Pillar R of the BEDROCK™ Framework: catastrophe risk, insurance integration, currency exposure, and tourism-cycle sensitivity — engineered as first-order structure, not afterthought

This is the pillar that makes BEDROCK™ a Caribbean framework rather than a developed-market template with a tan. Backing, Engineering, and Disclosure are universal disciplines — a bond structured to those three pillars would be sound in London or Toronto. Resilience is where the doctrine confronts the specific risk geography of the region it serves: a place where a single September afternoon can do more damage to an asset than a decade of ordinary business risk, where revenues arrive in one currency and debt is too often denominated in another, and where the dominant industry moves in cycles that no issuer controls.

Article 4 closed on the boundary of disclosure: there is a category of risk that transparency can describe but cannot dissolve. Naming the hurricane in the offering document does not move the hurricane. The Caribbean risks — catastrophe, currency, and cycle — must be disclosed honestly, but disclosure is necessary, not sufficient. They must be engineered against. Pillar R — Resilience — is the doctrine of that engineering, and its governing principle is uncompromising: in the Caribbean, resilience is a first-order structural feature, designed into the instrument from the term sheet, never an afterthought bolted on when the forecast turns.

This article sets out the Resilience doctrine across its three risk domains — catastrophe, currency, and cycle — and the scenario-testing standard that binds them together: the set of stress cases every BEDROCK™ instrument must survive on paper before it is offered. It closes where the hardest cases lead: the issuers whose existing structures cannot survive these stresses, and the restructuring work that must precede their return to the market.

Catastrophe Risk: Engineering for the Storm

The Caribbean sits in one of the world’s most active hurricane corridors, astride seismic faults, exposed to flood and storm surge. For an asset-anchored bond — whose entire premise is that the backing asset endures and appreciates — catastrophe is the existential risk: the single event that can impair the collateral, interrupt the cash flow, and trigger every covenant at once. The doctrine’s response is a layered architecture, because no single defence is sufficient.

Insurance as Structural Collateral

The first layer is insurance, treated not as an operating expense but as part of the security package — the assignment of insurances introduced in Article 3’s security perimeter. The doctrine’s requirements are specific: catastrophe cover (windstorm, earthquake, flood) sized to the full reinstatement value of the backing asset, not its book value; business-interruption cover sized to carry debt service through a realistic restoration period; proceeds assigned to the security trustee so that an insurance payout flows to restoring the collateral or repaying the bond, never into general corporate use; and — the discipline issuers most often neglect — verified insurer quality, because catastrophe cover written by an under-capitalised carrier is a promise that fails in exactly the correlated event it was bought for.

Parametric Cover for Speed

Traditional indemnity insurance pays after loss adjustment — a process that can take many months precisely when liquidity is most needed. The doctrine therefore favours pairing indemnity cover with parametric cover: insurance that pays a pre-agreed sum on a measured trigger (a hurricane of defined category within a defined radius, a quake of defined magnitude), without waiting for loss assessment. Parametric proceeds arrive in days, bridging the cash-flow gap while indemnity claims are settled. The two instruments are complementary, not alternative: parametric for speed, indemnity for completeness.

Physical and Reserve Resilience

Insurance transfers risk; it does not prevent damage. The doctrine’s third layer addresses the asset itself: backing assets should meet or exceed current hurricane and seismic building standards, with adaptation features (elevation against surge, hardened roofing and glazing, backup power and water) treated as value-protecting capital expenditure rather than discretionary cost — and funded, where material, through the capital expenditure (capex) reserve of Article 3. The debt service reserve completes the architecture: when the storm comes, funded reserves buy the weeks of time that turn a catastrophe into a managed interruption.

Currency Risk: Matching Money to Money

The second Caribbean risk is quieter than the hurricane but has impaired more regional credits: the mismatch between the currency an asset earns and the currency its debt demands. A foreign-exchange (FX) mismatch arises when an issuer earns revenue in one currency — often a local currency, sometimes US dollars from tourism — but services debt in another. A local-currency depreciation can then inflate debt service in real terms even as the business performs exactly to plan, turning a currency-market event into a credit event the asset never caused.

The doctrine’s headline rule, stated first in Article 3’s coupon section, is now elevated to a Resilience principle: debt service currency should follow revenue currency. The application runs in three cases.

- Natural matching first — issue the bond in the same currency the asset earns. A resort earning predominantly US dollars can prudently service US-dollar debt; a logistics asset earning local currency should, by default, issue in local currency. This is the cleanest resilience — the mismatch never exists.

- Engineered hedging second — where issuance must occur in a currency different from the dominant revenue — because that is where the institutional demand or the tenor is — the residual exposure must be hedged through the instrument’s life, with the hedge cost priced into the structure at issuance and the hedge counterparty’s quality assessed as rigorously as the insurer’s.

- Structural absorption third — where neither natural matching nor durable hedging is achievable, the structure must carry the exposure explicitly: a lower issuance loan-to-value (LTV), a higher debt service coverage ratio (DSCR) requirement, and an FX reserve, so that the instrument can absorb a defined depreciation without breaching. An unhedgeable mismatch is not necessarily disqualifying — but it must be paid for in structure, never ignored.

The doctrine’s discipline is captured in a single test from Article 3: hard-currency debt against local-currency income, unhedged and unreserved, is a stress test failed at the term sheet. Currency resilience is not a treasury refinement added later; it is a structural decision made before the bond is offered.

Cycle Risk: Designing for the Trough

The third risk is the one issuers most often wish away: the cycle. Tourism, the region’s signature industry and the source of much of its appreciating real estate, is cyclical and shock-prone — sensitive to global demand, to events in source markets, and to disruptions that arrive without warning. Commodity, construction, and trade cycles move the region’s other asset classes. An asset-anchored bond underwritten on average or peak performance is a bond underwritten for a year that may not recur on schedule.

The Resilience doctrine’s answer is to underwrite the trough, not the average. Three disciplines follow. First, debt service coverage must be tested against a realistic downturn scenario — a defined decline in occupancy, rate, or volume sustained for a defined period — and the structure sized so that coverage holds, with reserve support, through that trough. Second, the reserve stack should be calibrated to cycle length: a debt service reserve that covers a normal interruption may be too thin for a structural downturn, and counter-cyclical reserve building — sweeping surplus into reserves during peak years — prepares the instrument for the trough it knows will come. Third, covenants should breathe with the cycle: maintenance tests set with genuine headroom above trough performance, and springing protections (the cash sweep, the distribution lock of Article 3) that engage automatically when a downturn arrives, conserving cash inside the structure precisely when the temptation to distribute it is greatest.

A bond underwritten on average performance is underwritten for a year that may not recur on schedule. The Resilience doctrine underwrites the trough — and engineers the instrument to survive it.

The Scenario-Testing Standard

The three risk domains converge in a single discipline: before a BEDROCK™ instrument is offered, it must be shown to survive a defined set of stress scenarios on paper. This is the scenario-testing standard — the Resilience pillar’s equivalent of the appreciation evidence standard in Backing. It is not a sensitivity table buried in an appendix; it is a structural gate the instrument must pass.

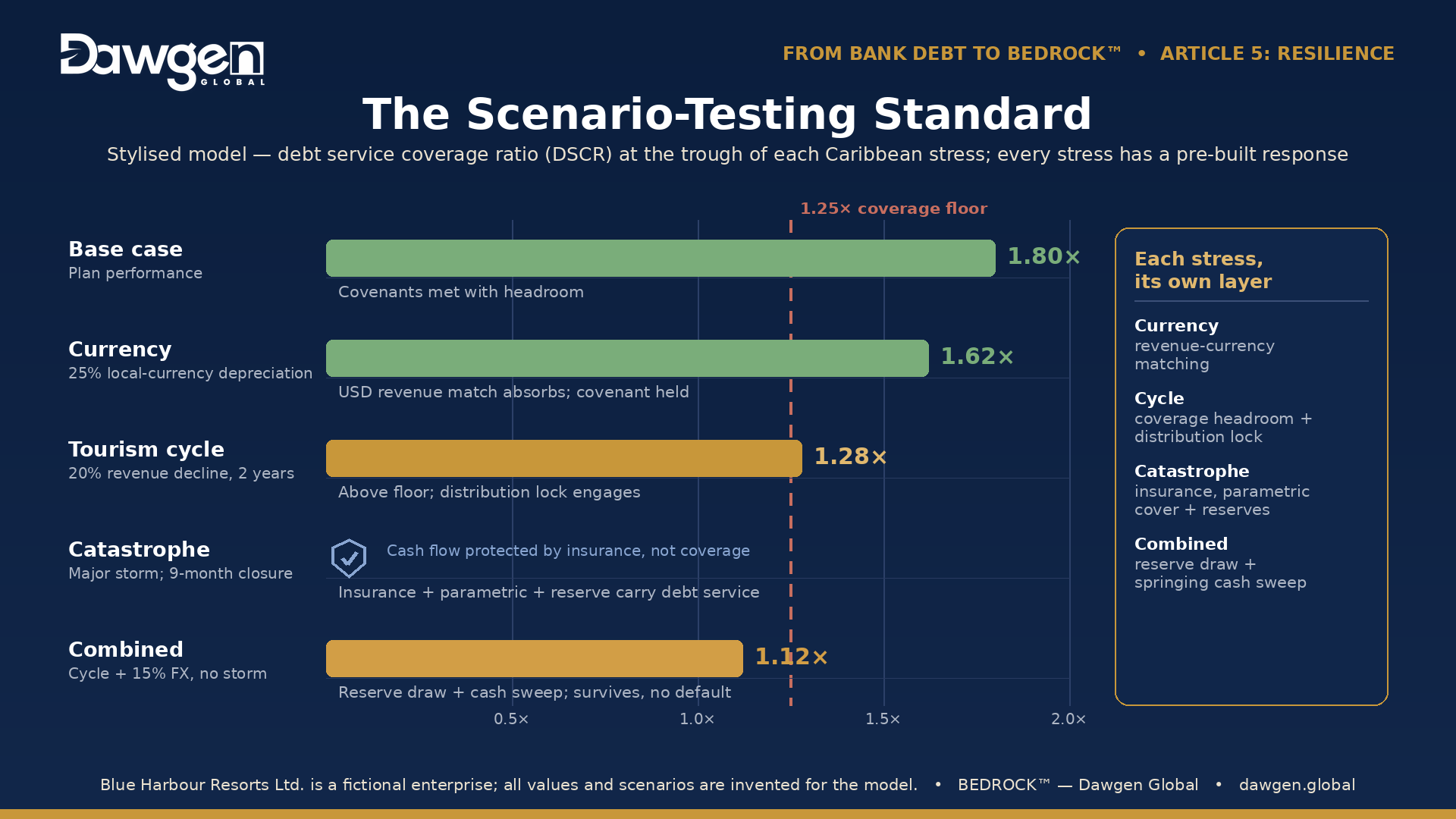

Return to Blue Harbour Resorts Ltd., the stylised hospitality issuer of the earlier articles — the US$40 million senior secured bond against an US$80 million beachfront property, with a six-month debt service reserve, assigned catastrophe insurance, and base-case DSCR of 1.8×. The scenario standard subjects it to the three Caribbean stresses, individually and in a combined case:

| Scenario | Stress applied | DSCR at trough | Outcome |

| Base case | Plan performance | 1.80× | Covenants met with headroom |

| Catastrophe | Major storm; 9-month closure | Insurance + reserve | BI cover + parametric carry debt service; restored |

| Currency | 25% local-currency depreciation | 1.62× | USD revenue match absorbs; covenant held |

| Tourism cycle | 20% revenue decline, 2 years | 1.28× | Above 1.25× floor; distribution lock engages |

| Combined | Cycle + 15% FX, no storm | 1.12× | Reserve draw; cash sweep on; survives, no default |

Read the table as the doctrine’s promise tested. No single stress breaks the instrument; each is absorbed by the layer designed for it — insurance and reserves for the storm, revenue-currency matching for the depreciation, coverage headroom and the distribution lock for the cycle. The combined case is deliberately severe — a multi-year downturn compounded by a currency shock — and it presses coverage close to the bone, drawing on reserves and triggering the cash sweep, yet the instrument survives without default. That is what stress-engineering means: not a structure that cannot be stressed, but one whose every plausible stress has a pre-built response. An instrument that passes this gate is resilient by design; one that cannot should be restructured, resized, or declined before it reaches an investor.

Blue Harbour Resorts Ltd. is a fictional enterprise created for illustrative purposes. All values, ratios, and scenarios are invented for the model, are not a forecast or recommendation, and do not reference any actual company, property, or engagement.

When the Structure Cannot Survive the Stress

The scenario-testing standard is a gate, and gates exclude. Some Caribbean issuers will run their existing structures through these scenarios and find that they fail — not because the asset is unsound, but because the financing around it was never engineered for the region’s risks. The common pattern is familiar from Article 3: short-tenor bank debt that must be refinanced in the middle of a downturn; catastrophe cover sized to book value rather than reinstatement, or written by a weak carrier; an FX mismatch carried nakedly because no one priced the alternative; reserves that exist on the balance sheet only as a hope. Such a structure does not survive the combined scenario — and the honest conclusion is that it must be repaired before it can be anchored.

This is again the interface with TRANSCEND™, Dawgen Global’s restructuring framework, and here the resilience dimension is explicit. The repair work is itself resilience engineering: refinancing mismatched debt into tenor that survives a cycle; rebuilding the insurance programme to reinstatement-value, trustee-assigned, well-rated cover; restructuring currency exposure through natural matching or durable hedging; and funding the reserve stack that converts paper resilience into real time. The sequence holds as it has throughout the series: TRANSCEND™ repairs the balance sheet so it can withstand the Caribbean’s stresses; BEDROCK™ then funds the growth on a foundation engineered to endure them. To attempt the second without the first is to issue an instrument that passes in fair weather and fails in the only weather the Caribbean reliably provides.

Defined Terms

Pillar R adds four terms to the series vocabulary:

Scenario-testing standard. The Resilience requirement that an asset-anchored bond demonstrate, before issuance, that it survives a defined set of stress scenarios — catastrophe, currency, and cycle, individually and combined — on paper. A structural gate, not an appendix.

Parametric cover. Catastrophe insurance that pays a pre-agreed sum on a measured trigger (storm category, quake magnitude) without loss adjustment — providing liquidity in days to bridge the gap while indemnity claims settle. Paired with indemnity cover: parametric for speed, indemnity for completeness.

Foreign-exchange (FX) mismatch. The condition in which an issuer earns revenue in one currency but services debt in another, so that a currency-market move can become a credit event the asset never caused. Resolved by natural matching, engineered hedging, or explicit structural absorption — never ignored.

Counter-cyclical reserve building. The practice of sweeping surplus cash into reserves during peak years so that the instrument is provisioned for the trough — calibrating the reserve stack to cycle length rather than to a single year’s interruption.

The Pillar in One Question

Resilience’s governing question is the one the Caribbean asks of every structure built within it: has the instrument been engineered to survive the region’s specific stress geography — storm, shock, and cycle? Answered honestly — with insurance treated as structural collateral, currency matched to revenue, coverage underwritten to the trough, reserves funded against the bad year, and the whole structure proven against a combined-stress scenario before issuance — that question turns the Caribbean’s risks from reasons not to lend into engineering problems with engineered solutions. That is the difference between an instrument that merely exists in the Caribbean and one built for it.

A resilient instrument, well-disclosed and soundly engineered against an appreciating asset, is now nearly complete. What remains is the machinery that enforces every promise it makes — the trustee who holds the security, the regulator whose rules it must satisfy, the board accountable for its obligations across fifteen years. That governance architecture is Pillar O, and it is next week’s subject: Article 6, Oversight: The Governance Machinery of Investor Protection.

Dawgen Global’s Corporate Finance, Advisory and Restructuring teams work with Caribbean issuers on capital structure design, bond readiness and balance sheet repositioning — including TRANSCEND™-led restructuring to engineer resilience into structures that cannot yet withstand the region’s risks. Enquiries: [email protected].

Next in the series: Article 6 — Oversight: The Governance Machinery of Investor Protection. Caribbean Boardroom Perspectives publishes Thursdays; companion editions appear in The Caribbean Advisory Brief on Saturdays.

BEDROCK™ and TRANSCEND™ are proprietary frameworks of Dawgen Global. © 2026 Dawgen Global. All rights reserved. dawgen.global

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210