months? A strategy answers a different set of questions entirely: Why does this function exist in this organization? What do our stakeholders — board, regulators, management, external auditor — need from us over the next three to five years? What must we be capable of by then that we are not capable of today? And how will we know we are succeeding? A plan without a strategy is a list of activities. The Standards now require the logic behind the list.

The requirement sits within the management domain of the Standards: the chief audit executive must develop and implement a strategy that supports the organization’s strategic objectives, aligns with stakeholder expectations, and includes a vision, strategic objectives, and supporting initiatives for the internal audit function itself — reviewed with the board and updated as circumstances change. Note the last clause: a strategy drafted once and filed does not conform. It is a living document with a refresh cadence.

What the Strategy Must Contain

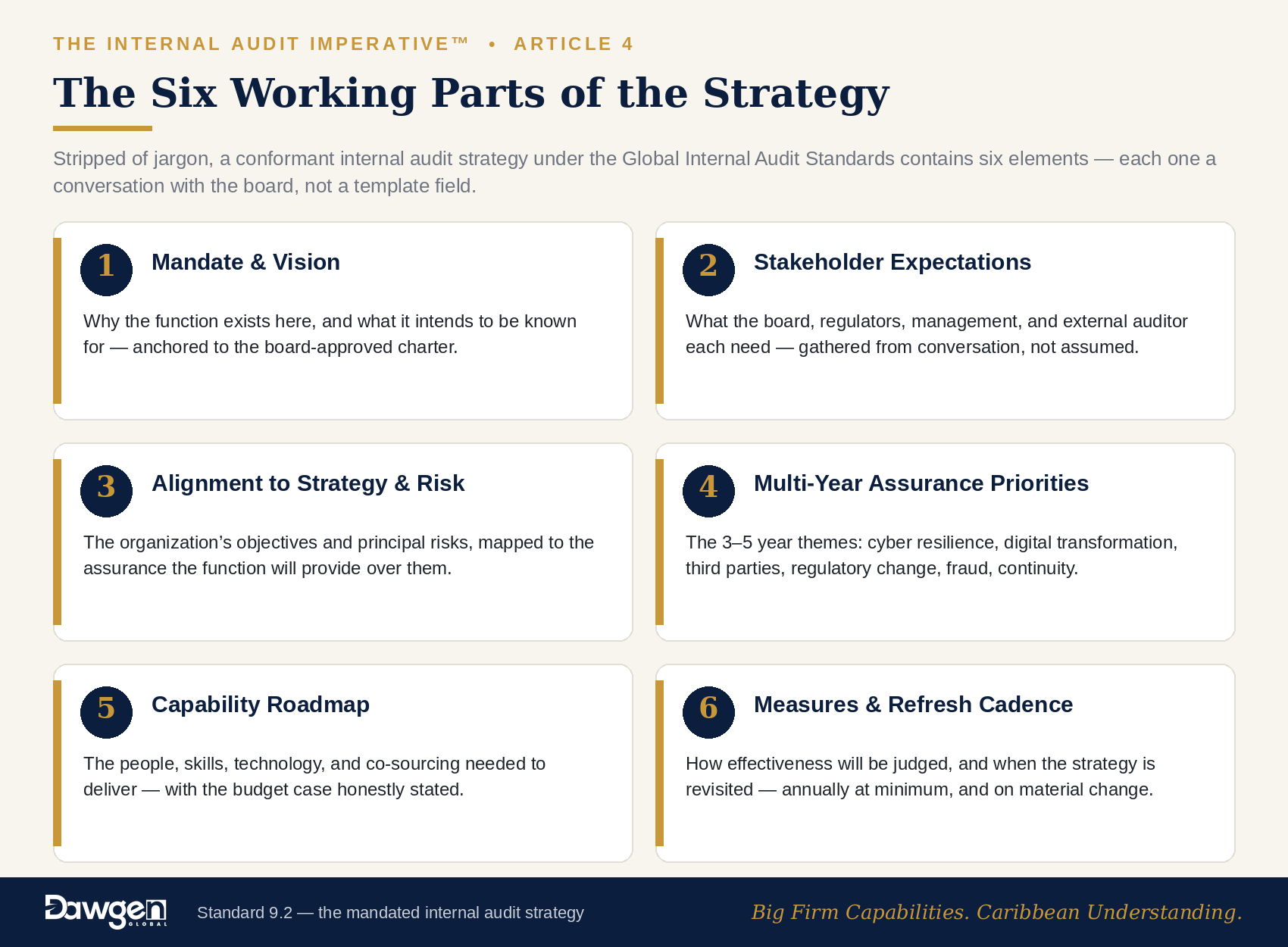

Stripped of jargon, a conformant internal audit strategy has six working parts:

- Mandate and vision. A concise statement of why the function exists in this organization and what it intends to be known for — anchored to the charter the board approved.

- Stakeholder expectations. What the board, audit committee, regulators, executive management, and external auditor each need from the function — gathered from conversation, not assumed.

- Alignment to enterprise strategy and risk. The organization’s own strategic objectives and principal risks, mapped to the assurance the function will provide over them.

- Multi-year assurance priorities. The three-to-five-year view of where audit effort will concentrate — not engagement titles, but themes: cyber resilience, digital transformation, third-party dependence, regulatory change, fraud, climate and continuity.

- Capability roadmap. The people, skills, technology, and co-sourcing arrangements required to deliver those priorities — with the budget conversation that follows honestly stated.

- Performance measures and refresh cadence. How the function will measure its own effectiveness, and when the strategy will be revisited — at minimum annually, and upon any material change in the organization’s direction or risk profile.

Calibrating the Strategy for the Caribbean

A strategy copied from a global template will fail the alignment test, because the risk landscape it assumes is not the one Caribbean organizations occupy. Regional strategies in 2026 should be weighing, at minimum: cybersecurity and digital transformation risk, as core banking replacements, payment modernization, and cloud migration sweep the region’s financial sector; regulatory transition, as Jamaica’s Twin Peaks reform re-draws supervisory expectations for governance functions; third-party and concentration risk, given the small number of critical service providers many island economies depend upon; climate and business continuity exposure, which for Caribbean enterprises is an annual operational reality rather than a distant scenario; and fraud and revenue integrity, the perennial themes behind the region’s recent restatements and write-offs. A strategy that names these honestly — and sequences assurance over them — will read as credible to any board, regulator, or external assessor.

Building It: A Five-Step Method

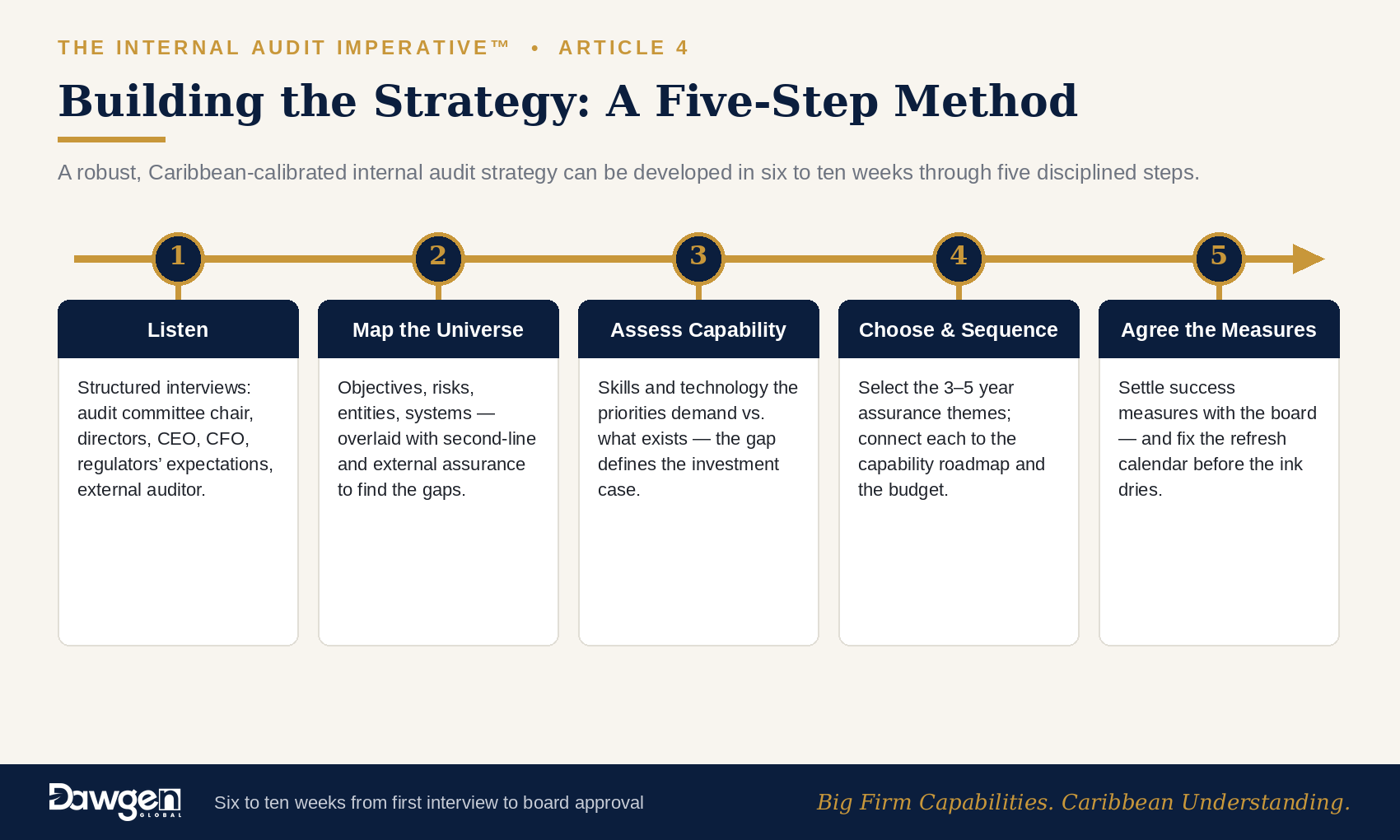

In practice, a robust strategy can be developed in six to ten weeks through five disciplined steps:

- Step 1 — Listen. Structured interviews with the audit committee chair, directors, CEO, CFO, key regulators’ published expectations, and the external auditor. The strategy’s credibility is built here.

- Step 2 — Map the assurance universe. Inventory the organization’s objectives, risks, entities, systems, and processes; overlay existing assurance from the second line and external audit; identify the gaps only internal audit can close.

- Step 3 — Assess capability honestly. Compare the skills and technology the priorities demand against what the function has. The gap defines the co-sourcing and investment case.

- Step 4 — Choose and sequence. Select the three-to-five-year assurance themes, sequence them, and connect each to the capability roadmap and budget.

- Step 5 — Agree the measures. Settle with the board how success will be judged — coverage of priority risks, findings resolved, stakeholder feedback, quality assessment results — and fix the refresh calendar.

The strategy conversation is the most valuable meeting an audit committee will hold this year — because it forces the board to say aloud what it actually wants from assurance.

Four Ways Strategies Die

Assessors and boards should watch for the four classic failure modes. Shelfware: the strategy is written for the assessor, filed after approval, and never referenced when the annual plan is built — a disconnect any competent reviewer will find in minutes. Template transplant: a document borrowed from a global firm’s model, describing risks the organization does not face and capabilities it does not have. Strategy without money: priorities that imply data analytics, cyber skills, and specialist co-sourcing, attached to a budget that funds none of them — the sufficiency statement to the board exists precisely to surface this conflict. No refresh: a strategy dated before the organization’s last pivot, acquisition, or regulatory change. Each failure mode is visible, and each is avoidable with the discipline the Standards now require.

What Changes When the Watchdog Becomes a Strategist

The practical difference is felt in the boardroom. A watchdog function reports backwards: here is what we found, here is who must fix it. A strategist function reports forward as well: here is where the organization’s next material control risk is forming, here is the assurance we have sequenced over it, and here is the capability we are building before the risk matures. Directors of Caribbean companies navigating digital transformation, regulatory reform, and post-restatement scrutiny do not need less of the first — they need much more of the second. The mandated strategy is how the second becomes possible.

The Dawgen Perspective

In our experience, the strategy requirement is the point in the new Standards where conformance work stops feeling like compliance and starts creating value. Charters and methodologies formalize what exists; the strategy forces choices about what should exist. Functions that take it seriously emerge with a sharper mandate, a defensible budget, and a board that finally understands what its assurance investment buys.

Dawgen Global facilitates internal audit strategy development across the Caribbean — running the stakeholder listening exercise with the independence an internal team cannot bring, mapping assurance universes under our CARISK™ and TRUST360™ frameworks, and building capability roadmaps that draw on our integrated cyber, IT, data analytics, and actuarial practices. Where capability gaps are confirmed, our co-sourcing model closes them without the fixed cost of specialist hires.

Next in the series: “The Board–Internal Audit Relationship: Reporting Lines, Independence, and the Caribbean Reality” — what functional reporting to the board means in practice, and how to make it work in family-controlled and state-owned entities.

| Build a Strategy Your Board Will Actually Use

Dawgen Global’s Internal Audit Strategy Development engagement delivers a conformant, Caribbean-calibrated strategy in six to ten weeks: stakeholder listening, assurance universe mapping, capability roadmap, budget case, and board facilitation — ready for approval and ready for assessment. One document. Every requirement. A function repositioned. Big Firm Capabilities. Caribbean Understanding. |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210