A Dawgen RISE-360™ guide for Jamaica and the Caribbean

Cash speed depends on proof quality. The organisations that obtain clean advances in Days 5–10 and settle without write-offs are those that treat claims as an operational workstream: evidence captured once and used many times; policy parameters extracted on Day 1; an adjuster brief that answers questions before they are asked; and a milestoned settlement plan tied to photos, logs, invoices, and BI calculations.

This guide delivers a full Legal & Claims playbook for Jamaica and the wider Caribbean: PD/BI/EE framing, folder standards, adjuster engagement cadence, advance request package composition, BI baselining and run-rate reconciliation, negotiation posture, pitfalls to avoid, and KPIs your board, lenders, and regulators will trust.

1) What “Good” Looks Like (Outcomes by Day 30)

-

Claim numbers issued for each policy section (PD/BI/EE) and location.

-

Advance received against PD/EE and (where warranted) BI within 10–20 days.

-

Evidence integrity ≥95% (timestamp/geo; naming convention; chain-of-custody).

-

Adjuster cadence stabilised (inspection windows booked; weekly checkpoint notes).

-

BI baseline agreed (margin schedules, run-rate, waiting period applications).

-

Dispute funnel managed early: scope, pricing, policy interpretation, deductibles.

-

Zero missed relief windows (duty waivers, tax/utility credits) linked to claim.

2) RISE-360™ Alignment

-

R — Readiness: policy register, endorsements, deductibles, waiting periods; naming conventions; Claims Dossier folder tree; message bank for notices.

-

I — Impact (0–72h): notify, obtain claim #s, schedule inspections, heavy evidence capture, extract parameters, set waiting periods in the BI clock.

-

S — Stabilization (Days 3–30): adjuster brief, PD schedule skeleton, vendor quotes, BI baseline & run-rate reconciliation, advance request package submission.

-

E — Elevation (31–90+): settlement strategy, wording improvements for next season, premium-credit evidence, and parametric options.

3) Policy Intelligence on Day 1

Create a one-pager per policy with the items below; circulate to Gold/Silver leads and Finance.

Key fields

-

Insurer / Policy # / Period

-

Sections & Sub-limits: PD, BI (waiting period, indemnity period), EE (caps).

-

Deductibles: fixed % or currency; per-location? per-occurrence?

-

Extensions: utilities; denial of access; ingress/egress; debris removal; expediting.

-

Notification: deadlines; method; required info.

-

Adjuster: assigned firm/contact; SLA for inspection.

-

Documentation standards: originals vs copies; digital acceptance; WORM/immutable storage guidance.

Rule of thumb: If it’s not written, it isn’t covered—log every assumption and confirm in writing.

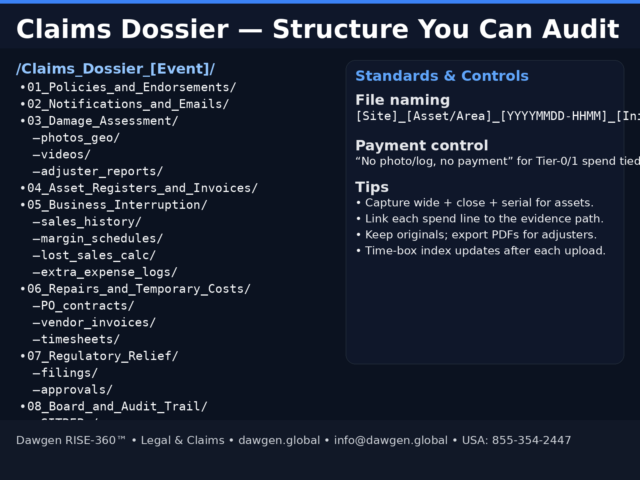

4) The Claims Dossier (Structure You Can Audit)

Use a standard, repeatable tree to prevent re-work and disputes.

File naming: [Site]_[Asset/Area]_[YYYYMMDD-HHMM]_[Initials]_[WIDE/CLOSE/SERIAL].jpg

Payment control: “No photo/log, no payment” for Tier-0/1 spend tied to claimable items.

5) PD / BI / EE: Frame the Claim the Way Insurers Think

-

PD (Property Damage): structural and asset damage; priced by scope + quotes + rate cards; photos with serials where applicable.

-

BI (Business Interruption): gross profit loss during waiting/indemnity periods less avoided costs; needs baseline and run-rate.

-

EE (Extra Expense): reasonable extra cost that mitigates BI; show how it reduces the loss (e.g., pop-ups, generators, LTE).

Golden thread: Evidence → Accounting entry → Claim schedule line → Policy section.

6) Adjuster Engagement Cadence

Day 1–2

-

Notify, get claim #, propose inspection windows.

-

Share SITREP v1 and status page; introduce Evidence Officer.

Day 3–4

-

Send Adjuster Brief (v0.9): policy summary, site list, hazards, photo index, first-fix priorities, vendor shortlist, H&S rules, contact tree.

Day 5–10

-

Conduct inspections; log open questions; submit Advance Request Package (see §8).

-

Agree evidence formats, pricing standards (rate cards), milestone proof.

Weekly

-

30-minute checkpoint: variances, approvals pending, next milestones.

Tip: Be proactive; an adjuster who never chases you is a signal your pack is complete.

7) Building the PD Schedule (Skeleton to Pricing-Ready)

-

Asset inventory: start with pre-event registers; add serials for equipment.

-

Photo pair set: wide (context) + close (detail) + serial; link to item line.

-

Scope of works: first-fix vs permanent repair; bill of quantities by site.

-

Pricing: compare two quotes where feasible; otherwise use rate cards; include start-by dates and warranty notes.

-

Evidence pack: delivery notes, timesheets, toolbox talks, H&S compliance, commissioning tests.

Milestones for PD advances

-

Materials onsite → 20–30%

-

50% progress → 25%

-

Practical completion → 20%

-

Final docs/warranty → 10%

8) The Advance Request Package (what gets you paid early)

Cover letter (per policy section) with:

-

Event summary and claim #.

-

Immediate needs (fuel, first-fix, comms kits) that mitigate BI.

-

Requested advance amount and milestone evidence gates.

-

Confirmation of account details and authorised signatories.

Attachments

-

Evidence index (hyperlinked) to the Dossier.

-

PD skeleton + quotes/rate cards + start-by clauses.

-

EE plan tied to BI mitigation (e.g., pop-ups save X gross margin/day).

-

BI baseline (see §9) and run-rate reconciliation.

-

SITREPs with timestamped operational status.

-

Relief filings (e.g., duty waivers) to demonstrate net-of-relief costing.

Tone: factual, concise, and auditable—no advocacy language needed when proof is strong.

9) BI Baseline & Run-Rate (how to stay “unarguable”)

9.1 Establish the baseline

-

Reference period: last 12 months; adjust for seasonality (month-on-month) and known structural changes (new site, discontinued line).

-

Gross Profit definition per policy (usually revenue – variable/avoidable costs).

-

Margin schedules: itemise variable costs (COGS, logistics, utilities linked to volume).

-

Documents: management accounts, VAT/GCT returns, bank and card settlement reports.

9.2 Run-rate reconciliation (post-event)

-

Daily sales by channel vs. baseline; explain variances (site Amber/Green, SKU availability).

-

Waiting period start/end; explicit date stamps.

-

Avoided costs ledger: power saved at closed sites, furloughed labour, reduced logistics.

9.3 Calculating BI

-

Lost Gross Profit within indemnity period = (Baseline GP – Actual GP) – Avoided Costs.

-

EE offsets: demonstrate how EE reduced loss (e.g., generator rental that enabled sales).

9.4 Presentation

-

One-page summary table + footnotes; supporting workbooks in 05_Business_Interruption/.

10) Extra Expense (EE) That Actually Clears

EE is accepted quickly when it is necessary and economical. Prove both.

-

Necessity: tie to a blocked revenue path (e.g., LTE router to run POS where fiber is down).

-

Economy: cheaper than BI loss avoided (show $ of GP protected per day).

-

Evidence: invoice/PO → delivery notes → usage logs (fuel, gen hours) → photos.

-

End date: show when expense stops or converts to permanent CAPEX.

11) Regulatory Relief Linkage

Capture reliefs to reduce claim frictions and show good faith:

-

Duty waivers for repair parts;

-

Tax deferrals;

-

Utility credits by outage duration;

-

Bank moratoria.

Store filings/approvals under 07_Regulatory_Relief/ and ensure net-of-relief numbers appear in claim schedules.

12) Negotiation Posture (Fair, Firm, Evidence-Led)

-

Facts first: “Here is the evidence pack; here is how it links to the policy section.”

-

Price sanity: rate cards; market comps; two quotes where feasible.

-

Scope clarity: first-fix vs permanent; what’s included/excluded.

-

BI conservatism: avoid heroic assumptions; publish avoided costs.

-

Without prejudice (jurisdiction-aware) labelling for settlement discussions.

-

Escalation: if stalled >14 days on a point, propose specific compromise (e.g., split difference contingent on extra documentation).

13) Legal Guardrails

-

Privilege: keep legal advice threads separate; label appropriately.

-

Privacy: redact personal data in shared packs; aggregate staff/customer info.

-

Anti-fraud: serialised assets and chain-of-custody; spot-checks weekly.

-

Contracting: all POs/SOWs include evidence obligations, H&S, warranty, and milestone gates.

14) KPIs & Dashboards (Board/Lender/Insurer-ready)

-

Time-to-notice (policy) and time-to-claim #.

-

Advance requested vs received (value and days).

-

Evidence completeness (% PD/EE lines with full pack).

-

Adjuster cadence (inspections booked; open queries count).

-

BI cycle time to baseline agreement.

-

Settlement progress (% of PD/BI/EE agreed; value at risk).

-

Relief on-time filings (100% target).

15) Day-by-Day (First 10 Days — Claims View)

-

Day 1–2: Notify; create claim #; schedule inspections; heavy evidence capture; extract policy parameters; set BI waiting period.

-

Day 3–4: Draft PD schedule skeleton; load sales history; start BI baseline; send adjuster brief.

-

Day 5–6: Lock vendor quotes for high-certainty PD; submit advance request package (PD + EE).

-

Day 7–8: Reconcile BI run-rate; update insurer on progress; confirm relief filings.

-

Day 9–10: Inspection follow-ups; close evidence gaps; agree advance milestone dates.

16) Templates (Copy-Ready)

16.1 Claim Notice (Email)

Subject: [Event] — Claim Notice — Policy [#] — [Company]

Dear [Insurer/Adjuster],

We are notifying a loss under [sections] for [sites] resulting from [event, date].

Please issue a claim number and propose inspection windows.

Our evidence repository and SITREP updates: [link].

Contacts: Incident Director [name], Evidence Officer [name].

Regards,

[Name/Title]

16.2 Adjuster Brief (Contents)

-

Policy summary and parameters;

-

Site list + R/A/G status + hazards;

-

Photo/video index (10 exemplars per site);

-

PD scope & vendor list;

-

EE plan (BI mitigation);

-

H&S working rules;

-

Contact tree;

-

Inspection schedule proposals.

16.3 Advance Request Cover (Excerpt)

We request an advance of US$[X] against PD/EE for the following milestones:

-

Materials onsite (US$A) — photos + delivery notes;

-

50% progress (US$B) — photo/video set + supervisor log;

-

Practical completion (US$C) — test logs + H&S closure.

BI mitigation from these spend items is estimated at US$[Y]/day of protected gross profit.

17) Common Failure Modes—and How to Avoid Them

-

Evidence after the fact → Train Bronze teams to capture with the naming convention from Hour 0.

-

Mixed pricing → Enforce rate cards; require start-by/finish and warranty in POs.

-

BI overreach → Use conservative baselines; disclose avoided costs; keep a clear audit trail.

-

Silence / gaps → Weekly checkpoint with adjuster; publish open-issue log.

-

Missed relief → Single tracker with owners and alarms; link to claim net-of-relief.

18) Elevation: Design a Better Programme for Next Season

-

Sums insured recalibration;

-

Wording upgrades: utilities, denial of access, ingress/egress, expediting;

-

Parametric top-up for rapid liquidity;

-

Premium credits: document hardening projects and tests;

-

Broker RFP: KPI-based service levels and catastrophe response expectations.

Speed with proof wins claims. With clean evidence, an adjuster‐friendly brief, disciplined PD/EE pricing, and BI baselines that withstand scrutiny, you unlock advances quickly and settle without drama. Integrate this Legal & Claims playbook into your Dawgen RISE-360™ programme and convert disruption into funded recovery—and a stronger, insurable operating model.

Next Step!

Let’s restore—and rise—together.

Dawgen Global’s RISE-360™ Legal & Claims team sets up claim governance, compiles advance packs, leads adjuster engagement, and negotiates settlements with the evidence trail insurers, lenders, and regulators trust.

Request a proposal: [email protected]

USA: 855-354-2447

Web: https://dawgen.global

At Dawgen Global, we help you make Smarter and More Effective Decisions.

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements