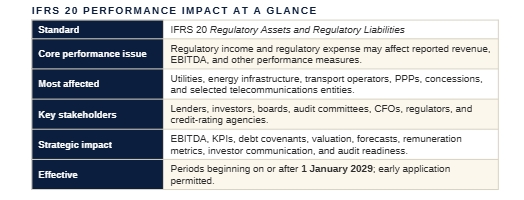

| Executive Summary

IFRS 20, Regulatory Assets and Regulatory Liabilities, will not merely change technical accounting for rate-regulated entities. It may also change how performance is measured, interpreted, financed, and communicated. For many regulated companies, IFRS 20 may affect reported revenue, operating profit, EBITDA, funds from operations, working capital, leverage ratios, interest cover, return measures, and debt-covenant calculations — because the standard requires companies within scope to recognise regulatory income and regulatory expense arising from differences in timing between when regulatory goods or services are supplied and when compensation is charged to, or deducted from, customers through regulated rates. The impact matters most for utilities, energy infrastructure, airports, seaports, transport operators, PPP entities, concession operators, and selected telecommunications businesses — entities that are capital-intensive, debt-funded, and closely watched by lenders, regulators, investors, boards, and rating agencies. IFRS 20 may improve transparency, but it may also introduce volatility, complexity, and comparability challenges in commonly used performance measures. Boards, CFOs, audit committees, lenders, and investors should begin assessing the implications now. Although the standard is effective for periods beginning on or after 1 January 2029, covenant analysis, stakeholder education, financial modelling, and communication planning should begin well before transition. Dawgen Global can assist with performance impact assessments, EBITDA and KPI analysis, covenant reviews, lender and investor communication, audit committee briefings, systems readiness, and implementation planning. |

1 IFRS 20 Is Also a Performance Reporting Issue

When a new accounting standard is issued, many organisations initially treat it as a financial reporting compliance project. That approach is too narrow for IFRS 20. For rate-regulated companies, the standard can affect some of the most closely watched numbers in the financial statements — revenue, operating profit, EBITDA, assets, liabilities, equity, working capital, leverage, interest cover, and funds from operations.

These measures are not merely accounting outputs. They influence board decisions, lender confidence, credit ratings, valuation discussions, management remuneration, investor messaging, tariff negotiations, and public accountability.

IFRS 20 should be viewed as a strategic reporting and stakeholder-communication issue, not simply a technical accounting exercise. Companies that prepare early will avoid covenant surprises and preserve confidence during transition.

2 Why EBITDA Matters So Much

EBITDA — earnings before interest, tax, depreciation, and amortisation — is widely used as a measure of operating performance and cash-generating capacity. Although it is not defined by IFRS Accounting Standards, it is relied on by lenders, investors, boards, rating agencies, valuation professionals, management teams, and analysts.

For regulated entities EBITDA is especially important, because many are capital-intensive and heavily debt-financed. Utilities, airports, ports, toll roads, energy infrastructure, and concession entities often use long-term borrowings to fund infrastructure assets, so lenders focus closely on recurring earnings, cash-flow visibility, and the stability of regulated returns.

IFRS 20 may affect EBITDA because regulatory income and regulatory expense are generally presented as revenue in profit or loss. If EBITDA is built up from revenue and operating profit, these new amounts may influence the measure — even though the underlying cash economics have not changed. The reported performance measure may move, and stakeholders must understand why.

3 How IFRS 20 Can Affect Reported Revenue and EBITDA

IFRS 20 supplements IFRS 15, Revenue from Contracts with Customers. IFRS 15 revenue generally reflects amounts charged to customers for goods or services supplied during the period; IFRS 20 addresses the additional effects of rate regulation where there is a difference in timing between compensation earned and amounts charged to customers.

A regulatory asset may arise when a company supplies regulated goods or services in the current period but will recover the related compensation through future regulated rates, producing regulatory income. A regulatory liability may arise when a company has charged customers amounts relating to another period, or must reduce future rates because it has already recovered more than it is entitled to retain, producing regulatory expense. Because both are generally classified as revenue, EBITDA may move in either direction.

| Effect on EBITDA | When it arises |

| Regulatory income — may increase EBITDA | Where current-period costs or compensation are recoverable through future regulated rates. |

| Regulatory expense — may decrease EBITDA | Where current billings include amounts relating to prior periods, or where future rate reductions are required. |

| Regulatory interest | May increase or decrease regulatory income or expense, depending on the terms of the regulatory agreement. |

| Recovery / fulfilment of prior balances | May change reported performance trends across periods as regulatory assets and liabilities unwind. |

This makes EBITDA analysis more informative — but also more complex.

4 Cash Collections Are Not the Same as IFRS 20 Performance

One of the most important messages for stakeholders is that IFRS 20 does not necessarily change the cash collected from customers in the current period. It changes how the effects of regulatory timing differences are recognised in the financial statements.

A company may report higher revenue and EBITDA because it has recognised regulatory income, even though the related cash will be recovered through future rates. Equally, a company may collect cash in the current period but recognise regulatory expense, because part of that cash relates to another period or must be returned through future rate reductions. Without careful explanation, users may wrongly assume that higher EBITDA means stronger current cash generation, or that lower EBITDA means weaker operations.

MANAGEMENT COMMENTARY SHOULD EXPLAIN

| • IFRS 15 revenue from customer billings

• Regulatory income and expense recognised in the period • Major drivers of regulatory asset and liability origination |

• Expected recovery or fulfilment periods

• Whether the effect is cash or non-cash this period • How the movement affects future tariffs and cash flows |

5 EBITDA Volatility: Real Change or Timing Effect?

IFRS 20 may introduce new forms of volatility into reported revenue and EBITDA — some of which reflects timing differences created by regulatory agreements rather than any change in underlying operations.

For example, a regulated electricity utility may incur significant storm-restoration costs in one year. If those costs are recoverable through future tariffs, regulatory income may increase EBITDA in the year the costs are incurred; in later years, as the company recovers the amount through customer rates, the regulatory asset reduces, changing the pattern of reported performance. Conversely, if a company over-recovers fuel costs in a year of falling fuel prices and must reduce future tariffs, regulatory expense may reduce EBITDA in the current period even though cash was collected. Stakeholders should therefore distinguish between:

| • Operational volatility

• Regulatory timing volatility • Tariff-driven volatility • Demand-driven volatility |

• One-off regulatory decisions

• Recurring regulatory mechanisms • Cash volatility vs. accounting volatility |

6 Why Lenders Should Pay Attention

Lenders should pay close attention because many loan agreements rely on IFRS-based performance measures. A borrower may have covenants based on EBITDA, debt-to-EBITDA, interest cover, debt-service coverage, current ratio, leverage ratio, tangible net worth, net debt-to-equity, or funds from operations to debt.

IFRS 20 can affect several of these. Even if cash flows do not change, the accounting numbers used in covenant calculations may: regulatory income may increase EBITDA and improve a debt-to-EBITDA ratio; regulatory expense may reduce EBITDA and worsen it; regulatory assets may raise total assets and affect leverage; regulatory liabilities may affect working capital and net worth. The risk is that covenant outcomes shift because of accounting transition rather than economic change. Lenders and borrowers should review financing documents early for:

| • Frozen-GAAP clauses

• Accounting-change provisions • Covenant reset mechanisms • Definitions of EBITDA and revenue |

• Treatment of non-cash regulatory income or expense

• Exclusions for regulatory assets and liabilities • Lender notification requirements for accounting changes • Renegotiation provisions and lender consent requirements |

7 Why Investors Should Pay Attention

Investors will need to understand how IFRS 20 affects reported performance and valuation. For rate-regulated companies, it may provide better information about future cash-flow prospects, because regulatory assets and liabilities show the financial effects of future recovery or future rate reductions — but these amounts must be interpreted carefully. Key investor questions include:

- Does regulatory income represent future recoverable cash flows, and how long will recovery take?

- Is recovery enforceable under the regulatory agreement, and what demand or credit risks affect it?

- Does regulatory expense indicate future tariff reductions?

- Are regulatory balances recurring or unusual?

- How does IFRS 20 affect EBITDA and valuation multiples, and should regulatory income be treated as operating performance?

- Are regulatory assets equivalent to cash or receivables, and how should regulatory liabilities affect enterprise value?

Investors should avoid simplistic interpretations. A higher post-IFRS 20 EBITDA figure may not mean stronger immediate cash generation; a lower figure may not mean weaker operating quality.

8 Why Boards and Audit Committees Should Pay Attention

Boards and audit committees must understand IFRS 20 because it affects governance, performance monitoring, risk oversight, and stakeholder communication. Boards should ask whether management has assessed the effect on board reporting packs, management accounts, budgets and forecasts, strategic plans, remuneration metrics, dividend policy, investor presentations, financing agreements, regulatory submissions, audit committee papers, risk registers, and internal controls.

Audit committees should focus particularly on judgement and audit evidence. IFRS 20 may involve significant estimates — future cash flows, recovery timing, regulatory interest, demand risk, credit risk, and enforceability — and the committee should also consider how the company will explain IFRS 20 effects in management commentary and disclosures.

9 Impact on Management Remuneration and Incentive Plans

Remuneration plans often rely on performance indicators such as revenue growth, EBITDA, operating profit, return on assets, return on equity, funds from operations, and cash-flow measures. IFRS 20 may affect these metrics, so that — if plans are not updated — management compensation could be influenced by accounting changes rather than actual operational performance. Regulatory income could increase EBITDA in a way not anticipated when targets were set; regulatory expense could reduce EBITDA and affect bonuses even where operations remain strong. Companies should review incentive arrangements to determine whether:

| • Targets need recalibration

• IFRS 20 effects should be included or excluded • Non-cash regulatory income or expense should be adjusted |

• Measures should be pre- or post-IFRS 20

• Remuneration committees need guidance • Disclosures are required to explain changes |

10 Impact on Budgets, Forecasts and Financial Models

IFRS 20 will require changes to budgeting and forecasting models. Companies will need to forecast not only customer billings and IFRS 15 revenue, but also the regulatory components that drive reported performance. Capital-intensive regulated companies often prepare multi-year forecasts for lenders, investors, regulators, and boards, and IFRS 20 may require those models to be redesigned — with finance working closely with regulatory affairs, legal, treasury, operations, and strategy to keep assumptions consistent. Models may need to capture:

| • Regulatory income and regulatory expense

• Regulatory asset origination and recovery • Regulatory liability origination and fulfilment • Regulatory interest income and expense |

• Expected future tariff adjustments

• Timing of recovery and fulfilment • Demand risk and credit risk • Alternative regulatory outcomes |

11 Impact on Valuation and Transaction Due Diligence

IFRS 20 may become an important due-diligence topic in transactions involving regulated entities — acquisitions, disposals, financing, concessions, PPPs, or listings — where buyers and investors must understand regulatory balances and their impact on future cash flows. A regulatory asset may be valuable where recovery is enforceable and likely; a regulatory liability may reduce future revenue or customer charges. Both must be understood before valuation conclusions are reached. Due diligence should consider:

| • The nature of regulatory assets and liabilities

• Enforceability of recovery rights and reduction obligations • Expected recovery or fulfilment period • Consistency with regulatory filings • Historical pattern of regulator decisions • Regulatory interest |

• Impact on EBITDA and enterprise-value multiples

• Impact on free-cash-flow forecasts • Whether balances are recurring or one-off • Sensitivity to demand or tariff changes • Treatment in purchase-price negotiations |

12 Non-GAAP and Alternative Performance Measures

Many regulated companies already use non-GAAP or alternative performance measures — adjusted EBITDA, adjusted operating profit, funds from operations, regulatory EBITDA, or management-defined measures — to explain the effects of rate regulation. IFRS 20 may reduce the need for some adjustments, since some regulatory timing effects will now be recognised in the financial statements. But it may also create new reasons to use alternative measures, particularly to distinguish:

| • IFRS 15 customer revenue from regulatory income or expense

• Cash earnings from non-cash regulatory timing effects • Recurring operating performance from exceptional regulatory adjustments |

• Recognised regulatory balances from unrecognised regulatory effects

• Tariff-driven performance from operational performance |

Any alternative performance measures should remain transparent, balanced, and clearly reconciled to IFRS measures.

13 Caribbean Implications: Why This Matters Regionally

For Caribbean regulated entities, IFRS 20’s impact on EBITDA, covenants, and investor communication may be especially important. Many regional utilities and infrastructure entities face high capital-expenditure needs, debt-funded infrastructure programmes, climate-resilience investment, hurricane-recovery costs, fuel-price volatility, renewable-energy transition costs, water-infrastructure upgrades, port and airport expansion, PPP financing, government-approved tariff frameworks, and public sensitivity around rate increases.

These realities mean IFRS 20 may affect not only financial reporting but also financing strategy, public communication, tariff discussions, and investor confidence. A utility recovering hurricane-restoration costs through future tariffs may recognise regulatory income and a regulatory asset — lenders and investors will need to understand the effect on EBITDA, debt-service capacity, and future cash recovery. A company required to reduce future tariffs after an over-recovery may recognise regulatory expense and a regulatory liability — and boards and regulators will need to explain why reported performance has changed and how future tariffs will be affected.

14 Practical Steps for CFOs

CFOs should take a structured approach to IFRS 20 performance and covenant readiness.

- Identify all regulatory agreements and rate mechanisms.

- Determine whether regulatory income and expense may arise.

- Estimate the impact on revenue, EBITDA, operating profit, and funds from operations.

- Review key internal KPIs and board reporting measures.

- Review loan agreements and covenant definitions, and assess whether lender communication is required.

- Update budgeting and forecasting models.

- Review management incentive arrangements.

- Prepare investor and regulator communication plans.

- Engage auditors early on judgements, estimates, and disclosures.

- Develop reconciliations between pre- and post-IFRS 20 performance.

- Train finance, regulatory, treasury, and board teams.

Early planning will reduce implementation pressure and improve stakeholder confidence.

15 What Each Stakeholder Should Ask

The same standard raises different questions depending on the lens. The table below summarises the priorities for each stakeholder group.

| Stakeholder | Key questions |

| Lenders | Will IFRS 20 affect EBITDA, leverage, interest cover, or debt-service ratios? Do loan agreements contain frozen-GAAP or accounting-change clauses? Should covenant definitions be amended? Are regulatory income and expense cash or non-cash this period? What is the expected timing of recovery or fulfilment? |

| Investors | How does IFRS 20 change revenue and EBITDA trends? Which regulatory balances are recurring versus one-off? Are regulatory assets recoverable through enforceable future rates? How should regulatory liabilities affect valuation? How does IFRS 20 affect free-cash-flow forecasts? |

| Boards & audit committees | Has management quantified the expected performance impact? Are systems able to produce reliable IFRS 20 data? How will KPIs and remuneration metrics be affected? Have auditors and lenders been engaged early? Is there a clear communication plan for stakeholders? |

16 How Dawgen Global Can Help

Dawgen Global helps regulated entities understand and communicate the performance implications of IFRS 20. Our services include:

- IFRS 20 revenue and EBITDA impact assessments, and regulatory income and expense analysis.

- KPI and performance metric reviews, and debt-covenant impact assessments.

- Lender and investor communication support.

- Board and audit-committee briefings, and management-remuneration metric reviews.

- Budgeting and forecasting model updates.

- Transaction and valuation support.

- Non-GAAP and alternative performance measure reviews.

- IFRS 20 accounting policy development, and systems and data readiness assessments.

- Audit preparedness documentation, and disclosure and management commentary support.

We help clients move beyond compliance — translating IFRS 20 into practical insight for financing, governance, valuation, and stakeholder confidence.

17 Conclusion: More Than the Notes to the Accounts

IFRS 20 will change how rate-regulated companies report and explain performance. It may affect revenue, EBITDA, financial ratios, covenants, forecasts, valuations, remuneration metrics, and investor communication.

The standard does not necessarily change the cash collected in a period, but it may change how regulatory timing differences are reflected in financial performance — a distinction that lenders, investors, boards, regulators, and management teams must understand clearly. For affected entities, the best response is early preparation: assess the impact, update models, review covenants, educate stakeholders, and develop clear communication plans before transition.

Dawgen Global is ready to support regulated entities across the Caribbean and beyond with IFRS 20 readiness, performance impact analysis, covenant reviews, audit preparedness, and stakeholder communication.

| Ready for the EBITDA, covenant, and performance reporting impact of IFRS 20?

Dawgen Global can help you assess the implications, update your financial models, brief your board, communicate with lenders and investors, and prepare for implementation with confidence. Let’s have a conversation. Website: www.dawgen.global/contact-us Email: [email protected]

|

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements