Executive Summary

Many organisations treat inventory as a finance topic—something to “reduce” to free up cash. In reality, inventory is an operating system outcome. It is shaped by planning quality, supplier reliability, service promises, lead times, forecasting discipline, and decision rights. When these fundamentals are weak, organisations end up paying an invisible penalty every day: the urgency tax.

The urgency tax shows up as:

-

emergency purchasing at premium prices

-

expedited freight and courier shipments

-

overtime and weekend work to “catch up”

-

stockouts that force substitutions, lost sales, and customer churn

-

excess inventory that expires, becomes obsolete, or must be discounted

-

working capital costs that rise sharply when interest rates increase

The paradox is that many firms carry too much inventory and still experience stockouts—because the issue is not “how much inventory,” but how inventory decisions are made.

This article explains:

-

Why poor planning is one of the highest-leverage cost reduction opportunities

-

How inventory creates cost across the value chain, not just on the balance sheet

-

The five inventory failure modes that destroy profitability

-

A practical 60–90 day pathway to reduce urgency costs while protecting availability

-

How the Dawgen V.A.L.U.E.-Chain Cost Advantage Framework™ helps organisations validate, analyse, prioritise, execute, and sustain planning-driven cost advantage

Inventory discipline is not austerity. It is a competitive capability: lower cost, better service, stronger cash generation, and more predictable operations.

What Is the “Urgency Tax”?

The urgency tax is the premium you pay when planning and replenishment are not working. It is the cost of reacting rather than managing.

You know the urgency tax is present when you see phrases like:

-

“We need it for tomorrow.”

-

“Just buy it—we’ll sort the paperwork later.”

-

“Ship it by air; we can’t wait.”

-

“Run overtime; we’re behind.”

-

“Why is this out of stock again?”

-

“We have too much of the wrong items.”

The urgency tax is expensive because it triggers costs across multiple functions:

-

procurement pays higher prices

-

logistics pays higher freight

-

operations pay overtime, rework, and disruption costs

-

sales loses credibility and discounts to compensate

-

finance carries higher working capital and write-off risk

In short: the urgency tax is a systemic cost, not a one-time event.

Why Inventory Is a Cost Reduction Strategy

Inventory decisions influence at least five major cost pools:

1) Procurement cost

When the business buys urgently, it often:

-

loses bargaining power

-

accepts higher spot prices

-

bypasses competitive sourcing

-

buys from non-preferred suppliers

-

pays for premium terms

2) Logistics and freight cost

Poor planning leads to:

-

expedited freight

-

partial container loads

-

inefficient consolidation

-

last-minute courier shipments

-

fragmented inbound deliveries

3) Operational cost (labour and productivity)

When stock arrives late or unpredictably, operations suffer:

-

schedule instability

-

overtime

-

changeovers and poor utilisation

-

waiting time and downtime

-

rework from substitutions or rushed processing

4) Commercial cost (service and margin leakage)

Stockouts and substitutions can trigger:

-

lost sales

-

penalties (in some contracts)

-

customer churn

-

discounting to recover goodwill

-

“special deliveries” to satisfy urgent demand

5) Working capital and write-off cost

Excess inventory creates:

-

financing cost

-

storage and handling cost

-

shrinkage and damages

-

obsolescence and expiry

-

slow-moving stock that must be discounted

This is why inventory is not simply a finance KPI. It is a core lever in sustainable cost reduction.

The Inventory Paradox: Too Much Stock and Still Stockouts

Many organisations experience both:

-

excess inventory overall, and

-

stockouts on critical items.

This happens when:

-

inventory is not allocated to the right items (wrong mix)

-

planning does not reflect demand variability

-

lead times are inconsistent and not measured

-

reorder rules are not aligned to service promises

-

exceptions are unmanaged and become “normal”

In these environments, inventory is not a buffer—it is noise.

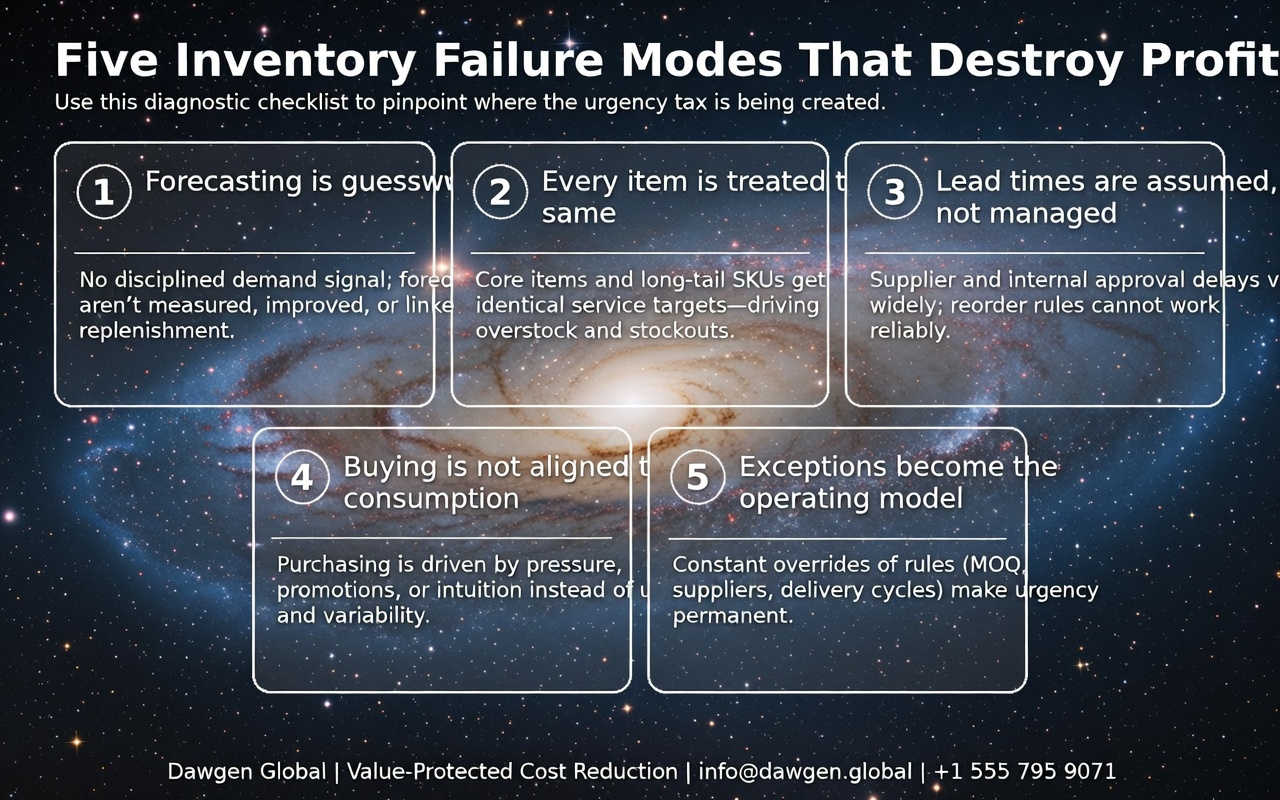

Five Inventory Failure Modes That Destroy Profitability

Failure Mode 1: “Forecasting is guesswork”

Forecasting doesn’t need to be perfect, but it must be:

-

disciplined

-

measured

-

improved over time

-

linked to replenishment decisions

When forecasting is informal, replenishment becomes reactive.

Failure Mode 2: “Every item is treated the same”

Not all items matter equally. A practical approach separates inventory into:

-

high runners / critical items

-

medium importance

-

low movers / long tail

When the business applies the same service target to all items, it overstocks the long tail and under-serves the core.

Failure Mode 3: “Lead times are assumed, not managed”

If supplier lead times are not tracked and improved, replenishment rules cannot work. In many cases:

-

lead time variability is larger than average lead time

-

suppliers are unreliable

-

internal approval delays add invisible lead time

Failure Mode 4: “Buying is not aligned to consumption”

Inventory replenishment should be driven by:

-

consumption and demand signals

-

lead times

-

service targets

-

variability

Instead, many businesses buy based on:

-

sales pressure

-

supplier promotions

-

“gut feel”

-

seasonality assumptions without data

Failure Mode 5: “Exceptions become the operating model”

If teams constantly override:

-

reorder rules

-

minimum order quantities

-

approved supplier lists

-

delivery cycles

…then the system cannot stabilise, and urgency becomes permanent.

Where the Savings Usually Hide (Inventory & Planning Opportunities)

Organisations often find high-confidence savings in:

Procurement and inbound

-

consolidating purchases (reduce fragmentation)

-

improving supplier reliability and fill rates

-

optimising Incoterms and shipment planning

-

reducing maverick purchasing triggered by urgency

Warehousing and handling

-

reducing handling touches through better slotting and layout

-

reducing write-offs through better FEFO/FIFO discipline

-

eliminating double handling caused by poorly planned inbound flow

Freight and distribution

-

reducing emergency freight

-

improving container utilisation

-

stabilising delivery schedules

Working capital

-

reducing days inventory outstanding (DIO) without harming availability

-

monetising obsolete stock through clearance strategy

-

improving replenishment to reduce overstock and stockouts simultaneously

A Practical 60–90 Day Pathway to Reduce the Urgency Tax

You don’t need perfect systems to begin. The objective is to stabilise and create a fact base.

Phase 1 (Weeks 1–2): Validate the baseline and pain points

-

quantify: emergency buys, expedited freight, overtime related to stock issues

-

identify: top 50 SKUs by revenue/volume and top 50 by stockout incidents

-

map: who makes replenishment decisions and how overrides happen

Output: a clear urgency tax estimate and hotspots.

Phase 2 (Weeks 3–6): Segment inventory and reset rules

-

implement ABC (or ABC/XYZ) segmentation:

-

A items: high impact, high availability focus

-

B items: balanced

-

C items: control and rationalisation focus

-

-

define service targets by segment

-

reset reorder points and safety stock using lead time and variability proxies

-

tighten approvals for exceptions

Output: a stabilised replenishment discipline that reduces noise.

Phase 3 (Weeks 6–12): Attack root causes

-

negotiate supplier reliability improvements

-

reduce lead time variability and internal approval delays

-

implement demand planning cadence

-

enforce purchase-to-pay discipline to reduce “urgent off-contract” buying

-

launch obsolete stock clearance programme with rules

Output: reduced urgency events, reduced expedited spend, improved availability.

How V.A.L.U.E.™ Applies to Inventory and Planning

V — Validate the Profitability Challenge

-

quantify the urgency tax

-

establish baseline KPIs: stockouts, expedited freight, DIO, write-offs, forecast accuracy proxy

A — Analyse the Value Chain and Cost-to-Serve

-

map inventory drivers across the chain

-

identify where urgency triggers cost-to-serve spikes (rush deliveries, substitutions, customer churn)

L — Locate Levers and Build Opportunity Portfolio

-

levers: segmentation, supplier reliability, lead time reduction, governance, planning cadence

-

quantify expected benefits ranges

U — Uplift & Prioritise

-

prioritise quick wins: exception controls, top-SKU stabilisation, clearance plan

-

build roadmap for structural improvements: supplier performance, planning process, tech enablement

E — Execute with Governance & Controls

-

weekly planning huddles

-

procurement discipline and exception approval workflow

-

finance validation of savings from reduced expedite and reduced write-offs

™ — Transform for Sustainability

-

embed KPI dashboard

-

run monthly S&OP-lite cadence

-

prevent exception creep through governance and accountability

Case Snapshot: Cutting Expedite Costs Without Losing Sales

A composite importer-distributor faced high margin pressure. Expedited freight and emergency purchasing had become routine. The business carried high inventory but still suffered frequent stockouts on core SKUs.

Actions taken:

-

segmented inventory into A/B/C items

-

reset reorder points and safety stock for A items

-

tightened exceptions (who can override, and when)

-

negotiated supplier fill-rate improvements

-

introduced a weekly planning cadence

Results achieved:

-

reduced expedited shipments

-

improved availability on core SKUs

-

reduced overstock in low movers

-

improved cash conversion—without sacrificing service

Planning Discipline Is a Competitive Advantage

Organisations don’t pay the urgency tax because they want to. They pay it because planning, governance, and supplier reliability are not strong enough.

If you want sustainable cost reduction:

-

stabilise planning

-

segment inventory intelligently

-

reduce lead time variability

-

enforce disciplined exceptions

-

reduce expedite and waste while protecting service

This is one of the most reliable paths to value-protected cost advantage.

Next Step!

Want to quantify and eliminate your urgency tax—while protecting availability?

Email [email protected] with the subject line “V.A.L.U.E. – Inventory & Planning Scan” to request an initial discussion and our data intake checklist.

WhatsApp Global: +1 555 795 9071 | Contact form: https://www.dawgen.global/contact-us/

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements