| Executive Summary

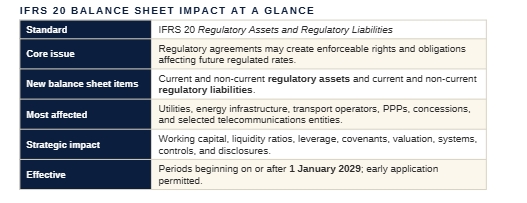

IFRS 20, Regulatory Assets and Regulatory Liabilities, changes how rate-regulated companies present their financial position. For entities within scope, the statement of financial position may now include regulatory assets and regulatory liabilities that reflect enforceable rights and obligations created by regulatory agreements. This is a significant development for utilities, energy-infrastructure companies, transport operators, PPP entities, concession operators, and selected telecommunications businesses — entities that operate under frameworks determining when costs are recovered from customers, when over-recoveries are returned, and how approved compensation is reflected in regulated rates. A regulatory asset may arise when a company has supplied regulated goods or services but will recover part of the related compensation through future regulated rates. A regulatory liability may arise when a company has charged customers amounts relating to another period, or must reduce future rates because it has already recovered more than it is entitled to retain. For companies that do not currently recognise regulatory balances, IFRS 20 may introduce new assets, liabilities, current and non-current classifications, disclosures, and financial ratios. For those already recognising such balances under previous policies or IFRS 14, IFRS 20 may still change the population, measurement, presentation, and disclosure of those balances. This article explains how IFRS 20 affects the balance sheet, why these items matter, the implications for financial metrics, and how Dawgen Global can help. |

1 Why the Balance Sheet Matters Under IFRS 20

The statement of financial position is more than a listing of assets and liabilities. It tells users what resources a company controls, what obligations it must settle, and how those resources and obligations may affect future cash flows.

For rate-regulated companies, the balance sheet has not always captured the full economic effects of regulation. A company may have held an enforceable right to recover approved costs through future tariffs without recognising it as an asset; equally, it may have had an obligation to reduce future rates after over-recovering from customers without recognising it as a liability.

IFRS 20 changes this. By requiring recognition of regulatory assets and regulatory liabilities where the criteria are met, the standard gives users a clearer picture of how regulatory agreements affect financial position and future cash flows.

This is not a cosmetic change. It can affect total assets, total liabilities, equity, working capital, liquidity, leverage, return measures, covenant calculations, and board-level performance reporting.

2 Regulatory Assets and Regulatory Liabilities Defined

The two new balance sheet items are mirror images of each other — one a right to recover, the other an obligation to give back. Both must be enforceable under the regulatory agreement; a management expectation of future recovery is not enough.

An enforceable right to add an amount to future regulated rates because the company has supplied regulated goods or services, or incurred allowable costs, for which it has not yet been compensated. It represents future economic benefit arising from the regulatory agreement — for example, storm-restoration costs a regulator allows to be recovered through tariffs over the next three years. |

An enforceable obligation to deduct an amount from future regulated rates, or otherwise reduce future charges to customers. It reflects amounts already recovered, or charged in the current period but relating to another period — for example, an over-recovery a regulator requires to be returned through lower future tariffs. |

EXAMPLES THAT MAY GIVE RISE TO A REGULATORY ASSET

| • Approved fuel cost under-recoveries

• Storm or disaster recovery costs • Approved pension cost recoveries • Grid modernisation costs recoverable through rates |

• Infrastructure repair costs recoverable through tariffs

• Performance incentives earned, recoverable later • Approved capital expenditure recoveries • Regulatory interest on recoverable balances |

EXAMPLES THAT MAY GIVE RISE TO A REGULATORY LIABILITY

| • Fuel cost over-recoveries

• Excess tariff collections • Customer rebate obligations • Future rate reductions required by the regulator |

• Penalties that reduce future recoverable amounts

• Performance adjustments owed to customers • Amounts billed in advance for future services • Over-recovery of approved operating costs |

3 How These Differ from Ordinary Receivables and Payables

A regulatory asset is not a trade receivable, and a regulatory liability is not a trade payable. The difference lies in how each is recovered or fulfilled — not by invoicing or paying a single counterparty, but through future regulated rates charged to the broad customer base. That indirect mechanism is what drives the measurement and disclosure complexity.

| Trade receivable / payable | Regulatory asset / liability | |

| Counterparty | A specific customer or supplier directly obligated. | The future customer base, via the regulator-approved tariff. |

| Settlement | Direct cash payment or receipt. | Recovered or fulfilled through higher or lower future regulated rates, credits, or tariff adjustments. |

| Key uncertainties | Credit risk of the counterparty. | Future demand, tariff approvals, regulatory decisions, recovery timing, and enforceability. |

| Implication | Relatively straightforward to measure. | Requires cash-flow estimation, judgement, and tailored disclosure. |

4 Why IFRS 20 May Significantly Change the Balance Sheet

For companies that do not currently recognise regulatory balances, IFRS 20 may introduce material new assets and liabilities — raising total assets, total liabilities, or, in many cases, both. Companies that already recognise regulatory balances may also see change, as IFRS 20 may alter which balances qualify, how they are measured, and how they are presented. The outcome depends on factors including:

| • The structure of the regulatory agreement

• Whether the company has under- or over-recoveries • Whether costs are recovered through future rates • Whether future rate reductions are required • The regulatory capital base |

• Whether regulatory depreciation creates timing differences

• The measurement of future cash flows • The discount or regulatory interest rate • Current vs. non-current classification |

5 Current and Non-Current Classification

IFRS 20 requires regulatory assets and liabilities to be presented as current or non-current, unless the company presents its statement of financial position in order of liquidity. The classification matters because it can affect working capital, liquidity ratios, and how management explains financial position.

A regulatory asset expected to be recovered through rates within 12 months may be current; one recovered over several years, non-current. Regulatory liabilities follow the same logic, depending on when they are expected to be fulfilled through future rate reductions or deductions. This requires reliable recovery and fulfilment schedules — and for capital-intensive entities, many regulatory balances will be long-term.

6 Measurement Using Cash-Flow-Based Techniques

IFRS 20 generally requires regulatory assets and liabilities to be measured using a cash-flow-based technique: estimating the future cash flows arising from each balance and discounting them at the regulatory interest rate specified or implied in the agreement, subject to the standard’s detailed requirements and available simplifications. This is a judgemental area requiring robust documentation, internal controls, and audit evidence. Measurement assumptions typically include:

| • Expected future tariff adjustments

• Expected demand or customer volumes • Timing of recovery or fulfilment • Regulatory interest income or expense • Demand risk |

• Credit risk

• Regulatory uncertainty • Enforceability of recovery rights • Expected future rate reductions • Changes in the regulatory framework |

7 Regulatory Capital Base and the Direct-Relationship Concept

One of the more technical areas of IFRS 20 concerns the regulatory capital base and regulatory depreciation. Some frameworks allow recovery of compensation through regulatory depreciation or a return on a regulatory capital base, but the relationship between that base and the company’s related assets varies by jurisdiction.

IFRS 20 includes requirements affecting whether certain regulatory assets or liabilities arising from regulatory depreciation are recognised — in some cases depending on whether there is a direct relationship between the regulatory capital base and related items. Companies should not assume that all regulatory capital base differences automatically create recognised balances. Areas to assess include regulatory capital base rules, asset registers, regulatory and accounting depreciation, tariff-determination methodologies, cost-recovery mechanisms, regulator decisions and rate orders, and differences between regulatory and accounting asset values.

8 How Balance Sheet Changes Affect Financial Ratios

Regulatory assets and liabilities can move ratios watched by boards, lenders, investors, rating agencies, and regulators. A current regulatory asset may improve working capital; a current regulatory liability may reduce it. Substantial non-current regulatory assets may raise total assets and dilute return on assets, while regulatory liabilities may affect leverage and debt-to-equity. Management should identify which ratios are used internally and externally, then assess how IFRS 20 may change them.

RATIOS POTENTIALLY AFFECTED

| • Current ratio and quick ratio

• Working capital • Debt-to-equity and net debt-to-equity • Debt-to-assets • Return on assets |

• Return on equity

• Asset turnover • Leverage ratios • Tangible net worth • Funds from operations to debt |

9 Debt Covenants and Financing Implications

Many regulated companies are capital-intensive and rely heavily on external financing — utilities, airports, seaports, toll roads, energy-infrastructure companies, and PPP entities often use long-term debt to fund infrastructure. Where loan agreements use IFRS-based metrics, regulatory assets and liabilities may affect covenant compliance. Even when IFRS 20 does not change cash flows, it may change reported assets, liabilities, revenue, EBITDA, and equity, so borrowers and lenders should consider whether agreements need clarification before the standard becomes effective.

COVENANT AND FINANCING TERMS TO REVIEW

| • Minimum net worth requirements

• Debt-to-equity and leverage ratios • Current ratio and interest coverage • EBITDA-based covenants • Tangible asset requirements • Debt-service coverage ratios |

• Frozen-GAAP clauses

• Accounting-change provisions and covenant resets • Definitions of EBITDA or net debt • Exclusions for regulatory assets or liabilities • Lender consent requirements • Reporting obligations on accounting changes |

Early lender communication will reduce the risk of misunderstanding.

10 Implications for Investors and Valuation

Investors and valuation professionals will need to understand how IFRS 20 affects reported financial position. Regulatory assets may represent future recoverable amounts, but they are not cash — their value depends on enforceability, future rates, customer demand, and the recovery period. Regulatory liabilities may reduce future revenue or tariffs without requiring direct cash settlement. For entities seeking financing, investment, acquisition, or listing, IFRS 20 may become a key due-diligence topic, raising questions such as:

- Whether regulatory assets and liabilities should be treated as operating items.

- How IFRS 20 affects EBITDA and enterprise-value multiples.

- How regulatory balances affect free-cash-flow forecasts.

- Whether future tariff recovery is reasonably assured.

- How timing differences and regulatory interest affect working capital and expected returns.

11 Implications for Caribbean Regulated Entities

The Caribbean context makes IFRS 20 particularly relevant. Many regional utilities and infrastructure operators face high capital-expenditure needs, fuel-cost volatility, climate-resilience requirements, hurricane-recovery costs, water-infrastructure challenges, renewable-energy transition costs, and public-service obligations — many of which may be recovered through regulated rates over time.

For boards and policymakers, IFRS 20 may improve transparency while requiring clearer communication about how current tariffs relate to past costs, future recoveries, over-recoveries, and long-term investment. For lenders and investors, it may provide more information about future cash-flow prospects, though it will require careful interpretation. Sectors most likely to be affected across the region include:

| • Electricity generation, transmission, and distribution

• Water and sewerage • Ports and airports • Toll roads and transport infrastructure • Renewable-energy infrastructure |

• Fuel-cost recovery arrangements

• Public-private partnership projects • State-owned commercial infrastructure • Regulated telecommunications and digital infrastructure |

12 Systems, Data and Control Requirements

Regulatory assets and liabilities cannot be reported reliably without appropriate systems and controls. This requires closer coordination across finance, regulatory affairs, operations, legal, tax, treasury, and internal audit — and should not wait until the year of adoption. A data-readiness and controls workstream should capture, for each balance:

| • The source of each regulatory asset or liability

• The relevant regulatory agreement • The period the timing difference originated • The expected recovery or fulfilment period • The future rates through which it will resolve • Regulatory interest |

• Movements during the period

• Opening-to-closing reconciliations • Maturity analysis • Unrecognised regulatory assets and liabilities • Assumptions and judgement approvals |

13 Disclosure Requirements: More Than Numbers

IFRS 20 requires disclosures that help users understand the financial effects of regulatory assets and liabilities — items that may be unfamiliar to some readers, so clear explanation is essential. Management should design disclosure templates early and align them with board reporting, audit-committee reporting, investor communication, and regulatory filings. Expected disclosures include:

| • Opening-to-closing reconciliations of regulatory balances

• Maturity analysis of expected recovery or fulfilment • Explanations of significant changes in the period • Information about regulatory income and expense |

• Information about unrecognised regulatory balances

• Judgements made in applying the standard • Uncertainties affecting recovery or fulfilment |

14 Questions Boards and CFOs Should Ask

Boards, CFOs, and audit committees should put the following on the early IFRS 20 readiness agenda.

- Do our regulatory agreements create enforceable rights to recover amounts through future rates?

- Do they create enforceable obligations to reduce future rates?

- What regulatory assets and liabilities may exist at the transition date?

- Are balances already tracked in regulatory reports, and are they suitable for IFRS reporting?

- How will we classify regulatory assets and liabilities as current or non-current?

- How will we estimate future recovery and fulfilment cash flows, and which assumptions need significant judgement?

- How will IFRS 20 affect working capital, leverage, liquidity, return measures, and covenants?

- Do our systems capture the data needed for reconciliations and maturity analysis?

- Have we discussed the expected impact with auditors, lenders, regulators, and investors?

15 How Dawgen Global Can Help

Dawgen Global assists regulated entities in understanding and implementing IFRS 20 from both a technical accounting and a practical business perspective. Our IFRS 20 balance sheet advisory services include:

- Regulatory asset and liability identification, and regulatory agreement and tariff framework reviews.

- Recognition and measurement assessments, and current / non-current classification analysis.

- Regulatory capital base and depreciation analysis.

- IFRS 20 balance sheet impact assessments.

- Working capital, liquidity, leverage, and covenant impact reviews.

- Accounting policy development, systems and data readiness reviews, and internal control design.

- Audit committee and board training, and auditor-ready technical position papers.

- Disclosure design and review.

- Investor, lender, and regulator communication support.

We help clients move from technical uncertainty to practical readiness — ensuring that IFRS 20 implementation supports transparent reporting, audit readiness, and stakeholder confidence.

16 Conclusion: A New Balance Sheet Discipline

IFRS 20 introduces a new balance sheet discipline for companies subject to rate regulation. Regulatory assets and liabilities will make the financial effects of regulated rates more visible, more comparable, and more decision-useful.

For affected companies, the implications may be significant: new assets and liabilities may appear, financial ratios may change, debt covenants may need review, systems may require enhancement, disclosures will become more detailed, and boards will need to understand the judgements involved. Those that prepare early will be best positioned to manage the transition, explain the impact, and use IFRS 20 as an opportunity to improve transparency.

Dawgen Global is ready to support regulated entities across the Caribbean and beyond with IFRS 20 readiness, implementation, audit preparedness, and stakeholder communication.

| Is your organisation ready for the balance sheet impact of IFRS 20?

Dawgen Global can help you identify regulatory assets and liabilities, assess financial statement implications, prepare your systems, train your teams, and communicate the impact with confidence. Let’s have a conversation. Website: www.dawgen.global/contact-us Email: [email protected]

|

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements