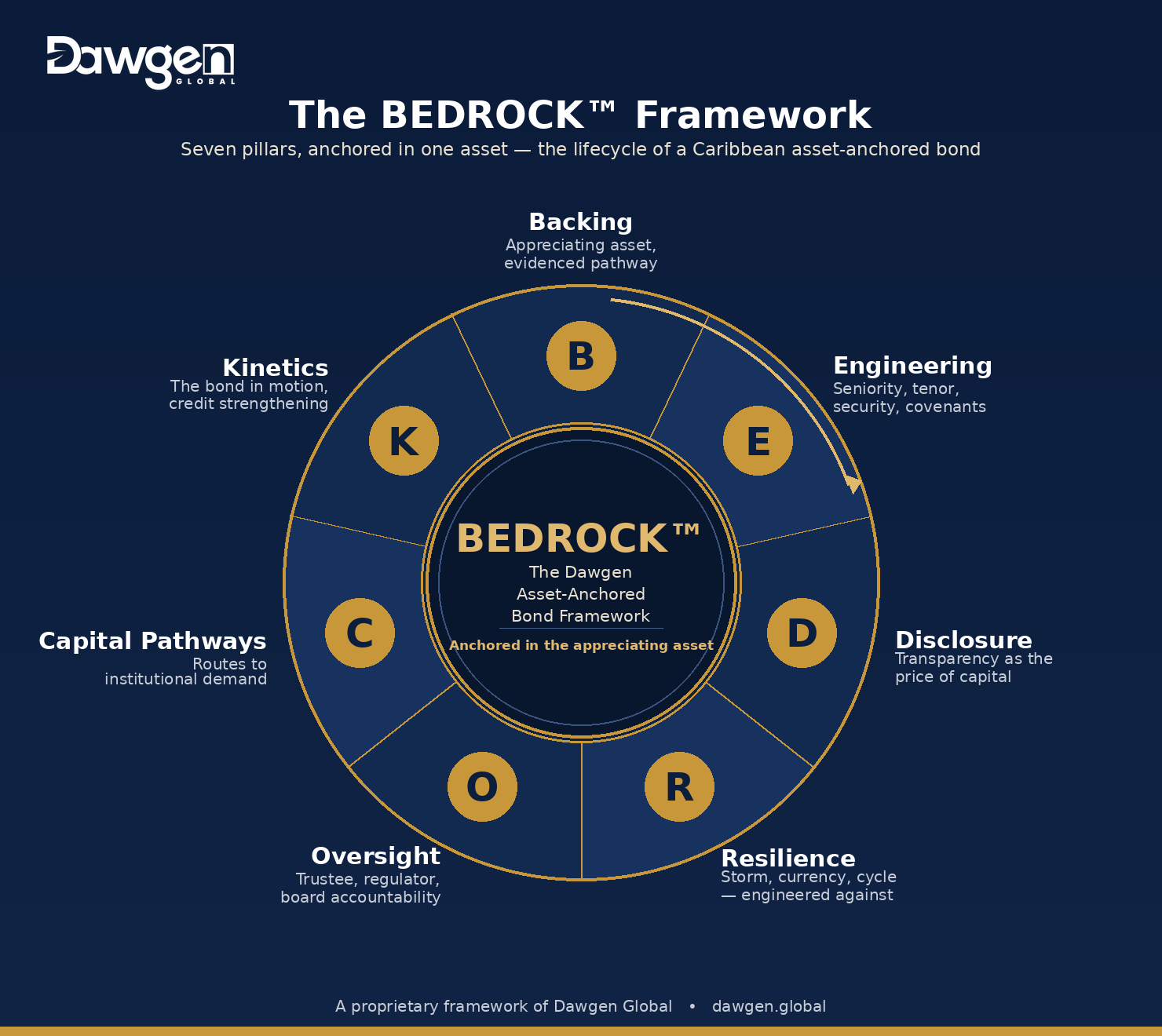

Pillar O of the BEDROCK™ Framework: trustees, regulatory alignment, and board accountability — the machinery that enforces every promise the instrument makes

By the close of Article 5, the BEDROCK™ instrument was substantially built: an appreciating asset, soundly engineered, fully disclosed, and stress-proofed against the Caribbean’s storms, currency shocks, and cycles. A prudent investor reading the offering document would find a credit they could underwrite. And yet they would still, rationally, hesitate — because everything described so far is a set of promises the issuer makes about itself. The security exists because the issuer granted it; the covenants bind because the issuer agreed to them; the reserves are funded because the issuer funded them. What happens when the issuer’s interests and the bondholders’ diverge — as, over fifteen years, they inevitably will?

That question is the reason Pillar O exists. Oversight is the governance machinery that converts the issuer’s promises into enforceable, independently monitored obligations — the trustee who holds the security on the investors’ behalf, the regulatory framework the instrument must satisfy, and the board accountability that makes directors personally answerable for the bond’s obligations. Where Disclosure (Pillar D) lets investors see the credit, Oversight ensures that what they see is enforced by someone other than the party they are relying on. It is the difference between trusting the issuer and not having to.

This article sets out the Oversight doctrine across its four domains — the trustee architecture, regulatory and listing alignment, board accountability, and use-of-proceeds governance — and the conflicts discipline that runs through all of them. Governance is the pillar issuers are most tempted to treat as paperwork. The doctrine treats it as part of the security package: machinery as load-bearing as the charge over the asset.

The Trustee: The Investors’ Standing Presence

Bondholders are, by nature, dispersed and passive. A pension fund holding a slice of a fifteen-year issue cannot monitor an issuer daily, enforce a covenant alone, or act in the chaos of a default. The trustee is the doctrine’s answer to that structural weakness: a single, independent, professional party that holds rights and security on behalf of all bondholders and acts for them across the life of the instrument. BEDROCK™ distinguishes two trustee functions, which may sit with one institution or two.

- The security trustee — the party that holds the security — the charges, the assignments, the share pledge of Article 3’s security perimeter — in trust for the bondholders. Because the security is held by the trustee rather than by individual investors, it can be enforced coherently, by one empowered party, rather than dissolving into a scramble of competing claims. This is what makes a dispersed bond issue enforceable at all.

- The bond trustee — the party that monitors compliance, receives the issuer’s reports and compliance certificates (Pillar D), administers covenant testing, convenes bondholders when decisions are needed, and exercises the bondholders’ collective rights. The bond trustee is the standing institutional presence that a passive, dispersed investor base otherwise lacks.

Three disciplines make the trustee real rather than ornamental. Independence: the trustee must have no economic interest in the issuer and no relationship that compromises its duty to bondholders. Capacity: it must be a professional trustee with the standing and resources to act, including in a crisis. Empowerment: the trust deed must give the trustee genuine powers — to demand information, to declare default, to accelerate, and to enforce the security — because a trustee with duties but no powers is a mailbox, not a protector. The doctrine’s test: in the scenario where the issuer most wants to delay, does the trustee have the standing and the authority to act anyway?

Regulatory and Listing Alignment

An asset-anchored bond is issued into a regulatory environment, and the doctrine treats regulatory alignment not as a hurdle to clear but as a layer of protection to embrace — because the same rules that constrain the issuer reassure the investor. Three dimensions matter.

Securities Regulation and Distribution Route

Every issue must satisfy the securities law of its jurisdiction — in the regional context, the relevant Financial Services Commission (FSC) or equivalent securities regulator. The doctrine’s decision is the distribution route: a public offering, with its fuller prospectus and continuing-obligation requirements, or an exempt or private placement to qualified institutional investors under the applicable exemptions. The choice (developed under Pillar C) shapes the disclosure and governance obligations the issue carries; the doctrine’s rule is that the route be chosen deliberately and its obligations met fully, never that the lighter route be used to evade protections the instrument should carry anyway.

Listing and Exchange Discipline

Where an issue is listed — on a regional securities exchange — the listing rules impose a continuing-obligations regime: periodic reporting, material-event disclosure, and corporate-governance standards enforced by the exchange. The doctrine views listing favourably beyond its liquidity benefits (a Pillar K matter): the exchange becomes an additional, independent monitor, and listed status is itself a signal of disclosure discipline that supports the pricing dividend of Article 4. Listing is not always the right route for every issue, but where chosen, its discipline is an asset, not a cost.

Sectoral and Prudential Overlay

Some backing assets and some investors carry their own regulators — the central bank, an insurance or pensions supervisor, a utility regulator. The doctrine requires that these overlays be mapped at issuance: an instrument that satisfies securities law but trips a prudential limit on its target investors, or a sector regulator’s consent requirement on its asset, is not ready to issue. Regulatory alignment means alignment with every regulator the instrument touches, not merely the securities regulator.

Board Accountability: Making Promises Personal

Trustees and regulators are external machinery. The third domain is internal: the accountability of the issuer’s own board and management for the bond’s obligations. A covenant is a promise by the company; the doctrine’s concern is to ensure that real, identifiable people are answerable for keeping it — because companies do not make decisions, directors do.

Three mechanisms give board accountability force. First, the compliance certificate of Article 4, signed by directors or the chief financial officer (CFO), attaches personal certification to covenant compliance: a named individual affirms, on the record, that the tests have been met. Second, the doctrine favours explicit board-level ownership of the bond relationship — a designated committee or director responsible for covenant oversight, investor reporting, and trustee liaison — so that the obligation has an owner rather than diffusing into general management. Third, the offering and the trust deed should make clear the directors’ duties in respect of the instrument: use of proceeds, accuracy of disclosure, and the duty to inform the trustee of deterioration promptly rather than to manage it quietly.

The deeper principle is alignment. The doctrine asks not only whether the board is accountable but whether its interests are aligned with the bondholders’: whether the distribution lock of Article 3 prevents the board from paying equity out of the bondholders’ cushion; whether related-party arrangements are disclosed and controlled; whether the people who control the asset gain when the bond is honoured and lose when it is not. Accountability without alignment is a signature on a certificate; accountability with alignment is a board that protects the instrument because protecting it is in everyone’s interest.

Use-of-Proceeds Governance

There is a moment of maximum vulnerability in any bond’s life: the moment the issuer receives the money. The investor has paid; the asset — especially in a development or expansion issuance — may not yet exist. Use-of-proceeds governance is the doctrine’s control over that gap, and it matters most precisely for the appreciating assets BEDROCK™ favours, many of which are built or expanded with the proceeds themselves.

The doctrine’s tools are escrow and milestones. Proceeds raised for construction or expansion should not flow to the issuer in a lump sum to be spent on trust; they should sit in a trustee-controlled account and be released against verified milestones — certified construction progress, independent confirmation that each tranche has produced the value it was meant to. This protects bondholders from the two classic development failures: proceeds diverted to other uses, and proceeds consumed by a project that stalls half-built. Ring-fencing completes the control: proceeds dedicated to the financed asset, segregated from the issuer’s general cash, so that the money raised against a specific appreciating asset actually builds that asset. Use-of-proceeds governance is how the offering document’s promises about the asset become contractual realities about the cash.

The Conflicts Discipline

Running through all four domains is a single concern that deserves its own statement: the management of conflicts and related-party dealings within the issuer’s group. The Caribbean’s corporate landscape is dominated by family-held and closely-controlled enterprises — a strength in commitment and continuity, but a structure in which the same individuals may sit on multiple sides of a transaction: as owner, as director, as counterparty, as lessor of the very asset that backs the bond.

The doctrine does not treat this as disqualifying — to do so would exclude much of the regional economy — but it treats it as something that must be surfaced and structured. Related-party arrangements that touch the backing asset or its cash flows must be disclosed fully (Pillar D), conducted on arm’s-length terms, and governed by independent decision-making where the conflict is material. The trust deed should constrain the issuer’s freedom to enter new related-party transactions that could impair the bondholders’ position, and the board’s independent members — or the trustee — should have a defined role where a conflict bites. The principle is simple: bondholders should never be exposed to a transaction whose terms were set by someone on both sides of it without independent scrutiny.

Governance is the pillar issuers are most tempted to treat as paperwork. The doctrine treats it as part of the security package — machinery as load-bearing as the charge over the asset.

The Oversight Architecture, at a Glance

The Oversight doctrine assembles into an architecture in which each actor guards against a specific failure — and no single party is asked to protect itself:

| Oversight Actor | Role | Failure It Prevents |

| Security trustee | Holds charges, assignments, and pledges in trust for all bondholders | Disorderly, competing enforcement by dispersed investors |

| Bond trustee | Monitors compliance, receives certificates, convenes and acts for bondholders | A passive investor base unable to detect or respond to breach |

| Securities regulator | Enforces offering and continuing-disclosure law (FSC or equivalent) | Inadequate or misleading disclosure to the market |

| Exchange (if listed) | Enforces listing rules, reporting, and governance standards | Erosion of disclosure discipline over the bond’s life |

| Board / CFO | Certifies compliance personally; owns the bond relationship | Covenants treated as the company’s problem, owned by no one |

| Escrow / milestone control | Releases proceeds against verified progress | Proceeds diverted or consumed by a stalled project |

| Independent directors | Scrutinise related-party dealings affecting the bond | Self-dealing on both sides of a transaction |

The architecture’s logic is redundancy: trustee, regulator, exchange, board, and escrow each guard a different failure, and the failure of any one is caught by another. This is also why governance maturity is one of the dimensions the BEDROCK™ Bond Readiness Index assesses — and why issuers with sound assets but thin governance frequently route first to Advisory, to build the board structures, trustee relationships, and related-party controls an institutional issue requires, before coming to market.

Defined Terms

Pillar O adds three terms to the series vocabulary:

Trustee architecture. The arrangement by which an independent, empowered security trustee holds the bond’s security and an independent bond trustee monitors and enforces compliance on behalf of all bondholders — converting a dispersed, passive investor base into a coherent, enforceable creditor.

Use-of-proceeds governance. The control regime — trustee-held escrow, milestone-based release, and ring-fencing — ensuring that bond proceeds build or acquire the specific appreciating asset they were raised against, rather than being diverted or consumed by a stalled project.

Conflicts discipline. The requirement that related-party arrangements touching the backing asset or its cash flows be disclosed, conducted at arm’s length, and subjected to independent scrutiny — so that bondholders are never exposed to terms set by a party on both sides of a transaction.

The Pillar in One Question

Oversight’s governing question is the one a bondholder asks when trust runs out: is there independent, empowered machinery that enforces the bargain between issuer and investor for the full tenor? Answered honestly — with a real trustee, full regulatory alignment, personal board accountability, governed use of proceeds, and a disciplined approach to conflicts — that question turns the instrument from a set of promises the investor must trust into a set of obligations the investor can rely on others to enforce. Governance, properly built, is not the cost of issuing a bond; it is part of what makes the bond worth buying.

Five pillars now stand: an appreciating asset, soundly engineered, fully disclosed, stress-proofed, and independently governed. The instrument is complete — but it is not yet capital. It must still reach the investors built to hold it, through the right route, into the right hands, in a market deep enough to receive it. Connecting the instrument to the capital is the work of the next pillar, and it is next week’s subject: Article 7, Capital Pathways: Connecting Issuers to Institutional Demand.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning — including the board, trustee and governance build-out that brings an issuer to institutional standard. Enquiries: [email protected].

Next in the series: Article 7 — Capital Pathways: Connecting Issuers to Institutional Demand. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ — The Dawgen Asset-Anchored Bond Framework is a proprietary framework of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210