Markets teach control lessons in two ways: privately, through the quiet findings of a well-functioning assurance system — or publicly, through announcements no board ever wants to draft. Over the past two years, the Jamaica Stock Exchange has delivered several of the second kind: a substantial inventory write-off at a listed company, a material restatement of previously reported figures accompanied by a change of external auditor, and a persistent pattern of late-filed audited financial statements affecting a meaningful share of the market. Each was disclosed publicly; each moved a share price; and each, examined closely, is a story about assurance that arrived too late.

A note on method: this article relies exclusively on publicly disclosed information, names no company or individual, and offers governance analysis rather than accusation. The purpose is not to relitigate specific events but to extract the internal audit lessons they hold for every Caribbean board — because the control weaknesses behind public failures are never unique to the companies that disclose them. They are simply the ones whose weaknesses matured first. This sixth article in The Internal Audit Imperative™ examines three patterns and the assurance disciplines that interrupt them.

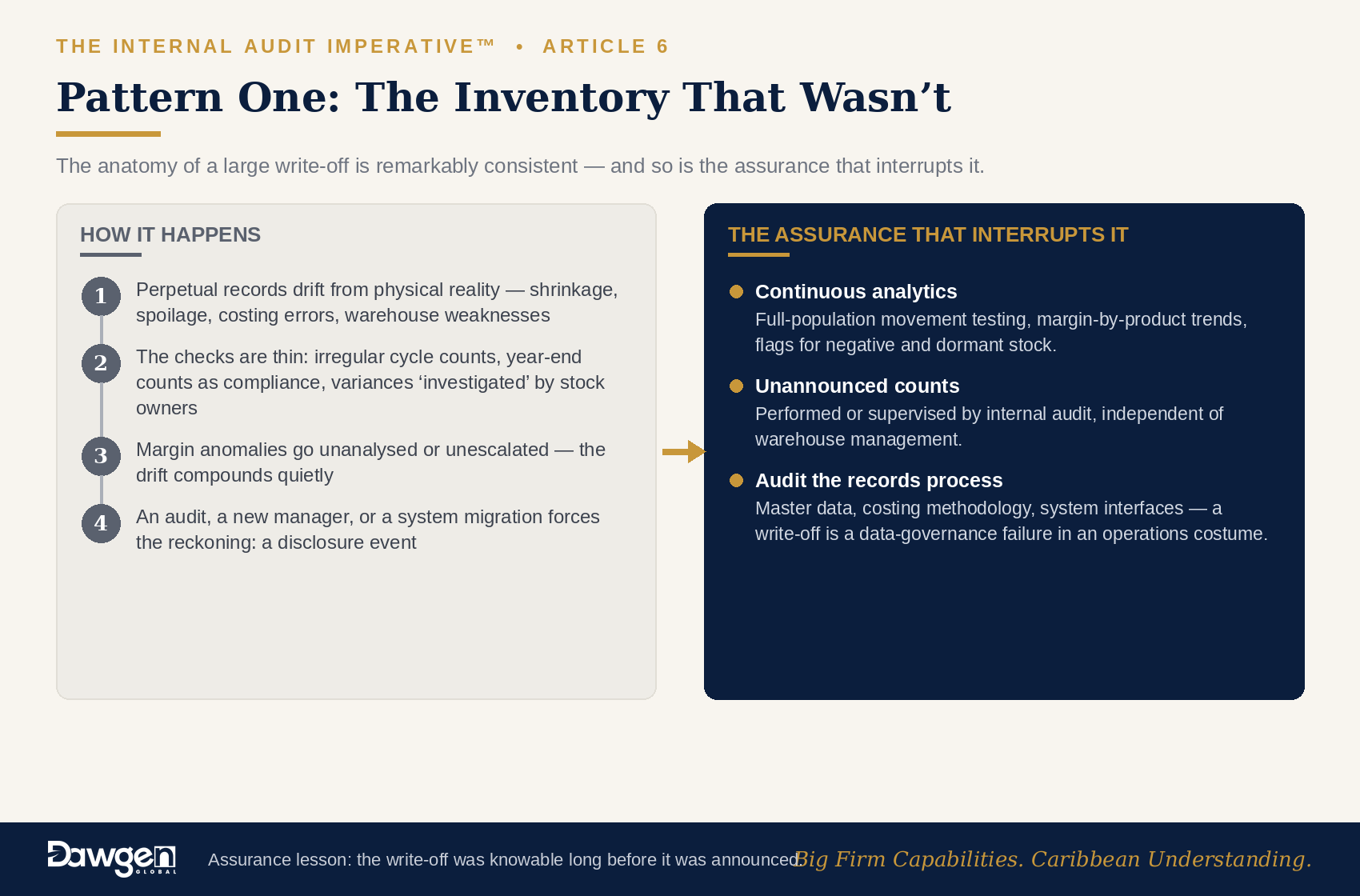

Pattern One: The Inventory That Wasn’t

The anatomy of a large inventory write-off is remarkably consistent across companies and industries. Perpetual inventory records drift away from physical reality — through shrinkage, spoilage, costing errors, receiving and dispatch discrepancies, or weaknesses in warehouse controls — and the drift compounds quietly because the checks that should catch it are thin: cycle counts are irregular or poorly supervised, full physical counts are treated as a year-end compliance exercise, variances are “investigated” by the same team that manages the stock, and margin analysis that would flag the anomaly is either not performed or not escalated. By the time an external audit, a new manager, or a system migration forces a reckoning, the adjustment is no longer an operational correction. It is a disclosure event.

The internal audit lessons: First, inventory-heavy businesses warrant continuous, analytics-driven assurance — full-population testing of movements, margin-by-product trend analysis, and automated flags for negative stock, dormant items, and cost anomalies — not an annual sample. Second, unannounced counts, performed or supervised by internal audit with genuine independence from warehouse management, remain one of the highest-yield procedures in the auditor’s toolkit precisely because they are unfashionable. Third, the function must audit the integrity of the perpetual records process itself — master data, costing methodology, interfaces between systems — because a write-off is usually a data-governance failure wearing an operations costume.

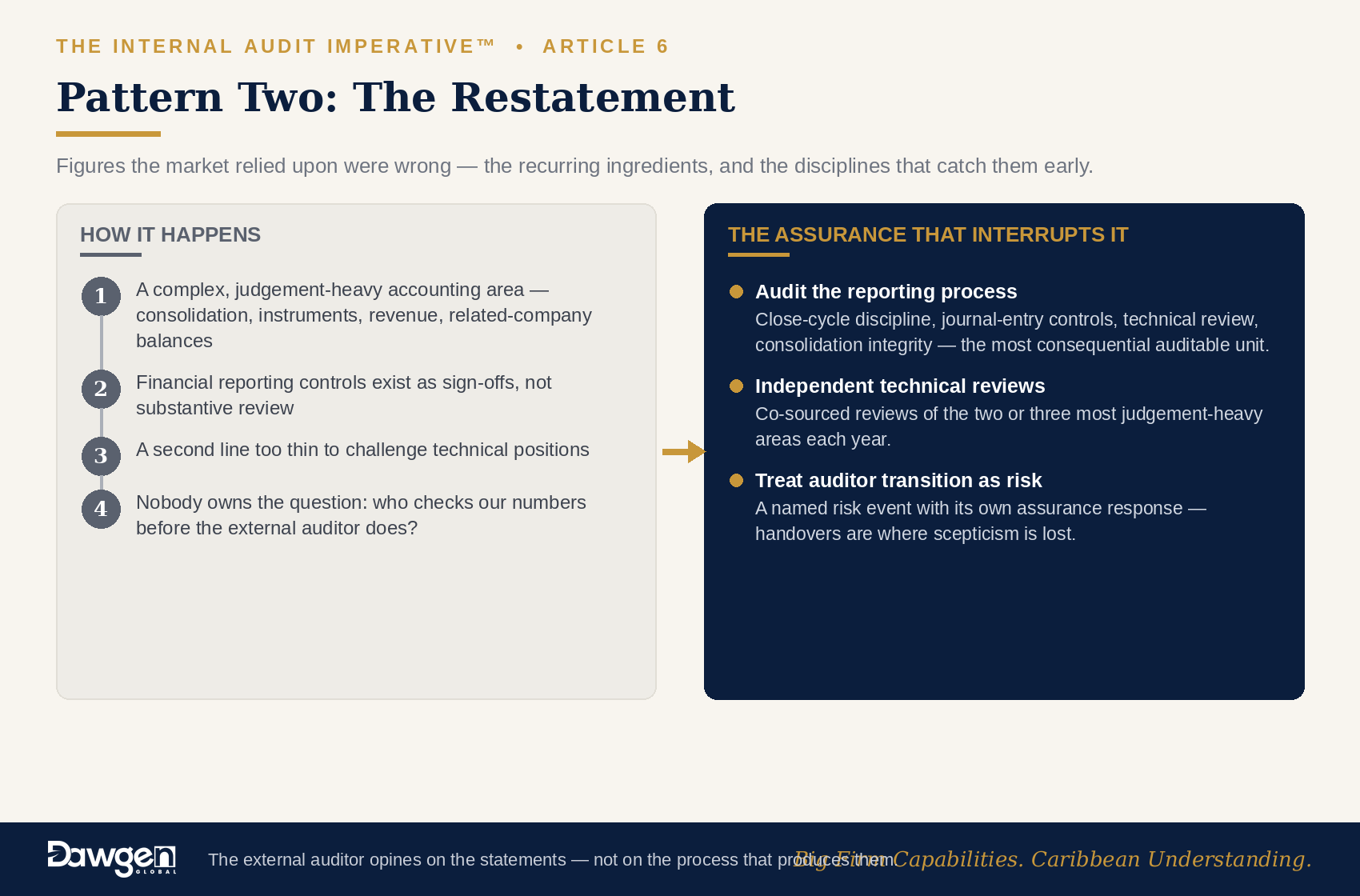

Pattern Two: The Restatement

A restatement announces that figures the market relied upon were wrong — and restatements of equity or comparative results, particularly when accompanied by a change of external auditor, signal something deeper than a bookkeeping slip. The recurring ingredients: a complex or judgement-heavy accounting area (consolidation, financial instruments, revenue recognition, related-company balances) handled by a finance team stretched thin; financial reporting controls that exist as sign-offs rather than substantive review; a second line too small to challenge technical positions; and an assurance map on which nobody — not internal audit, not the audit committee — owned the question: who is checking that our reported numbers are right before the external auditor does?

The internal audit lessons: The financial reporting process is itself an auditable unit — arguably the most consequential one — yet many Caribbean functions have never audited it, on the mistaken theory that the external audit covers it. It does not: the external auditor opines on the statements, not on the health of the process that produces them. A conformant function audits close-cycle discipline, technical accounting review, journal-entry controls, and consolidation integrity; commissions or co-sources independent technical accounting reviews of the two or three most judgement-heavy areas each year; and treats an external auditor transition as a named risk event with its own assurance response, because handover periods are when institutional knowledge — and institutional scepticism — is most easily lost.

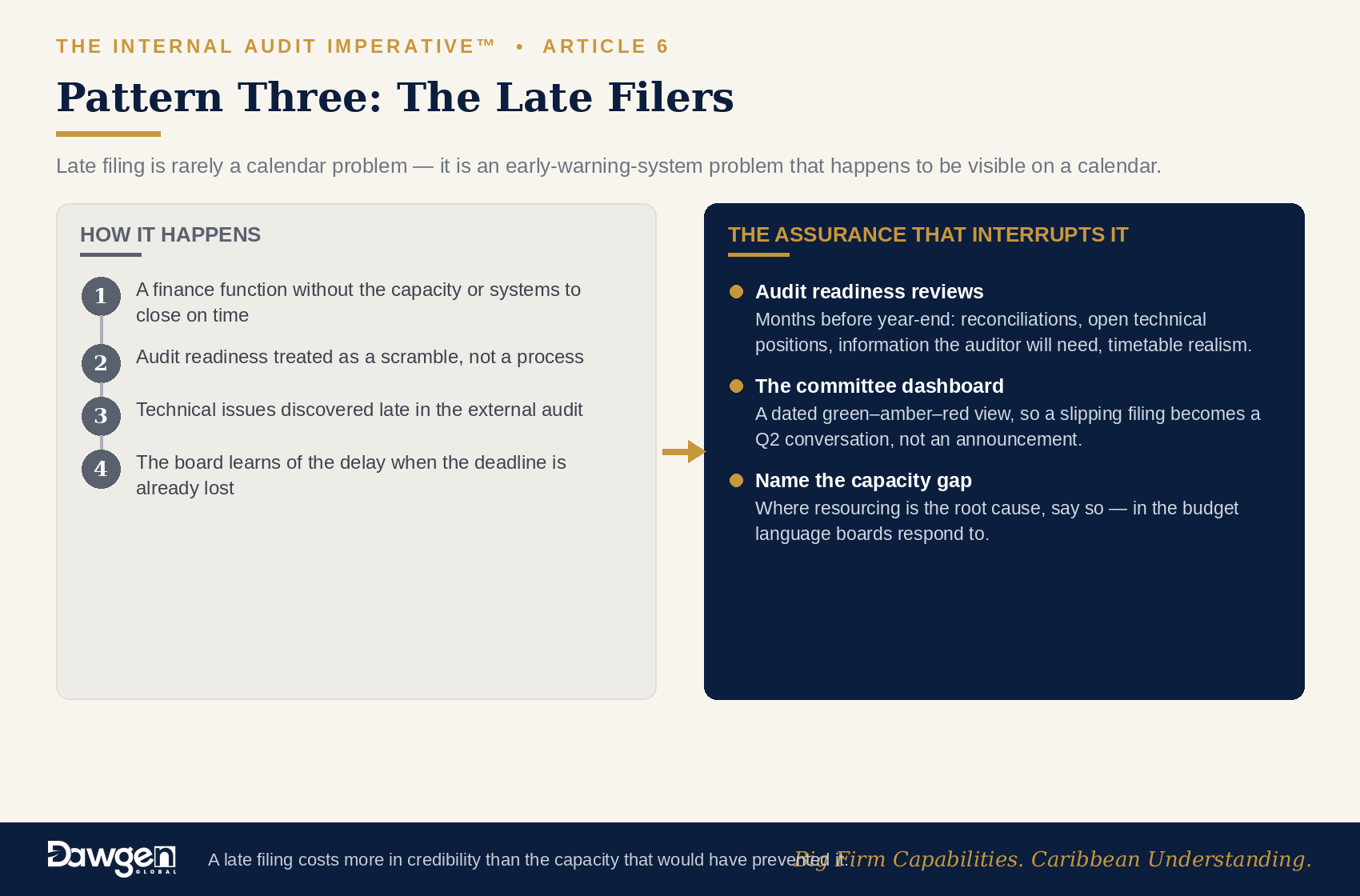

Pattern Three: The Late Filers

Less dramatic than a write-off but corrosive in aggregate, chronic late filing of audited financial statements has affected enough listed companies to draw regulatory attention and, at times, trading suspensions. Behind almost every late filing sits the same short list: a finance function without the capacity or systems to close on time; audit readiness treated as a scramble rather than a process; unresolved technical issues discovered late in the external audit; and — the governance tell — a board that learns of the delay when a deadline is already lost rather than when the risk first emerged. Late filing is rarely a calendar problem. It is an early-warning system problem that happens to be visible on a calendar.

The internal audit lessons: A function positioned as the board’s early warning system audits audit readiness months before year-end: the status of reconciliations, unresolved technical positions, information the external auditor will require, and the realism of the close timetable. It reports a simple, dated dashboard to the audit committee — green, amber, red — so a slipping filing becomes a Q2 conversation rather than a public announcement. And where capacity is the root cause, it says so in the resource language boards respond to, because a late filing costs more in market credibility than the finance capacity that would have prevented it.

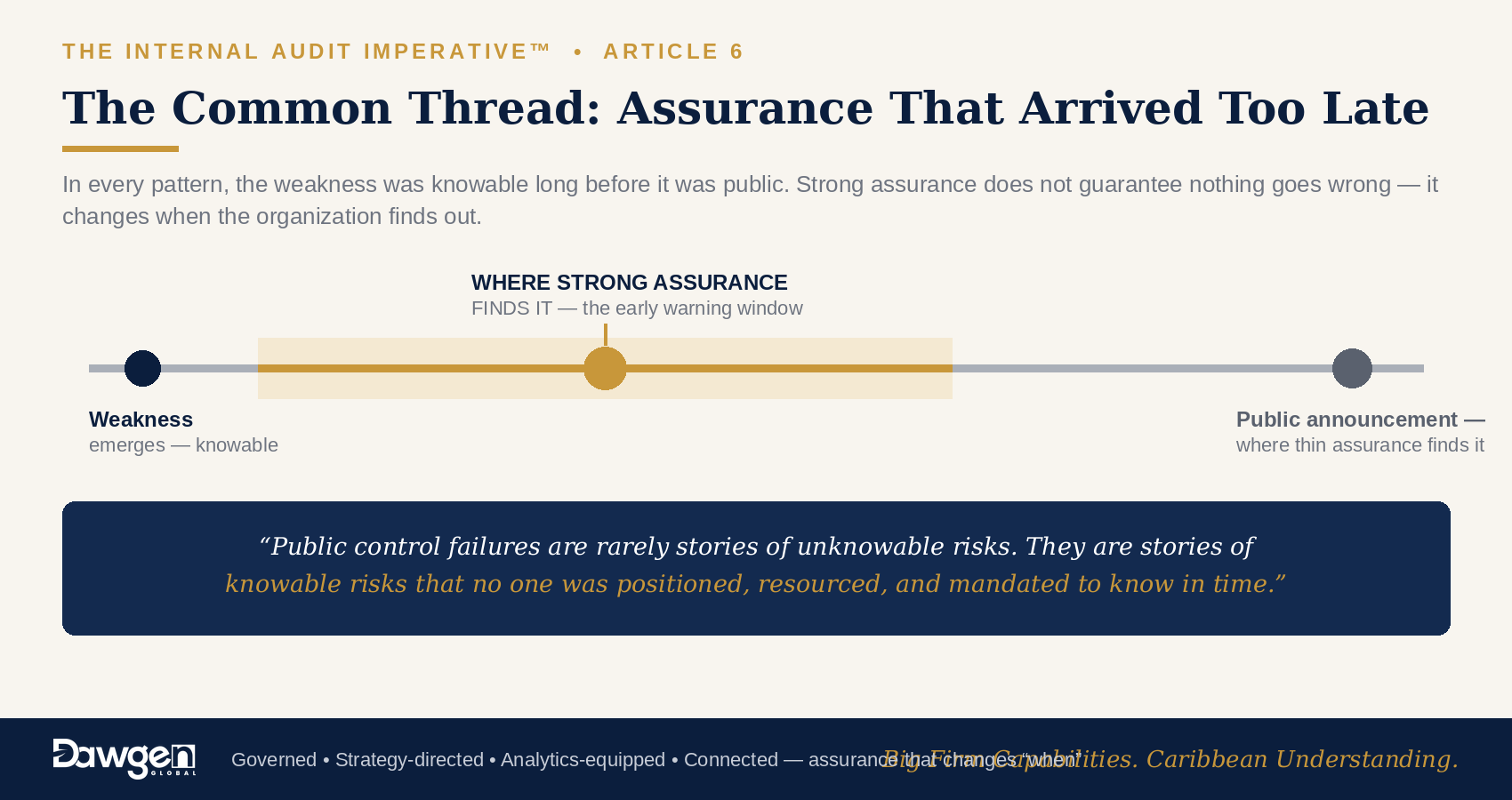

The Common Thread: Assurance That Arrived Too Late

Strip away the accounting specifics and the three patterns share one architecture. In each, the control weakness existed and was knowable long before it became public. In each, the mechanisms that should have surfaced it early — continuous monitoring, a resourced second line, an independent internal audit with the mandate to look — were thin, absent, or reporting into the wrong place. And in each, the board’s first substantive engagement with the issue came at the announcement stage, when the remaining options were disclosure management rather than prevention. This is precisely the failure mode the Global Internal Audit Standards were rewritten to interrupt: a function governed by the board, directed by a strategy, equipped with analytics, and connected to the second line does not guarantee that nothing goes wrong — it changes when the organization finds out, and “when” is everything.

Public control failures are rarely stories of unknowable risks. They are stories of knowable risks that no one was positioned, resourced, and mandated to know in time.

What Boards Should Commission Now

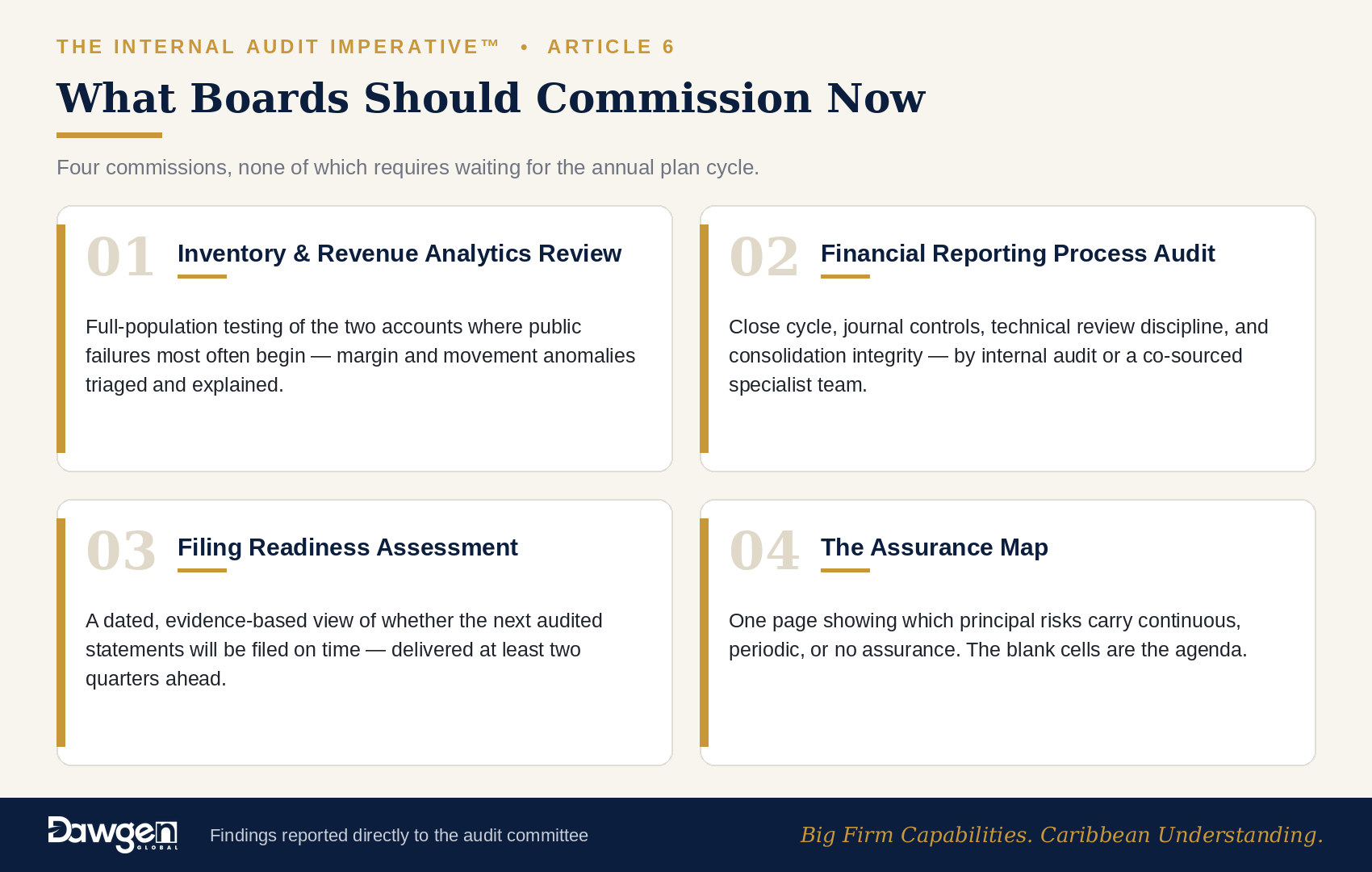

Directors reading these patterns against their own organizations can respond with four commissions, none of which requires waiting for the annual plan cycle:

- An inventory and revenue analytics review — full-population testing of the two accounts where public failures most often begin, with margin and movement anomalies triaged and explained.

- A financial reporting process audit — close cycle, journal controls, technical review discipline, and consolidation integrity, performed by internal audit or a co-sourced specialist team.

- A filing readiness assessment — a dated, evidence-based view of whether the next audited statements will be filed on time, delivered to the committee at least two quarters ahead.

- An assurance map — one page showing which of the organization’s principal risks carry continuous assurance, periodic assurance, or none at all. The blank cells are the agenda.

The Dawgen Perspective

It is tempting for directors to read public control failures as stories about other companies. The more useful reading is statistical: the companies that disclose are drawn from the same control environment the rest of the market operates in — the same talent pool, the same systems, the same pressures. What distinguishes them is not that their weaknesses were unusual but that their weaknesses matured. Every board therefore faces a simple question: would we know? If inventory records were drifting, if a technical position were wrong, if the filing were going to be late — would the board know now, or at the announcement? Building the apparatus that answers “now” is the entire project of this series.

Dawgen Global’s integrated assurance teams — internal audit, data analytics, forensic, IT, and technical accounting under D·ASSURE™ and TRUST360™ — deliver precisely these reviews across 15+ Caribbean territories, as one-off board commissions or as part of a co-sourced internal audit programme.

Next in the series: “The Three Lines in Practice: Making Risk, Compliance, and Internal Audit Work Together” — how to build the connected assurance ecosystem that makes early warning possible.

| Would Your Board Know — Now, or at the Announcement?

Dawgen Global’s Control Health Check delivers the four board commissions in one engagement: inventory and revenue analytics, a financial reporting process audit, a filing readiness assessment, and a one-page assurance map — with findings reported directly to your audit committee. Knowable risks, known in time. Email us | [email protected] | |

About Dawgen Global

Dawgen Global is an independent, integrated multidisciplinary professional services firm headquartered at 47 Trinidad Terrace, New Kingston, Jamaica, serving more than 15 territories across the Caribbean. Founded and led by Dr. Dawkins Brown, Executive Chairman, the firm is independent and not affiliated with any international network. It delivers a full suite of professional services under one roof: audit and assurance; tax advisory; IT and digital transformation; risk management; cybersecurity; actuarial and insurance regulatory advisory; HR advisory; mergers and acquisitions; corporate recovery; business advisory and strategy; accounting BPO and virtual CFO services; and legal process outsourcing.

The proposition is simple: big-firm capability without the big-firm price. Dawgen Global’s integrated approach is built for the specific complexities and opportunities of the Caribbean market, helping organizations make sharper, better-informed decisions that drive measurable progress.

To explore a partnership, reach out:

- Website: dawgen.global

- Email: [email protected]

- WhatsApp (Global): +1 555-795-9071

- Caribbean offices: +1 876-665-5926 | +1 876-929-3670 | +1 876-926-5210