Profit is an opinion. Cash is a fact. Businesses do not die of unprofitability — they die of running out of cash, and many die profitable.

The Problem, Lived

It is Thursday afternoon, and “Devon” is doing the arithmetic he does every Thursday afternoon. Payroll runs tomorrow: that number is fixed. The equipment lease is due Monday: fixed. A supplier who has carried him for sixty days has stopped being polite. Against all of that, one number that refuses to move: the balance in the business account. Two corporate clients owe him more than four times what he needs — invoices forty and seventy days old, both “in process.” He will spend tonight deciding, once again, who gets paid and who gets a phone call.

Here is what makes Devon’s Thursday truly maddening: his business is profitable. His accountant confirmed it — a healthy surplus on last year’s income statement. The jobs make money. The margins are real. And none of it can make payroll tomorrow, because profit lives on paper and payroll is paid in cash.

This is the profitable-but-broke paradox, and it is the most dangerous condition in small business precisely because everything looks fine from the outside. Revenue is growing. Customers are signing. The P&L smiles. Meanwhile the company is quietly suffocating in the gap between when money is earned and when money arrives.

Why It Happens Here

Caribbean small businesses operate inside a structural cash squeeze that most business literature never mentions. On the inflow side, the region’s dominant customers — large corporates and government entities — routinely pay in forty-five, sixty or ninety days, and a small supplier has little leverage to demand better. On the outflow side, the opposite rule applies: wages, statutory obligations, rent and utilities are due on the clock, and many suppliers of imported goods require payment — often in foreign exchange — weeks or months before the goods can be sold. The small business sits in the middle, financing everyone else’s timing with cash it does not have.

Layer on the regional amplifiers: seasonality that concentrates revenue in a few months while costs run all year; thin access to affordable credit, which removes the buffer that businesses elsewhere take for granted; and the fact that most owners track their business through the profit-and-loss lens their accountant reports in, not the cash lens their survival depends on. Then comes the cruelest twist of all — growth makes it worse. Every new contract means spending on labor and materials today for revenue that arrives in ninety days. Unmanaged, success itself becomes the thing that kills the company. Businesses genuinely do grow themselves to death.

| The One-Sentence Reframe

Stop asking “are we profitable?” and start asking “will we have cash in week seven?” Profitability is measured over a year and tells you if the model works. Cash is measured in weeks and tells you if you will be alive to enjoy the model working. You need both — but only one of them can kill you by Friday. |

Why Generic Advice Fails

The internet’s standard prescriptions assume conditions that do not hold here. “Open a line of credit” assumes accessible, affordable credit. “Charge late fees” assumes leverage over customers ten times your size. “Use an app that syncs your banking data” assumes integrations that many regional banks do not offer. Most of this advice was written for a world of thirty-day payment norms and cheap capital — and following it in a ninety-day, expensive-capital environment produces frustration, not cash.

What works in the Caribbean context is not a product but a discipline: seeing cash forward instead of backward, and then systematically re-engineering the timing of money in and money out. That is exactly what the CASHFLOW360™ framework within Dawgen Global’s VENTURE™ system was built to install.

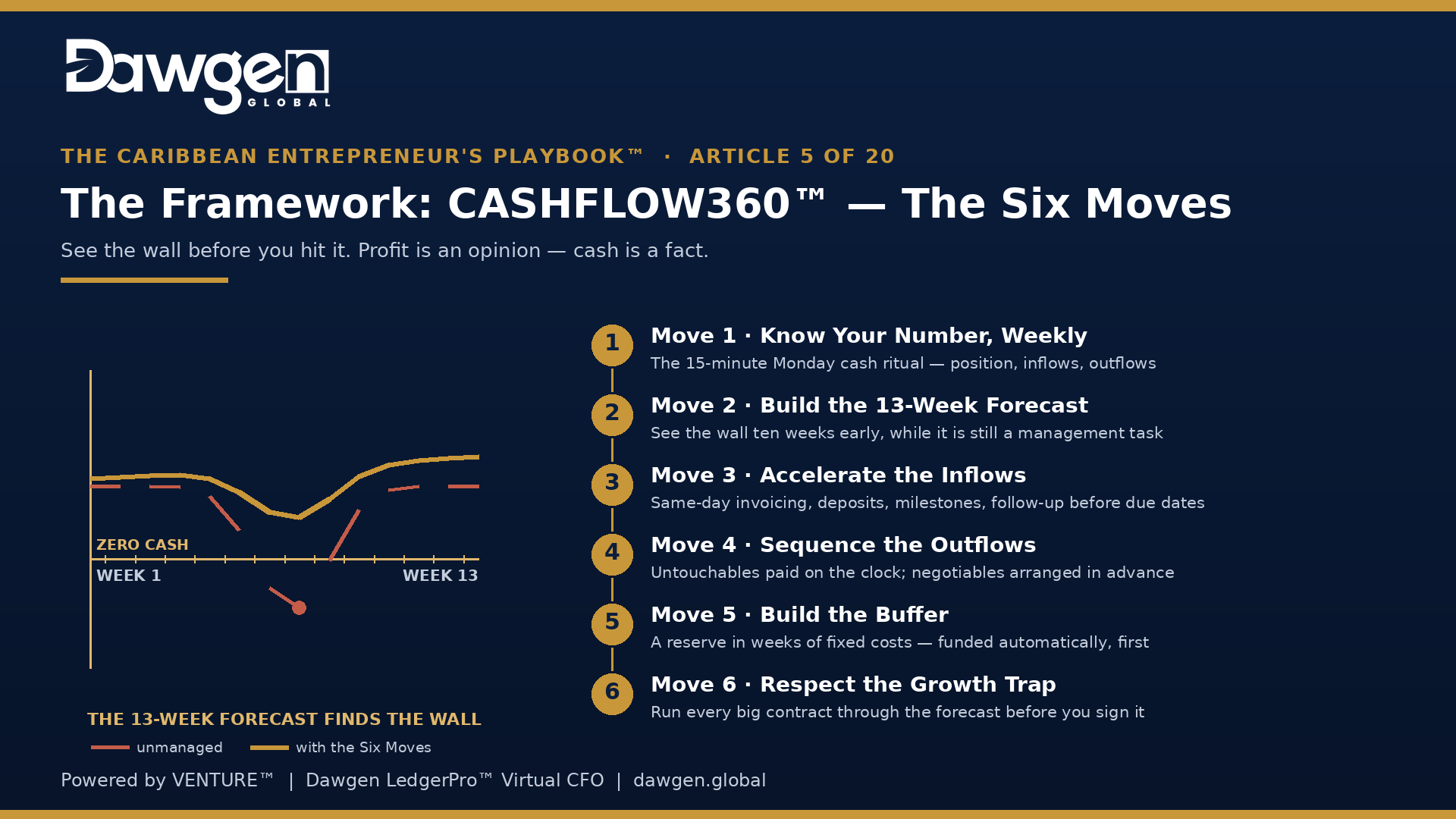

The Framework: CASHFLOW360™ — The Six Moves, Step by Step

Cash flow is fixed with six moves, in sequence. The first two give you sight; the middle two re-engineer timing; the last two build permanence:

- Move 1 · Know Your Number, Weekly — Institute a fifteen-minute Monday ritual: one page showing cash in the bank, money expected in over the next four weeks (by name and date, not hope), and money that must go out. Most owners can state last month’s sales and cannot state next Friday’s cash position. Reverse that. The weekly cash ritual is to a business what a pulse check is to a patient.

- Move 2 · Build the 13-Week Rolling Forecast — Extend the ritual into the single most powerful tool in small-business finance: a rolling thirteen-week cash forecast — every expected inflow and outflow, week by week, one quarter ahead. Thirteen weeks is long enough to see a crisis while there is still time to prevent it, and short enough to be honest. The forecast’s job is to find the wall before you hit it: the week where the line goes negative. A crisis discovered in week two is a catastrophe; the same crisis discovered ten weeks early is a management task.

- Move 3 · Accelerate the Inflows — Attack the gap between earning and receiving at every joint: invoice the day the work completes, not at month-end; require deposits before work begins and milestone payments on longer jobs, so the customer finances the work instead of you; install a follow-up rhythm that starts before the due date, not thirty days after it; and consider a modest early-payment discount — a small margin sacrifice is often the cheapest financing available to you. Every day shaved off your average collection time is permanent, recurring cash.

- Move 4 · Sequence the Outflows — Match the timing of money out to the reality of money in. Separate obligations into the untouchables — payroll and statutory payments, which are always paid on time, in full — and the negotiables, where terms can be arranged. Then talk to your suppliers before you are late, not after: a supplier told in advance becomes a partner in your timing; a supplier surprised becomes a creditor. Businesses rarely lose suppliers because of slow payment; they lose them because of silence.

- Move 5 · Build the Buffer — Set a reserve target expressed in weeks of fixed costs — not a vague ambition but a number on the forecast — and fund it with a fixed percentage of every receipt, transferred automatically to a separate account before spending decisions are made. The buffer converts emergencies back into inconveniences. It is also, not incidentally, what transforms your posture in every negotiation: the business that can survive six weeks without a receipt negotiates very differently from the one that cannot survive one.

- Move 6 · Respect the Growth Trap — Before accepting any large new contract, run it through the forecast first: what must be spent, in which weeks, against receipts arriving when? Know your cash conversion cycle — the days between paying for inputs and collecting from the customer — because that number tells you how much every dollar of growth will cost you in cash before it pays you in profit. Growth is not free. Budget for it deliberately, or it will finance itself out of your payroll.

The Framework in Action: A Worked Scenario

The following scenario is a fictional composite created for this series to illustrate the framework. It does not depict any actual business or client of the firm.

Return to Devon and his Thursday arithmetic. His first thirteen-week forecast takes an afternoon to build and is, in his words, the most frightening document he has ever read: it shows the line crossing zero in week seven, driven by a large materials purchase landing three weeks before the related project payment. But for the first time, the crisis is visible in advance — which means for the first time, it is preventable. He approaches the customer with a milestone-billing proposal and the supplier with a split-payment arrangement. Both agree. The wall in week seven becomes a dip.

Then the system goes in. New contracts carry a deposit requirement — he loses exactly one prospective customer over it, and concludes the customer was a future bad debt identifying itself early. Invoices go out the day work completes, with follow-up calls the week before due dates. Two percent of every receipt moves automatically to a reserve account. In this illustration, six months later his average collection time has fallen by more than three weeks, the buffer covers a month of fixed costs, and the Thursday arithmetic is simply gone — replaced by a Monday ritual that takes fifteen minutes and a forecast that has already caught two more walls while they were still ten weeks away. The business is not dramatically more profitable than before. It is dramatically more alive.

Self-Diagnostic: How Close Is the Wall?

One point for every “no”:

- Do you know, right now, your expected cash position four weeks from today?

- Do you maintain a rolling forecast that looks at least one quarter ahead, week by week?

- Are invoices issued the day work completes, with follow-up before the due date?

- Do you hold a cash reserve equal to at least four weeks of fixed costs?

- Before taking a large order, do you calculate what it will consume in cash before it pays?

Two or more points means you are managing cash by instinct in an environment engineered to punish instinct. The wall may already be on your forecast — you simply haven’t built the forecast that would show it.

When to Call In Help

The six moves can be self-installed by a disciplined owner with time. But certain signals say the situation needs professional horsepower now: the Thursday arithmetic has become routine; you are financing the business from personal funds or delaying statutory payments; you cannot build the forecast because the bookkeeping behind it is months behind; or growth is accelerating and every new win makes the pressure worse, not better. Each of these means the problem is compounding weekly — and cash problems, unlike most business problems, have a clock on them.

This is precisely the gap the Virtual CFO model exists to close. Most small businesses cannot justify a full-time finance executive — but through Dawgen LedgerPro™, they can access one at a fraction of the cost: the bookkeeping brought current and kept current, the thirteen-week forecast built and maintained, the weekly cash ritual run for you, and an experienced finance professional in the room for every pricing, hiring and expansion decision. It is the difference between owning a map and having a navigator.

| START A 13-WEEK CASH FLOW FORECAST WITH A VIRTUAL CFO

Dawgen Global’s Virtual CFO service, powered by Dawgen LedgerPro™ and the CASHFLOW360™ framework, begins with your business’s first thirteen-week cash flow forecast — built with you, from your real numbers, in days. You will see every wall before you hit it, and leave with the full six-move system installed: collection acceleration, payment sequencing, an automated buffer and a weekly cash ritual that takes fifteen minutes. Contact us today to start your forecast — before Thursday does its arithmetic again. 📩 [email protected] | 📞 876-929-3670 / 876-665-5926 | 🇺🇸 855-354-2447 | 🌐 dawgen.global GET THE FULL PLAYBOOK This is Article 5 of The Caribbean Entrepreneur’s Playbook™ — 20 problems, 20 how-to frameworks, one system. Pre-register at dawgen.global to receive the complete Playbook e-book on release, free. |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210