A Buy-Side Mandate with a Single Strategic Question

A well-run Caribbean beverage distributor had outgrown its home market. Its board knew the next chapter would require scale. What it did not yet know was which target, in which neighbouring jurisdiction, at which price, and on which terms would translate ambition into a consolidated business worth more than the sum of two separate companies. This Standard describes how a disciplined buy-side mandate answered those four questions in seventeen weeks.

1. The Signal

Across the Caribbean, the distribution sector is quietly being rewritten. Route density, warehousing economics, exclusive supplier relationships, and the cost of regulatory compliance all favour operators with scale. For owner-managed distributors that grew up serving a single-island market, the strategic question has shifted. It is no longer whether regional scale matters. It is whether scale will be built organically, acquired deliberately, or conceded to a more aggressive competitor who acts first.

The hypothetical subject of this Standard is a profitable family-controlled beverage distributor operating in one Caribbean jurisdiction, with annual revenues in the mid eight-figure range, a strong portfolio of exclusive brand agreements, and a board whose members had begun, individually and then collectively, to ask the same strategic question: if consolidation is coming, are we acquirers or are we targets?

The board chose to be acquirers. The mandate that followed was a disciplined buy-side advisory engagement anchored by MERIDIAN™, Dawgen Global’s M&A Value Architecture Model.

2. The Context

The acquirer’s situation was strong but time-bounded. Five conditions defined the engagement context.

An established home-market position

The acquirer held meaningful market share in its home jurisdiction, supported by long-standing relationships with international brand principals and a well-invested fleet and warehouse network. Organic growth in the home market was slowing. The brand principals were beginning, in conversations with the acquirer’s founder, to ask whether regional distribution might be consolidated.

A shareholder base approaching a natural transition point

Three generations of the founding family held the equity. The second-generation CEO had served for fifteen years. The third generation was professionally active in the business but had not yet taken executive responsibility. A strategic transaction was understood, across the family, as an opportunity to crystallise value, introduce institutional governance, and create a platform large enough to employ the next generation in roles of genuine substance.

A visible target universe in neighbouring jurisdictions

Two to three potential targets in neighbouring Caribbean jurisdictions had been informally identified by the acquirer’s management and by its international brand principals. None of these targets was publicly for sale. Each would require a carefully constructed approach, and in some cases a proprietary introduction through the brand-principal relationship.

A board prepared to commit but not to rush

The board had approved a buy-side engagement and allocated a transaction budget. It had also made clear that it would not pursue an acquisition that did not meet defined financial and strategic thresholds. The mandate was explicitly to examine the target universe with rigour, not to reach a pre-selected conclusion.

A financing environment requiring early attention

The board preferred a financing structure combining retained earnings, a regional bank facility, and a potential minority institutional co-investment. The engagement would need to run financing readiness in parallel with target identification, rather than sequentially.

3. The Approach

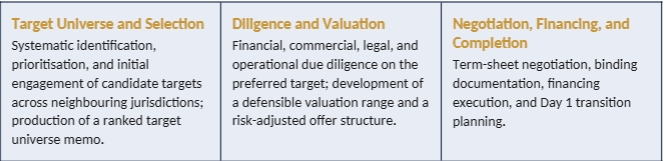

MERIDIAN™ structured the mandate across three sequenced phases, each with a go/no-go decision gate, and each designed to produce a specific governance-grade deliverable the board could use to make the next decision.

Each phase closed with a board paper that stated what had been concluded, what remained open, and what the board was being asked to decide. At every gate, the board retained the option to pause, redirect, or withdraw. This is the discipline of buy-side advisory: the acquirer’s strategic freedom is the client’s most valuable asset, and the engagement is designed to preserve it at every stage.

4. The Work

Phase One: Target universe and selection (weeks 1–5)

The first five weeks produced a structured target universe memo covering eleven candidate companies across three neighbouring Caribbean jurisdictions. Each candidate was profiled against a consistent framework: market position, portfolio overlap with the acquirer, financial scale, ownership structure, known willingness to consider transactions, and fit with the acquirer’s stated integration appetite.

Four candidates were deprioritised after this initial work — two because of portfolio conflicts with the acquirer’s existing brand principals, one because of governance complexity that would have required a multi-year cleanup before completion, and one because informal diligence suggested financial performance materially weaker than the candidate’s public posture. The remaining seven candidates were ranked, and the top three were approved by the board for proprietary approach.

Two of the top three candidates declined further engagement. The third — a mid-sized distributor in a neighbouring jurisdiction with a strongly complementary portfolio and an ageing owner-manager open to a succession conversation — agreed to a confidential exploratory discussion. That discussion progressed to a signed mutual non-disclosure agreement and a preliminary information exchange by the end of week five.

Phase Two: Diligence and valuation (weeks 6–11)

Six weeks of integrated diligence followed. Financial diligence tested reported EBITDA against normalisation adjustments for owner compensation, related-party transactions, inventory methodology, and non-recurring items. Commercial diligence mapped the target’s customer base by channel, verified the stability of its key supplier agreements, and assessed the realism of its forward volume projections. Legal diligence examined the target’s corporate structure, material contracts, regulatory permits, and potential litigation exposure. Operational diligence assessed the target’s warehouse, fleet, and systems capacity for post-completion integration.

The diligence work produced three important findings. First, normalised EBITDA was approximately twelve per cent below the target’s reported figure, primarily because of owner compensation adjustments and inventory methodology differences. Second, two of the target’s key supplier agreements contained change-of-control provisions that would require pre-completion consent and that introduced negotiating leverage for those suppliers. Third, the target’s warehouse capacity was adequate for the combined business for approximately eighteen months, after which a capacity investment would be required.

The valuation work produced a defensible range rather than a single number — a discounted cash flow value, a precedent-transaction multiple value, and a strategic-value uplift reflecting route density and procurement synergies. The range informed the offer structure: a headline price anchored to the mid-point, an earn-out element tied to the stability of key supplier agreements through the first eighteen months post-completion, and a retention package for the target’s senior operational team.

Phase Three: Negotiation, financing, and completion (weeks 12–17)

The final six weeks ran three workstreams in parallel. Term-sheet negotiation moved the headline price, the earn-out mechanics, and the completion conditions across five drafts before reaching a signed document. Financing execution confirmed the regional bank facility on acceptable covenants, with the minority institutional co-investor taking a smaller position than initially contemplated but on better terms. Day 1 transition planning produced an integration charter, a retention communication plan, and a one-hundred-day priorities document.

Completion occurred on the planned date. The combined business, on a pro forma basis, held materially greater scale in the acquirer’s supplier relationships and a substantially expanded regional footprint.

5. The Solution

The deliverable of a buy-side mandate is not a single document. It is a sequence of decisions, each captured in a governance-grade paper the board can defend to its shareholders, its lenders, its regulators, and eventually to history. The mandate produced eight such papers across seventeen weeks.

| Target Universe Memo

Ranked assessment of eleven candidates across three jurisdictions. |

Approach Strategy

Proprietary engagement design for the top three candidates. |

| Diligence Charter

Scope, workstreams, access protocols, and diligence gate criteria. |

Valuation Opinion

Defensible range supported by three methodologies and documented assumptions. |

| Offer Structure Memo

Headline price, earn-out mechanics, retention package, and completion conditions. |

Financing Paper

Facility structure, covenant package, and co-investment terms. |

| Day 1 Transition Plan

Integration charter, retention communications, and one-hundred-day priorities. |

Completion Report

Executed transaction documentation and post-completion governance handover. |

Each paper was signed by the engagement partner, reviewed by an independent partner, and presented to the board in a structured session. The board’s decision at each gate was minuted. Nothing relied on memory or informal understanding. This is the governance architecture that distinguishes a buy-side mandate from a transaction introduction.

6. The Effect

The transaction itself was the visible result. The deeper effects were three.

First, the acquirer’s board learned to operate at a different cadence. A family-controlled distributor accustomed to informal strategic conversation had navigated a seventeen-week engagement of board papers, signed decisions, and documented governance. The habits formed during the mandate now carry into its regular board cycle. Strategic choices are structured, papered, and recorded in a way they previously were not.

Second, the acquirer’s relationship with its international brand principals shifted. A distributor that had previously been one of several in the region was now the largest operator across its expanded footprint. Brand principals that had previously managed the relationship at a regional level now managed it at a head-office level. The commercial terms available to the acquirer reflected this shift.

Third, the third generation of the founding family gained an opportunity structure that had not previously existed. The combined business was large enough to support meaningful executive roles, group-level functions, and a professionalised governance architecture. What began as a transaction became, in practice, a platform.

7. The Transferable Lesson

Caribbean boards considering buy-side transactions often conflate two different engagements. The first is transaction introduction — a broker connects the acquirer to a willing seller. The second is buy-side advisory — a disciplined mandate that identifies the universe of possible targets, narrows the universe against the acquirer’s strategic criteria, conducts governance-grade diligence on the preferred target, constructs a defensible offer, negotiates documentation, and delivers Day 1 readiness.

The first engagement is faster and cheaper. The second produces decisions the board can defend. For Caribbean boards contemplating a move from single-jurisdiction operator to regional platform, the difference matters. The single most transferable lesson from this mandate is that buy-side advisory, properly structured, is not a cost of the transaction. It is the instrument by which the transaction’s quality is determined.

Take the next step with Dawgen Global

| THE SIGNAL

Your board has identified regional scale as the next strategic chapter, but the target universe is not yet defined and the diligence architecture is not yet built. THE OFFER A MERIDIAN™ buy-side advisory engagement, structured across three gated phases, delivers a ranked target universe, governance-grade diligence on the preferred target, a defensible offer structure, and Day 1 readiness — typically within sixteen to twenty weeks. THE CHANNEL Email [email protected]

|

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements