Why AI systems must be explainable, traceable, and defensible from the start

EXECUTIVE SUMMARY

As artificial intelligence becomes embedded in business operations, one question becomes unavoidable: can the organization prove what happened? When AI influences a decision, produces an output, or triggers a workflow, management must be able to reconstruct the process — the data used, the instruction given, the output produced, the human review, the approval, and the final action. That is auditability by design: evidence trails built into the AI operating model from the beginning, not reconstructed after a dispute, audit, or regulatory inquiry. This article — the fifth in Dawgen Global’s AI Governance & Assurance Series and the evidence foundation beneath the previous four — sets out the ten components of Dawgen Global’s AI evidence trail framework, explains why explainability alone is not enough, addresses the special challenges of agentic AI, and gives boards the one question that reveals whether an auditability gap exists.

Can the organization prove what happened?

Artificial intelligence is changing how organizations make decisions, process information, serve customers, manage risk, and execute work. AI tools can summarize complex documents, generate reports, analyze transactions, recommend actions, detect anomalies, support compliance reviews, and automate workflows.

But as AI becomes more embedded in business operations, one question becomes unavoidable: can the organization prove what happened?

When an AI system influences a decision, produces an output, triggers a workflow, or supports management judgment, the organization must be able to explain and evidence the process. What data was used? What instruction was given? What output was produced? Who reviewed it? What decision followed? Was the action approved? Was the result consistent with policy, law, regulation, and business intent?

This is the essence of auditability by design. AI systems should not be deployed first and documented later. Auditability must be built into the AI operating model from the beginning.

This article is the fifth in our AI Governance & Assurance Series — and in a real sense, it is the foundation beneath the other four. Converged cyber-AI controls (article one), agent guardrails (article two), independent assurance (article three), and continuous validation (article four) all depend on the same raw material: evidence. Without audit trails, every one of those disciplines becomes opinion without support.

The AI evidence gap

Many organizations are adopting AI faster than they are building evidence trails around AI use. Employees may use generative AI tools to draft documents, analyze data, summarize customer issues, prepare management reports, or review contracts. Departments may introduce AI-enabled platforms without fully understanding logging, retention, review, and control requirements. Vendors may embed AI into enterprise systems without clearly explaining how outputs are generated or tracked.

This creates an AI evidence gap. The organization may know that AI was used, but not be able to prove how it was used. It may rely on AI-generated output, but not retain the input, prompt, data source, version, review record, or approval evidence. It may accept an AI recommendation, but not document the rationale for management’s final decision.

That weakness can become serious when there is a dispute, audit, regulatory inquiry, customer complaint, data breach, financial reporting issue, or operational failure.

For Caribbean organizations, the evidence obligation is already written into law and practice. Jamaica’s Data Protection Act makes accountability a standard — a data controller must be able to demonstrate how personal data was processed, which is an evidence requirement, not merely a policy one. Financial-sector regulators expect technology-risk decisions to be documented and defensible. And where AI touches processes that feed the financial statements — estimates, provisioning, reconciliations, fraud monitoring, revenue analytics — external auditors will ask for this evidence at year-end. An AI-supported balance that cannot be evidenced is an audit problem waiting to be found.

Why auditability matters

Auditability is not only an audit concern. It is a governance, cybersecurity, compliance, legal, operational, and reputational requirement.

For boards and executives, auditability provides confidence that AI is operating within the organization’s risk appetite. For internal audit, it provides the evidence needed to test controls. For regulators, it supports transparency and accountability. For customers and stakeholders, it strengthens trust. For management, it enables investigation, learning, remediation, and defensible decision-making.

Without auditability, AI becomes difficult to govern. An organization may struggle to answer basic questions:

- Which AI tool was used, and what data was accessed?

- Was confidential or personal data included?

- What prompt or instruction was submitted, and what output did the AI produce?

- Was the output reviewed by a human — and was the decision accepted, rejected, or modified?

- Who approved the final action?

- Did the AI system behave consistently with policy?

- Was there any exception, override, or incident?

If these questions cannot be answered with evidence, the organization has a control weakness.

Explainability is not the same as auditability

Organizations often discuss explainability when speaking about AI. Explainability is important, especially for high-impact AI systems. It refers to the ability to understand, in practical terms, why an AI system produced a particular output or recommendation.

Auditability is broader. Auditability asks whether the organization can reconstruct the full decision pathway. It is concerned not only with how the model behaved, but also with governance, data use, user activity, controls, approvals, exceptions, monitoring, and management accountability.

An AI output may be partially explainable but still poorly auditable if there are no logs, no review evidence, no approval trail, and no record of how the output was used. For AI assurance, both are needed: explainability to understand the output, and auditability to evidence the control environment.

The new audit trail: from system logs to decision logs

Traditional IT audit often focuses on system logs, access records, change management evidence, configuration settings, and transaction histories. AI requires a broader evidence trail. Organizations must move from system logging alone to decision logging.

Decision logging captures the journey from input to output to action. It should show not merely that a system was accessed, but how AI influenced the business decision.

For example, where AI supports a credit decision, contract review, fraud alert, procurement recommendation, compliance assessment, financial estimate, customer response, or cybersecurity action, the organization should retain sufficient evidence to support management’s conclusion. The evidence trail should show the business context, the AI interaction, the control checks, the human review, the final decision, and any exception handling.

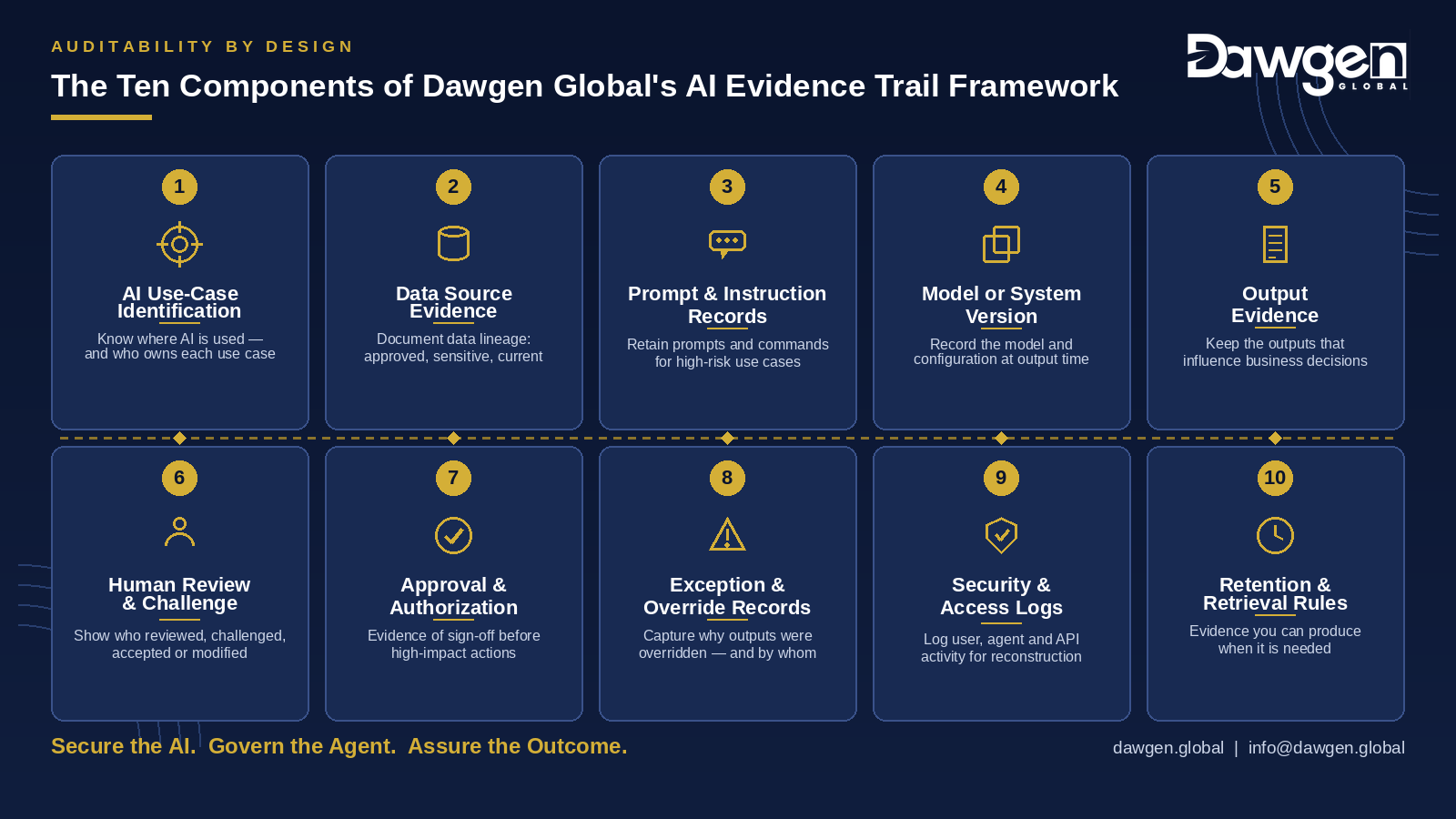

The ten components of Dawgen Global’s AI evidence trail framework

Dawgen Global recommends that organizations build AI audit trails around ten practical components.

1. AI use-case identification

Each AI-supported process should be clearly identified. The organization should know where AI is used, whether it supports low-risk productivity tasks or high-impact business decisions, and who owns the use case.

2. Data source evidence

The audit trail should document the data sources used by the AI system — internal or external, approved or unapproved, sensitive or non-sensitive, current or historical, structured or unstructured. Data lineage matters because poor data governance can undermine the reliability of AI outputs.

3. Prompt and instruction records

For generative AI and agentic AI, prompts and instructions are part of the control environment. The organization should retain relevant prompts, system instructions, user inputs, and workflow commands for high-risk use cases. This allows reviewers to assess whether the AI was properly instructed and whether users attempted to bypass controls.

4. Model or system version

AI systems may change over time. Vendors update models. Internal teams adjust configurations. Prompt libraries evolve. Workflows are modified. The audit trail should record the model, tool, version, configuration, or workflow state used at the time of the output.

5. Output evidence

The AI-generated output should be retained where it influences a business decision or regulated process. This includes summaries, recommendations, classifications, alerts, scores, drafts, decisions, or actions proposed by the AI.

6. Human review and challenge

Auditability requires evidence of meaningful human oversight. The record should show who reviewed the AI output, what they considered, whether they challenged the output, and whether they accepted, modified, or rejected it. Human review should not become a symbolic approval step.

7. Approval and authorization

Where AI outputs lead to business actions, there should be evidence of approval. This is especially important for payments, contracts, customer communications, regulatory filings, financial reporting, hiring, lending, procurement, cybersecurity response, and legal conclusions.

8. Exception and override records

When AI outputs are overridden or exceptions occur, the organization should capture the reason. Overrides can reveal control weaknesses, model performance issues, policy conflicts, or emerging risks.

9. Security and access logs

AI audit trails must include cybersecurity evidence: user access, agent access, data retrieval, system interactions, API calls, privileged activity, failed access attempts, and unusual behavior. For AI agents, tool calls and autonomous actions should be logged in a manner that allows reconstruction.

10. Retention and retrieval rules

Evidence is only useful if it can be retained and retrieved. Organizations should define retention periods, storage locations, access restrictions, legal hold procedures, and retrieval responsibilities. Auditability fails when evidence exists temporarily but cannot be produced when needed. Under Dawgen Global’s TRUST360™ continuous-governance approach, retention and retrieval are monitored as living controls — tested regularly, not assumed.

Auditability for AI agents

AI agents create special auditability challenges because they may operate across multiple systems and perform several steps to complete a task. An AI agent may read a document, query a database, draft an email, call an application, update a workflow, generate a recommendation, and request approval. Each step may occur quickly and across different platforms.

For agentic AI — governed under Dawgen Global’s D-AGENTICA™ methodology — auditability must capture:

- Agent identity, task objective, and tools called

- Systems accessed, data retrieved, and intermediate steps

- Output generated, approval requested, and action completed

- Exception or failure events and human oversight

- Time and sequence of activities

The goal is to ensure that the organization can reconstruct what the agent did and determine whether it acted within approved authority.

The role of auditability in AI assurance

AI assurance depends on evidence. Without evidence, assurance becomes opinion without support. An AI assurance review should test whether audit trails are complete, reliable, accessible, protected, and appropriate to the risk level of each AI use case.

Assurance providers should examine whether the organization can produce evidence over AI governance and ownership, risk classification, data governance, cybersecurity controls, model validation, human oversight, output quality, exception handling, vendor management, incident response, and board reporting.

The stronger the audit trail, the stronger the assurance conclusion.

Common auditability weaknesses

In its advisory work, Dawgen Global sees several recurring weaknesses as AI adoption expands. First, AI use is decentralized and informal, making it difficult to identify all use cases. Second, employees may use public or third-party tools without approved logging or data controls. Third, AI outputs may be copied into reports or emails without preserving the original prompt, data, or review evidence. Fourth, vendor contracts may not provide sufficient audit rights or transparency. Fifth, management may rely on AI outputs without defining who is accountable for the final decision.

These weaknesses are manageable — but only if they are identified early.

Building auditability by design

Organizations should not wait for an audit finding, regulatory inquiry, or AI failure before addressing evidence trails. Auditability should be part of AI design and implementation. Before deploying an AI system, management should define:

- What evidence must be captured, and who owns it?

- Where will it be stored, and how long will it be retained?

- Who can access it, and how will it be protected?

- How will exceptions be reported, and how will evidence be reviewed?

- How will the board receive assurance?

These questions should be built into AI project governance, vendor selection, system configuration, cybersecurity design, internal control documentation, and user training.

The board-level question

Boards and audit committees should ask a simple but powerful question:

If an AI-supported decision is challenged, can management reconstruct and defend what happened?

If the answer is uncertain, the organization has an auditability gap. The board does not need to review every AI log or prompt. However, it should expect management to establish the systems, controls, policies, and assurance mechanisms necessary to produce reliable evidence when required.

“An AI decision that cannot be evidenced cannot be properly governed. Auditability must be designed into AI from the start, because trust requires more than output — it requires proof.”

— Dr. Dawkins Brown, Executive Chairman, Dawgen Global

How Dawgen Global can help

Dawgen Global supports organizations across the Caribbean and globally in designing secure, governed, auditable, and assurance-ready AI systems. Our integrated multidisciplinary model brings together cybersecurity, IT audit, internal audit, external audit, risk advisory, data protection, compliance, and board advisory expertise — big firm capabilities, Caribbean understanding.

A practical engagement pathway:

- Assess — AI Auditability & Evidence Trail Review; AI Governance & Cyber Risk Readiness Assessment; AI Inventory and Risk Classification; AI Vendor Audit Rights and Transparency Review

- Design — AI Logging and Retention Framework Design; Human-in-the-Loop Control Design; Agentic AI Activity Logging Design under D-AGENTICA™; AI Policy and Procedure Development

- Assure continuously — Continuous AI Control Monitoring under TRUST360™; Independent AI Assurance Review; Board and Audit Committee AI Risk Briefings

Take the first step

Can your organization prove how AI-supported decisions are made, reviewed, approved, and monitored? Dawgen Global can help you design AI audit trails that strengthen governance, cybersecurity, compliance, risk management, and board assurance.

Secure the AI. Govern the Agent. Assure the Outcome.

Contact Dawgen Global today to request an AI Auditability & Evidence Trail Review.

Email: [email protected] | Web: dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210