Every technology returns, eventually, to the problem that created it. Article 3 of this series traced the cell company’s birth to the captive insurance boardrooms of the 1990s, where rent-a-captive platforms were selling a separation they could not legally guarantee. A quarter-century later, the segregated accounts company (SAC) arrives in Jamaica as a general-purpose vehicle — but its deepest grooves were cut by insurance, and it is in insurance that Jamaica’s Segregated Accounts Companies Act, 2024 may work its most visible transformation. Government commentary has said as much, naming insurance among the sectors the Act is expected to change. This tenth instalment maps the vehicle onto Caribbean risk financing: the captive structures it unlocks, the underwriting discipline it imposes, the run-off machinery it provides, and the domicile opportunity it opens for Jamaica — drawing, as ever, on the regional model on which the Jamaican statute is built.

Why Insurance Invented the Cell

The problem is worth restating, because it remains the clearest illustration of what the vehicle is for. A captive insurer lets an organisation finance its own risk: premiums that would have gone to the commercial market are paid instead to an insurer the organisation owns, retaining underwriting profit and investment income when losses run well. But a captive needs capital, a licence and administration — a fixed cost that only large risks justify.

The rent-a-captive answered by sharing one licensed insurer among many unrelated participants, each running its own programme inside the vehicle, separated by contract and bookkeeping. The flaw, as Articles 2 and 3 showed, was structural: if one participant’s losses blew through its allocated funds, or the vehicle failed, every participant’s assets stood behind every participant’s liabilities. Guernsey’s protected cell company of 1997 was the industry’s answer, and the Caribbean segregated accounts statutes refined it. What the SAC gives an insurance platform is precisely what contract could not: statutory walls between programmes, effective in the insolvency that insurance exists to think about.

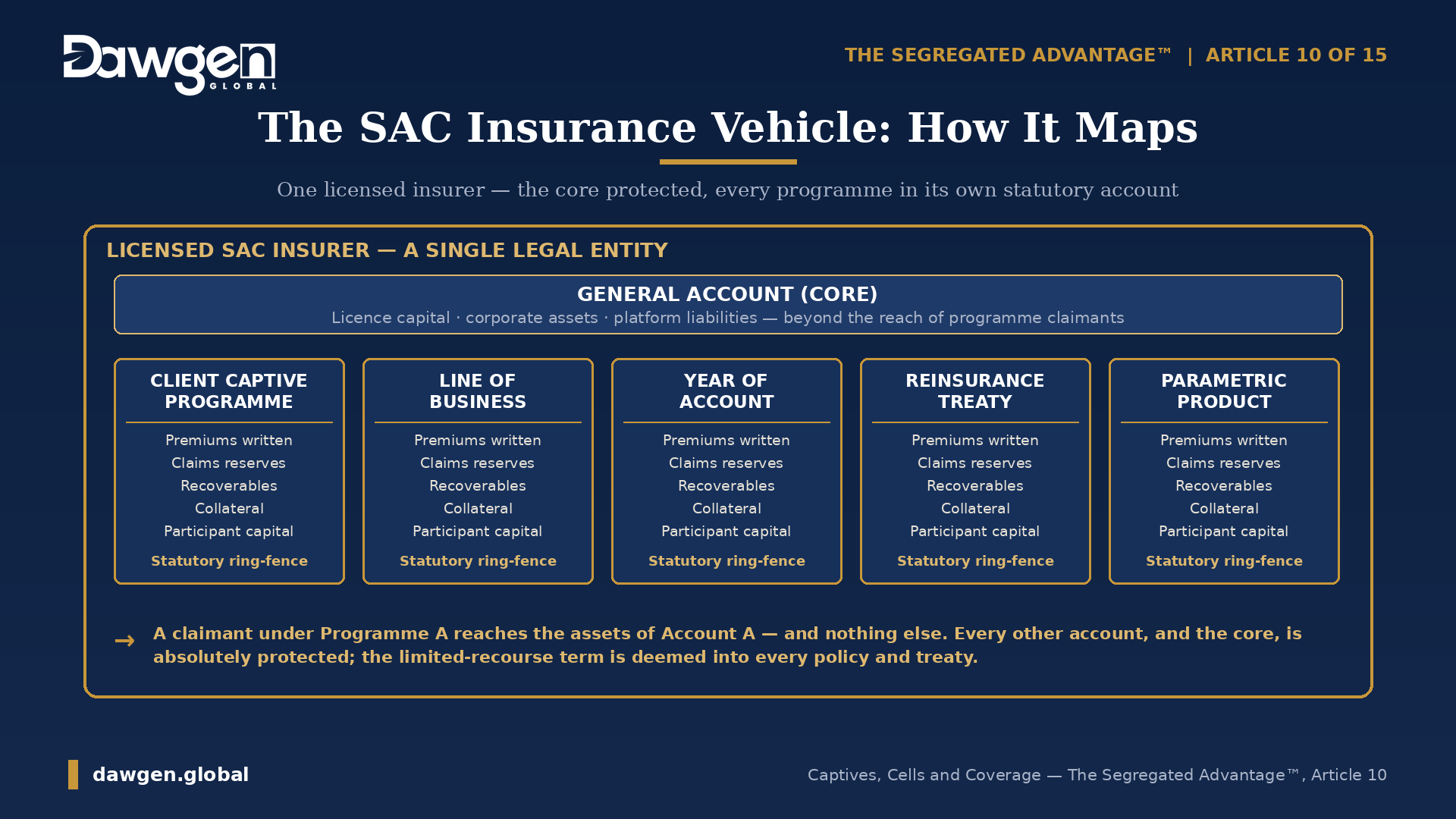

The SAC Insurance Vehicle: How It Maps

The mapping is natural because the vehicle was shaped around it. The licensed insurer registers as a SAC through the insurance gateway of Article 5 — under the Bahamian benchmark, with the written consent of the insurance supervisor; in Jamaica, within the supervisory perimeter of the Financial Services Commission. Each programme becomes a segregated account: a client’s captive programme on a rent-a-captive platform, a line of business, a year of account, a reinsurance treaty, a parametric product. Premiums written for the programme are linked to its account; so are its claims reserves, its recoverables, its collateral and its investment assets. Capital supporting the programme — the participant’s contribution in a cell-captive model — is linked share capital of the account, and the account owner is the participant whose programme it is. The insurer’s own licence capital, corporate assets and platform-level liabilities sit in the general account, the core. A claimant under Programme A’s policies has recourse to Account A’s assets; Programme B’s reserves and the insurer’s core are, in the statute’s words, absolutely protected — and the deemed limited-recourse term of Article 4 writes that wall into every policy and treaty automatically, displaceable only by express agreement.

The Structures It Unlocks

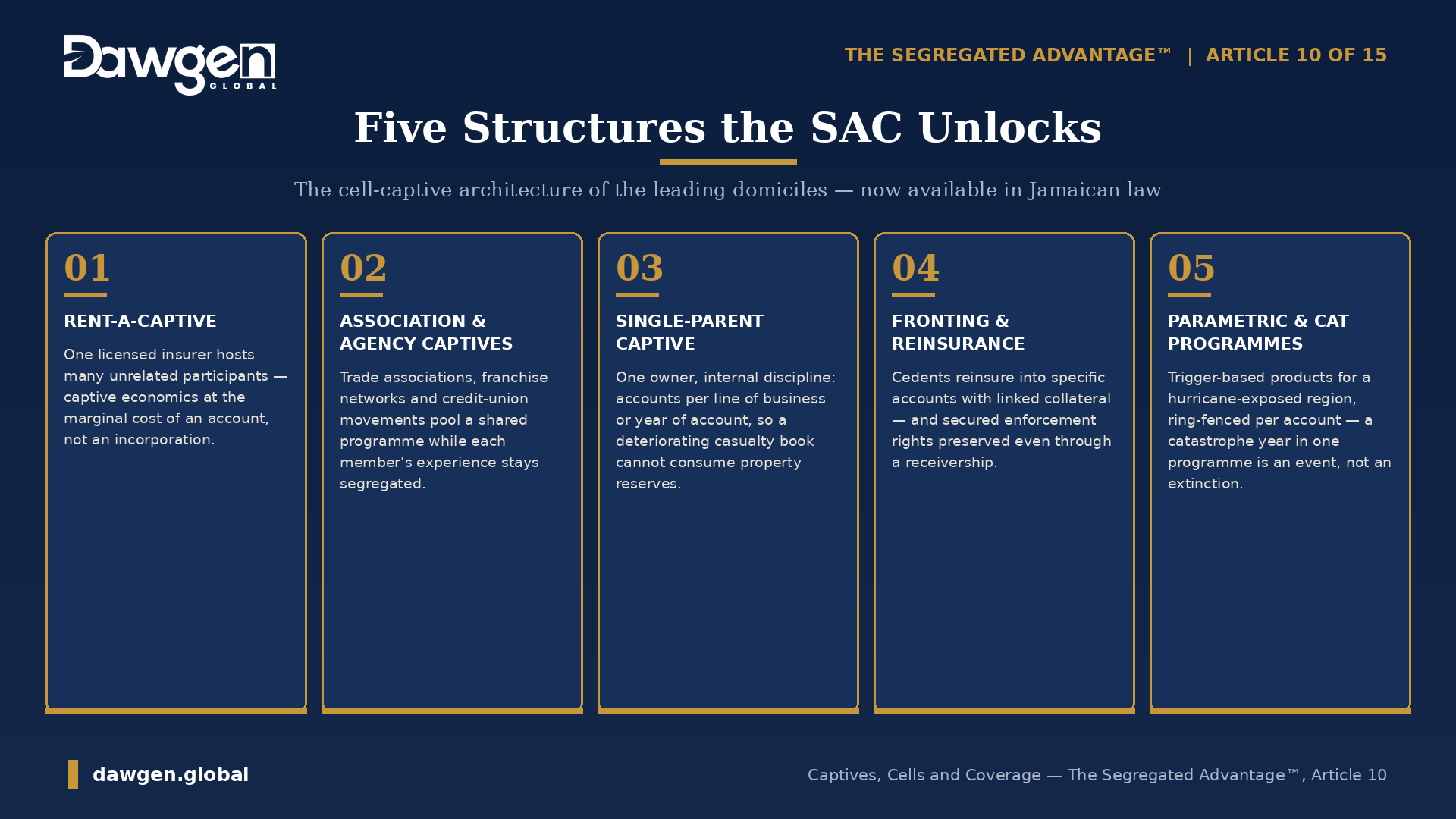

From that base, the familiar architecture of the cell-captive world becomes available in Jamaican law. The rent-a-captive proper: one licensed SAC insurer hosting many unrelated participants, each with its own account, its own capital, its own underwriting result — captive economics without a licensed company per client, at the marginal cost of an account rather than an incorporation. The association or agency captive: a trade association, franchise network or credit-union movement pooling a shared programme while segregating each member’s or each product’s experience. The single-parent captive with internal discipline: one owner, but accounts per line of business or per year of account, so that a deteriorating casualty book cannot consume the property programme’s reserves, and legacy years can be closed cleanly. Fronting and reinsurance structures: a commercial fronting insurer ceding into specific accounts of a SAC reinsurer, with collateral linked to the account it secures — and, critically, with the secured-counterparty carve-out of Article 8 preserving the cedent’s enforcement rights even in a receivership. And the newer frontier: parametric and catastrophe programmes for a hurricane-exposed region, each trigger-based product ring-fenced in its own account so that a catastrophe year in one programme is an event, not an extinction.

Underwriting Discipline, Account by Account

The regime’s solvency architecture, examined in Article 8, reads as if written by an actuary. Each account must be able to pay its own liabilities as they fall due — which, for an insurance account, means reserving discipline programme by programme: actuarially estimated claims liabilities, premium deficiency, and the collateral or capital to stand behind them, all linked to the account and visible in its records. Surplus is released the same way: no dividend or capital return may leave an account that would thereby fail its solvency test, so a profitable programme distributes on its own numbers while an adverse one retains — the cell-captive bargain enforced by statute rather than by the manager’s discretion. The record-keeping duties of Article 4 map onto insurance accounting done properly — premiums, reserves, recoverables and expenses booked to the account they belong to — and the segregated accounts representative of Article 5, where applicable, stands as the statutory early-warning system, obliged to report to the regulator within thirty days of forming the view that an account is reasonably likely to become insolvent. For boards, the disclosure trinity of Article 7 has a specific insurance edge: every policy, treaty, collateral agreement and broker communication must disclose the SAC and identify the account, with the directors personally liable for the omission.

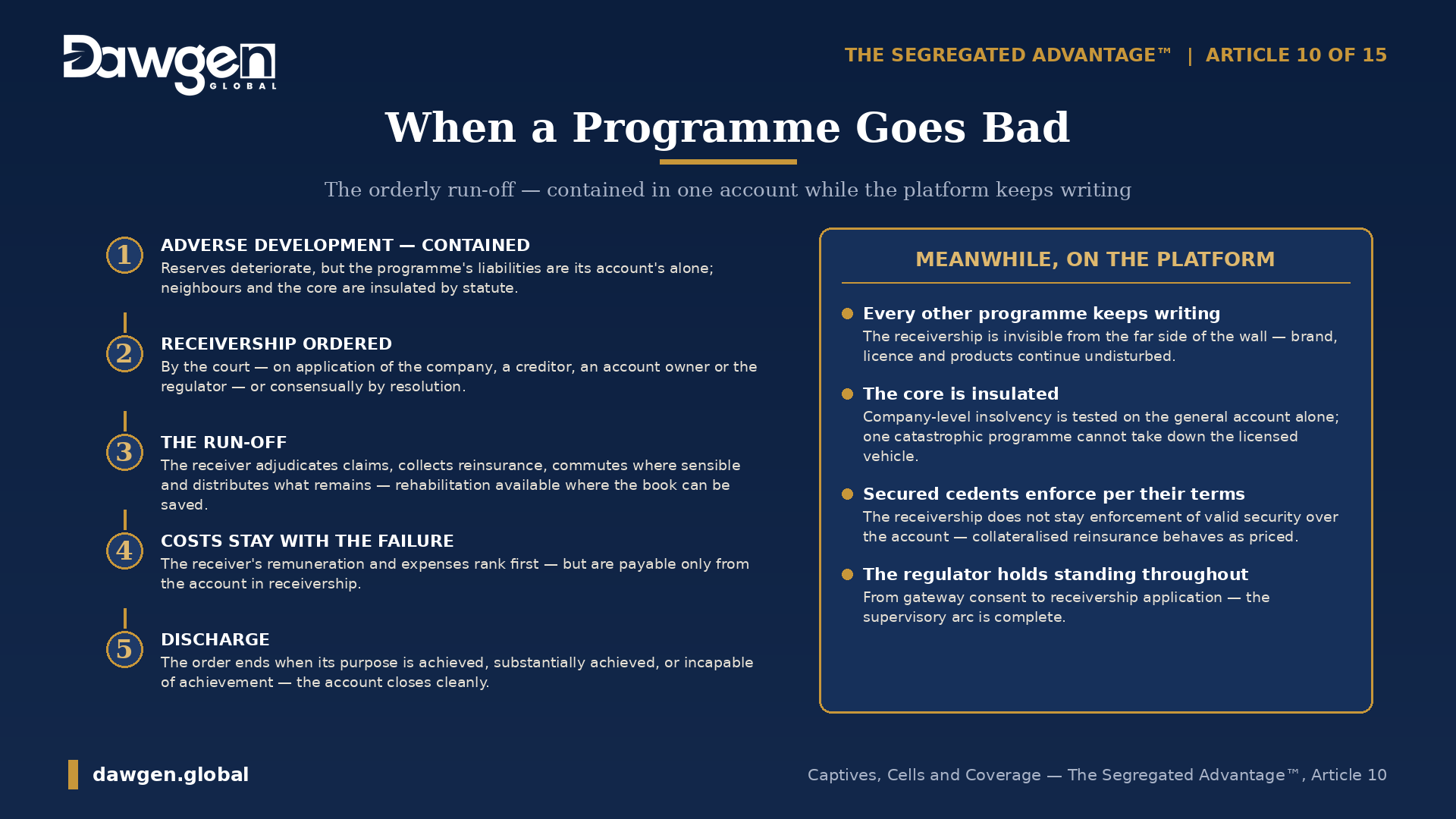

When a Programme Goes Bad

Insurance is the industry of adverse development, and the SAC’s insolvency machinery might have been designed for it — because, historically, it was. A programme whose reserves prove inadequate is contained by construction: its liabilities are its account’s alone, its deterioration cannot reach its neighbours, and the platform’s core is insulated. Where containment must become process, the receivership of Article 8 supplies the insurance industry’s most valued distress tool — the orderly run-off. A receiver confined to the account manages the tail: adjudicating claims, collecting reinsurance, commuting where sensible, distributing what remains — at the account’s own cost, under the court’s supervision, with the regulator holding standing throughout, while every other programme on the platform continues writing. Rehabilitation sits in the statute alongside run-off, so a programme that needs restructuring rather than burial has a lawful path. And because company-level insolvency is tested on the general account alone, one catastrophic programme cannot, of itself, take down the licensed vehicle — the nightmare scenario of every multi-client platform, answered in statute.

Jamaica’s Captive Opportunity

Why does this matter beyond technique? Because the Caribbean’s insurance economics are changing, and Jamaica has positioned itself to participate rather than spectate. Regional businesses face hardening property-catastrophe markets and protection gaps that make self-insurance and alternative risk transfer more attractive every renewal season; conglomerates that once bought everything from the commercial market now weigh captives for retained layers, deductibles buy-downs and uninsurable exposures. Until now, those structures were built offshore — in the domiciles whose statutes Article 3 traced.

The Jamaican SAC changes the calculus in two directions at once. Domestically, it lets Jamaican and regional groups build cell-captive programmes at home, inside a familiar legal system, with local professional support. Internationally, it gives the JIFSA programme a credible insurance product to market: a Bermuda-family vehicle in an anglophone jurisdiction actively inviting operators — with the Bahamas’ 2025 move to incorporated segregated accounts signalling exactly the second-generation features Jamaica’s own framework will be measured against. The domicile contest is real and the incumbents are formidable; but domicile decisions turn on regulation, professional depth and cost as much as statute, and on all three Jamaica has a case to make.

What Insurers and Risk Managers Should Do Now

For the industry, the near-term agenda writes itself. Licensed insurers should evaluate the platform play: whether registering a SAC vehicle — or establishing one — positions them to host cell programmes for clients, associations and affiliates that today have nowhere local to go. Corporate risk managers should revisit the captive feasibility studies that previously died on incorporation costs, because the marginal economics of an account change the answer. Brokers and MGAs should map which of their programmes could be structured into accounts, and what the disclosure and account-identification disciplines mean for their documentation. And everyone touching the sector should watch the regulations and the FSC’s implementing practice, where the insurance-specific calibration of the regime will be settled. Dawgen Global supports this agenda across its service lines — captive feasibility and structuring, actuarial reserving and solvency analysis through its Actuarial & Insurance Regulatory Advisory Division, regulatory engagement, account-level insurance accounting design, and audit and assurance over segregation integrity. The next article takes the analysis onshore in the most literal sense: real estate, project finance, and the developer who never has to incorporate five companies again.

Frequently Asked Questions

What is a rent-a-captive and how does a SAC improve it?

A rent-a-captive shares one licensed insurer among many unrelated participants, each running its own programme. Historically the programmes were separated only by contract and bookkeeping; a segregated accounts company (SAC) makes each programme a statutorily ring-fenced account, so one participant’s losses cannot reach another’s assets or the insurer’s core — even in insolvency.

How is an insurance programme structured inside a SAC?

The programme becomes a segregated account: its premiums, claims reserves, recoverables, collateral and investment assets are linked to the account; participant capital is linked share capital; and the participant is the account owner. The insurer’s licence capital and platform liabilities sit in the general account, protected from programme claimants.

Can a policyholder of one programme claim against another programme’s assets?

No. A liability linked to one account is enforceable only against that account’s assets, and every policy and treaty is deemed to contain a term that the counterparty has no recourse to other accounts or the general account — displaceable only by express written agreement by parties with authority over the exposed accounts.

How does solvency work in a SAC insurance structure?

Account by account. Each programme must be able to pay its own liabilities as they fall due, which imports actuarial reserving discipline per account; dividends and capital returns are blocked from any account that would thereby fail its test; and the statutory representative, where required, must report a reasonable likelihood of account insolvency to the regulator within thirty days.

What happens when a programme develops adversely?

The deterioration is contained in its account, and where process is needed the account enters receivership — the insurance industry’s orderly run-off, court-supervised, at the account’s own cost, with the regulator holding standing and secured cedents’ enforcement rights preserved — while every other programme continues writing. One bad programme cannot, of itself, bring down the licensed vehicle.

Could Jamaica become a captive insurance domicile?

That is the ambition the Act serves. The SAC gives Jamaica a Bermuda-family insurance vehicle inside its international financial services centre strategy, letting regional groups build cell-captive programmes at home and inviting international operators. The incumbents are established, but domicile decisions turn on regulation, professional depth and cost as much as statute — and Jamaica now has the statute.

How can Dawgen Global help?

Dawgen Global supports captive feasibility and structuring, actuarial reserving and solvency analysis through its Actuarial & Insurance Regulatory Advisory Division, regulator engagement, account-level insurance accounting design, and audit and assurance over segregation integrity. Contact [email protected] to discuss your programme.

Previously in the series: Article 9 — The Umbrella Fund Reimagined: SACs and the Future of Collective Investment Schemes in Jamaica.

Next in the series: Article 11 — One Developer, Many Projects, Zero Contagion: SACs in Real Estate and Project Finance.

This article is provided for general information and is not legal or tax advice. Specific structures should be verified against the current text of the Segregated Accounts Companies Act, 2024, its regulations, and the requirements of the relevant Jamaican regulators.

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210