In the pursuit of maximizing shareholder value, many companies lean heavily on tools like dividends and stock buybacks. These actions are often well-received by investors and can have a direct impact on Total Shareholder Return (TSR) — the popular metric that combines stock appreciation and dividends into one figure.

In the pursuit of maximizing shareholder value, many companies lean heavily on tools like dividends and stock buybacks. These actions are often well-received by investors and can have a direct impact on Total Shareholder Return (TSR) — the popular metric that combines stock appreciation and dividends into one figure.

But beneath the surface, these capital allocation decisions can distort performance assessments, especially when used to evaluate operational success. In this article, we examine how poorly timed buybacks and unrealistic reinvestment assumptions related to dividends can make TSR a misleading performance benchmark.

💸 Understanding the Capital Allocation Effect

Capital allocation decisions are strategic — they reflect how management deploys excess cash:

-

Dividends provide regular income to shareholders

-

Buybacks reduce the number of shares outstanding, often increasing earnings per share and potentially boosting stock price

These actions directly affect TSR by increasing the numerator in the TSR formula. However, TSR assumes that all dividends are reinvested in the company’s own stock, often at the prevailing market price. Similarly, it treats buybacks as inherently beneficial, without adjusting for timing or effectiveness.

📉 When Capital Allocation Backfires

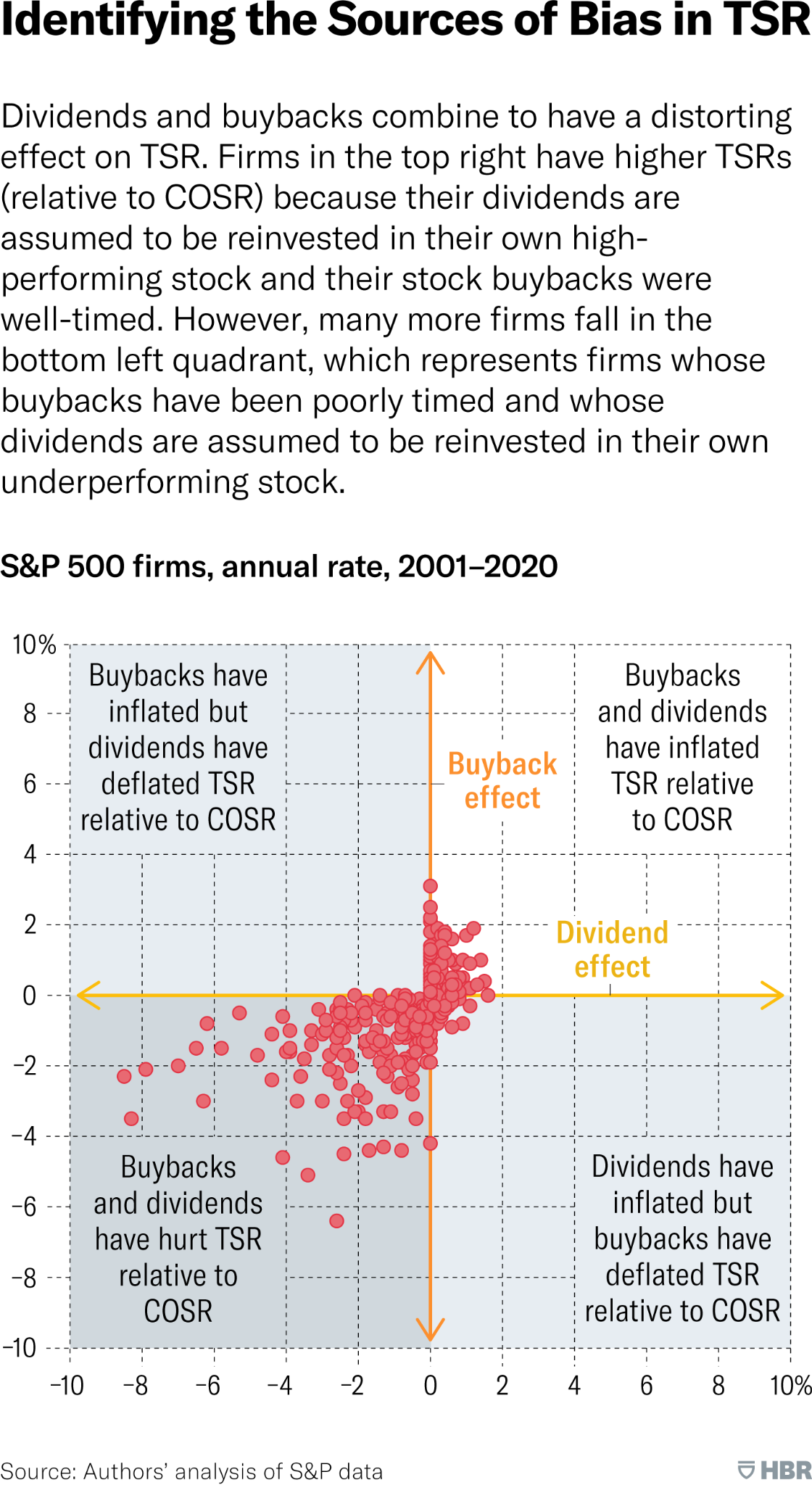

Recent data from 2001 to 2020 across S&P 500 firms reveals that many companies fall into the bottom-left quadrant of the COSR–TSR comparative chart. This quadrant reflects firms where both dividends and buybacks actually hurt TSR relative to COSR.

Here’s why:

🕒 Poor Timing of Buybacks

Firms frequently conduct buybacks during market peaks, when their stock is expensive. This diminishes long-term return because the company overpays for its own shares, yielding minimal value for remaining shareholders. What appears as shareholder-friendly behavior ends up destroying value.

♻️ Dividend Reinvestment Fallacy

TSR calculations assume that dividends are automatically reinvested into the company’s stock. But this reinvestment is theoretical and often doesn’t reflect investor behavior. Worse yet, if the firm’s stock is underperforming, reinvesting dividends into more of the same stock could be value-destructive — especially when market sentiment is weak.

🧭 Quadrant Analysis: Mapping the Distortion

The quadrant visualization of COSR vs TSR provides a powerful framework:

-

Top Right Quadrant: Firms with well-timed buybacks and strong stock performance. Here, both TSR and COSR are high.

-

Bottom Left Quadrant: Firms with poorly timed buybacks and reinvested dividends into weak stocks, resulting in TSR underperforming COSR.

-

Top Left Quadrant: Buybacks inflate but dividends deflate TSR (relative to COSR).

-

Bottom Right Quadrant: Dividends inflate but buybacks deflate TSR (relative to COSR).

The largest cluster of firms falls in the bottom left, reinforcing that most capital allocation decisions do not enhance shareholder return as measured by TSR, and instead obscure underlying operational strength.

🏢 Implications for Leaders and Boards

Boards and executives must acknowledge that TSR is not a neutral scoreboard. It rewards specific types of behavior — not always aligned with long-term success:

-

Executives may be incentivized to return capital rather than reinvest it productively

-

Buybacks may be pursued for short-term EPS boosts, not strategic growth

-

Dividend consistency may be prioritized over strategic flexibility

COSR, by excluding these externalities, delivers a truer picture of performance by focusing solely on the operating core.

🌍 The Dawgen View: Realigning with Operational Value

At Dawgen Global, we believe that the health and sustainability of a business should be evaluated based on its operational core, not just its market-facing performance. For companies in Caribbean markets and other emerging economies, this distinction is particularly important.

In these regions, firms often operate in less liquid and more volatile capital markets, where external forces — such as currency fluctuations, investor concentration, and geopolitical shifts — can significantly skew stock-based metrics like TSR. Add to that the increasing pressure to “reward shareholders” through dividends and buybacks, and companies risk prioritizing short-term cosmetic wins over long-term strategic growth.

That’s why our advisory approach focuses on realigning capital allocation strategies with operational value creation. We encourage clients to evaluate dividends and buybacks not as default value-returning mechanisms, but as tools whose effectiveness must be measured, monitored, and justified in the context of sustainable performance.

🧭 Dawgen Global’s Key Recommendations

✅ 1. Audit the Timing and Effectiveness of Buybacks

Not all buybacks are created equal. While well-timed repurchases can be accretive, poorly timed ones — especially during inflated stock valuations — can destroy shareholder value and create misleading performance signals. We recommend that boards:

-

Establish clear policies for buyback authorization and execution windows

-

Regularly conduct post-buyback reviews comparing expected vs. actual value delivered

-

Treat buybacks as capital allocation decisions — not merely shareholder appeasement tactics

✅ 2. Disclose Operational KPIs Alongside TSR in Investor Reports

Too often, investor communications are dominated by TSR and stock trends. To restore balance and credibility, firms should pair these with clear, operational performance metrics, such as:

-

Return on invested capital (ROIC)

-

EBITDA margin improvements

-

Customer retention and acquisition rates

-

Operational cost savings

-

Product innovation cycles

This multi-dimensional approach allows shareholders to distinguish between value created through core growth and that created through financial engineering.

✅ 3. Use COSR to Benchmark Internal Performance

COSR strips away the distortive effects of capital distributions and focuses strictly on operational return. Integrating COSR into:

-

Internal scorecards

-

Board dashboards

-

Strategic planning reviews

…ensures that decision-making is rooted in value creation and not market sentiment. COSR also enables fair comparisons between business units or subsidiaries in different geographic or market conditions.

✅ 4. Align Executive Incentives with COSR and Long-Term Value Creation

Linking executive compensation solely to TSR may incentivize risky financial behavior, such as issuing debt to fund buybacks or delaying necessary investments to maintain dividends. We advise clients to:

-

Introduce COSR-based performance targets into executive bonus and LTIP structures

-

Include metrics tied to strategic initiatives, such as digital transformation, market expansion, or ESG compliance

-

Shift from quarterly-based measurements to multi-year value delivery frameworks

This ensures that leadership remains focused on building durable competitive advantage, not chasing transient share price bumps.

📈 Looking Ahead

As financial reporting grows more transparent and capital markets become more discerning, the traditional reliance on TSR alone is no longer sufficient. The modern performance conversation must go deeper — beyond optics, beyond capital flows — and into the operational heartbeat of the business.

COSR is the corrective lens companies need to focus on sustainable, strategic, and stakeholder-aligned value. It moves the conversation from “What happened to our stock?” to “What have we built, improved, or strengthened operationally?”

In the next article of this series, we’ll explore how executive compensation structures based on TSR may incentivize the wrong behaviors — and how firms can adopt COSR-aligned metrics to drive stronger alignment between leadership incentives and long-term business health.

Next Step!

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

✉️ Email: [email protected] 🌐 Visit: Dawgen Global Website

📞 Caribbean Office: +1876-6655926 / 876-9293670/876-9265210 📲 WhatsApp Global: +1 876 5544445

📞 USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements