| IN THIS ARTICLE

The sixth article of twelve. It opens Act III of the series — The Application — by addressing the sector that is, empirically, both the most consequential AI adopter in the Caribbean and the sector under the most direct supervisory scrutiny: financial services. Articles 1, 2 and 3 established why the cycle matters, what the technology is, and what it costs at SME scale. Articles 4 and 5 specified the guardrails of data sovereignty and regulatory readiness. The series now turns to application — the specific domains where AI is reshaping Caribbean institutional practice. Financial services is the appropriate place to begin, because the sector’s scale, its regulatory exposure, and its data intensity make every editorial argument from the previous five articles converge here. By the end of this article you will be able to: 1. Distinguish, with precision, the AI use cases that are READY for your specific Caribbean financial services sub-sector today from those that are PREMATURE — because a tier-one commercial bank, a credit union, a general insurer, and a securities firm face materially different opportunities and risks. 2. Apply the D-AGENTICA™ Financial Services AI Use-Case Map as a board-level instrument for prioritising AI investment over the next twelve months in a way that reflects your sub-sector’s actual position rather than the industry-wide marketing narrative. 3. Recognise the three patterns of AI deployment in Caribbean financial services that I observe consistently producing better outcomes — and the three patterns that are consistently producing capital destruction — so that your institution can build the first set rather than discover the second. |

The chair of a Caribbean banking group I advise telephoned me in late February with a question that had emerged at his strategy retreat. The board had spent two days discussing AI. They had emerged, he said, with three problems. The first was that everyone in the room had a different definition of what AI actually was — a problem Article 2 of this series was specifically written to solve. The second was that the management team had presented a long list of potential AI initiatives without any framework for distinguishing the genuinely high-value from the merely fashionable. The third was that he, as chair, had no confident view of which initiatives the board should authorise this year and which should wait.

‘Dr. Dawkins,’ he said, ‘our management team is bright and our technology people are competent. But I cannot tell from the slides they presented whether they are recommending the right things. I need a framework I can use, as chair, to interrogate their priorities at the next strategy session. Can you give me one?’

That is the conversation this article is going to help with. It is also, in my experience, the specific conversation that distinguishes Caribbean financial services boards that are governing AI well from those that are deferring the conversation. The well-governed boards are not the ones with the most sophisticated technical understanding; they are the ones whose chairs can interrogate the priority list with a defensible framework. The deferred conversations almost always start with management presenting a list and end with the board saying ‘let us think about it’ — because nobody on the board has the framework needed to take a substantive position.

Articles 1 through 5 of this series have built the foundations needed for that interrogation. Article 1 argued why this cycle is structurally different and why the Caribbean lag pattern will not provide cover. Article 2 installed the vocabulary required to distinguish genuinely agentic capability from chatbots marketed as such. Article 3 calibrated the realistic economics of AI for Caribbean SME scale and introduced the Sequencing Framework that responsible adopters are following. Articles 4 and 5 specified the guardrails — data sovereignty and regulatory readiness — within which adoption must be designed.

Act III of the series now begins. Where Acts I and II addressed the conceptual and governance foundations, Act III turns to application: the specific domains where AI is reshaping Caribbean institutional practice over the next twenty-four months. There are three of those domains addressed in the next three articles. Financial services, addressed in this article, comes first because the sector’s scale and supervisory exposure make every prior editorial argument converge here. Article 7 will address the Caribbean workforce transition — how AI is reshaping the work itself. Article 8 will address the finance function specifically — how AI is reshaping the work of the CFO and the finance team.

This article is organised in four parts. First, I will name the four sub-sectors of Caribbean financial services and explain why a single ‘financial services’ frame is too coarse for the AI conversation; the sub-sectors face materially different opportunities and risks, and a board chair governing one needs different priorities from a board chair governing another. Second, I will introduce the D-AGENTICA™ Financial Services AI Use-Case Map — the named instrument for this article — which differentiates use cases by sub-sector and maturity. Third, I will name the three patterns of deployment I observe consistently producing better outcomes in our region. Fourth, I will name the three patterns I observe consistently destroying capital, so that the boards reading this article can avoid them.

By the time you finish, you will be able to interrogate your management team’s AI priority list with the framework the chair I described needed. Whether you agree with the specific cell assignments in the Use-Case Map matters less than whether you have applied a defensible methodology to distinguish what to authorise from what to defer. The methodology is what your board’s decisions will be measured against, not the specific items on this year’s list.

Why ‘financial services’ is too coarse a frame

The first error I observe in Caribbean AI conversations about financial services is that ‘financial services’ is treated as a single sector. It is not. The Caribbean financial services landscape contains at least four distinct sub-sectors, each with materially different scale, customer relationships, regulatory posture, and risk profile. An AI use case that is ready for a tier-one commercial bank may be premature for a credit union; a use case that is appropriate for a general insurer may be inappropriate for a securities firm. A board chair governing AI without sub-sector differentiation is governing in the wrong frame.

Sub-sector one — Tier-one commercial banks

The largest Caribbean banks have the data volumes, the operational scale, and the customer-touchpoint frequency to make AI deployment economically rational across multiple back-office functions. They also operate under the most direct supervisory scrutiny in the region. A tier-one bank in Jamaica, Trinidad, the Bahamas, or Barbados is not a small institution; many are part of regional groups with assets measured in tens of billions and operating across multiple jurisdictions. For these institutions, the question is not whether to deploy AI but where to deploy it first, in what sequence, and with what controls. The Use-Case Map below is calibrated to give them defensible answers.

Sub-sector two — Smaller commercial banks and credit unions

This sub-sector — which dominates Caribbean financial services by institutional count if not by asset size — faces a fundamentally different calculation. Smaller institutions cannot economically justify the same AI deployments as tier-one banks because the per-transaction costs of bespoke implementation do not amortise across the same volume base. But they also have a structural advantage: their member or customer relationships are more personal, and AI deployments calibrated to support rather than replace those relationships can produce material productivity gains without the supervisory exposure that comes with autonomous customer-facing AI. The smaller bank or credit union that gets this right will be doing different things from a tier-one bank, not just smaller versions of the same things.

Sub-sector three — General insurers

Caribbean insurance companies face perhaps the most concentrated near-term AI opportunity in the region. The claims process — from first notification of loss through document handling, adjuster assignment, and settlement — is highly structured, document-intensive, and produces large volumes of repetitive work that AI assistants and agents can address with relatively low risk. The same is true of policy administration. The key constraint for Caribbean insurers is that their customer base is often less digitally mature than the bank customer base, which means customer-facing AI must be deployed with stronger human-handoff disciplines than would be appropriate for retail banking.

Sub-sector four — Securities, capital markets, and asset management

The smallest of the four sub-sectors by institutional count, but the most heterogeneous in AI readiness. Securities dealers, asset managers, and pension administrators have the most data-intensive operations of any Caribbean financial services sub-sector, but they also have the highest supervisory exposure on autonomous decision-making — a securities firm using AI for trade execution or portfolio construction faces materially more regulatory risk than the same firm using AI for trade processing or client reporting. This sub-sector has the largest gap between what AI is technically capable of and what is currently appropriate to deploy, and the boards governing these firms need the most discipline in saying no to use cases that are not yet justified by the supervisory environment.

| A use case that is ready for a tier-one bank may be premature for a credit union. A use case that is appropriate for a general insurer may be inappropriate for a securities firm. Sub-sector matters. |

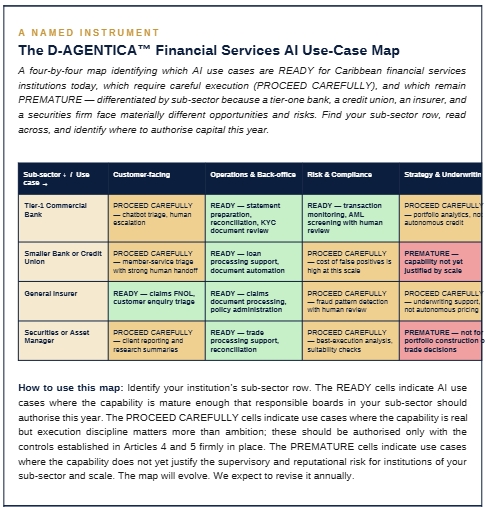

The use-case map, calibrated for Caribbean reality

With the four sub-sectors named, the question for any board becomes practical: where, in our specific sub-sector, is the capability real this year, where is execution discipline the binding constraint, and where is the capability still premature for institutions of our scale? The instrument below provides the answers, calibrated to what I currently observe in Caribbean engagements and supervisory conversations. The map will evolve — we expect to revise it annually — but the methodology of sub-sector-by-use-case differentiation will not.

Three categorisations carry across all four sub-sectors. READY indicates use cases where the capability is mature, the execution risk is manageable with the controls established in Articles 4 and 5, and responsible boards in the relevant sub-sector should authorise this year. PROCEED CAREFULLY indicates use cases where the capability is real but the execution discipline matters more than the ambition; these should be authorised only with strong governance in place, and the institution should expect to invest as much in process design and control as in the AI itself. PREMATURE indicates use cases where the capability does not yet justify the supervisory and reputational risk for institutions of the relevant sub-sector and scale; the appropriate posture is monitored deferral, not refusal in principle.

| A NAMED INSTRUMENT

The D-AGENTICA™ Financial Services AI Use-Case Map A four-by-four map identifying which AI use cases are READY for Caribbean financial services institutions today, which require careful execution (PROCEED CAREFULLY), and which remain PREMATURE — differentiated by sub-sector because a tier-one bank, a credit union, an insurer, and a securities firm face materially different opportunities and risks. Find your sub-sector row, read across, and identify where to authorise capital this year.

|

Three observations about the map are worth dwelling on, because they are the observations most likely to be missed by a board reading it quickly.

PROCEED CAREFULLY is not consolation

The largest single category in the map is PROCEED CAREFULLY — not READY, not PREMATURE. This is deliberate. The current state of Caribbean financial services AI is that most genuinely valuable use cases sit precisely in the zone where the capability is real but the execution discipline is the binding constraint. A board that interprets PROCEED CAREFULLY as ‘avoid for now’ will under-invest. A board that interprets it as ‘READY in disguise’ will over-deploy. The discipline of PROCEED CAREFULLY is reading the cell carefully, identifying what specific controls are required, and proceeding only when those controls are in place — the same discipline I named for amber cells in the Article 4 Decision Matrix.

Customer-facing AI is the most over-prescribed use case

Across all four sub-sectors, the customer-facing column tilts toward PROCEED CAREFULLY rather than READY. This reflects what I consistently observe in our engagements: customer-facing AI deployments in Caribbean financial services are the most likely to fail not because the technology does not work, but because the customer base, the regulatory exposure, and the brand risk make autonomous deployment riskier than vendor marketing suggests. Caribbean financial institutions over-investing in customer-facing chatbots are, in my observation, the largest single source of capital destruction in the regional AI conversation. Operations and back-office deployments produce materially better risk-adjusted returns and should be the priority for most institutions.

PREMATURE means ‘not yet’, not ‘never’

Two cells in the map are marked PREMATURE: autonomous strategy and underwriting at smaller banks and credit unions, and portfolio construction or trade decisions at securities and asset managers. These cells reflect current supervisory reality and current capability maturity, not a permanent judgment. Eighteen months from now, both cells may have moved to PROCEED CAREFULLY. The discipline is monitored deferral — your institution should know what would change for these cells to move, should be tracking those triggers, and should be prepared to act when they occur. PREMATURE without monitoring becomes refusal-in-principle, which is the slow path to being overtaken by competitors.

| WHAT WE OBSERVE IN CARIBBEAN FINANCIAL SERVICES AI ENGAGEMENTS

Across the financial services AI engagements our firm has supported in the past eighteen months — covering institutions in three Caribbean territories and four sub-sectors — a consistent pattern emerges. The institutions that authorise AI investment in the READY cells of their sub-sector row, defer the PREMATURE cells, and apply genuine execution discipline to the PROCEED CAREFULLY cells, deliver materially better twelve-month outcomes than institutions that pursue use cases driven by vendor marketing rather than sub-sector calibration. The methodology of sub-sector-aware prioritisation is, in our experience, more important than the specific use cases chosen — because the methodology produces a defensible audit trail that supervisors recognise as governance maturity, and the methodology produces investment decisions that are calibrated to actual capability rather than to fashion. |

Three patterns that consistently produce better outcomes

Across the Caribbean financial services AI engagements I have observed in the past eighteen months, three deployment patterns consistently produce better outcomes than the alternatives. I want to name them directly so the boards reading this article can deliberately choose them.

Pattern one — augment the back office before the front line

The institutions producing the strongest twelve-month AI outcomes are those that have authorised back-office and operations deployments first — statement preparation, reconciliation, document review, claims processing — and held customer-facing deployments back until the institution’s operating literacy with AI is mature. The reasoning is structural: back-office workflows are higher-volume, more standardised, and lower-risk per error than customer-facing workflows. An AI deployment that misclassifies a back-office document is recoverable; one that misadvises a customer about a regulated product is materially harder to recover from. Boards that authorise back-office first build the operational capability that makes customer-facing deployments succeed two years later.

Pattern two — keep the human in every consequential loop

The Caribbean financial services AI deployments I see succeeding share a specific design discipline: humans remain in the loop for every consequential decision, regardless of whether the technology could plausibly automate the decision. AI prepares the document; the relationship manager signs it. AI flags the suspicious transaction; the AML analyst confirms it. AI summarises the customer enquiry; the service representative responds to it. This is not technological timidity; it is governance design. Caribbean supervisors will judge an institution by the consequences of its decisions, not by the sophistication of its automation. An institution whose AI made a defensible decision under human oversight is in a different supervisory position from an institution whose AI made the same decision autonomously — even if the decision was identical.

Pattern three — tie every deployment to a specific operational metric

The institutions getting clear value from AI deployments are those that have committed, before deployment, to a specific operational metric the AI is meant to move — average claims handling time, statement preparation cost, reconciliation cycle time, AML alert false-positive rate. The metric is measured before the deployment to establish a baseline, measured during the deployment to validate progress, and measured at six and twelve months to confirm the gain. Institutions that deploy AI without committing to a specific metric typically discover, eighteen months later, that they cannot tell whether the deployment produced value or merely added cost. This is not a measurement problem; it is a governance problem. Boards should require the metric commitment as a precondition of deployment authorisation, and should hold management accountable for reporting against it.

Three patterns that consistently destroy capital

The mirror image of the patterns above is also worth naming. The Caribbean financial services AI deployments I see destroying the most capital are those that exhibit one or more of the following three failure modes. None is technologically novel; all are governance failures in disguise. The boards reading this article that recognise these patterns in their own institutions should treat the recognition as an early warning.

Failure one — the consultant-driven roadmap with no operational owner

A regional consulting firm presents a Caribbean financial institution with a multi-year AI transformation roadmap. The roadmap is genuinely sophisticated. The board approves the strategy. Eighteen months later, several specific deployments have been launched but no single executive within the institution has been personally accountable for any of them, the operational metrics that were supposed to move have not moved measurably, and the consulting firm’s engagement has rolled into a follow-on phase. This pattern — strategy without accountability — is, in my direct experience, the single largest source of capital destruction in Caribbean financial services AI today. The fix is unambiguous: every authorised deployment must have a named internal executive who owns the operational outcome and whose role specification includes the metric commitment. Without named accountability, strategy becomes activity, and activity does not produce results.

Failure two — the vendor-led pilot that never converts

A vendor offers a Caribbean financial institution a free or heavily-discounted pilot of an AI capability. The pilot succeeds in narrow technical terms; the institution is impressed; the vendor presents an enterprise contract. The institution signs. Twelve months later, utilisation analytics show that the enterprise deployment is being used for a small fraction of its potential, the operational metrics that justified the contract have not moved, and the renewal conversation is contentious. The fix is to require that every vendor-led pilot include, before signature, a defined enterprise scope, defined operational metrics, defined utilisation targets, and a defined exit ramp if the targets are not met. The Caribbean institutions that have applied this discipline consistently report better commercial outcomes and stronger long-term vendor relationships than those that have not.

Failure three — the technology-team-driven programme with no business sponsor

A Caribbean financial institution’s technology team identifies AI as a strategic priority and builds a programme around it. The technology team is competent and well-intentioned. But no business unit head has personally championed the programme; no specific business outcome has been agreed; no operational metric has been committed. The programme produces capability — platforms, models, infrastructure — without producing business results. Eighteen months later, the programme is technically sophisticated and commercially silent. The fix is to require that every AI programme have a named business sponsor at the level of business unit head or above, with personal accountability for the business outcome the programme is meant to produce. Technology cannot succeed without business ownership; this has been true of every technology investment for forty years, and is no less true of AI today.

Looking across these three failure modes together, a single underlying pattern becomes visible: each is a governance failure that presents itself as a technology question. The consultant-led roadmap looks like a strategy problem; it is in fact an accountability problem. The vendor-led pilot looks like a procurement question; it is in fact a contracting discipline problem. The technology-team-driven programme looks like a structural choice; it is in fact a sponsorship problem. None of the three is solved by buying better technology, hiring better consultants, or selecting different vendors. All three are solved by the same governance disciplines a well-run Caribbean institution applies to every other strategic investment: named accountability, written commitments, and periodic review. The boards reading this article that recognise these patterns in their own institutions should treat the recognition not as criticism but as opportunity — the patterns are correctable, and the corrections are inexpensive relative to the capital they preserve.

| A CARIBBEAN FINANCIAL SERVICES PATTERN WE OBSERVE REPEATEDLY

Across the financial services AI engagements we have reviewed for clients in the past year, the institutions whose programmes were producing measurable business outcomes shared three structural features: a named business sponsor for every authorised initiative, a specific operational metric committed in writing before deployment, and a quarterly board-level review of progress against that metric. The institutions whose programmes were not producing measurable outcomes typically lacked all three. The technology was rarely the differentiator. The governance discipline almost always was. |

What this article has established, and what comes next

This article has done four things. It has named the four sub-sectors of Caribbean financial services and made the case that a single ‘financial services’ frame is too coarse for the AI conversation. It has introduced the D-AGENTICA™ Financial Services AI Use-Case Map as the named instrument for this article — the sixth in the series — differentiating sixteen specific use case scenarios as READY, PROCEED CAREFULLY, or PREMATURE. It has named the three deployment patterns I see consistently producing better outcomes in our region. And it has named the three failure modes I see consistently destroying capital, so that boards can recognise them early.

Taken together with the five instruments from the previous articles — the Three-Question Board Diagnostic, the Agentic Vendor Assessment, the SME AI Sequencing Framework, the Data Sovereignty Decision Matrix, and the Caribbean Regulatory Readiness Self-Assessment — the Use-Case Map gives Caribbean boards a complete instrument library for governing AI in financial services. The first instrument tells you where you stand. The second distinguishes capability from marketing. The third sequences the spend at SME scale. The fourth classifies the data exposure. The fifth assesses the regulatory readiness. The sixth identifies what to authorise this year, calibrated to your sub-sector. An institution that applies all six in their proper place is governed in a way that meets the supervisory expectations currently signalled in our region and the ones likely to emerge over the coming thirty-six months.

Next article, Article 7, addresses the second domain of Act III: the Caribbean workforce transition. Where this article addressed AI as an institutional capability, Article 7 addresses AI as a force reshaping the work itself — the specific roles that change, the specific roles that disappear, the specific roles that emerge, and the institutional and human-capital responsibility Caribbean leaders carry in the next thirty-six months. The named instrument in that article will be the D-AGENTICA™ Caribbean Workforce Transition Map — a structured way for boards and executive teams to engage with workforce planning in an AI-augmented operating model.

One reflection to carry into your next strategy session. The Caribbean financial services boards that will be best positioned in 2028 are not the boards with the longest AI roadmaps. They are the boards whose chairs can interrogate the priority list with a defensible methodology, whose institutions have moved decisively in the READY cells of their sub-sector, who have applied real execution discipline to the PROCEED CAREFULLY cells, and who have monitored — not refused — the PREMATURE ones. The boards doing this work in 2026 are the boards whose institutions will compound the advantage through 2030. The boards waiting for clarity will inherit the rules that the first group helped to shape.

A second reflection, specific to the supervisory environment Article 5 named. The Caribbean financial supervisor of 2028 will not arrive at your institution and ask whether you used AI well. They will ask three more specific questions. Did your board take AI seriously as a governance matter, with written evidence? Did your institution distinguish use cases by capability maturity and sub-sector appropriateness, with documented methodology? Did your authorised deployments have named accountable executives and committed metrics, with audit-trail evidence? An institution that can produce yes to those three questions, with documentary support, will be well positioned regardless of the specific use cases it chose. An institution that cannot will face supervisory pressure regardless of how technically sophisticated its deployments became. The Use-Case Map in this article is not the answer the supervisor will ask for; the discipline of having applied something like it is.

| FOR THE BOARD AGENDA

This article has specified, with sub-sector calibration, what Caribbean financial services boards should authorise this year on AI. A board chair or audit committee chair reading this article has earned the right to ask their leadership team one specific question and to propose one specific decision that will materially improve the quality of AI investment over the next twelve months. THE QUESTION Within sixty days, can management produce an AI investment plan organised around our specific sub-sector row of the D-AGENTICA™ Financial Services AI Use-Case Map — with named business sponsors, committed operational metrics, and quarterly board-level review milestones for every authorised deployment, and explicit monitoring criteria for the PREMATURE cells we are choosing to defer? THE DECISION That the leadership team will revise the institution’s AI investment plan within sixty days to align with the Use-Case Map, will name a single accountable executive sponsor for each authorised deployment, will commit to specific operational metrics for each, and will report quarterly to the board on progress against those metrics for the duration of each deployment. |

| THE CARIBBEAN AI ADOPTION IMPERATIVE

A 12-Article Series from Dawgen Global NEXT IN THIS SERIES Article 07 — The Caribbean Workforce Transition How AI is reshaping the work itself — and the institutional responsibility leaders carry MEASURE YOUR ORGANISATION’S AI READINESS Request the free D-AGENTICA™ AI Maturity Self-Assessment!! Email us :[email protected] |

About Dawgen Global

“Embrace BIG FIRM capabilities without the big firm price at Dawgen Global, your committed partner in carving a pathway to continual progress in the vibrant Caribbean region. Our integrated, multidisciplinary approach is finely tuned to address the unique intricacies and lucrative prospects that the region has to offer. Offering a rich array of services, including audit, accounting, tax, IT, HR, risk management, and more, we facilitate smarter and more effective decisions that set the stage for unprecedented triumphs. Let’s collaborate and craft a future where every decision is a steppingstone to greater success. Reach out to explore a partnership that promises not just growth but a future beaming with opportunities and achievements.

Email: [email protected]

Email: [email protected]  Visit: Dawgen Global Website

Visit: Dawgen Global Website

WhatsApp Global Number : +1 555-795-9071

WhatsApp Global Number : +1 555-795-9071

Caribbean Office: +1876-6655926 / 876-9293670/876-9265210  WhatsApp Global: +1 5557959071

WhatsApp Global: +1 5557959071

USA Office: 855-354-2447

Join hands with Dawgen Global. Together, let’s venture into a future brimming with opportunities and achievements